Fed Governor Adriana Kugler to resign

Introduction & Market Context

Equinix (NASDAQ:EQIX) held its Q2 2025 earnings conference call on July 30, 2025, showcasing solid financial performance driven by strong monthly recurring revenue (MRR) growth and improved operating leverage. The data center giant continues to expand its global footprint while maintaining leadership in interconnection services, a critical component of its value proposition.

Following a strong Q1 2025 where the company raised guidance amid robust AI-related demand, Equinix’s Q2 presentation demonstrates continued execution of its strategic initiatives across global markets. The company’s diversified revenue streams and strategic capital investments position it well in the competitive digital infrastructure landscape.

Quarterly Performance Highlights

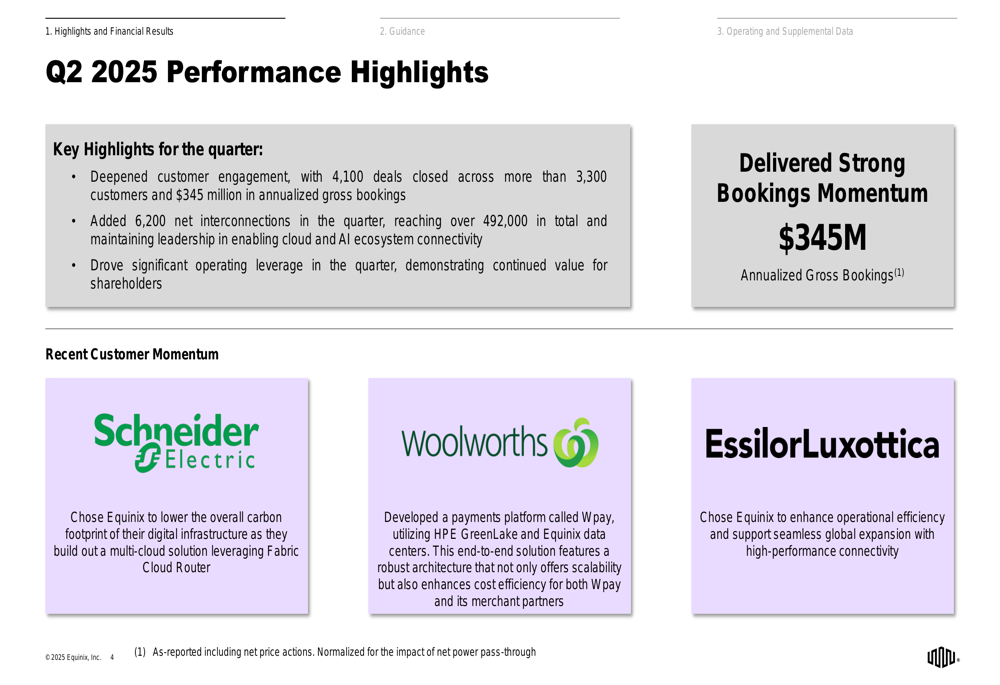

Equinix reported significant customer engagement in Q2 2025, closing 4,100 deals across more than 3,300 customers, resulting in $345 million in annualized gross bookings. The company’s interconnection business continues to thrive, with 6,200 net interconnections added during the quarter, bringing the total to over 492,000.

As shown in the following performance highlights slide, Equinix is maintaining its leadership in enabling cloud and AI ecosystem connectivity while driving significant operating leverage:

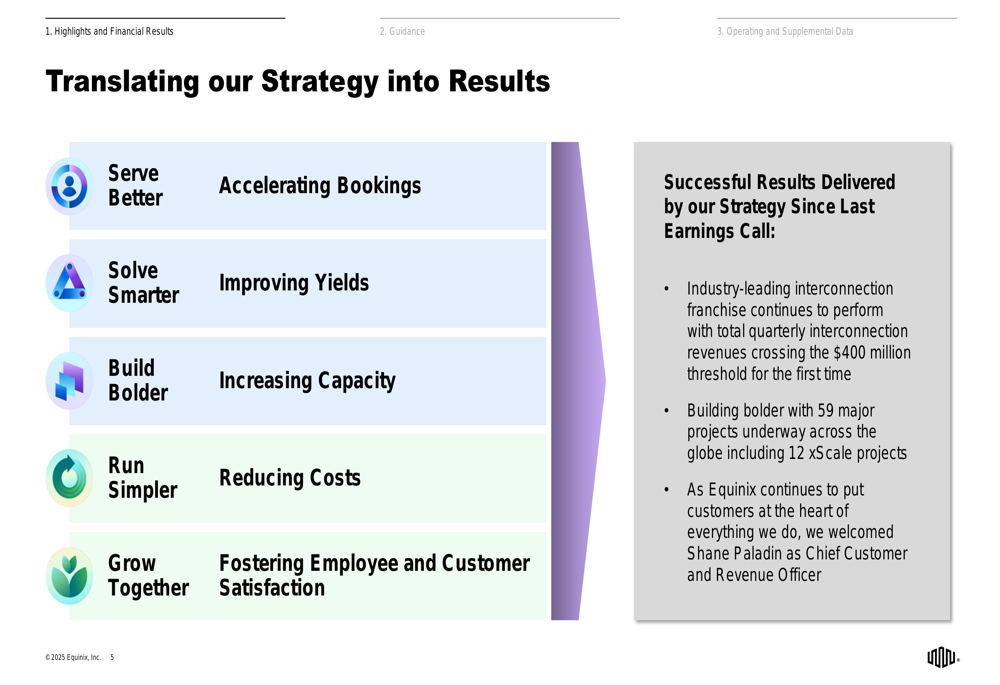

A notable milestone was achieved in Q2 as quarterly interconnection revenues crossed the $400 million threshold for the first time, underscoring the strength of Equinix’s interconnection franchise. This achievement aligns with the company’s strategic pillars, which focus on serving customers better, solving problems smarter, building bolder, running operations simpler, and growing together.

The following slide illustrates how Equinix is translating its strategy into tangible results:

Detailed Financial Analysis

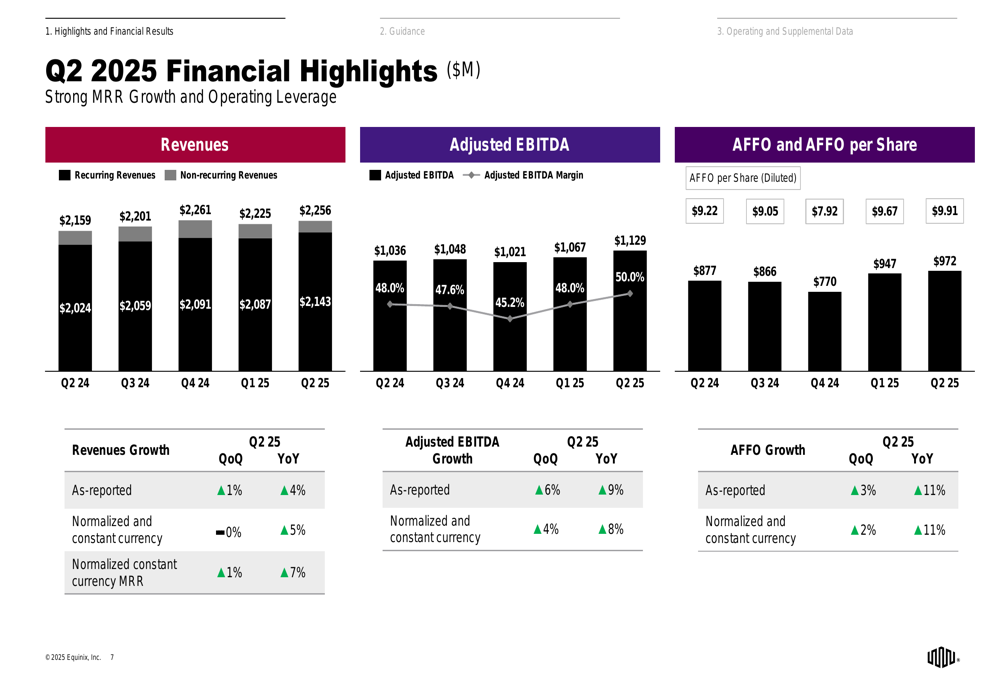

Equinix reported total revenues of $2,256 million for Q2 2025, representing a 4% year-over-year increase on an as-reported basis and 5% growth on a normalized constant currency basis. More importantly, normalized constant currency MRR grew 7% year-over-year, indicating strong underlying business momentum.

The company demonstrated improved profitability with Adjusted EBITDA of $1,129 million, growing 9% year-over-year as-reported and 8% on a normalized constant currency basis. AFFO per share reached $9.91, an 11% increase year-over-year on both as-reported and normalized constant currency bases.

The following financial highlights slide provides a comprehensive overview of Equinix’s Q2 2025 performance:

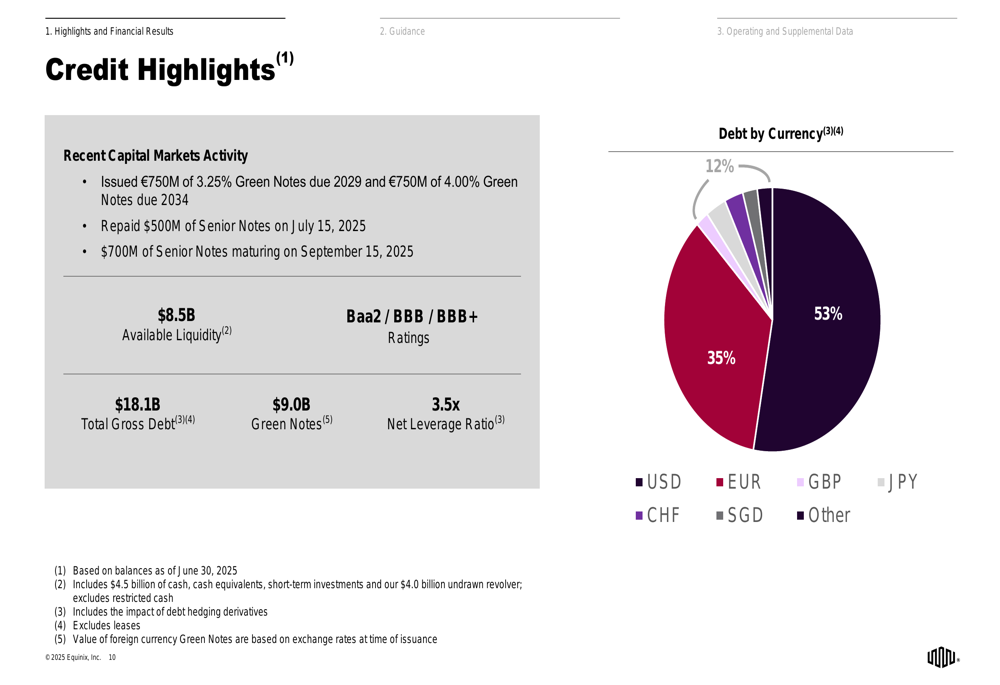

From a credit perspective, Equinix maintains a strong financial position with $8.5 billion in available liquidity and a net leverage ratio of 3.5x. The company recently issued €750 million of 3.25% Green Notes due 2029 and €750 million of 4.00% Green Notes due 2034, bringing its total green notes to $9.0 billion. Equinix also repaid $500 million of Senior Notes on July 15, 2025, with another $700 million maturing on September 15, 2025.

The following credit highlights slide details the company’s debt structure and recent capital markets activity:

Strategic Initiatives & Capital Allocation

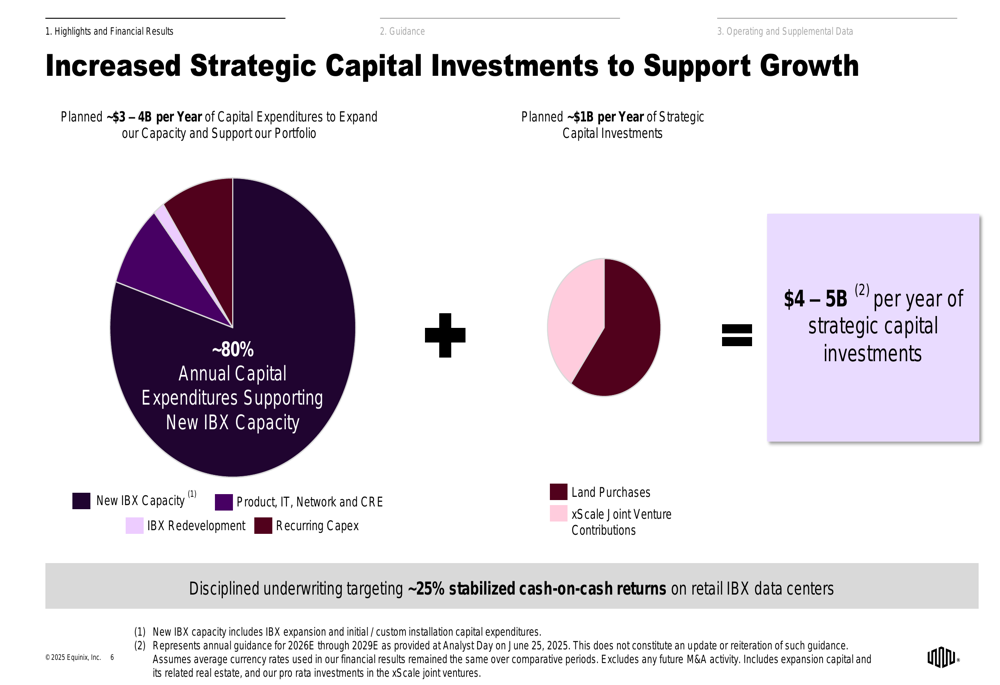

Equinix continues to invest strategically in expanding its global footprint, with approximately $3-4 billion per year allocated to capital expenditures for new capacity and portfolio support. An additional $1 billion per year is directed toward strategic capital investments, including land purchases and xScale joint venture contributions.

The company’s disciplined underwriting approach targets approximately 25% stabilized cash-on-cash returns on retail IBX data centers, as illustrated in the following capital investment strategy slide:

For Q2 2025, Equinix reported total capital expenditures of $989 million, with $934 million classified as non-recurring (primarily for expansion) and $55 million as recurring. Major retail project openings during the quarter included facilities in Chicago, Dallas, Salalah, Toronto, and Washington, D.C.

The detailed capital expenditures breakdown shows the company’s continued focus on expansion:

Equinix’s stabilized data centers continue to deliver strong returns, with 189 stabilized IBX facilities (out of 248 total) collectively operating at 82% utilization. These stabilized assets generated 3% year-over-year revenue growth on a constant currency basis and delivered a 69% Cash Gross Profit Margin, resulting in 26% annual Cash Gross Profit on Gross PP&E investment.

The following slide illustrates the performance of Equinix’s stabilized data center portfolio:

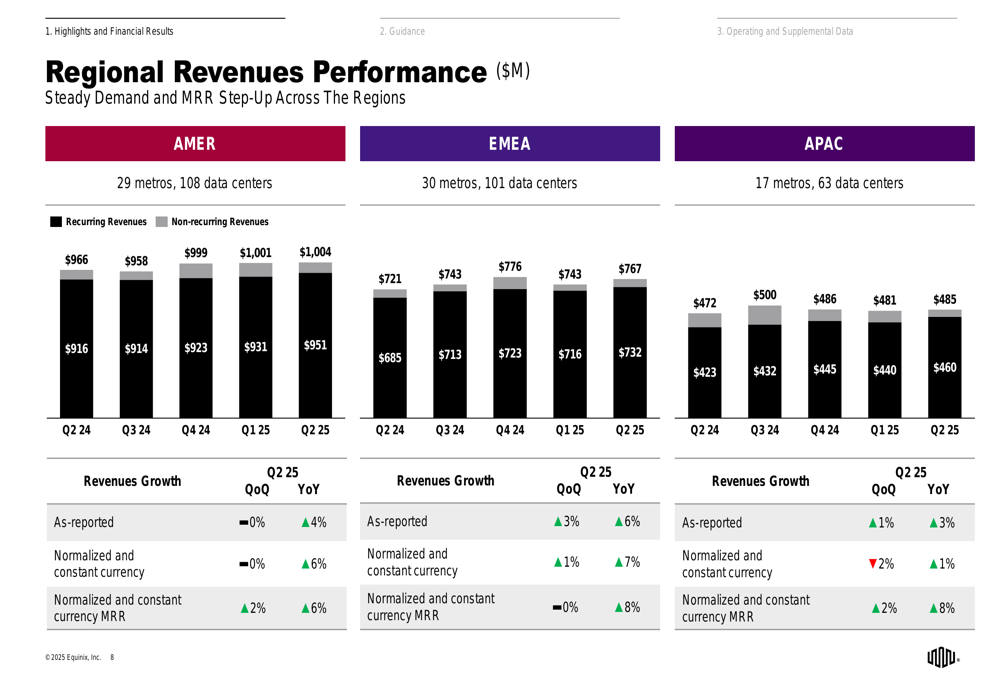

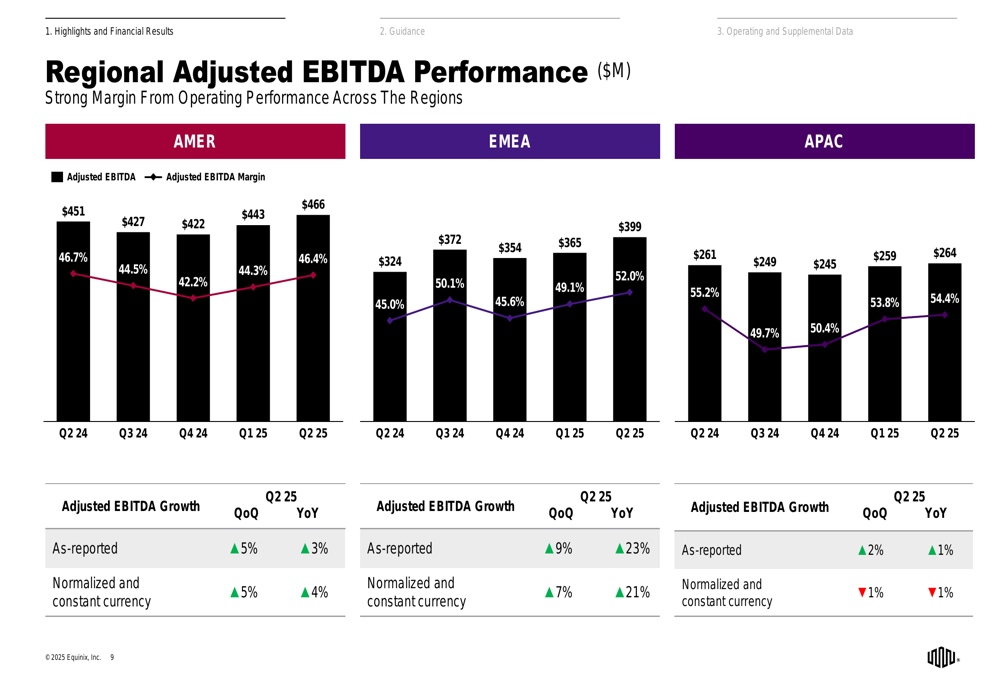

Regional Performance

Equinix’s global operations are divided into three regions: Americas (AMER), Europe, Middle East and Africa (EMEA), and Asia-Pacific (APAC). Each region showed distinct performance characteristics in Q2 2025.

The Americas region generated $1,004 million in revenues across 29 metros and 108 data centers. Revenue growth was 4% year-over-year as-reported and 6% on a normalized constant currency basis. The region’s Adjusted EBITDA was $466 million with a margin of 46.4%.

EMEA delivered the strongest performance with $732 million in revenues across 30 metros and 101 data centers. Revenue growth reached 6% year-over-year as-reported and 7% on a normalized constant currency basis. The region’s Adjusted EBITDA was $399 million with an impressive margin of 52.0%, showing 23% year-over-year growth as-reported.

The Asia-Pacific region generated $455 million in revenues across 17 metros and 63 data centers. Revenue growth was more modest at 3% year-over-year as-reported and 1% on a normalized constant currency basis. The region’s Adjusted EBITDA was $264 million with the highest margin at 54.4%.

The following slides provide detailed breakdowns of regional revenue and Adjusted EBITDA performance:

Forward-Looking Statements

While Equinix’s Q2 2025 presentation doesn’t explicitly provide updated guidance figures, the company’s strategic investments and expansion projects suggest confidence in continued growth. With 59 major projects underway globally, including 12 xScale projects, Equinix is positioning itself for future capacity demands.

The company’s focus on operating leverage and strategic capital allocation indicates a balanced approach to growth and profitability. The appointment of Shane Paladin as Chief Customer and Revenue Officer also signals Equinix’s commitment to enhancing its customer engagement and revenue generation capabilities.

Based on the Q1 2025 earnings call, Equinix had previously raised its full-year revenue guidance to reflect a growth range of 7-8%, with adjusted EBITDA margins expected to reach approximately 49%. The Q2 results appear to be tracking in line with these expectations, particularly with the strong MRR growth and improved operating leverage highlighted in the presentation.

As Equinix continues to execute its strategy across global markets, investors should monitor the company’s ability to maintain pricing power, manage capital expenditures efficiently, and capitalize on emerging opportunities in AI and cloud infrastructure.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.