Raytheon awarded $71 million in Navy contracts for missile systems

Introduction & Market Context

Expro Group Holdings N.V. (NYSE:XPRO), a global provider of energy services, delivered its third consecutive quarter of results exceeding expectations according to its Q2 2025 presentation released on July 29. The company reported significant quarter-over-quarter improvements in both revenue and profitability metrics while maintaining a strong backlog of $2.3 billion.

The positive results come as Expro continues to focus on its international and offshore business, which represents approximately 80% of revenue. Despite the stock trading significantly below its 52-week high of $23.33, recent performance shows signs of operational improvement, with shares closing at $9.00, up 4.05% in the most recent session.

Quarterly Performance Highlights

Expro reported Q2 2025 revenue of $423 million, representing an 8% increase quarter-over-quarter from the $391 million reported in Q1. More impressively, Adjusted EBITDA jumped 24% sequentially to $94 million, resulting in an Adjusted EBITDA margin of 22% – an improvement of 200 basis points from the previous quarter.

The company generated $36 million in Adjusted Free Cash Flow during the quarter, representing 9% of revenue and highlighting Expro’s continued focus on capital discipline and operational efficiency.

As shown in the following financial performance summary:

The results mark a continuation of Expro’s positive momentum, following its Q1 2025 performance where the company reported an earnings per share of $0.25, significantly beating the $0.12 forecast at that time.

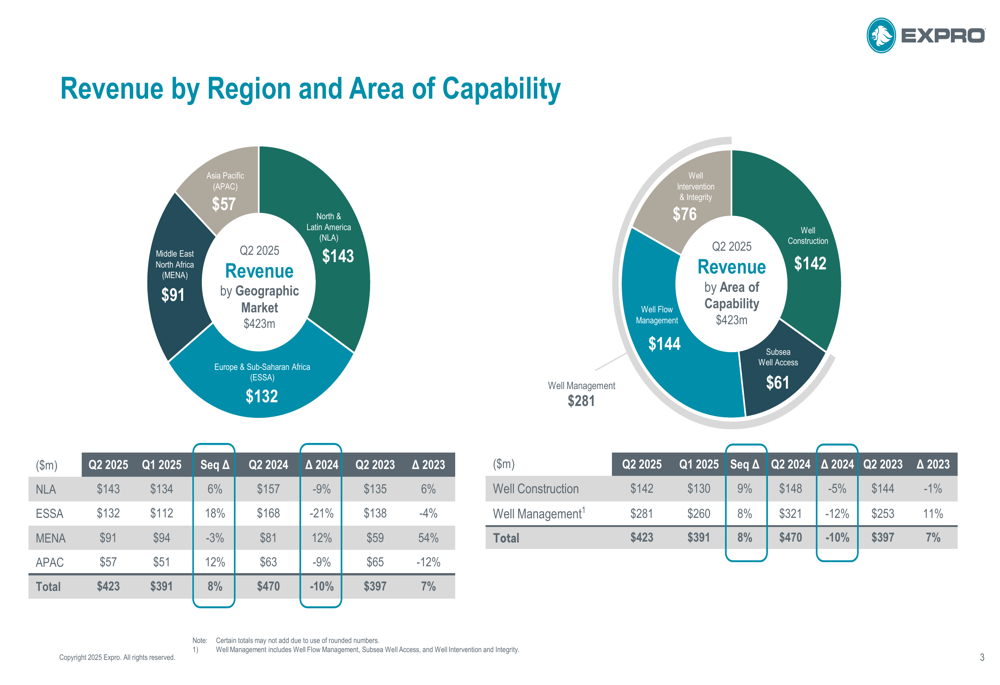

Regional Performance Analysis

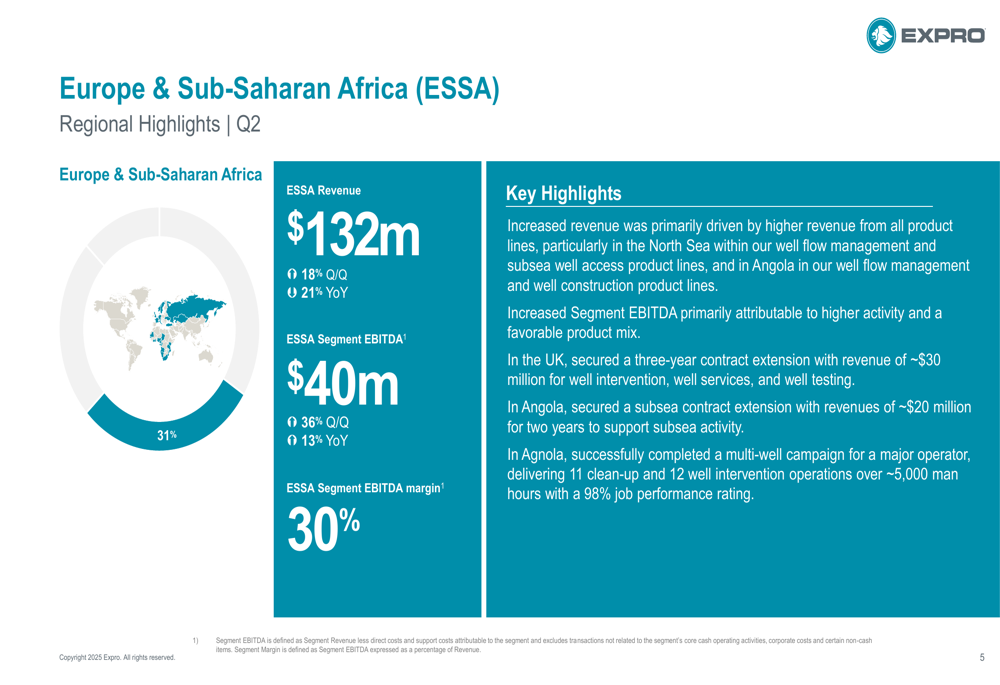

Expro’s performance varied across its four geographic regions, with particularly strong results in Europe & Sub-Saharan Africa (ESSA):

The ESSA region delivered the strongest growth, with revenue increasing 18% quarter-over-quarter to $132 million and segment EBITDA jumping 36% to $40 million. This resulted in an impressive 30% EBITDA margin for the region, driven by increased activity in the North Sea and Angola.

North & Latin America (NLA) remained Expro’s largest revenue contributor at $143 million (up 6% Q/Q), generating $34 million in segment EBITDA with a 24% margin. The company secured significant contract wins in this region, including a five-year, multi-rig well construction contract in Guyana worth over $120 million.

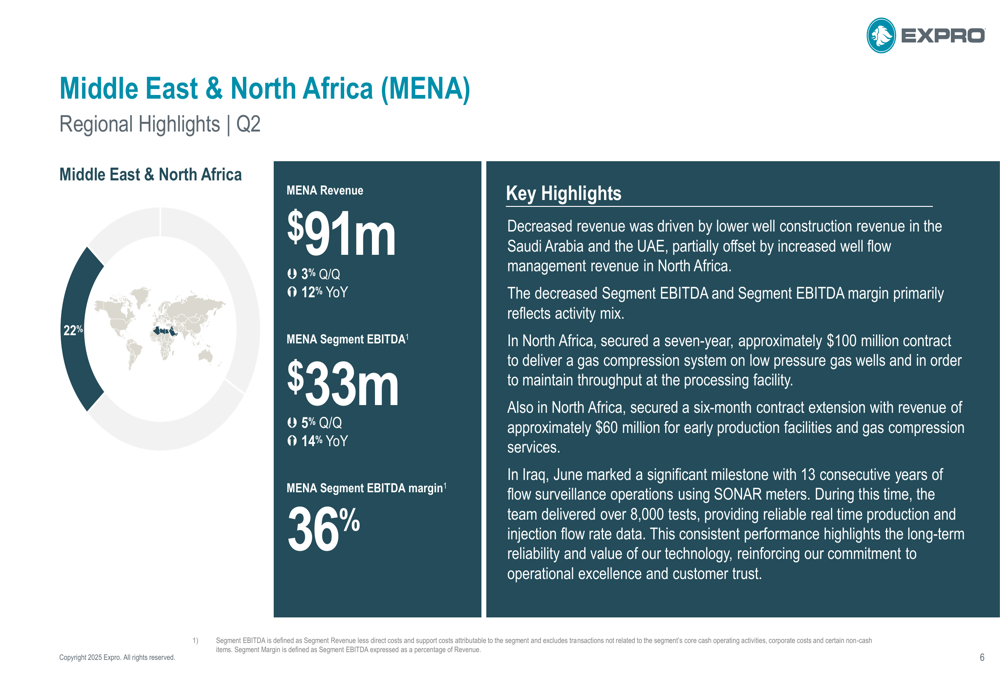

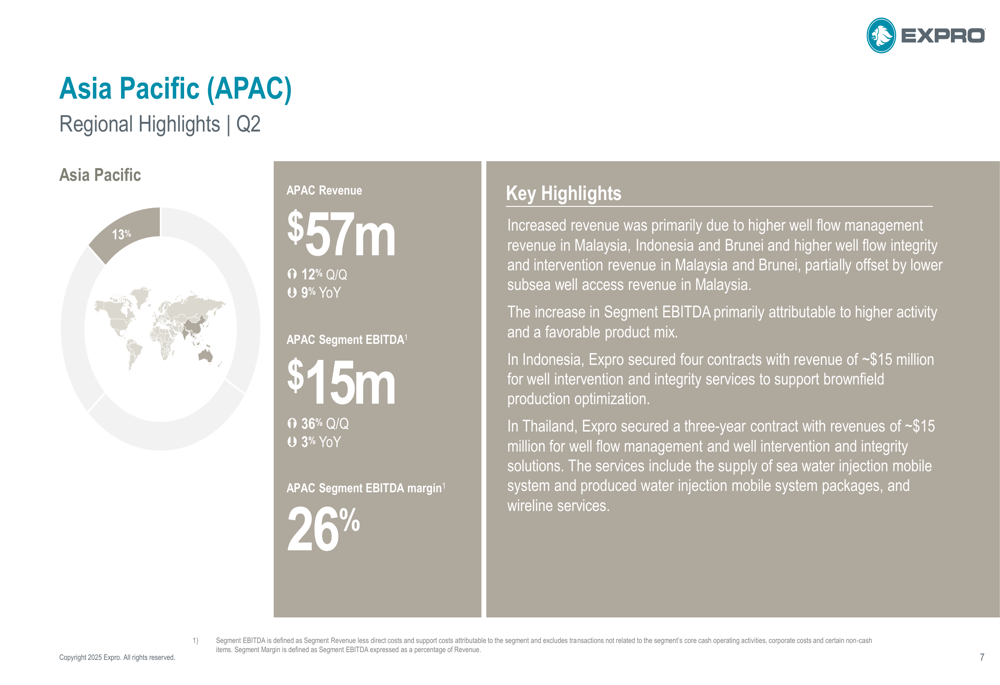

The Middle East & North Africa (MENA) region, while experiencing a slight 3% revenue decline to $91 million, maintained the highest profitability with a 36% segment EBITDA margin. Meanwhile, Asia Pacific (APAC) showed recovery with 12% revenue growth to $57 million and a 36% increase in segment EBITDA.

The regional breakdown demonstrates Expro’s global diversification and ability to maintain strong margins across various markets:

Strategic Initiatives & Technology

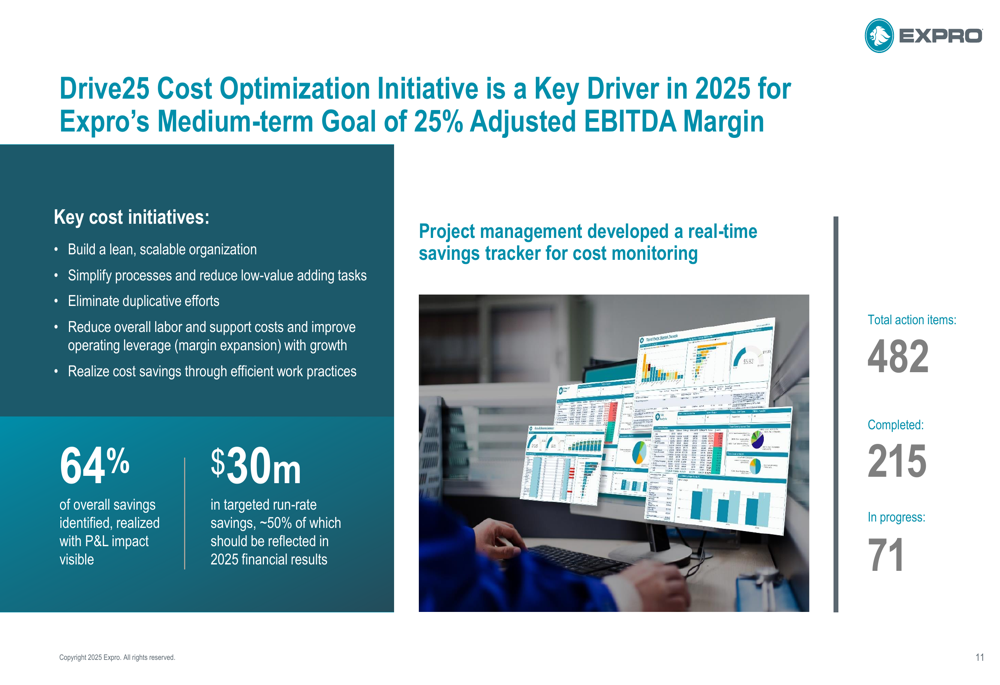

A key driver of Expro’s improving financial performance is its Drive25 cost optimization program, which has completed over 60% of planned cost improvement initiatives. The company has implemented real-time tracking dashboards to monitor realized cost savings throughout 2025.

The initiative is central to Expro’s medium-term goal of achieving a 25% Adjusted EBITDA margin, as illustrated in the following slide:

Expro is also focusing on technology deployment to increase automation, improve safety, and optimize production. Notable achievements in Q2 included the deployment of the BRUTE® Armor Packer in West Africa, the fully automated Remote Clamp Installation System in the North Sea, and the Generation-X Remote Plug Launcher combined with the Skyhook cement line in the Middle East offshore.

These technological advancements support the company’s strategy of differentiating itself in the market while improving operational efficiency and safety.

Outlook & Guidance

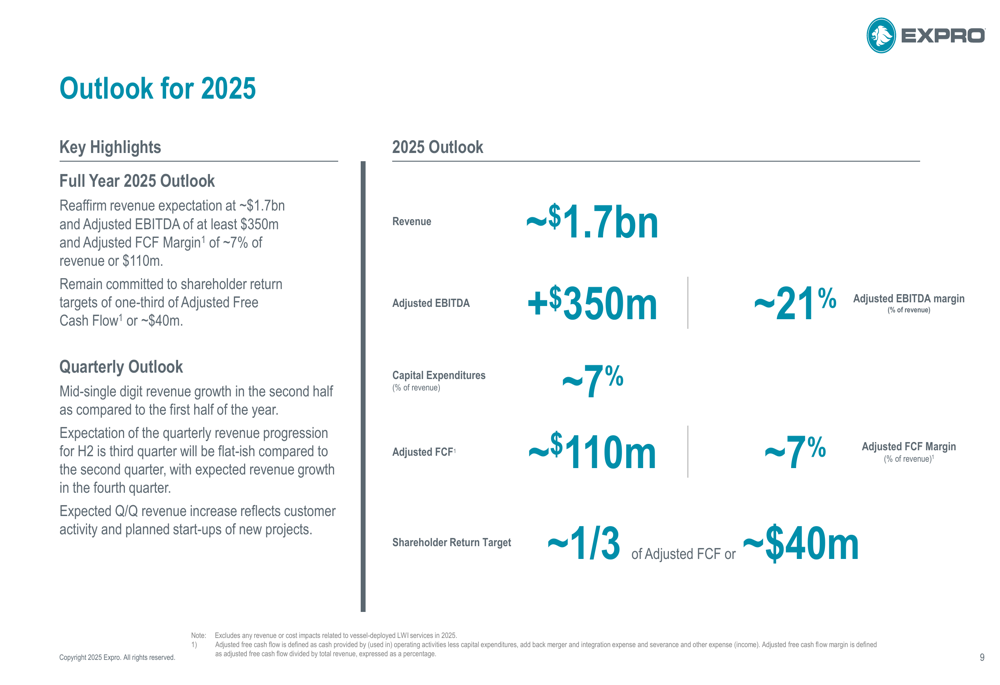

Expro reaffirmed its full-year 2025 guidance, projecting:

- Revenue of approximately $1.7 billion

- Adjusted EBITDA of at least $350 million

- Adjusted Free Cash Flow of approximately $110 million (7% of revenue)

The company expects mid-single-digit revenue growth in the second half of 2025 compared to the first half. Expro remains committed to shareholder returns, targeting approximately one-third of Adjusted Free Cash Flow (around $40 million) to be returned to shareholders.

For the longer term, Expro outlined ambitious medium-term targets:

The company aims to reach $2 billion in revenue with a 25% Adjusted EBITDA margin and 10% Adjusted Free Cash Flow margin. These targets will be supported by organic revenue growth, improved activity mix with increased drilling and completions spending by customers, and continued cost optimization.

Conclusion

Expro’s Q2 2025 presentation portrays a company executing well on its operational and financial objectives, with three consecutive quarters of results exceeding expectations. The improvement in margins and cash flow generation demonstrates the effectiveness of the company’s Drive25 cost optimization program.

While regional performance varies, with particular strength in Europe & Sub-Saharan Africa, the company’s global diversification and strong backlog of $2.3 billion provide visibility for future revenue. The focus on technology deployment and operational efficiency positions Expro to potentially achieve its medium-term financial targets.

However, investors should note that despite these positive operational trends, Expro’s stock remains significantly below its 52-week high, suggesting the market may still be cautious about the company’s long-term prospects or broader industry challenges. The coming quarters will be crucial in determining whether Expro can maintain its positive momentum and convince investors that its operational improvements will translate into sustained shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.