Trump says Nvidia not allowed to sell advanced AI chips to China- 60 Minutes

Introduction & Market Context

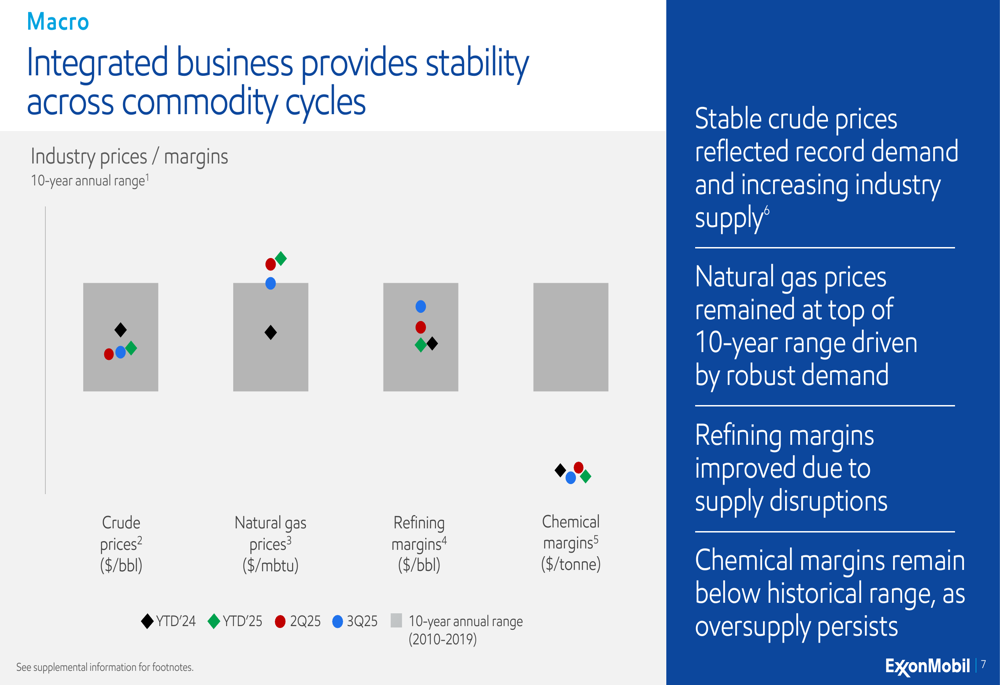

ExxonMobil (NYSE:XOM) reported strong third-quarter 2025 results on October 31, delivering $7.5 billion in GAAP earnings amid a mixed commodity price environment. The oil giant’s integrated business model provided stability as crude prices remained steady, natural gas prices held at the top of their 10-year range, and refining margins improved due to supply disruptions.

The company’s stock dipped slightly in pre-market trading by 0.44% to $114.19 despite exceeding analyst expectations, with earnings per share of $1.88 surpassing the forecast of $1.83. During regular trading, the stock continued its decline, falling 0.82% to $114.69.

As shown in the following slide highlighting market conditions across ExxonMobil’s business segments:

Quarterly Performance Highlights

ExxonMobil’s third-quarter performance demonstrated the company’s ability to execute effectively across its portfolio. GAAP earnings reached $7.5 billion, with earnings excluding identified items at $8.1 billion. Cash flow from operations was particularly strong at $14.8 billion, driven by record production in the Permian Basin and Guyana.

The company returned $9.4 billion to shareholders during the quarter, including $5.1 billion in share buybacks, while maintaining an industry-leading balance sheet with a net debt-to-capital ratio of just 9.5%.

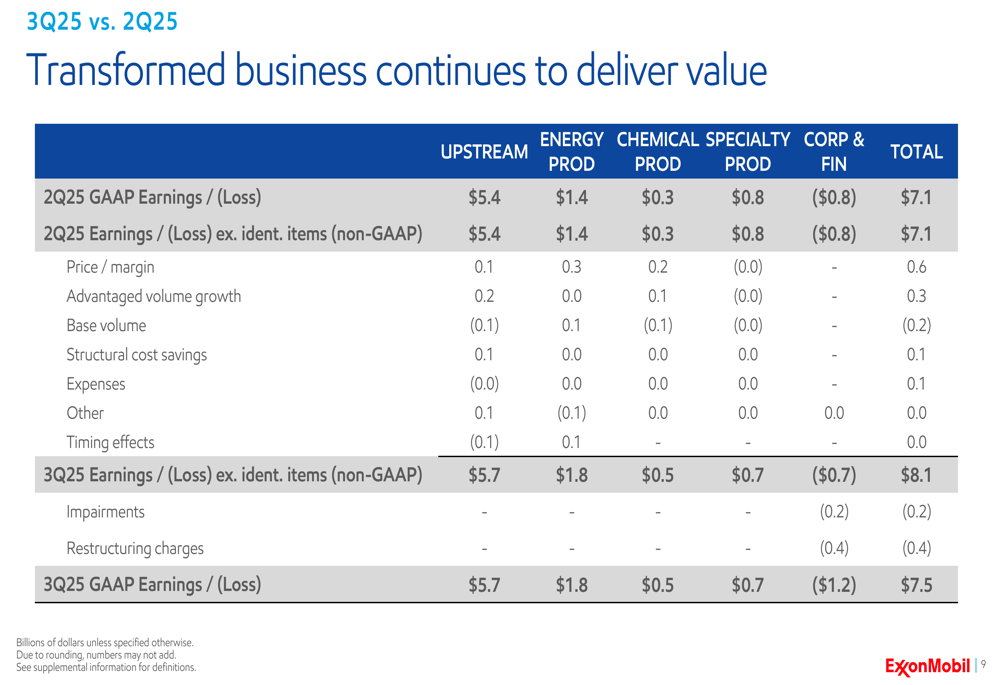

The following slide summarizes ExxonMobil’s key financial results for the third quarter:

Quarter-over-quarter performance showed improvement, with GAAP earnings increasing from $7.1 billion in Q2 2025 to $7.5 billion in Q3 2025. This growth was primarily driven by favorable price/margin impacts of $0.6 billion and advantaged volume growth of $0.3 billion, partially offset by base volume decline and expenses.

Strategic Initiatives and Project Execution

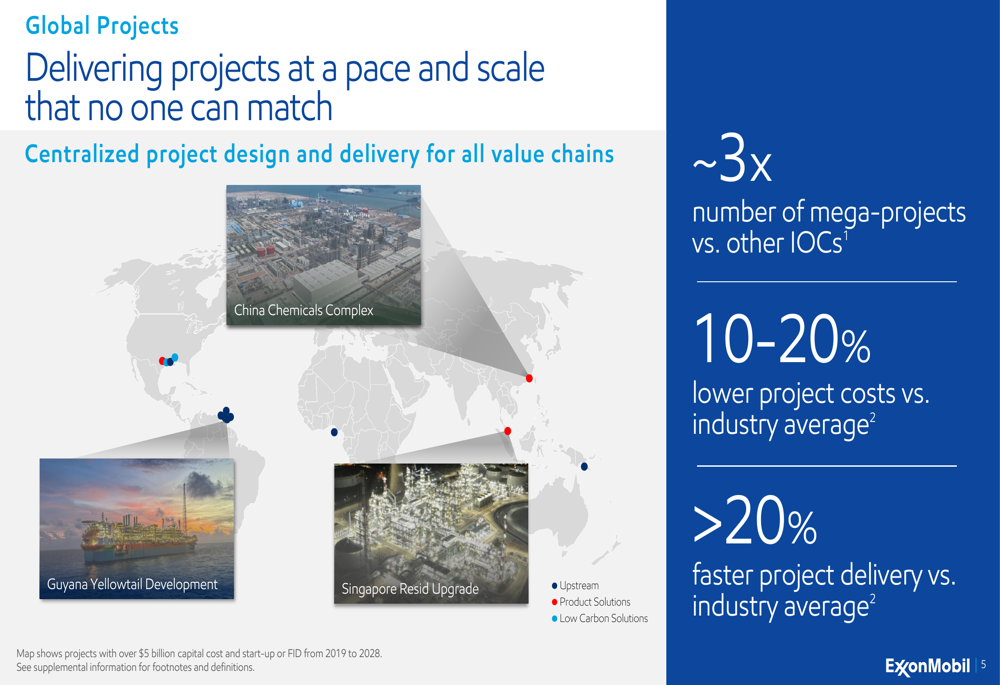

ExxonMobil continues to demonstrate strong project execution capabilities, with 8 of 10 key 2025 projects successfully started up and the remaining two on track. The company highlighted its centralized project design and delivery approach, claiming approximately three times the number of mega-projects compared to other international oil companies, with 10-20% lower project costs and more than 20% faster project delivery versus industry averages.

Strategic investments during the quarter included the Superior Graphite acquisition, Permian acreage acquisitions, and investment in a next-generation supercomputer, all aimed at maximizing long-term value.

The following slide illustrates ExxonMobil’s global project footprint and execution capabilities:

Financial Analysis and Cost Discipline

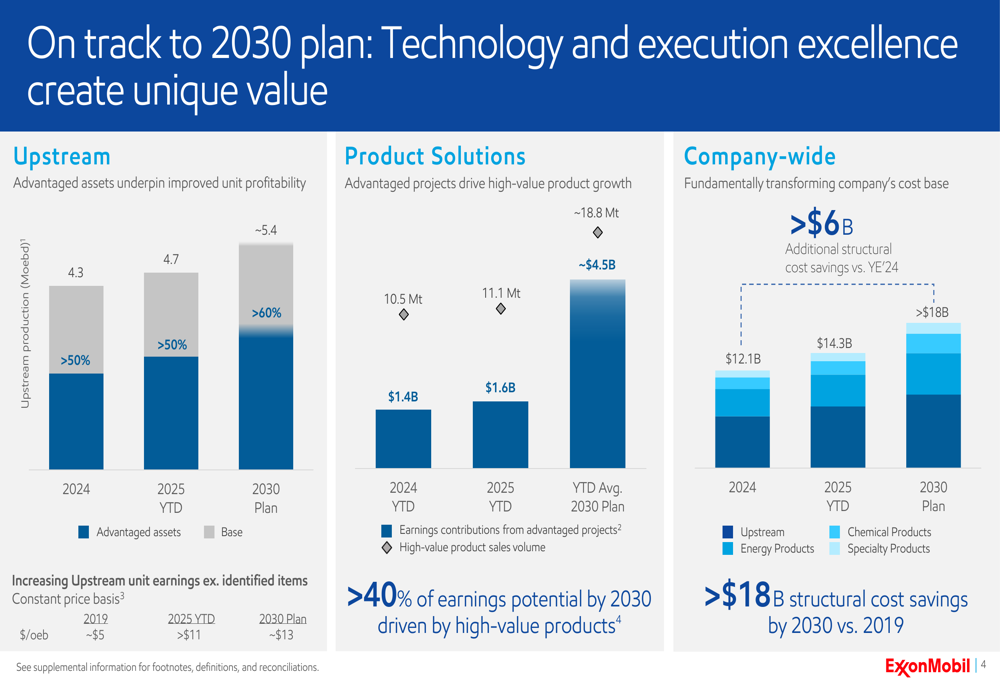

A cornerstone of ExxonMobil’s strategy continues to be rigorous cost discipline. The company has achieved $14.3 billion in structural cost savings compared to 2019 and remains on track to deliver more than $18 billion in savings by 2030. This focus on cost efficiency has helped maintain profitability despite fluctuations in commodity prices.

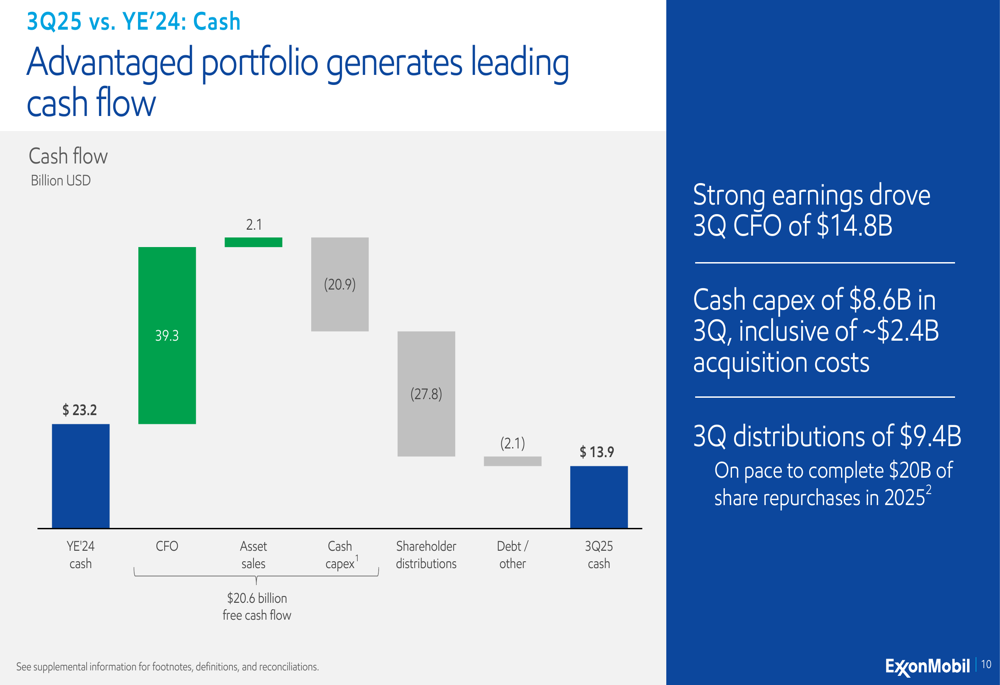

Cash flow management has been equally impressive, with the company starting the year with $23.2 billion in cash, generating $39.3 billion from operations, and returning $27.8 billion to shareholders through the third quarter.

The following cash flow waterfall chart illustrates the movement of funds during the first nine months of 2025:

ExxonMobil’s progress toward its 2030 plan shows steady improvement in unit profitability, with upstream unit earnings excluding identified items more than doubling from approximately $5 per oil-equivalent barrel in 2019 to over $11 in 2025 year-to-date, with a target of approximately $13 by 2030.

The company’s product solutions segment is also seeing growth in high-value products, with sales volumes increasing from 10.5 million tonnes in 2024 to 11.1 million tonnes in 2025 year-to-date, targeting approximately 18.8 million tonnes by 2030.

Forward-Looking Statements

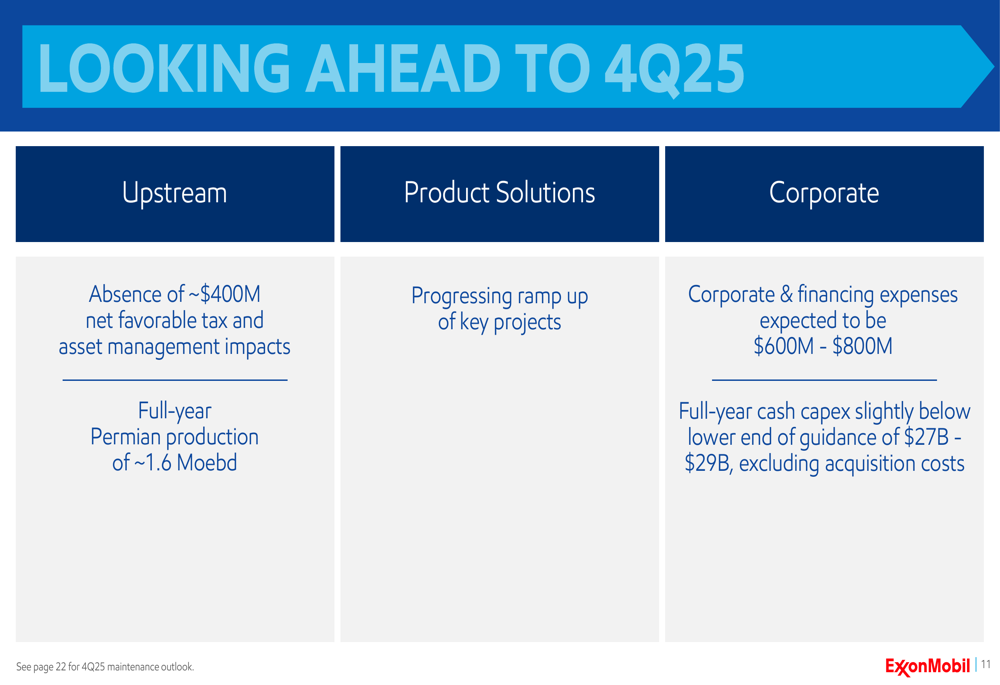

Looking ahead to the fourth quarter of 2025, ExxonMobil expects the absence of approximately $400 million in net favorable tax and asset management impacts in the upstream segment. The company projects full-year Permian production to reach approximately 1.6 million oil-equivalent barrels per day.

In the product solutions segment, ExxonMobil is progressing with the ramp-up of key projects. Corporate and financing expenses are expected to be between $600 million and $800 million for the fourth quarter.

Notably, the company anticipates full-year cash capital expenditures to come in slightly below the lower end of its $27 billion to $29 billion guidance range, excluding acquisition costs. This disciplined capital approach, combined with the company’s increased quarterly dividend of $1.03 per share (marking the 43rd consecutive year of higher dividend-per-share annual payments), underscores ExxonMobil’s commitment to balancing growth investments with shareholder returns.

CEO Darren Woods emphasized the company’s strategic focus during the earnings call, stating, "We buy value, not volume," and highlighted the successful execution of challenging commitments. He also noted the impact of technical innovation on the company’s performance, saying, "Our longstanding focus on and investment in technical innovation is paying dividends."

As ExxonMobil continues to execute its long-term strategy, the company appears well-positioned to navigate market volatility while delivering on its commitments to shareholders, though investors will be watching closely to see if the slight stock decline signals broader concerns about the energy sector’s outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.