Gold prices briefly hit record high over $3,500/oz on fiscal, tariff concerns

Introduction & Market Context

Erste Group Bank presented its Q2 2025 financial results on August 1, 2025, showcasing strong performance across key metrics. The Vienna-based banking group, which maintains a commanding presence across Central and Eastern Europe, reported significant profit growth and upgraded several aspects of its full-year guidance.

The presentation, delivered by CEO Peter Bosek, CFO Stefan Dörfler, and CRO Alexandra Habeler-Drabek, highlighted the bank’s "strong business performance and fast capital build" amid a generally favorable economic environment in its core markets.

Quarterly Performance Highlights

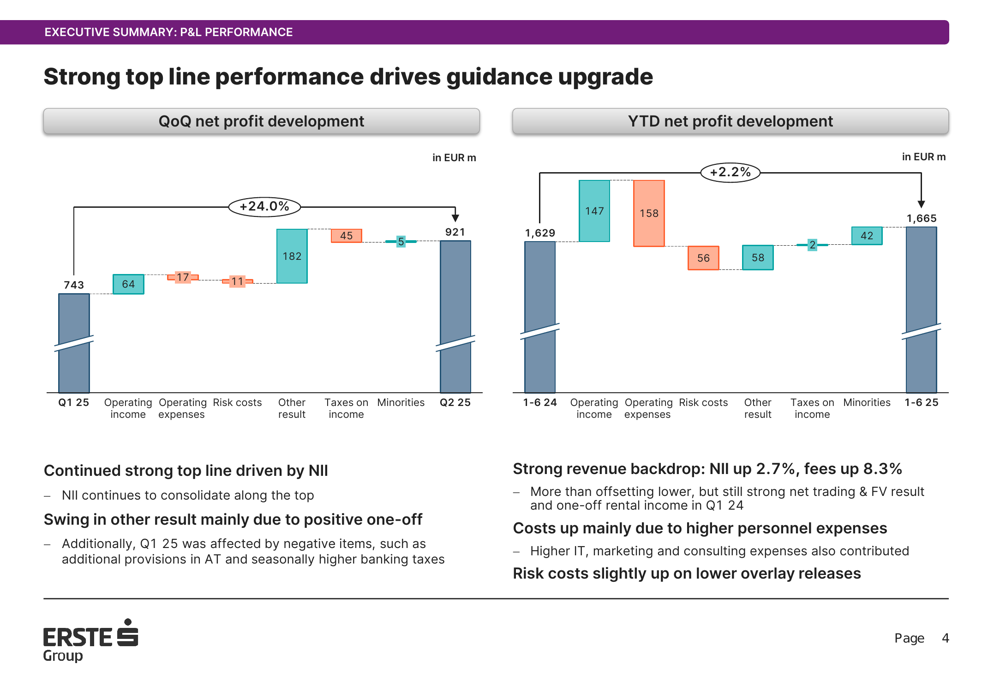

Erste Group reported a Q2 2025 net profit of EUR 921 million, representing a substantial 24.0% increase from EUR 743 million in Q1 2025. Year-to-date net profit reached EUR 1,665 million, up 2.2% compared to the same period last year.

The strong performance was primarily driven by robust net interest income and fee growth, with the bank noting that "NII continues to consolidate along the top" despite slight margin compression.

As shown in the following chart of quarterly profit development:

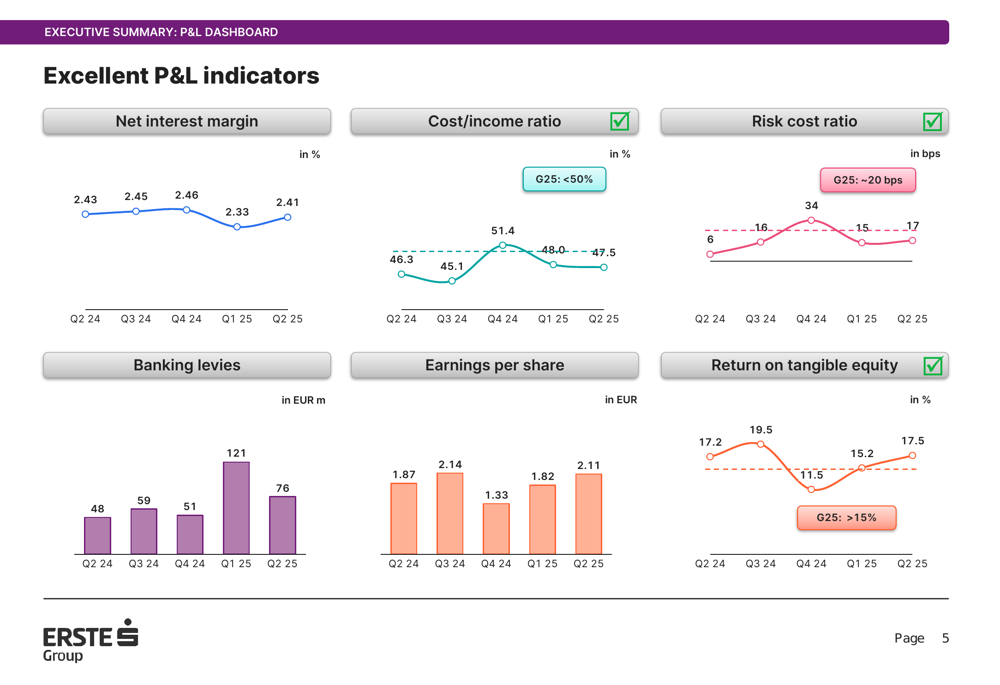

Key performance indicators remained excellent, with the net interest margin at 2.41% in Q2 2025, only slightly below the 2.43% recorded in Q2 2024. The cost/income ratio remained well-managed, tracking toward the bank’s 2025 target of below 50%.

The following chart illustrates these and other key P&L indicators:

Net fee and commission income consolidated near record levels, with the bank reporting that fees were up 8.3% year-over-year. This growth was supported by strong performance in the Group Markets business, which is running ahead of 2024 results, and continued growth in asset management despite market volatility.

Operating expenses increased, primarily due to higher personnel costs, with the bank maintaining its 2025 guidance of approximately 5% cost growth. Despite this increase, the strong revenue backdrop enabled Erste Group to maintain favorable operating efficiency.

Balance Sheet & Capital Position

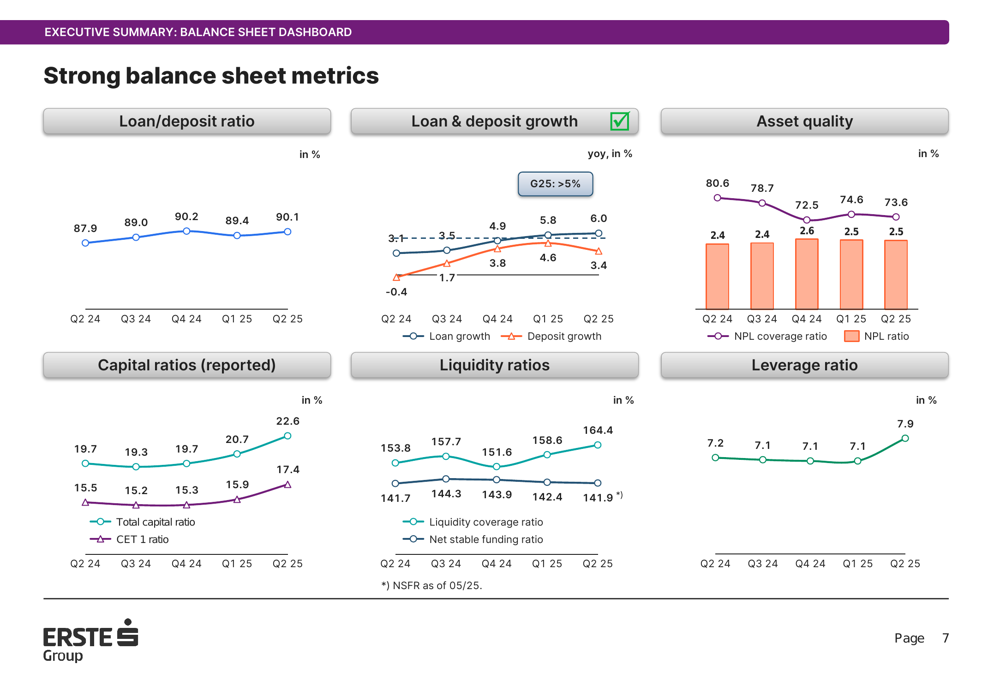

Erste Group reported well-balanced customer volume growth, with loans up 2.7% year-to-date and deposits increasing by 2.8%. The loan-to-deposit ratio stood at 90.1% in Q2 2025, up from 87.9% in Q2 2024, indicating efficient balance sheet utilization while maintaining strong liquidity.

The following chart shows the bank’s strong balance sheet metrics:

Asset quality remained strong across the bank’s footprint, with the non-performing loan (NPL) ratio and coverage ratio both at healthy levels. Risk costs were moderate year-to-date, prompting the bank to upgrade its 2025 risk cost guidance to approximately 20 basis points.

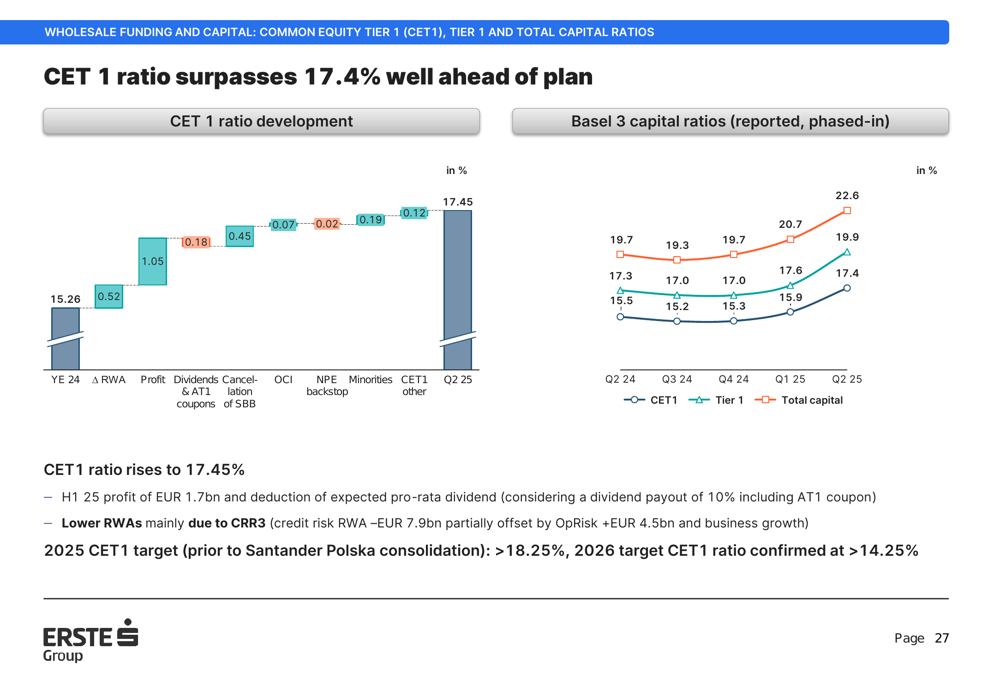

One of the most impressive aspects of Erste Group’s performance was its capital position. The Common Equity Tier 1 (CET1) ratio rose to 17.45%, reflecting fast capital build and measured risk-weighted asset inflation. The bank upgraded its 2025 CET1 target to above 18.25% (prior to Santander (BME:SAN) Polska consolidation), while confirming its 2026 target of above 14.25%.

The following chart illustrates the development of the bank’s capital ratios:

Strategic Initiatives

Erste Group continued to make progress on its digital banking initiatives, with its George platform reaching 9 million monthly active users. This digital growth supports the bank’s strong retail business momentum, with improvements in housing finance volumes across the group and growth in consumer finance.

The bank’s geographic footprint spans several Central and Eastern European countries, with particularly strong customer bases in the Czech Republic (4.6 million customers) and Austria (4.3 million customers). This diversification provides stability and multiple growth avenues.

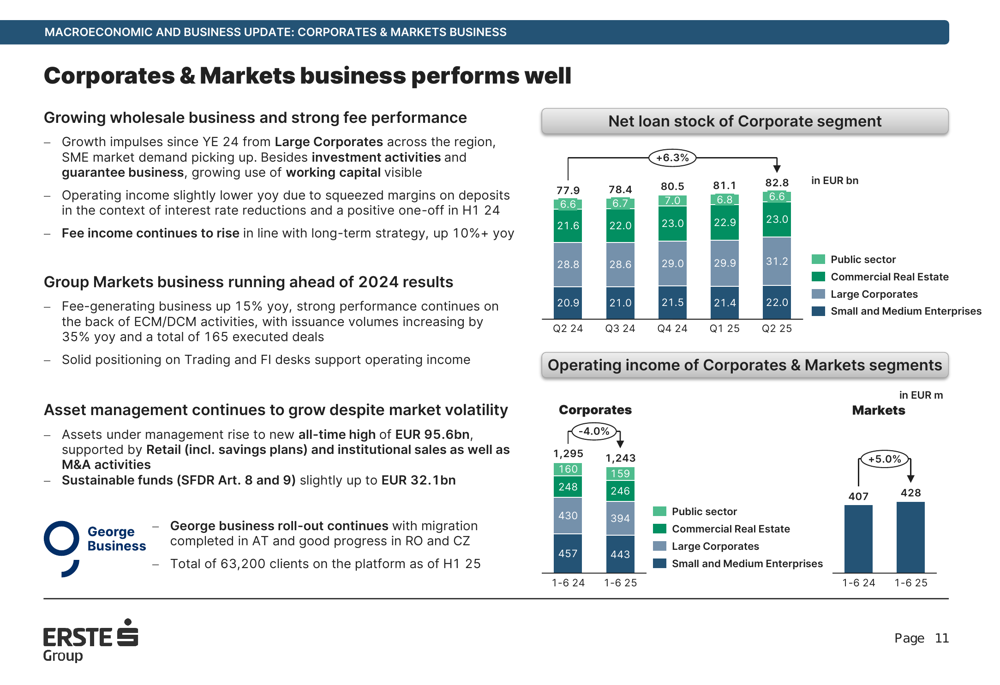

The corporate and markets segments also showed strong performance, with growth in wholesale business and strong fee income. The following chart illustrates this performance:

Forward-Looking Statements

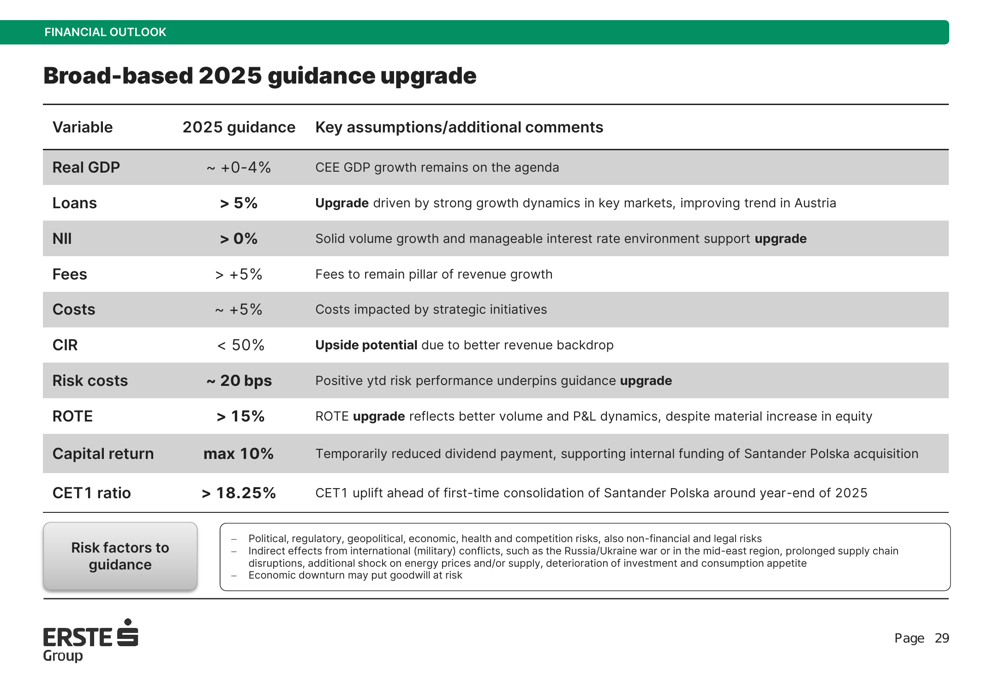

Based on its strong year-to-date performance, Erste Group upgraded several aspects of its 2025 guidance. The bank now expects:

- Loan growth above 5% (upgraded)

- Net interest income growth above 0% (upgraded)

- Fee income growth above 5% (confirmed)

- Cost growth of approximately 5% (maintained)

- Cost/income ratio below 50% (confirmed)

- Risk costs of approximately 20 basis points (upgraded)

- Return on tangible equity above 15% (upgraded)

- CET1 ratio above 18.25% prior to Santander Polska consolidation (upgraded)

The following table provides a comprehensive overview of the bank’s financial outlook:

The bank noted that its outlook is subject to certain risk factors, including potential deterioration in the macroeconomic environment, geopolitical tensions, and regulatory changes. However, the overall tone of the presentation was confident, supported by strong performance metrics across multiple dimensions of the business.

Erste Group’s commanding market shares across the CEE region, favorable deposit mix, and strong capital position provide a solid foundation for continued performance in line with its upgraded guidance. The bank’s sustainability strategy, centered on green transition and social inclusion, also positions it well for long-term growth in an increasingly ESG-focused market environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.