TSX drops after Canadian index edges higher in prior session

Introduction & Market Context

Exelixis Inc. (NASDAQ:EXEL) reported strong second-quarter 2025 results driven by continued growth of its cabozantinib franchise and early success in the neuroendocrine tumor (NET) market. The company presented its financial results on Monday, July 28, 2025, highlighting significant commercial momentum despite facing a slight decline in aftermarket trading, with shares down 1.13% to $38.50 following the announcement.

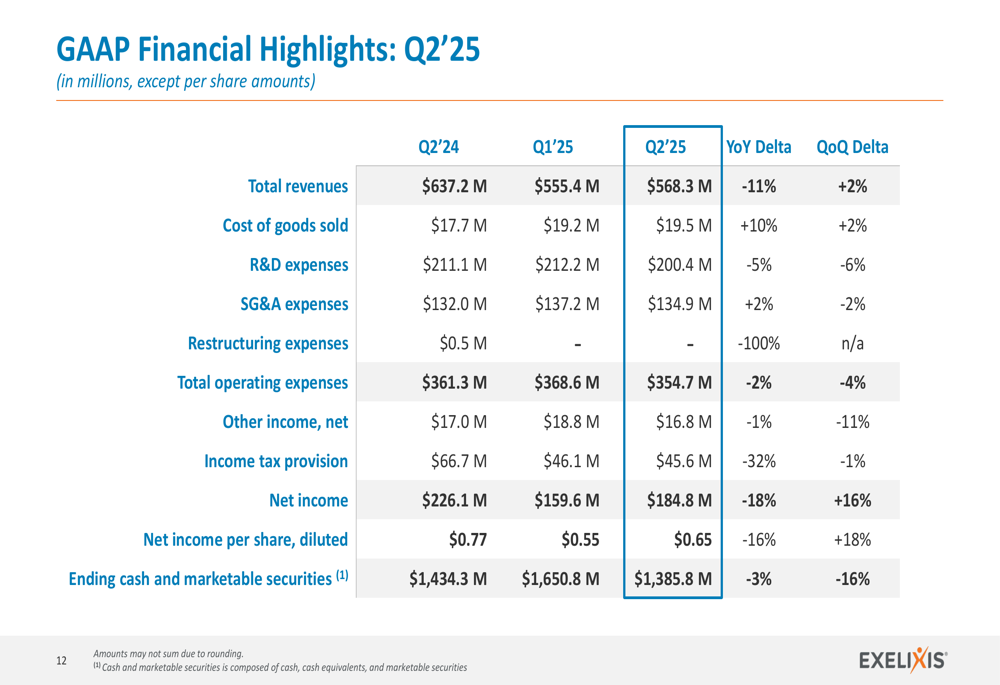

The oncology-focused biopharmaceutical company reported total revenues of $568.3 million for Q2 2025, representing a 2% increase quarter-over-quarter but an 11% decrease year-over-year, primarily due to lower collaboration revenues compared to the prior year.

Quarterly Performance Highlights

Exelixis reported cabozantinib net product revenues of $520 million in Q2 2025, marking a substantial 19% year-over-year increase from $438 million in Q2 2024. This growth was partially offset by lower collaboration revenues, which came in at $48.2 million compared to $199.6 million in the same period last year.

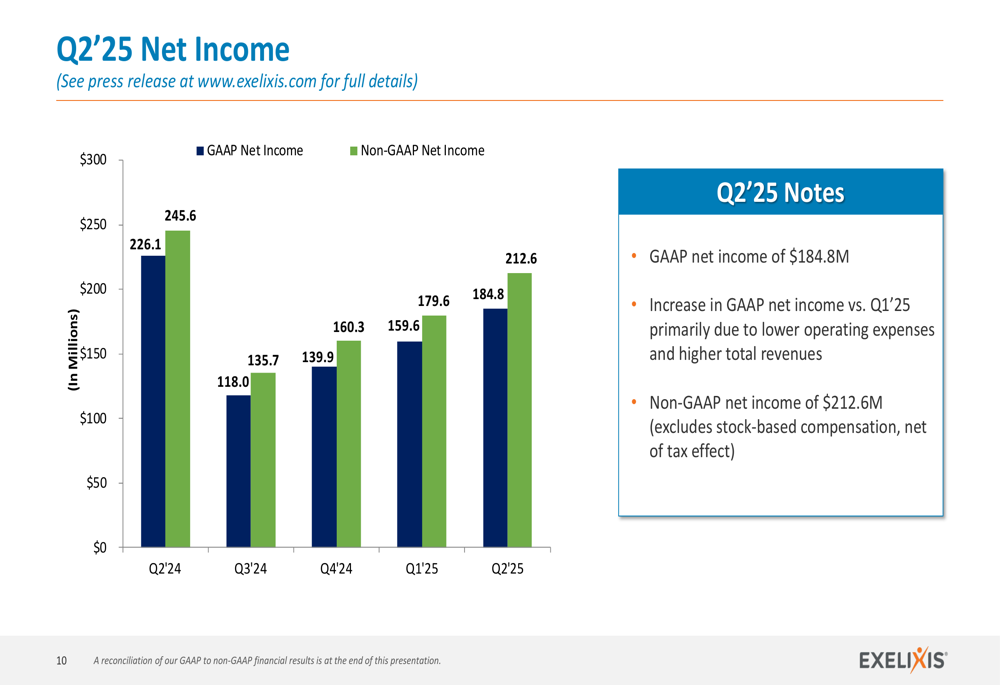

The company’s GAAP net income reached $184.8 million, or $0.65 per diluted share, representing a 16% increase from Q1 2025 but an 18% decrease compared to Q2 2024. On a non-GAAP basis, which excludes stock-based compensation, net income was $212.6 million, or $0.75 per diluted share.

As shown in the following comprehensive financial summary, Exelixis maintained strong profitability despite increased investment in its pipeline:

Operating expenses decreased by 4% quarter-over-quarter to $354.7 million, primarily due to lower R&D expenses, which fell 6% to $200.4 million. The company’s cash position stood at $1.39 billion at the end of Q2, reflecting continued investment in stock repurchases.

The following chart illustrates Exelixis’ net income performance over the past five quarters:

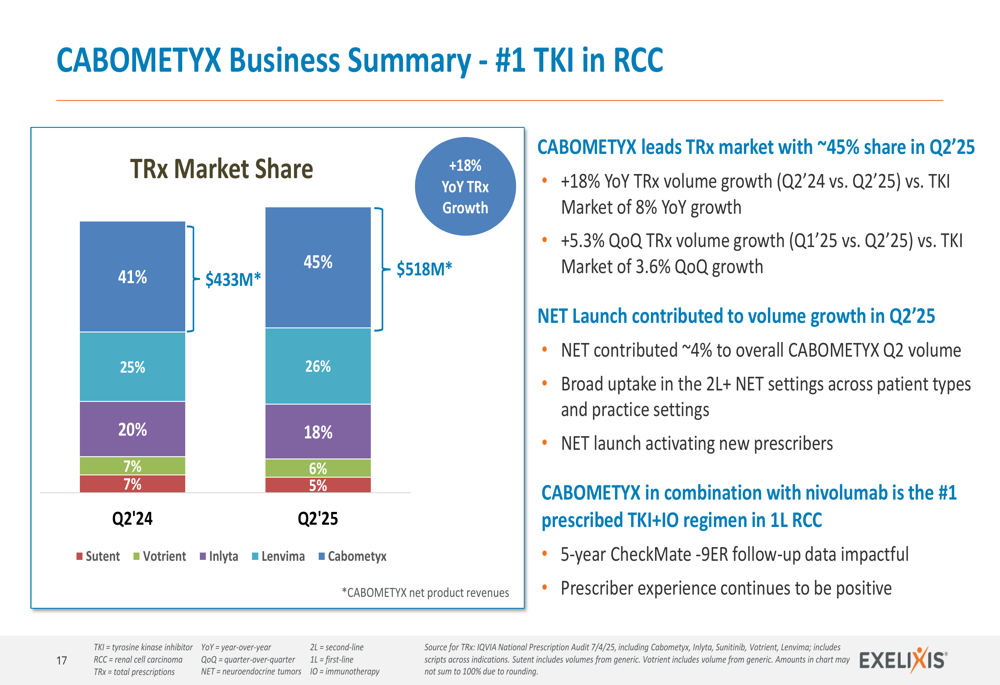

CABOMETYX Commercial Success

CABOMETYX continued to strengthen its market leadership position in renal cell carcinoma (RCC), maintaining its status as the #1 prescribed TKI+IO combination therapy with nivolumab for the eleventh consecutive quarter. The drug captured approximately 45% of the TKI market share in Q2 2025, up from 41% in Q2 2024.

The following chart demonstrates CABOMETYX’s dominant market position and growth trajectory:

A significant contributor to CABOMETYX’s growth was its recent approval and launch in the neuroendocrine tumor (NET) market. The NET indication contributed approximately 4% to overall CABOMETYX Q2 volume, with the drug rapidly capturing approximately 35% of new patient share for second-line and beyond oral therapies in this segment.

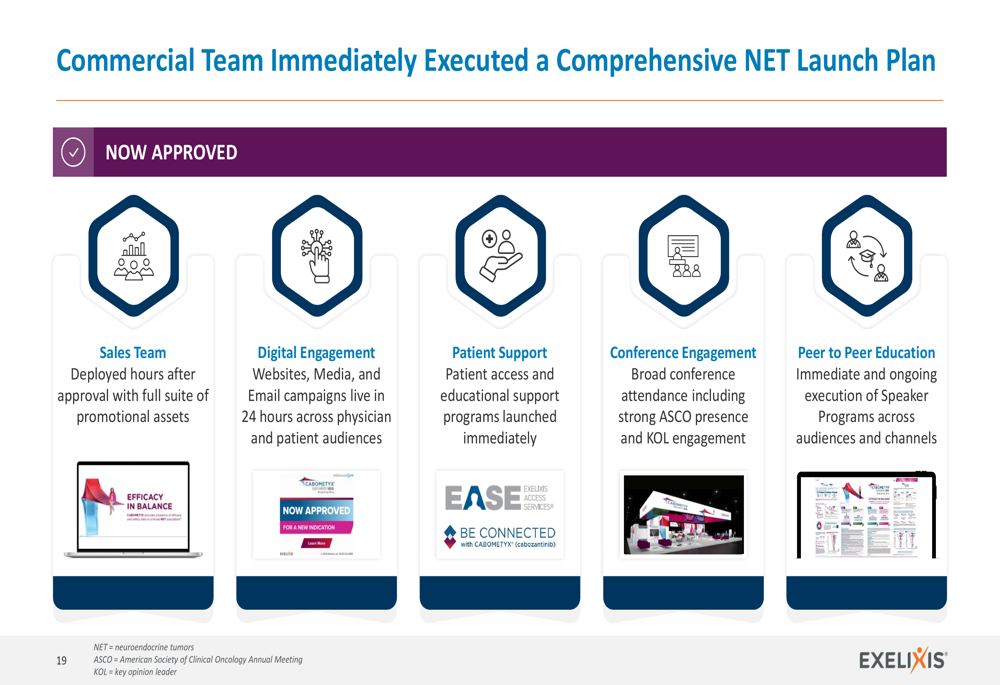

As illustrated in the following slide, Exelixis executed a comprehensive launch plan for CABOMETYX in NET:

The company reported that physician reception to CABOMETYX in NET has been overwhelmingly positive, with the drug already being viewed as the "best in class" oral therapy in NETs. Early adoption has been broad across patient types and practice settings.

Pipeline Development Updates

Exelixis provided several important updates on its pipeline candidate zanzalintinib, highlighting both advances and strategic adjustments:

1. STELLAR-303: The pivotal study of zanzalintinib plus atezolizumab in metastatic colorectal cancer (mCRC) showed positive topline results with a statistically significant improvement in overall survival in the intention-to-treat population. The company plans to discuss these results with regulators with the intention of filing a New Drug Application.

2. STELLAR-304: Enrollment has been completed for this pivotal study of zanzalintinib plus nivolumab in first-line non-clear cell renal cell carcinoma (nccRCC), with topline results expected in the first half of 2026.

3. STELLAR-305: Based on emerging phase 2 data, competitive landscape assessment, and evaluation of other potentially larger commercial opportunities, Exelixis decided not to advance this study in head and neck squamous cell carcinoma (HNSCC) to phase 3.

4. STELLAR-311: A new phase 3 pivotal study of zanzalintinib in advanced NET was initiated in Q2 2025, aiming to establish the drug as the preferred first oral therapy in NET.

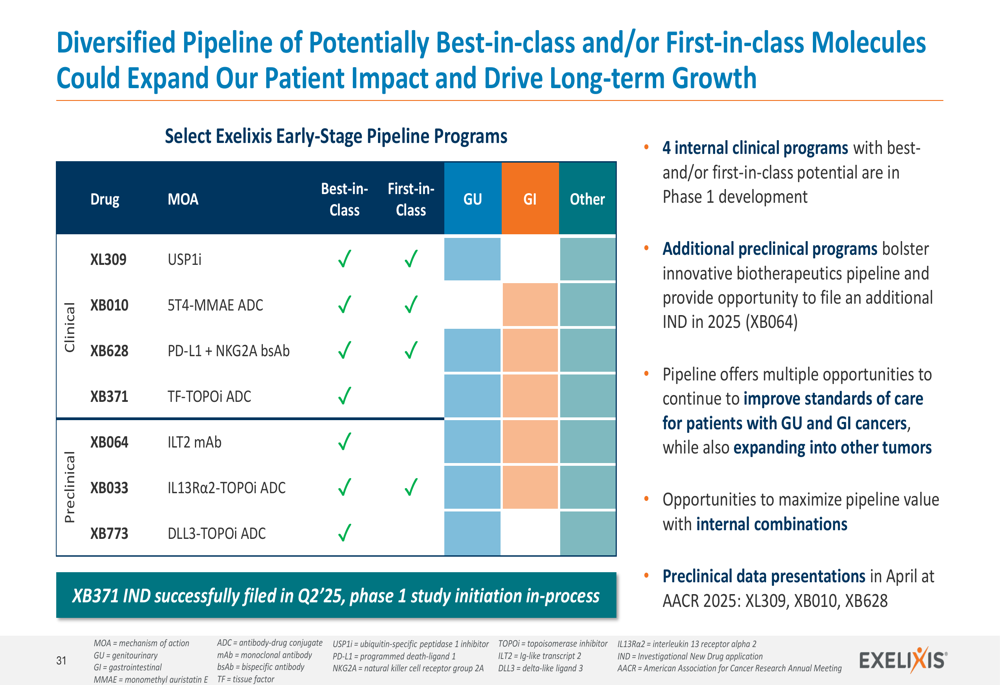

The company also highlighted its diversified early-stage pipeline, featuring four clinical programs with potential best-in-class and/or first-in-class molecules:

Financial Position & Outlook

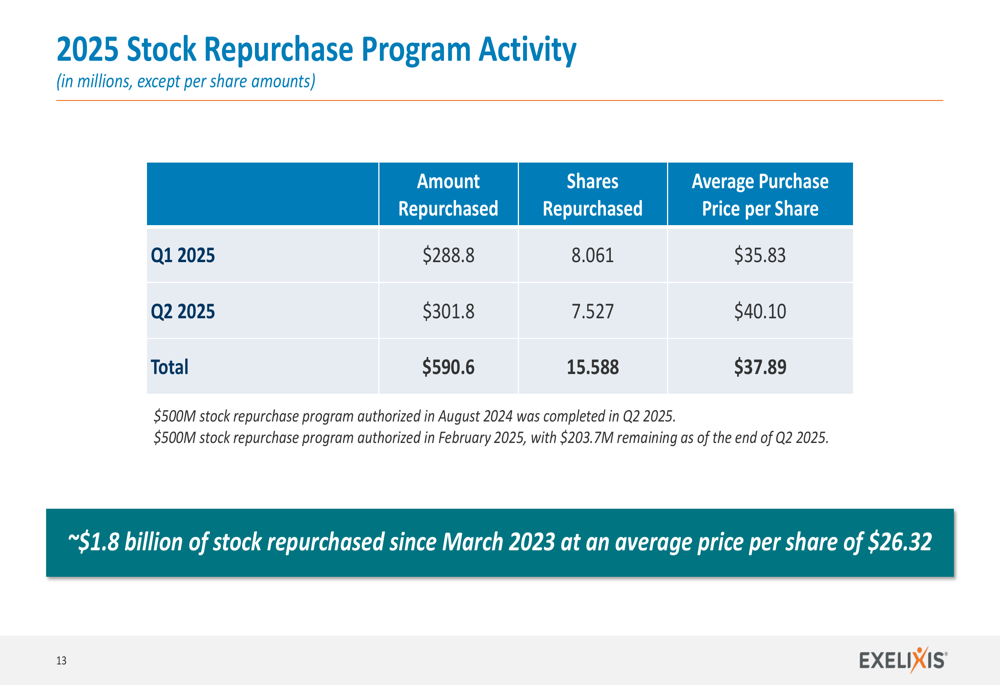

Exelixis continued its stock repurchase program, buying back $301.8 million worth of shares in Q2 2025 at an average price of $40.10 per share. Combined with Q1 repurchases, the company has bought back $590.6 million in shares during the first half of 2025. Since March 2023, Exelixis has repurchased approximately $1.8 billion in stock at an average price of $26.32 per share.

The following chart details the company’s recent stock repurchase activity:

For the full year 2025, Exelixis maintained its financial guidance, projecting:

- Total revenues: $2.25-$2.35 billion

- Net product revenues: $2.05-$2.15 billion

- R&D expenses: $925-$975 million

- SG&A expenses: $475-$525 million

- Effective tax rate: 21-23%

The company indicated it may update this guidance as the NET launch momentum builds and as it gains further clarity on additional revenue opportunities in the second half of 2025.

Michael M. Morrissey, Ph.D., President and CEO of Exelixis, emphasized the company’s balanced approach to growth, stating, "We work in a tough business, and I’m pleased to see our resilience and drive." He added, "We’re not looking to just build a big pipeline, but carefully and quickly identify the winners."

With its strong commercial performance, advancing pipeline, and solid financial position, Exelixis appears well-positioned to continue its growth trajectory, though investors will be closely watching the development of zanzalintinib and the continued expansion of CABOMETYX in the NET market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.