Moody’s upgrades Agnico Eagle’s rating to A3 on debt reduction

Essential Utilities Inc. (NYSE:WTRG) reported robust second quarter 2025 results, with earnings per share increasing 35.7% year-over-year to $0.38, according to the company’s presentation released on August 1, 2025. The water and natural gas utility reaffirmed its full-year EPS guidance of $2.07-$2.11 while highlighting its ongoing infrastructure investments and acquisition strategy.

The company’s stock closed at $36.80 on August 1, up 2.55% for the day, though still below its 52-week high of $41.78.

Quarterly Performance Highlights

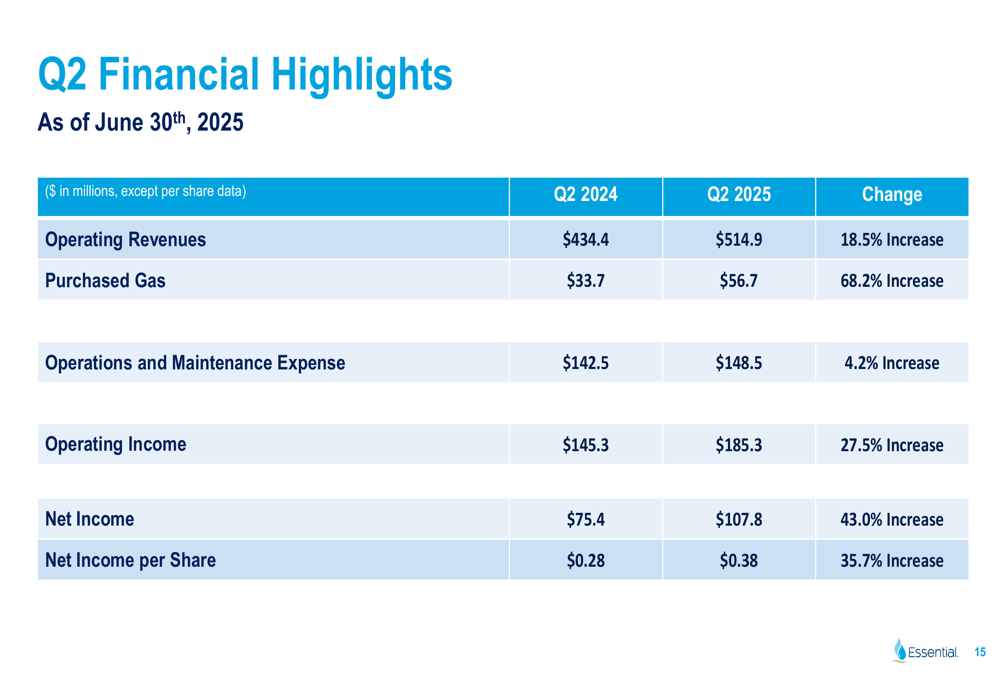

Essential Utilities delivered strong financial performance in Q2 2025, with operating revenues increasing 18.5% to $514.9 million compared to $434.4 million in Q2 2024. Net income rose 43.0% to $107.8 million, up from $75.4 million in the same period last year.

As shown in the following chart detailing the company’s financial highlights for the quarter:

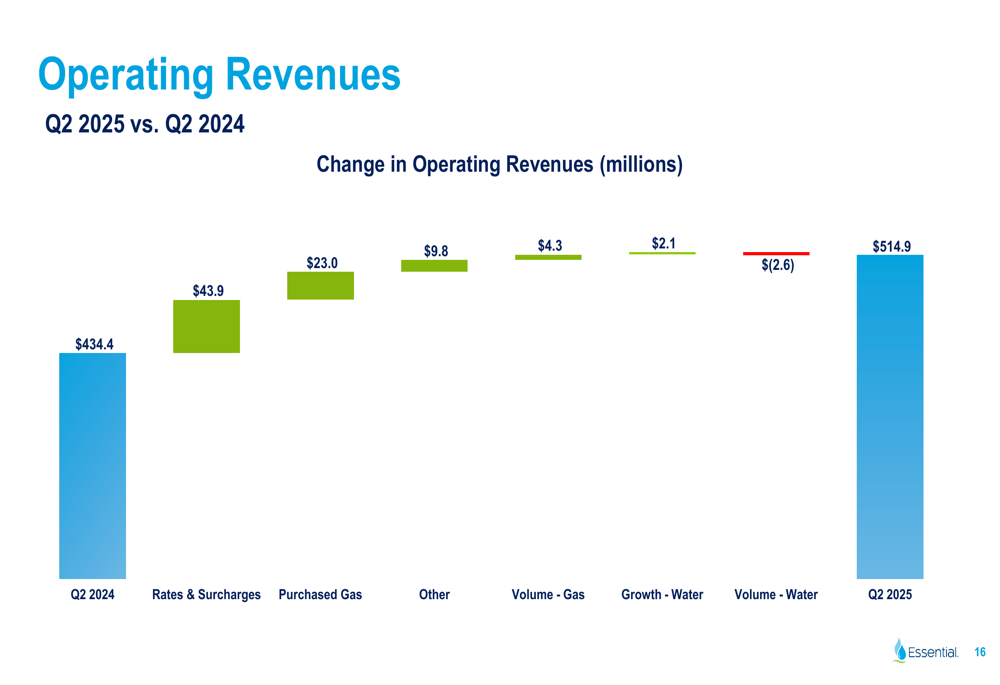

The significant revenue growth was primarily driven by rate increases and surcharges, which contributed $43.9 million, along with a $23.0 million increase in purchased gas. The company also saw contributions from other revenues ($9.8 million) and gas volume increases ($4.3 million), partially offset by a decrease in water volume revenue of $2.6 million.

This breakdown of revenue drivers is illustrated in the following waterfall chart:

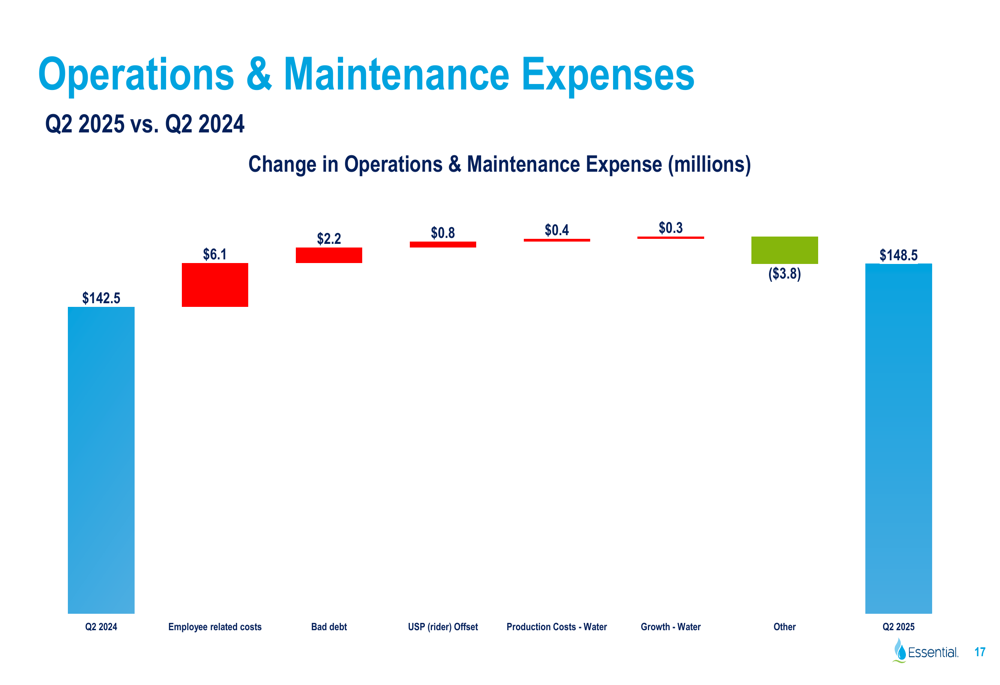

Operations and maintenance expenses increased modestly by 4.2% to $148.5 million, with employee-related costs accounting for the largest portion of the increase at $6.1 million. The company continues to demonstrate cost discipline, as shown in this expense breakdown:

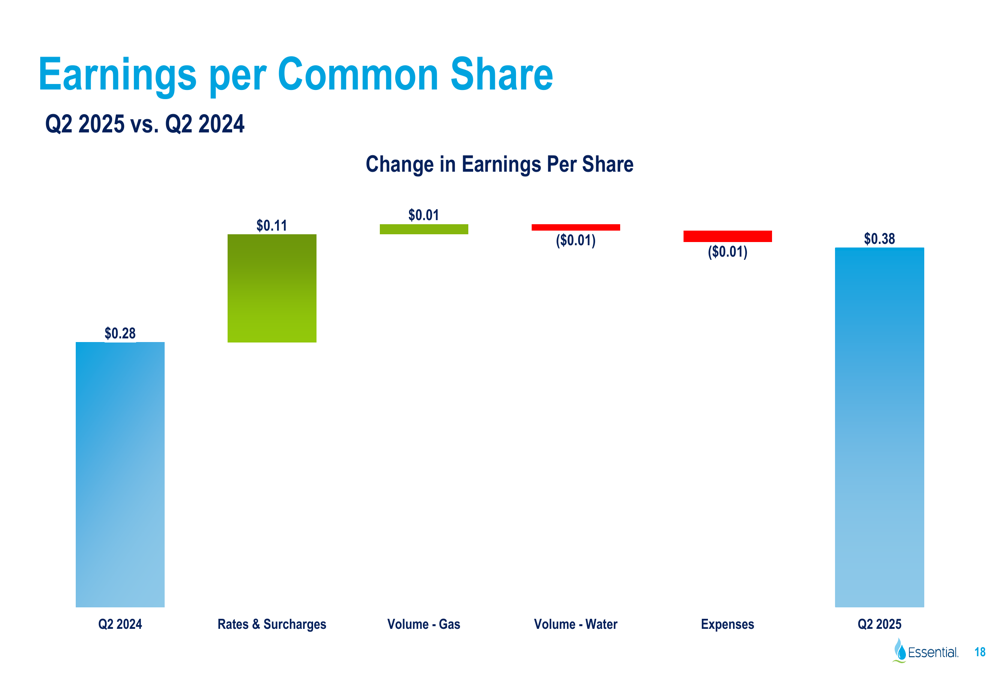

The combination of strong revenue growth and controlled expenses resulted in the significant improvement in earnings per share, as illustrated in this EPS bridge:

Year-to-date, Essential Utilities has achieved an EPS of $1.41, up 12.8% from the same period in 2024, with the company noting that approximately 40-50% of annual earnings are typically recorded in the first quarter due to seasonal factors.

Strategic Initiatives

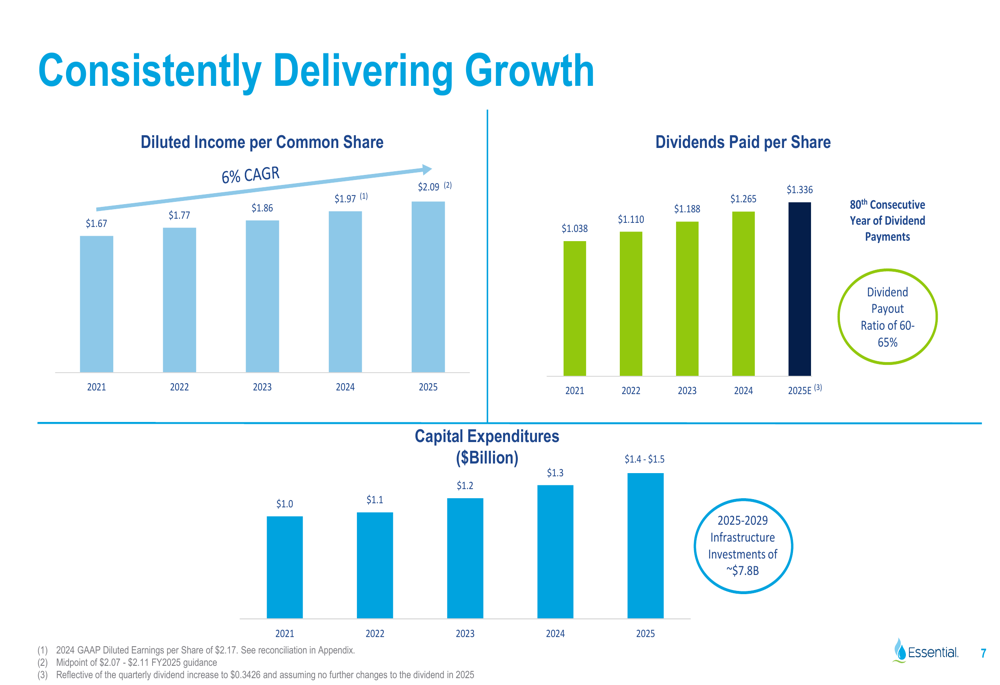

Essential Utilities continues to execute on its infrastructure investment strategy, with planned capital expenditures of $1.4-$1.5 billion for 2025, part of a broader $7.8 billion infrastructure investment plan for 2025-2029.

The company highlighted its consistent growth trajectory in earnings per share, dividends, and capital expenditures:

Acquisitions remain a key growth driver, with the company reporting over 135,000 water and wastewater customers acquired through M&A since 2015, resulting in approximately $550 million in rate base increase. Current pending transactions are expected to add over 200,000 customers with a total purchase price of approximately $301 million.

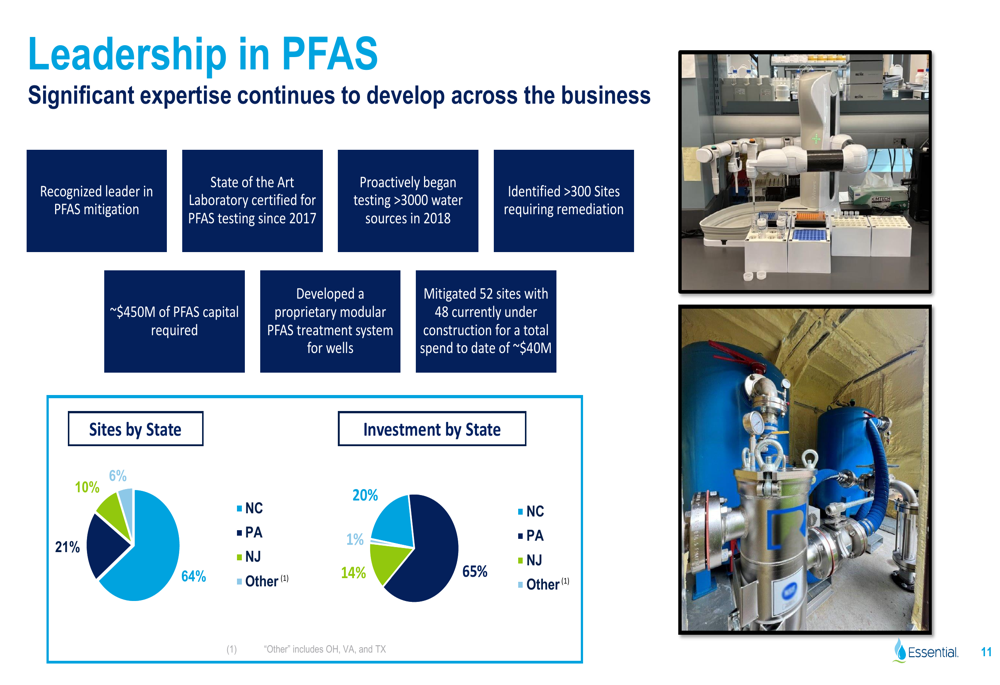

Essential Utilities also emphasized its leadership in PFAS (per- and polyfluoroalkyl substances) remediation, having identified over 300 sites requiring treatment with an estimated capital requirement of approximately $450 million. The company has developed a proprietary modular PFAS treatment system and has already mitigated 52 sites with 48 more currently under construction.

Forward-Looking Statements

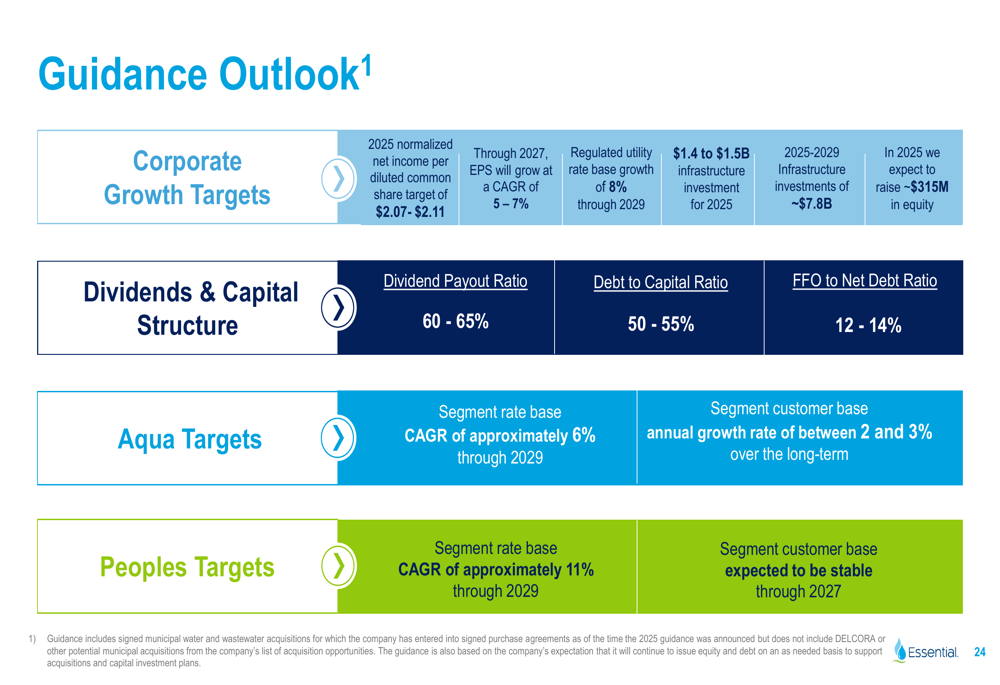

Essential Utilities reaffirmed its 2025 guidance and provided a comprehensive outlook for future growth:

Key guidance points include:

- 2025 normalized EPS target of $2.07-$2.11

- EPS growth CAGR of 5-7% through 2027

- Regulated utility rate base growth of 8% through 2029

- Dividend payout ratio target of 60-65%

- Segment-specific targets including approximately 6% rate base CAGR for Aqua and 11% for Peoples through 2029

The company also announced a 5.25% dividend increase, marking its 80th consecutive year of dividend payments, reinforcing its commitment to shareholder returns.

Competitive Industry Position

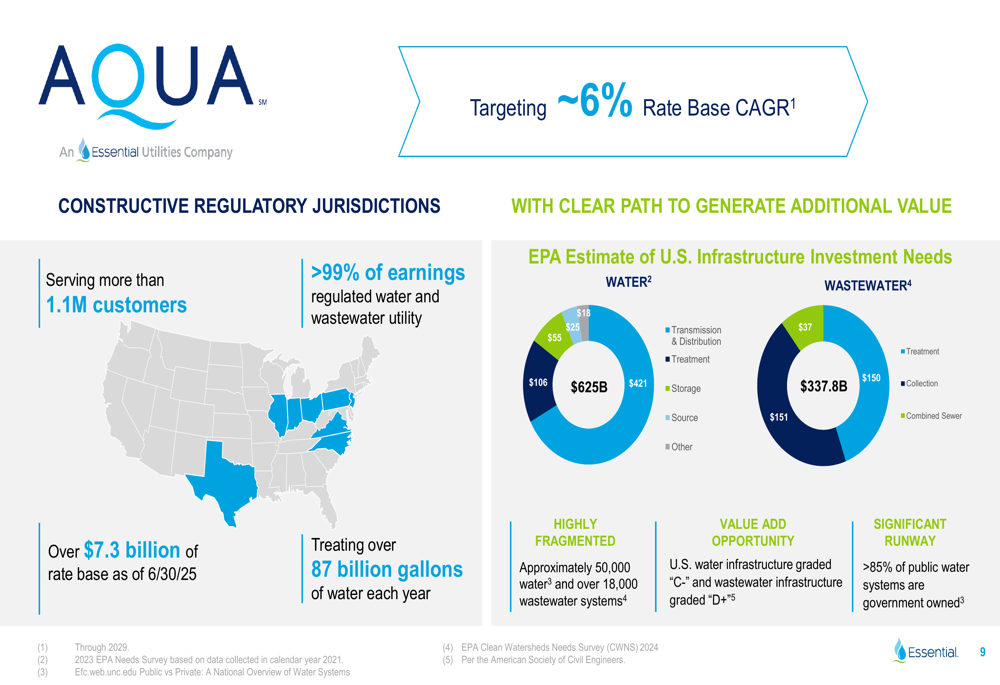

Essential Utilities highlighted the significant market opportunity in the fragmented water and wastewater industry, with approximately 50,000 water and over 18,000 wastewater systems in the United States. With more than 85% of public water systems being government-owned, the company sees substantial runway for future acquisitions and growth.

The EPA estimates U.S. infrastructure investment needs at $625 billion for water and $337.8 billion for wastewater, with current infrastructure graded "C-" for water and "D+" for wastewater, underscoring the long-term growth potential in the sector.

The company serves more than 1.1 million customers with over 99% of earnings coming from regulated water and wastewater utility operations. Essential Utilities treats over 87 billion gallons of water annually and has a rate base of over $7.3 billion as of June 30, 2025.

In Texas, a key growth market, the company has achieved a customer CAGR of 3.2% since 2015, adding approximately 25,000 water and wastewater customers, with over 90,000 more under contract or negotiation. The Texas rate base has grown at a CAGR of 13.5% since 2015 and is expected to reach $1.1 billion by year-end 2029.

Essential Utilities continues to demonstrate operational excellence, maintaining top quartile performance in O&M efficiency per customer since 2015 and significantly outperforming the national average in terms of system violations (1.4% versus 12.6% national average in 2024).

With its strong financial performance, strategic growth initiatives, and commitment to infrastructure investment, Essential Utilities appears well-positioned to continue its trajectory of consistent growth while delivering essential services to an expanding customer base.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.