Microvast Holdings announces departure of chief financial officer

EverCommerce Inc (NASDAQ:EVCM) reported first-quarter 2025 results that exceeded guidance, with revenue growth accelerating on a pro forma basis and significant margin expansion. The company’s May 8 earnings presentation highlighted strong payments volume growth, successful AI integration initiatives, and robust free cash flow generation.

Quarterly Performance Highlights

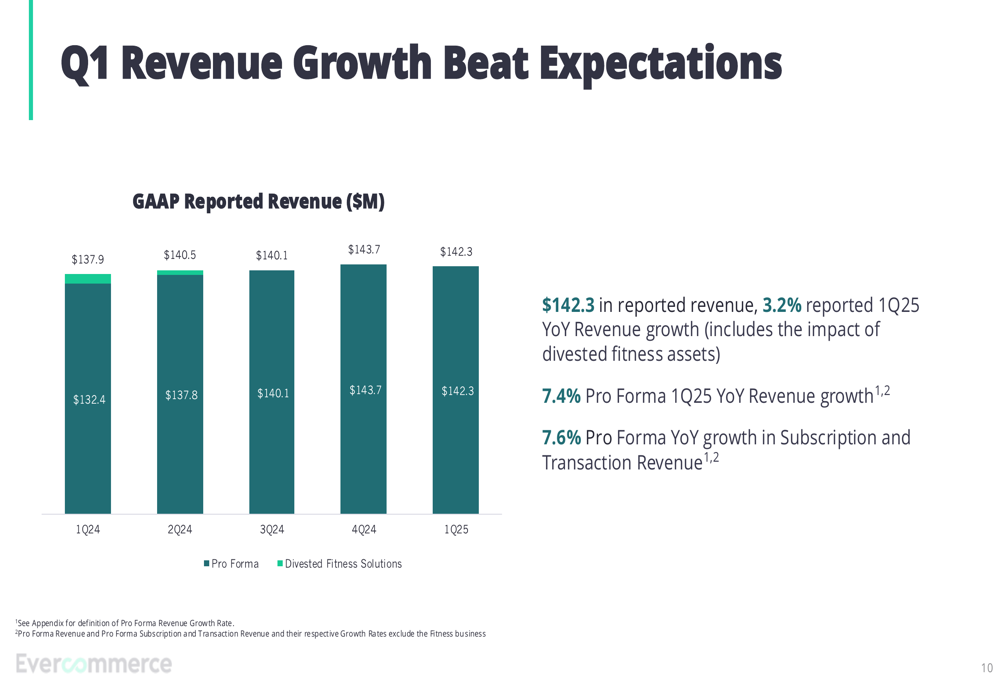

EverCommerce reported Q1 2025 revenue of $142.3 million, beating the top end of its guidance range with 3.2% year-over-year growth on a reported basis. When excluding divested fitness assets, pro forma revenue growth reached 7.4% year-over-year, showing acceleration in the company’s core business.

"Revenue of $142.3M beat the top end of the guidance range, with Reported Revenue growth of 3.2% YoY and Pro Forma growth of 7.4% YoY, excluding fitness sale," the company stated in its presentation.

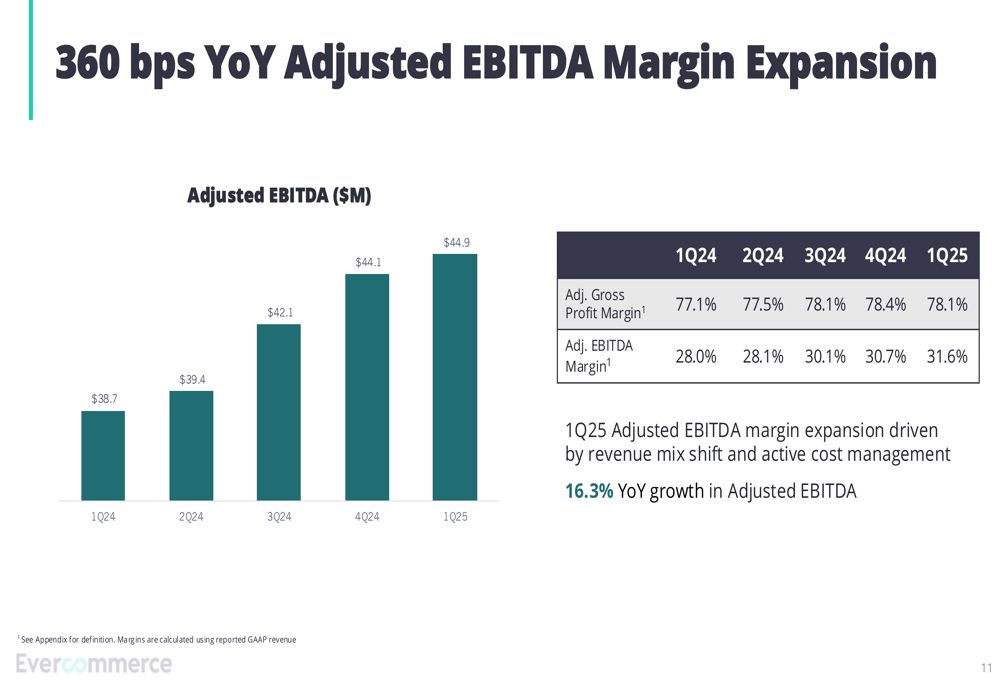

The company’s adjusted EBITDA also exceeded guidance, reaching $44.9 million with a 31.6% margin, representing a significant 360 basis point expansion compared to the year-ago period.

As shown in the following chart of quarterly revenue performance:

EverCommerce has maintained consistent revenue growth over the past five quarters, with Q1 2025 showing continued momentum in its core business segments. The company’s subscription and transaction revenue, which represents its recurring revenue base, grew 7.6% year-over-year on a pro forma basis.

Margin expansion has been particularly impressive, as illustrated in this chart of adjusted EBITDA performance:

The company attributed this margin improvement to "revenue mix shift and active cost management," resulting in 16.3% year-over-year growth in adjusted EBITDA. Gross profit margins have remained consistently strong at 78.1% in Q1 2025.

Strategic Initiatives

EverCommerce continues to focus on three key strategic initiatives: AI integration, payments enablement, and cross-selling across its customer base of over 725,000 global service businesses.

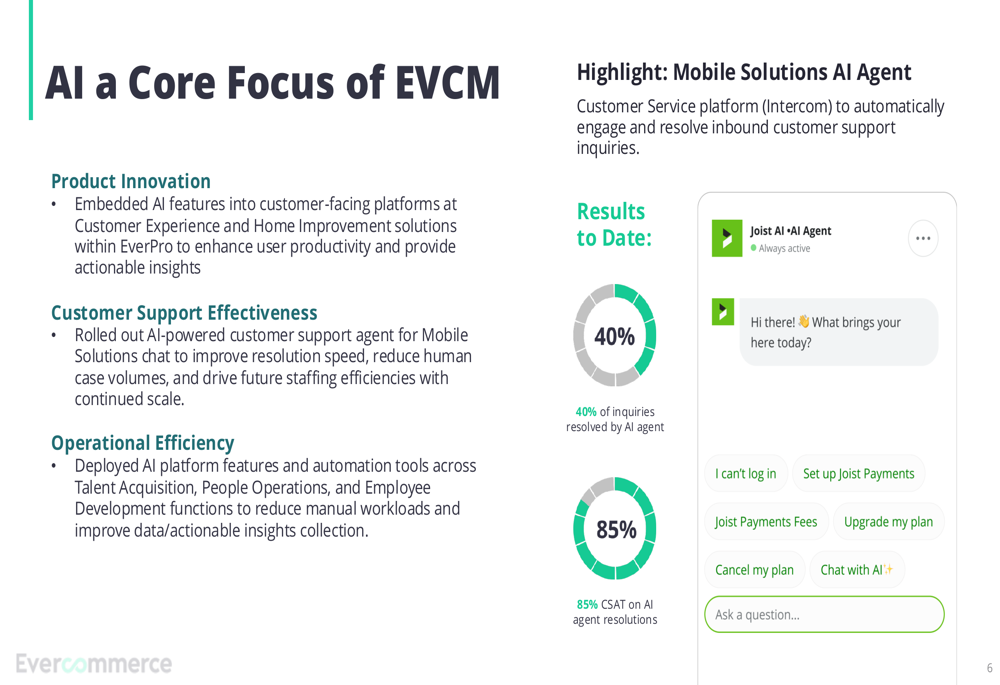

The company has made significant progress in embedding AI capabilities across its product portfolio, as shown in this overview:

The AI integration strategy spans product innovation, customer support, and operational efficiency. Notably, the company’s AI-powered customer support agent for Mobile Solutions is resolving 40% of inquiries while maintaining an 85% customer satisfaction rating, demonstrating both efficiency gains and service quality.

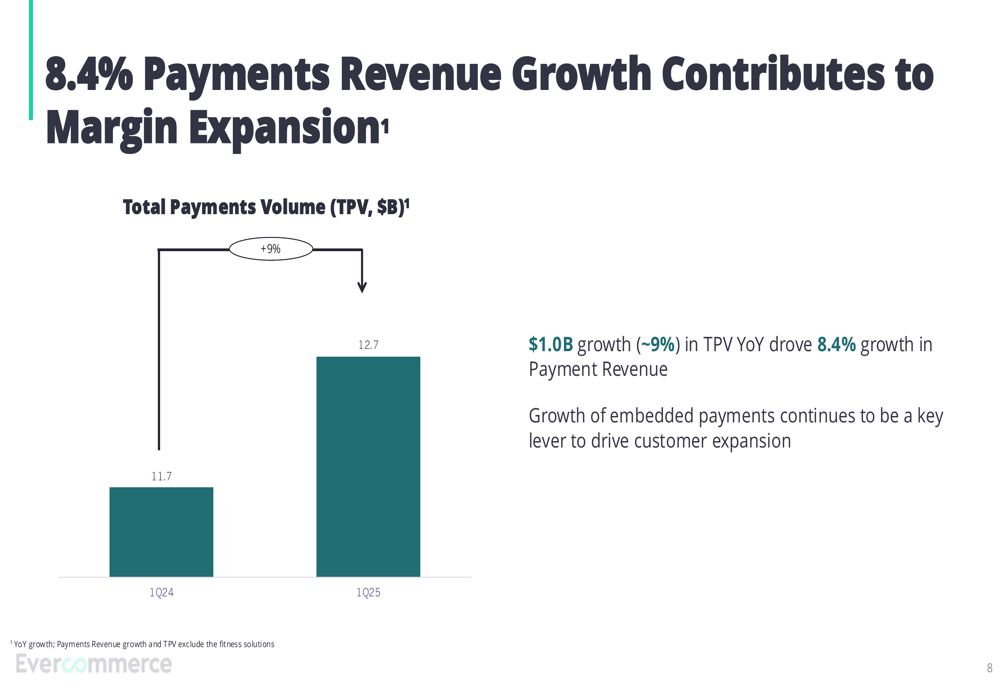

Payments growth remains a core driver of the company’s performance, with Total (EPA:TTEF) Payments Volume (TPV) increasing by approximately 9% year-over-year to $12.7 billion, driving 8.4% growth in payments revenue.

As illustrated in the following chart of payments volume growth:

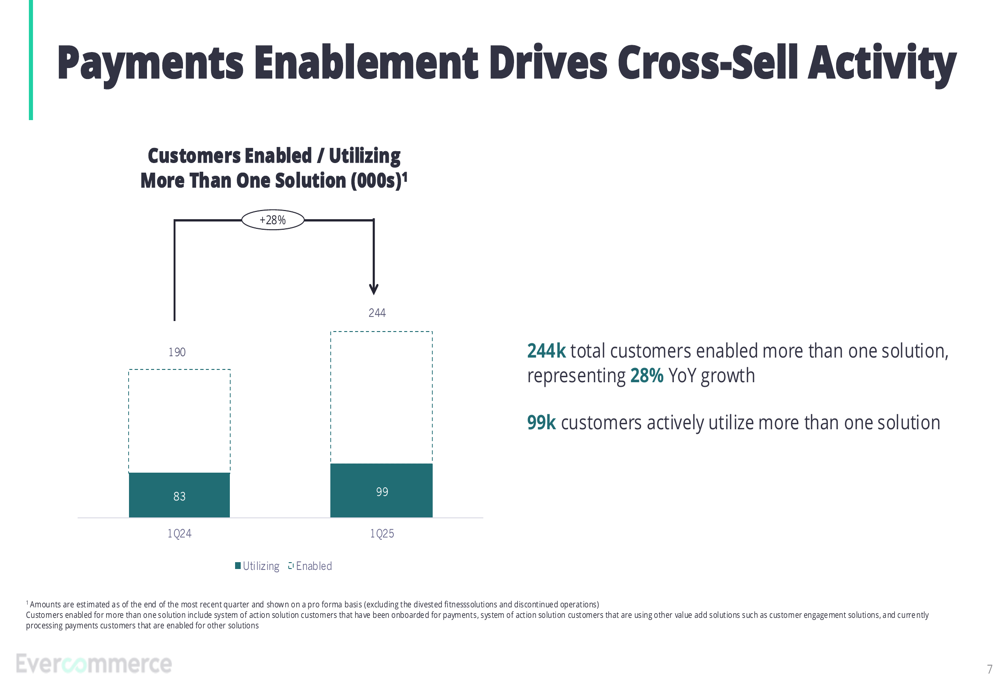

The company’s cross-selling efforts are showing strong results, with 244,000 customers now enabled for more than one solution, representing 28% year-over-year growth. Of these, 99,000 customers are actively utilizing multiple solutions.

The following chart demonstrates this cross-selling momentum:

Detailed Financial Analysis

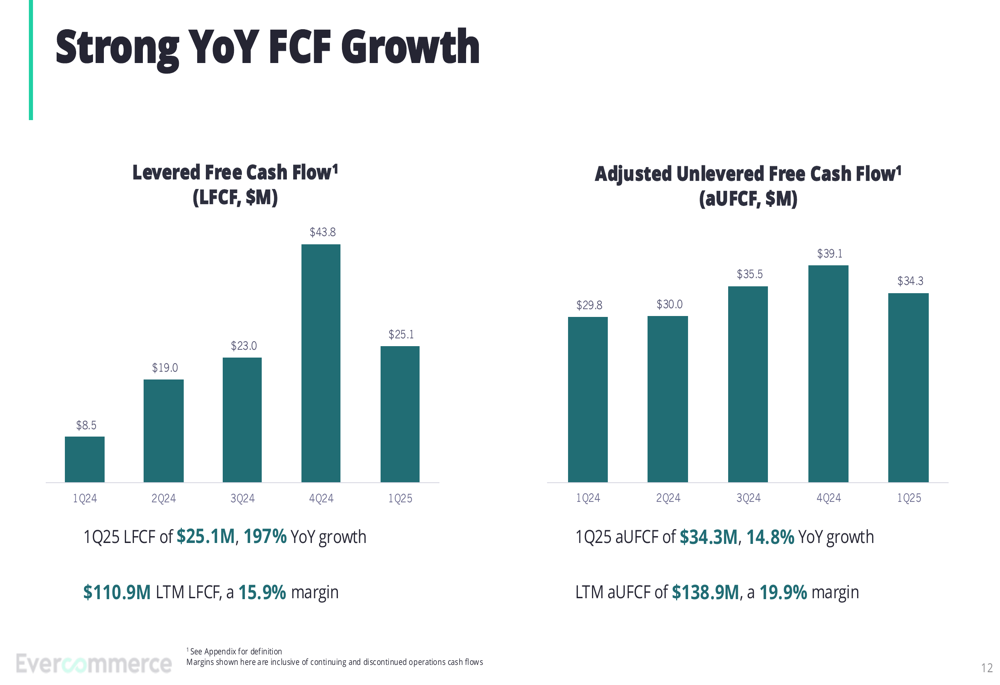

EverCommerce’s financial position strengthened considerably in Q1, with free cash flow showing dramatic improvement. Levered Free Cash Flow (LFCF) reached $25.1 million, representing 197% year-over-year growth, while Adjusted Unlevered Free Cash Flow (aUFCF) grew 14.8% to $34.3 million.

The company’s cash flow performance is illustrated in this chart:

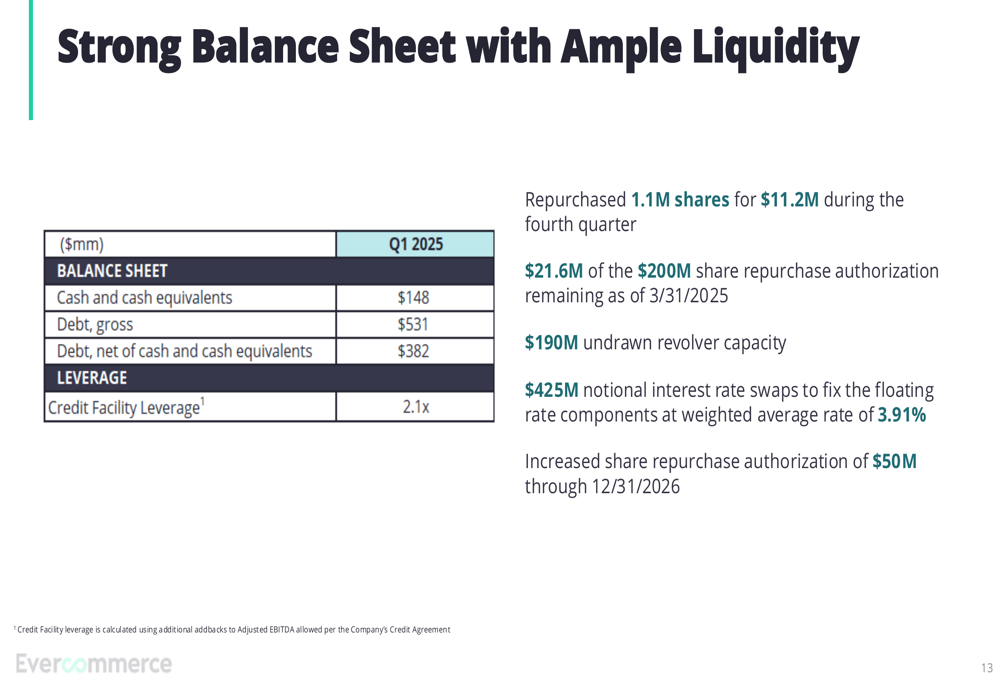

The balance sheet remains solid with $148 million in cash and cash equivalents against $531 million in gross debt, resulting in net debt of $382 million. The company’s credit facility leverage ratio stands at 2.1x, indicating a manageable debt position.

EverCommerce continued its share repurchase program, buying back 1.1 million shares for $11.2 million during the fourth quarter. The company also announced an increase and extension of its share repurchase authorization by $50 million through December 31, 2026.

The following slide details the company’s balance sheet and liquidity position:

Forward-Looking Statements

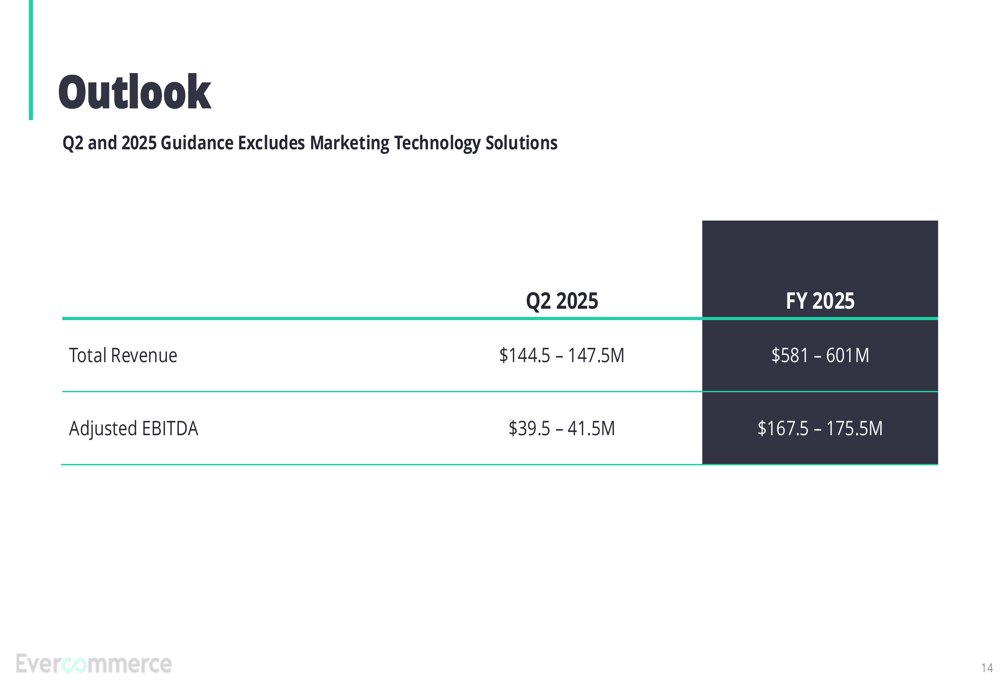

Looking ahead, EverCommerce provided guidance for both Q2 and full-year 2025. For the second quarter, the company expects revenue between $144.5 million and $147.5 million, with adjusted EBITDA of $39.5 million to $41.5 million.

For the full year 2025, EverCommerce projects revenue of $581 million to $601 million and adjusted EBITDA between $167.5 million and $175.5 million. This guidance excludes the Marketing Technology Solutions segment.

The company’s outlook is summarized in this guidance table:

This guidance suggests continued confidence in the company’s growth trajectory despite broader market uncertainties. The focus on high-margin recurring revenue streams and operational efficiencies appears to be yielding results, as evidenced by the expanding EBITDA margins.

EverCommerce’s stock closed at $10.12 on May 8, 2025, up 2.27% for the day, according to available market data. The company’s shares have traded between $8.10 and $12.35 over the past 52 weeks, with the current price representing a recovery from lows seen after the Q4 2024 earnings release, when the stock fell 6.15% following a wider-than-expected loss per share.

The Q1 2025 results mark a significant improvement from the previous quarter, with the company returning to profitability on a net income basis, reporting $934,000 in net income from continuing operations compared to a loss in the previous quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.