Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

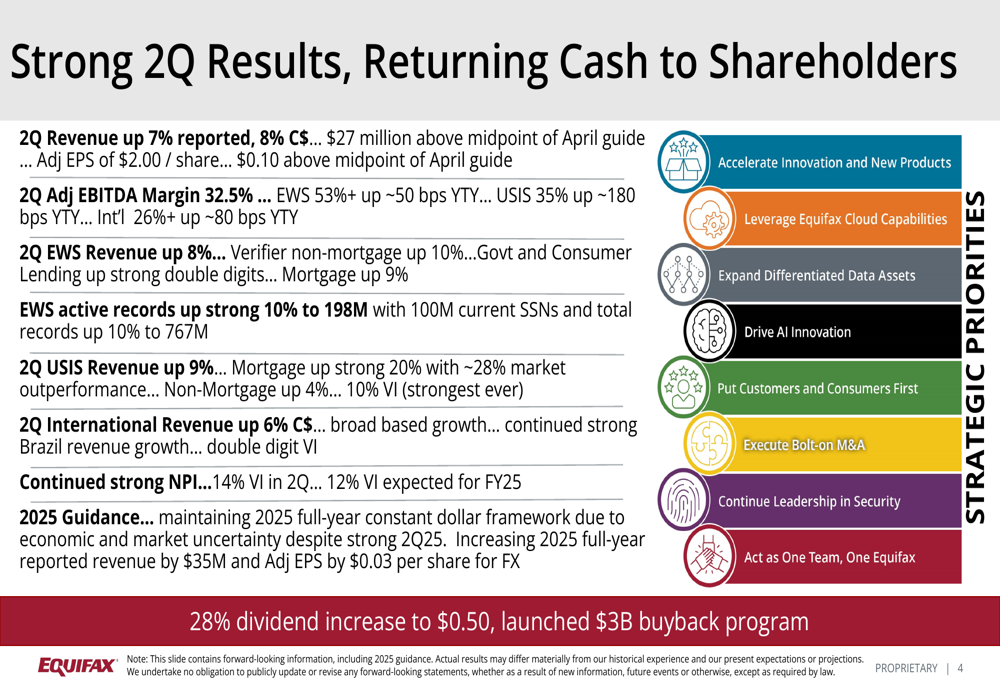

Equifax Inc . (NYSE:EFX) released its second quarter 2025 earnings presentation on July 22, showing accelerated growth across all business segments. The company reported revenue growth of 7% (8% in constant currency), reaching $27 million above the midpoint of guidance. The stock responded positively in pre-market trading, rising 2.45% to $266, building on its recent momentum after closing at $259.64 the previous day.

The results demonstrate continued improvement from Q1 2025, when the company reported 4% year-over-year revenue growth. This acceleration comes despite persistent challenges in the mortgage market, where interest rates remain elevated.

As shown in the following comprehensive overview of Q2 results:

Quarterly Performance Highlights

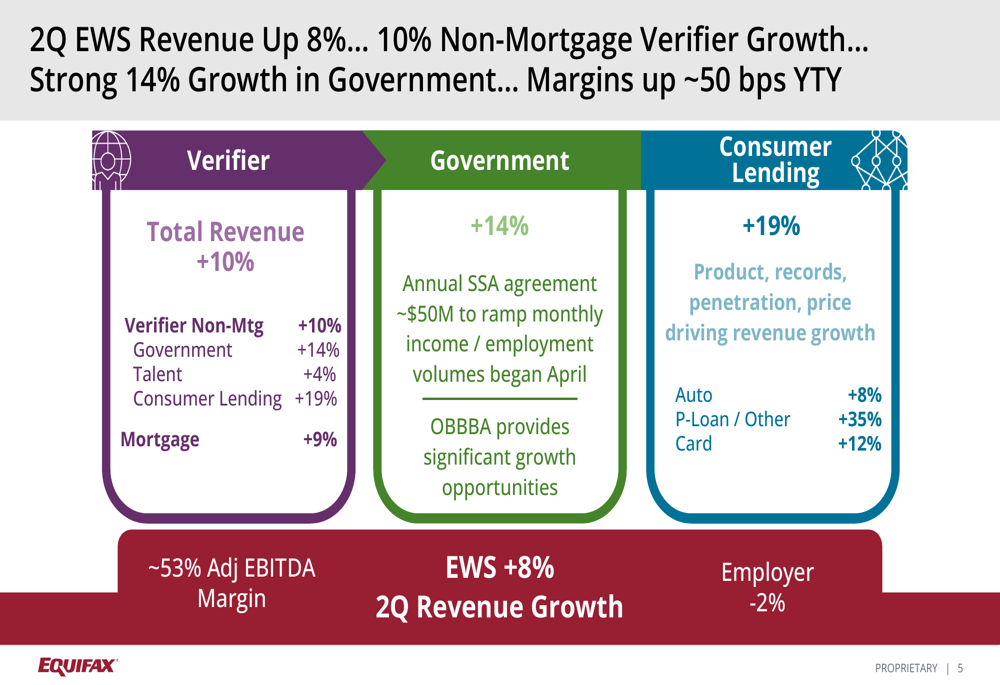

Equifax’s Workforce Solutions (EWS) segment led performance with 8% revenue growth, driven by Verifier non-mortgage services (+10%), government services (+14%), and consumer lending (+19%). The mortgage component of EWS also performed well, growing 9% despite challenging market conditions.

The breakdown of EWS revenue growth illustrates the segment’s diverse growth drivers:

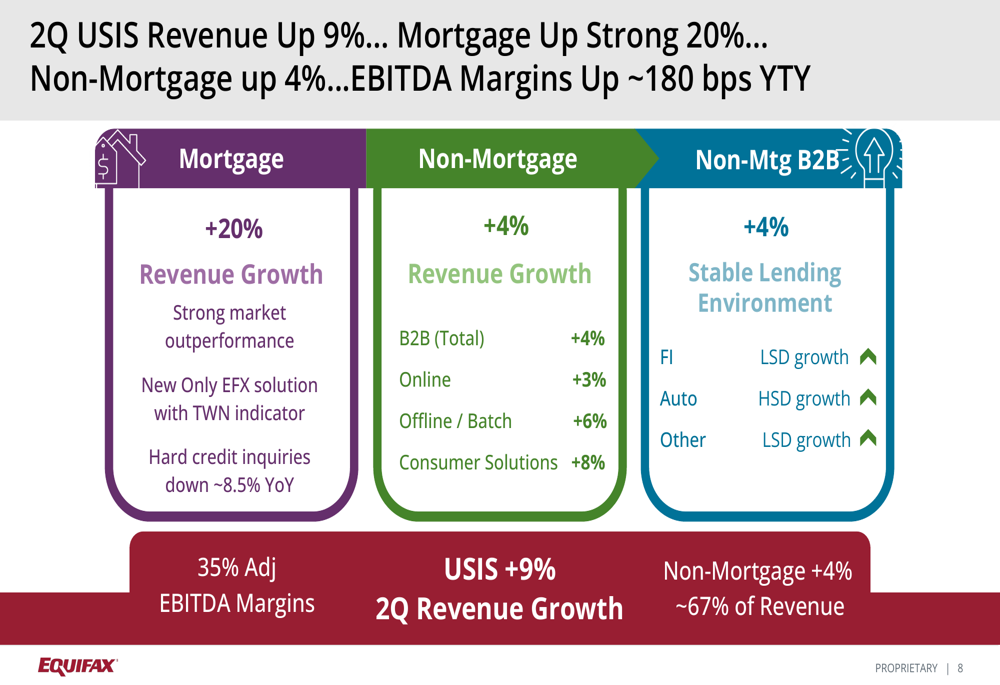

The U.S. Information Solutions (USIS) segment delivered an impressive 9% revenue increase, with mortgage services surging 20% despite industry headwinds. Non-mortgage services grew at a more modest 4%, with financial institutions showing low single-digit growth and automotive in the high single digits. The segment maintained strong adjusted EBITDA margins of over 35%.

The USIS revenue breakdown shows the significant contribution from mortgage services:

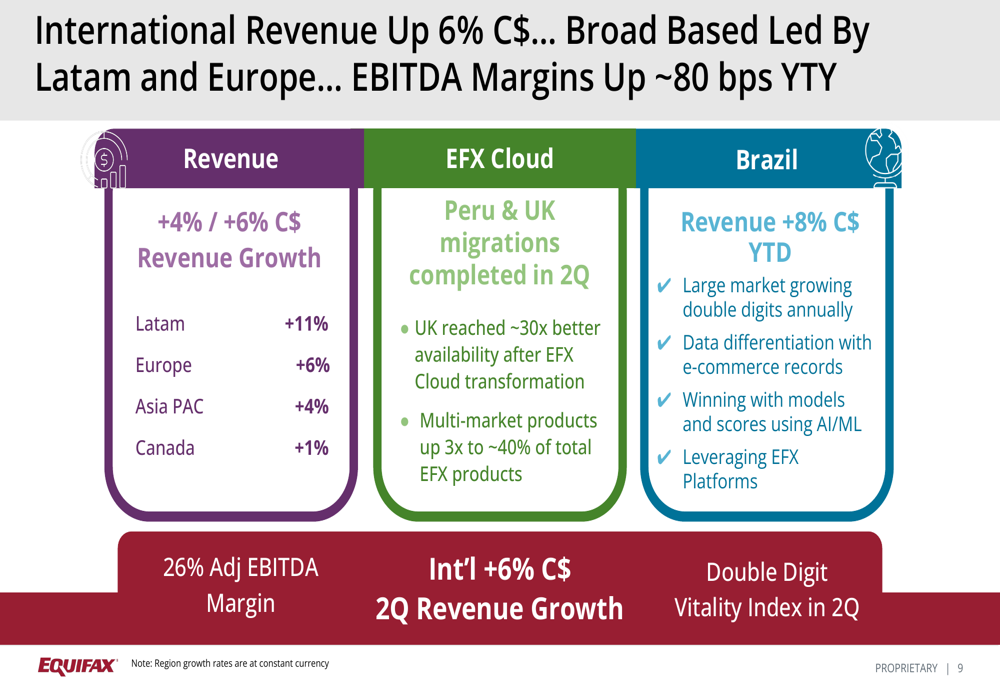

International operations posted 6% revenue growth in constant currency, with particularly strong performance in Latin America (+11%) and Europe (+6%). The company completed cloud migrations in Peru and the UK during the quarter, with the UK achieving approximately 30 times better availability after its cloud transformation.

The international revenue growth across regions is visualized here:

Strategic Initiatives

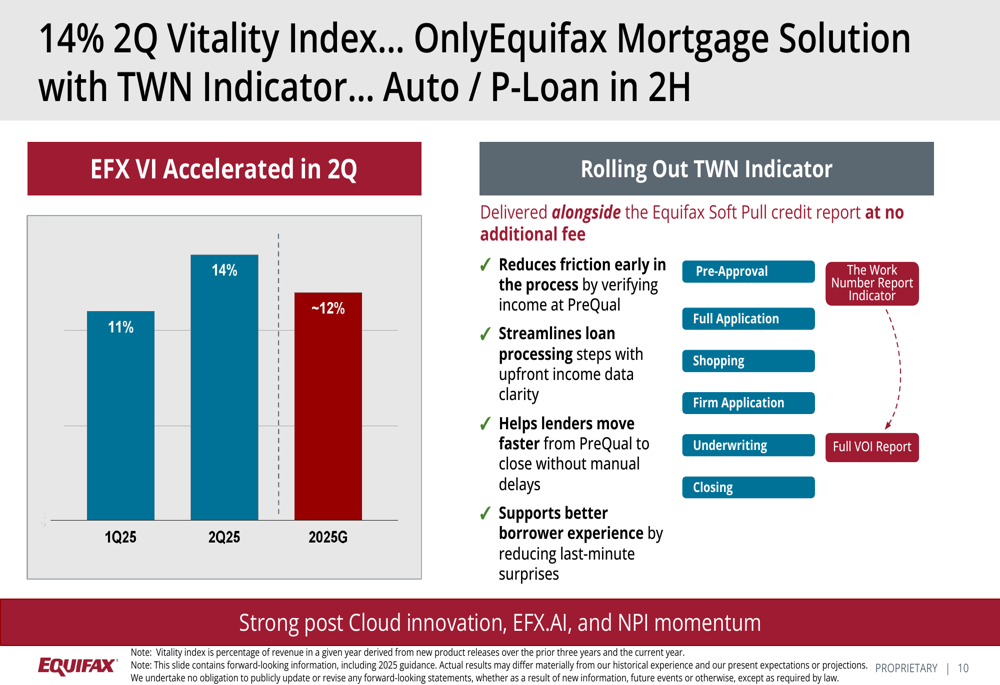

Equifax continues to expand its data assets, particularly The Work Number (TWN), which shows significant growth potential. The company added four new partners year-to-date, building on ten additions in the second half of 2024. Active records increased 10% year-over-year to 198 million, with total records growing 10% to 767 million.

The company’s innovation metrics show improvement, with the Vitality Index (percentage of revenue from products introduced in the last three years) increasing from 11% in Q1 2025 to 14% in Q2. This acceleration reflects successful product launches, including the TWN Indicator, which reduces friction in loan processing.

The following chart illustrates the improving Vitality Index:

Forward-Looking Statements

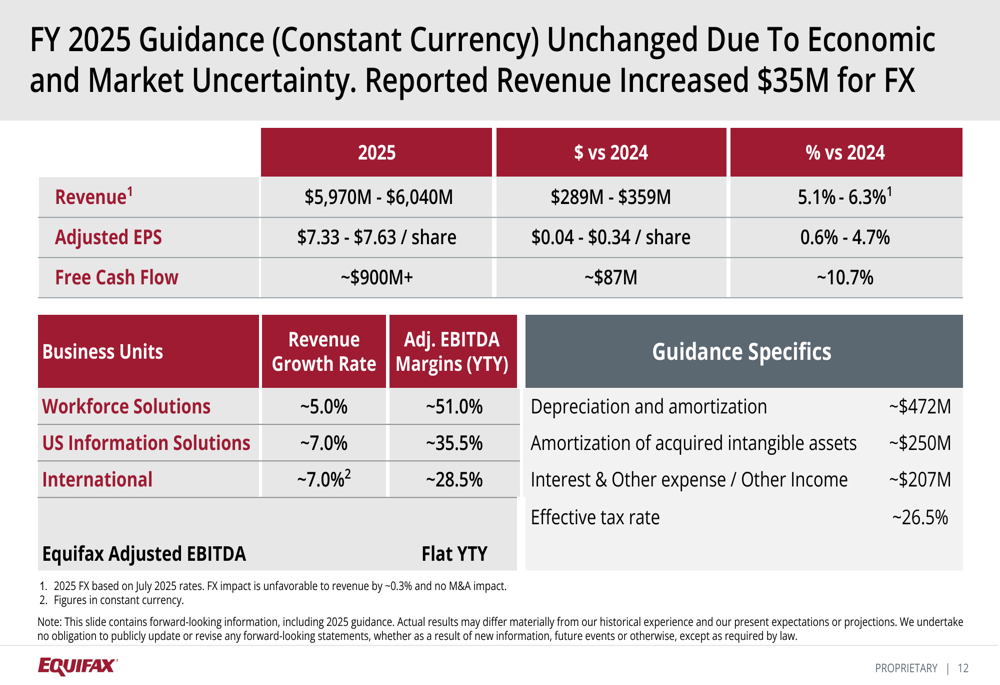

Equifax maintained its full-year 2025 guidance while increasing reported revenue by $35 million and adjusted EPS by $0.03 to account for foreign exchange impacts. The company expects full-year revenue between $5,970 million and $6,040 million, with adjusted EPS of $7.33 to $7.63 per share. Free cash flow is projected at approximately $900 million or higher, with cash conversion exceeding 95%.

For the third quarter of 2025, Equifax forecasts revenue between $1,505 million and $1,535 million, with adjusted EPS ranging from $1.87 to $1.97 per share.

The detailed full-year guidance is presented here:

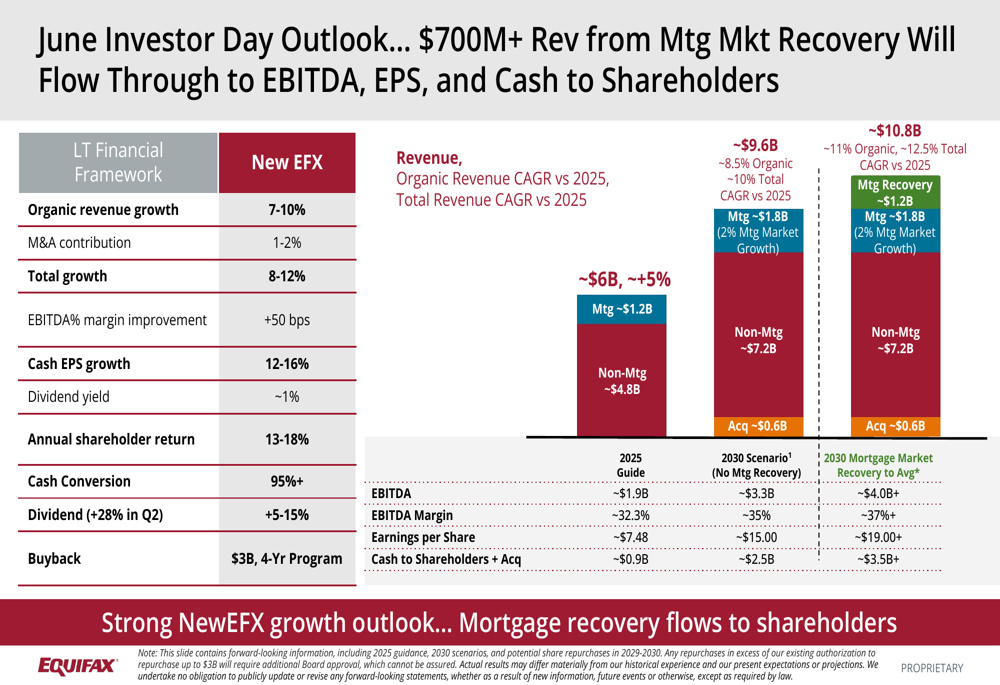

Looking further ahead, Equifax presented its long-term outlook from its June Investor Day, projecting significant growth through 2030. The company anticipates continued revenue expansion driven by organic growth and strategic acquisitions, with additional upside potential from mortgage market recovery.

The long-term outlook is visualized in this forward-looking projection:

Shareholder Returns

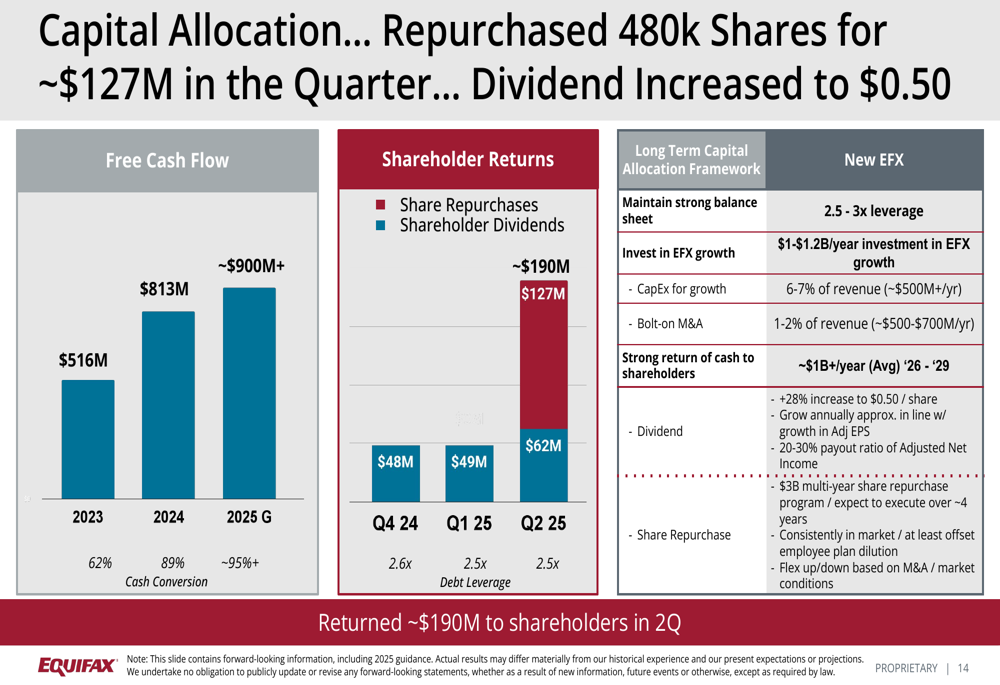

In a significant move to return cash to shareholders, Equifax announced a 28% dividend increase to $0.50 per share and a $3 billion share repurchase program expected to be executed over four years. The company began repurchases in Q2 2025, buying back 480,000 shares for approximately $127 million.

These shareholder returns are supported by Equifax’s improving free cash flow, which has grown from $516 million in 2023 to a projected $900+ million in 2025. The company’s capital allocation framework balances investments in growth, bolt-on acquisitions, and shareholder returns.

The following chart illustrates the company’s improving free cash flow and capital allocation strategy:

Equifax’s strong Q2 performance and shareholder-friendly initiatives reflect management’s confidence in the company’s long-term growth trajectory, even as it navigates varying conditions across its diverse business segments. With cloud transformation substantially complete and data assets continuing to expand, the company appears well-positioned to execute on its strategic priorities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.