TSX runs higher on rate cut expectations

Essex Property Trust (NYSE:ESS) revealed strong second-quarter performance in its latest corporate presentation, highlighted by significant growth in Net Income per diluted share and strategic portfolio management. The multifamily REIT, which focuses on West Coast markets, reported continued momentum following its strong first-quarter results.

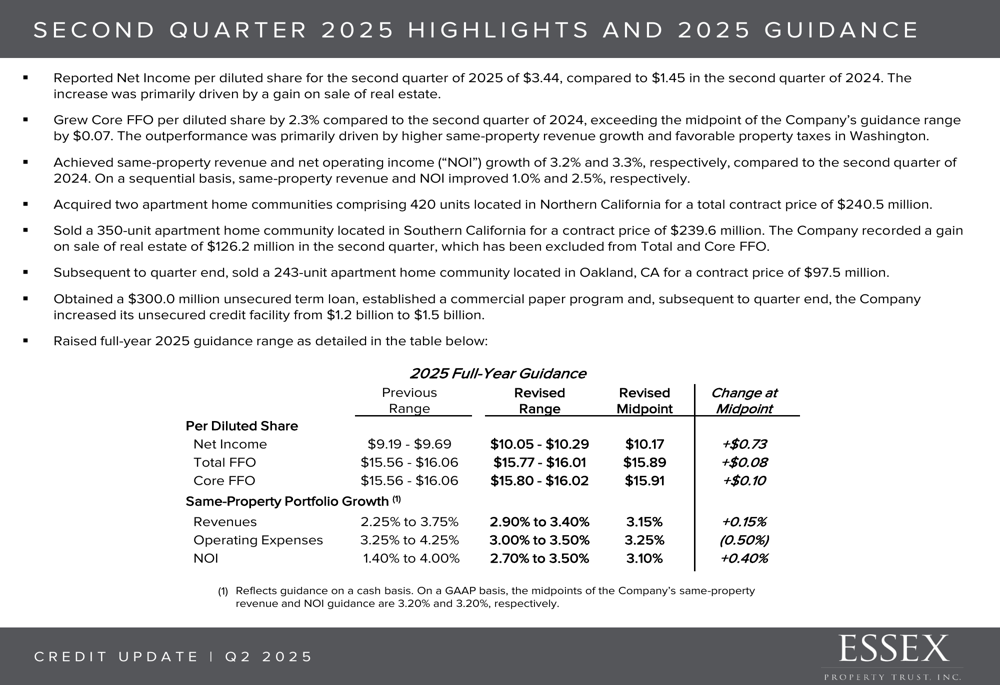

Quarterly Performance Highlights

Essex Property Trust reported substantial growth in its second quarter 2025 results, with Net Income per diluted share increasing dramatically from $1.45 to $3.44. Core Funds From Operations (FFO) per diluted share grew by 2.3% compared to the same period last year, while same-property revenue and net operating income (NOI) increased by 3.2% and 3.3%, respectively.

These results continue the positive trajectory seen in Q1 2025, when the company reported an earnings per share of $3.16, significantly exceeding analyst expectations of $1.43.

As shown in the following quarterly highlights slide, the company has maintained steady operational growth while executing on its portfolio optimization strategy:

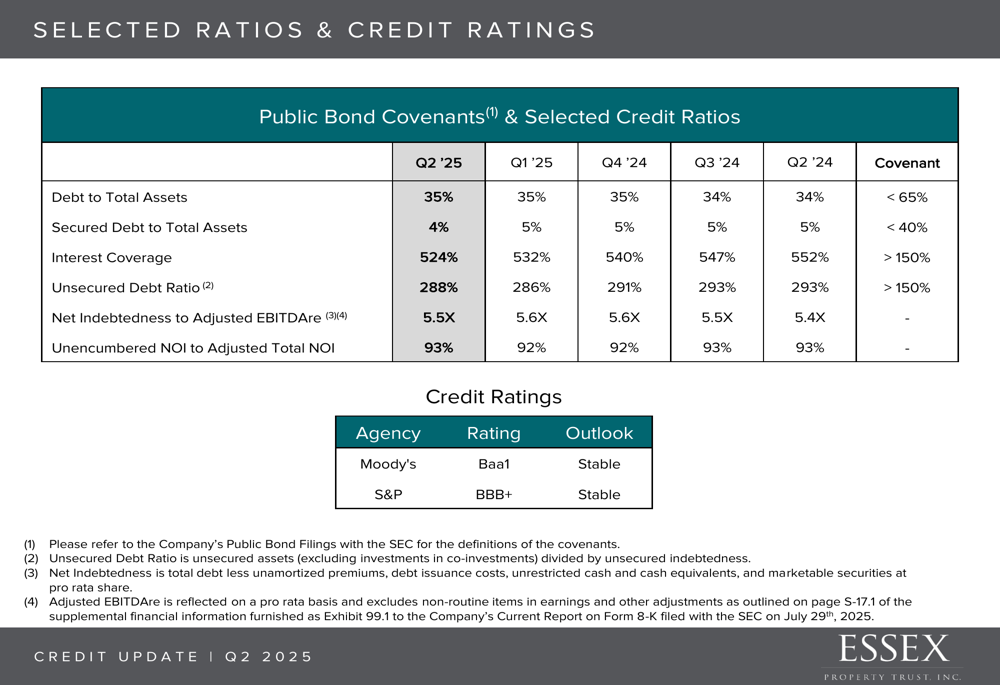

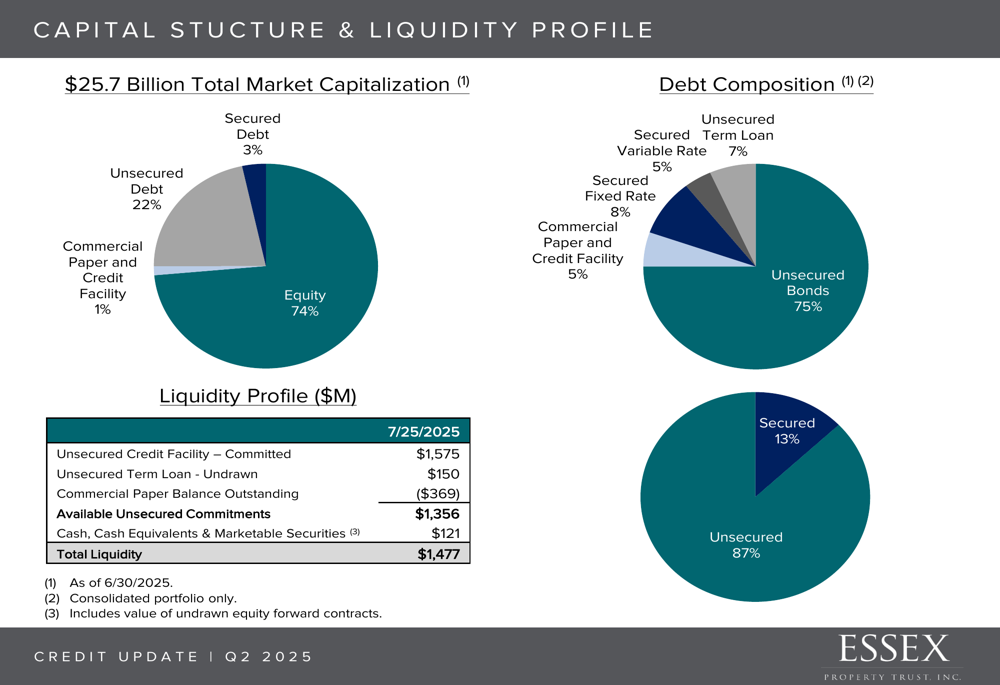

Capital Structure and Liquidity

Essex maintains a conservative financial position with total market capitalization of $25.7 billion. The company’s debt metrics remain well within covenant requirements, with a Debt to Total (EPA:TTEF) Assets ratio of 35% in Q2 2025, significantly below the 60% covenant requirement. Interest coverage stands at a robust 524%, demonstrating strong cash flow relative to debt obligations.

The following table details Essex’s key financial ratios and credit ratings:

The company’s capital structure reflects a conservative approach, with equity comprising 74% of total capitalization. Unsecured bonds make up the majority (75%) of the company’s debt composition, providing financing stability and flexibility.

Essex reported total liquidity of $1.48 billion as of July 25, 2025, including $1.36 billion in available unsecured commitments and $121 million in cash and marketable securities. This strong liquidity position enables the company to pursue strategic opportunities while maintaining financial flexibility.

The following capital structure breakdown illustrates Essex’s balanced approach to financing:

Strategic Property Transactions

During the second quarter, Essex executed balanced portfolio management with strategic acquisitions and dispositions. The company acquired two apartment communities totaling 420 units for $240.5 million, while simultaneously selling a 350-unit apartment community for $239.6 million and a 243-unit property for $97.5 million.

These transactions reflect Essex’s ongoing strategy to optimize its portfolio by acquiring properties in high-growth submarkets while divesting from less strategic locations. The nearly equivalent value of acquisitions and dispositions demonstrates a disciplined approach to capital allocation.

Additionally, the company secured a $300 million unsecured term loan during the quarter, further enhancing its financial flexibility.

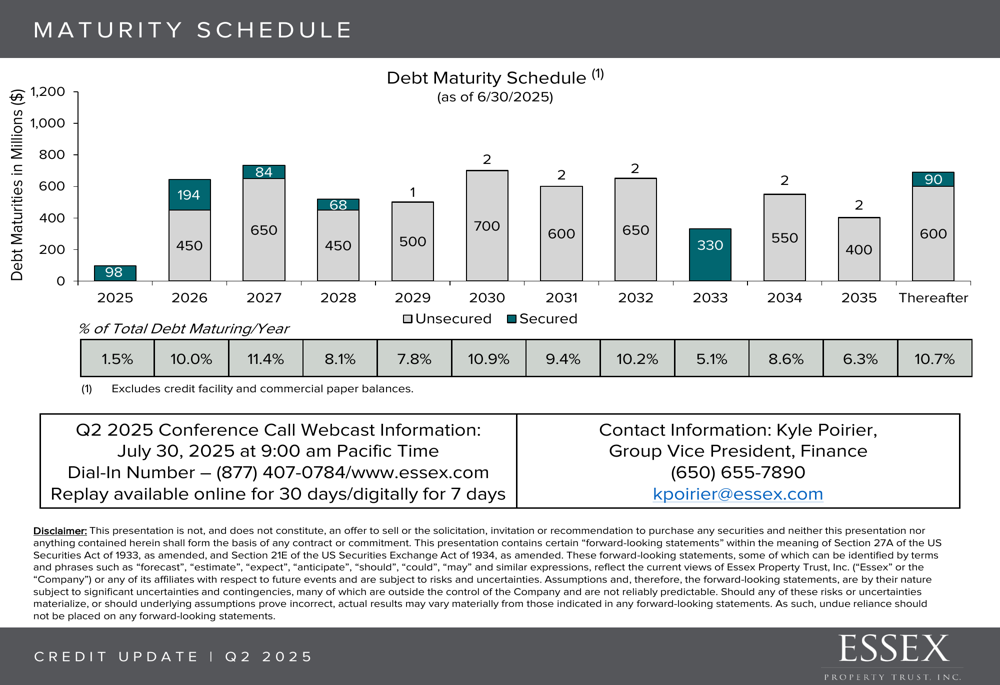

Debt Management Strategy

Essex’s debt maturity schedule reveals a well-structured approach to managing future obligations, with no significant debt concentration in any single year. This staggered approach helps mitigate refinancing risk and provides flexibility in managing capital needs across economic cycles.

As illustrated in the following maturity schedule, the company has manageable debt maturities in the coming years:

The largest single-year maturity occurs in 2030 at $700 million, representing approximately 14% of total debt. This balanced maturity profile aligns with Essex’s conservative financial management approach.

Forward-Looking Guidance

Essex Property Trust maintained its full-year 2025 guidance, projecting Net Income per diluted share between $10.05 and $10.29, Total FFO between $15.77 and $16.01, and Core FFO between $15.80 and $16.02 per diluted share.

For its Same-Property Portfolio, the company anticipates revenue growth between 2.90% and 3.40%, operating expense increases of 3.00% to 3.50%, and NOI growth ranging from 2.70% to 3.50%.

This guidance reflects continued optimism about Essex’s West Coast markets, despite macroeconomic uncertainties. In the previous quarter’s earnings call, CEO Angela Kleinman had noted, "We view that the downside risk is lower in our markets and it’s primarily because of supply," suggesting confidence in the company’s regional positioning.

Essex Property Trust’s stock closed at $283.16 on July 29, 2025, up 2.65% for the day, and remains within its 52-week trading range of $243.85 to $317.73. The company continues to demonstrate financial strength and operational stability in the competitive multifamily housing sector.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.