Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Farmers & Merchants Bancorp Inc (NASDAQ:FMAO) recently presented its second quarter 2025 investor presentation, highlighting continued financial strength and strategic growth initiatives. The Ohio-based community bank, which serves communities across Northwest Ohio, Northeast Indiana, and Southern Michigan, reported modest asset growth alongside more substantial improvements in profitability metrics.

FMAO shares are currently trading at $25.16, down 3.42% year-to-date, with a 52-week range of $20.88 to $34.15. The bank continues to position itself as a leading regional financial institution with a strong focus on agricultural lending and community banking.

Quarterly Performance Highlights

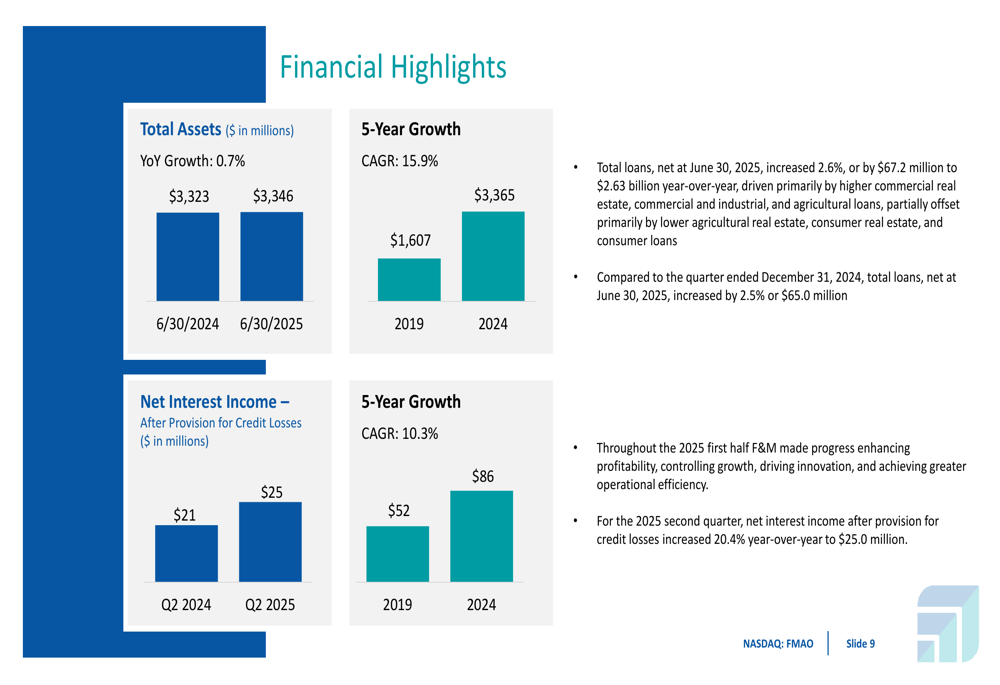

For the second quarter of 2025, F&M reported significant improvement in net interest income after provision for credit losses, which increased 20.4% year-over-year to $25.0 million. Total assets reached $3,346 million as of June 30, 2025, representing a modest 0.7% increase from $3,323 million a year earlier.

Total loans increased 2.6% year-over-year, or by $67.2 million, to $2.63 billion as of June 30, 2025. This steady loan growth reflects the bank’s conservative approach to expansion while maintaining strong credit quality.

As shown in the following financial highlights:

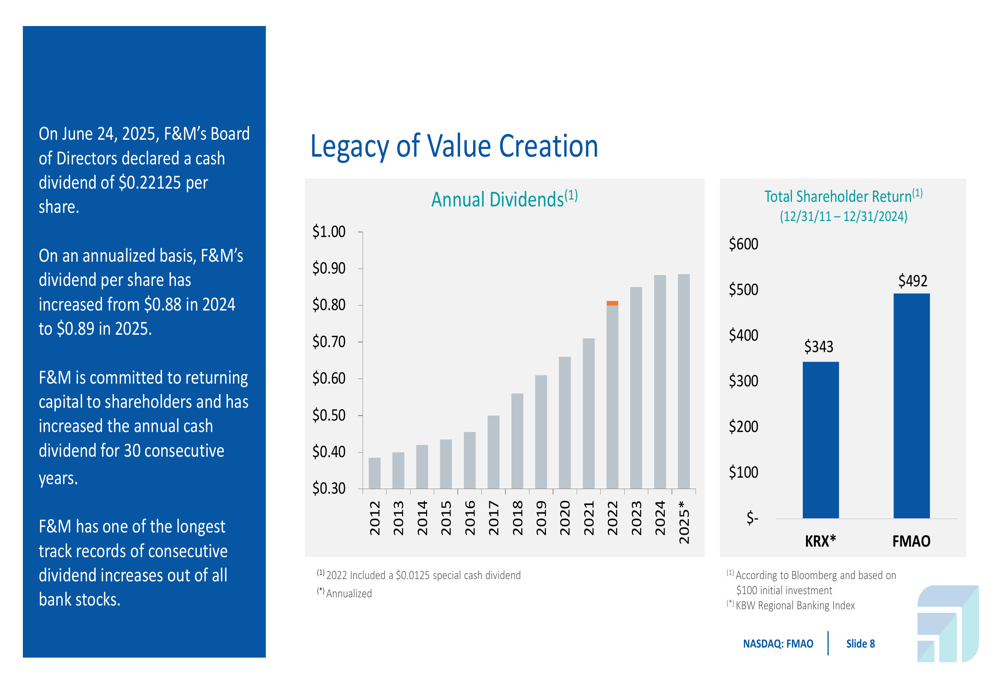

The bank’s board of directors declared a quarterly cash dividend of $0.22125 per share on June 24, 2025, which amounts to $0.89 annualized. This marks the 30th consecutive year of dividend increases for F&M, underscoring its commitment to shareholder returns.

Strategic Growth Initiatives

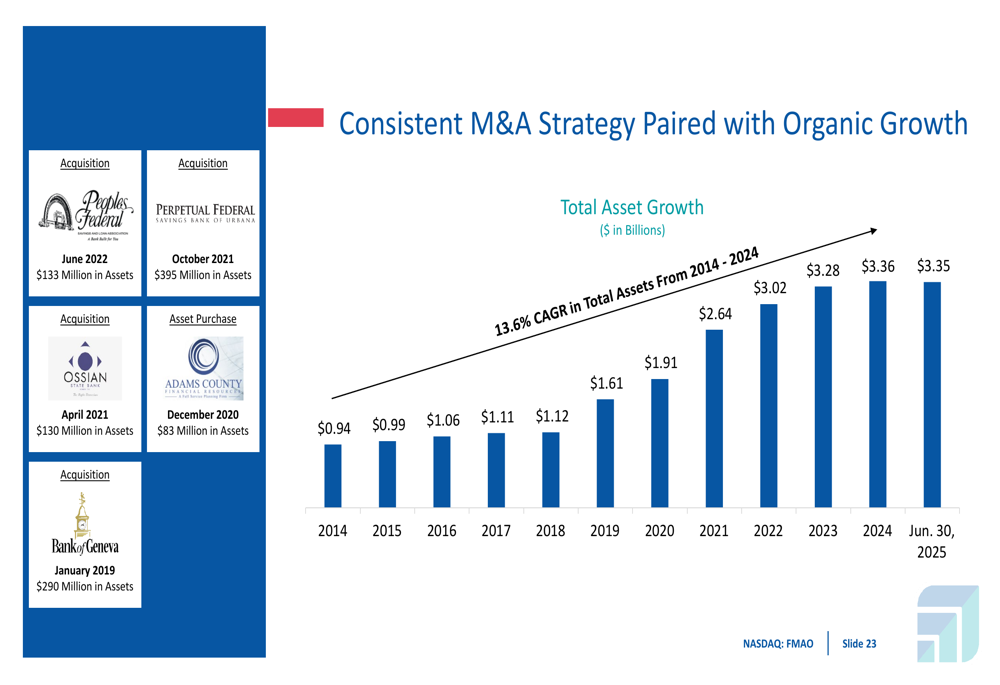

F&M has implemented a three-year strategic plan focused on enhancing profitability, controlling growth, continuous innovation, and operational efficiency. The bank has been expanding its footprint through both organic growth and strategic acquisitions, with four successful acquisitions completed between 2019 and 2022.

The bank’s total assets have grown at a compound annual growth rate (CAGR) of 15.9% from 2019 to 2024, demonstrating the effectiveness of its expansion strategy. This growth trajectory is illustrated in the following chart:

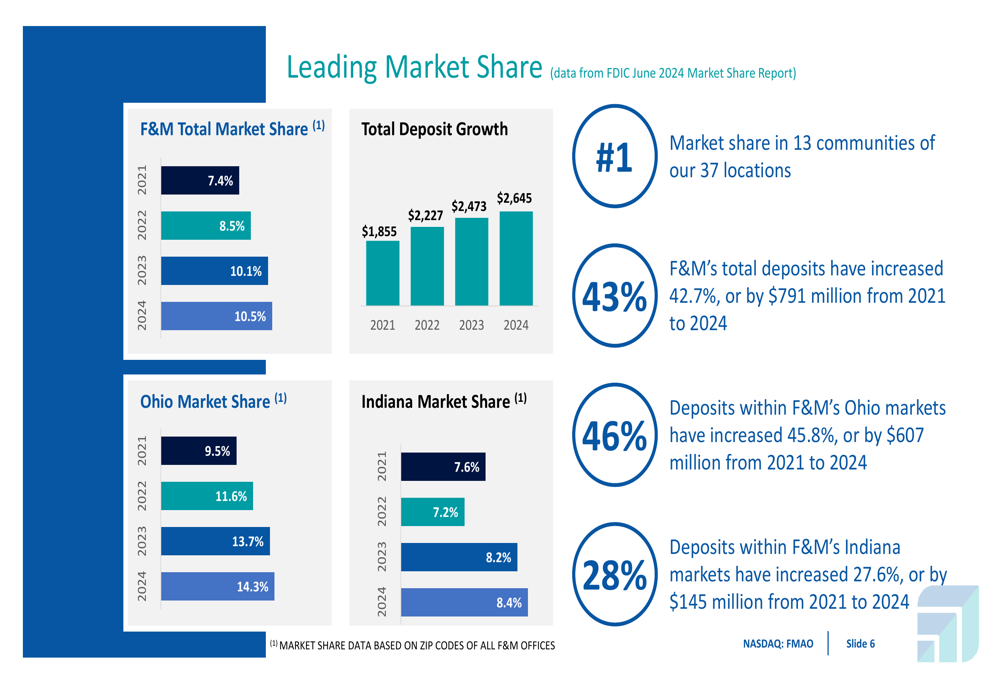

F&M has also been focused on deposit growth, with total deposits increasing by 42.7% or $791 million from 2021 to 2024. The bank holds the #1 market share position in 13 communities across its 37 locations, with particularly strong performance in its Ohio markets.

New offices opened in 2023 in Fort Wayne, IN, Birmingham, MI, Toledo, OH, and Oxford, OH have already contributed $53.9 million in new deposits and $80.5 million in new loans during 2024, showing early success in the bank’s geographic expansion strategy.

Credit Quality and Risk Management

F&M maintains a conservative approach to lending, with strong asset quality metrics as of June 30, 2025. The bank reported an allowance for credit losses (ACL) to total loans ratio of 1.07%, non-performing assets to total assets of just 0.11%, and net charge-offs to loans of 0.00%.

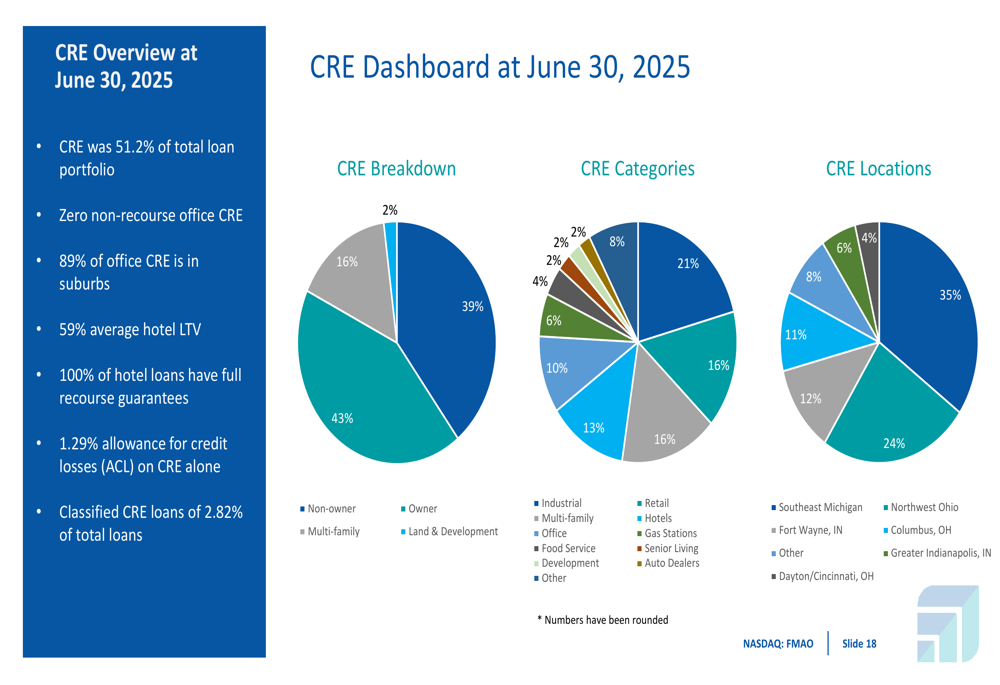

The bank’s commercial real estate (CRE) portfolio, which represents 51.2% of total loans, is well-diversified across property types and geographic locations. The following chart provides a detailed breakdown of the CRE portfolio:

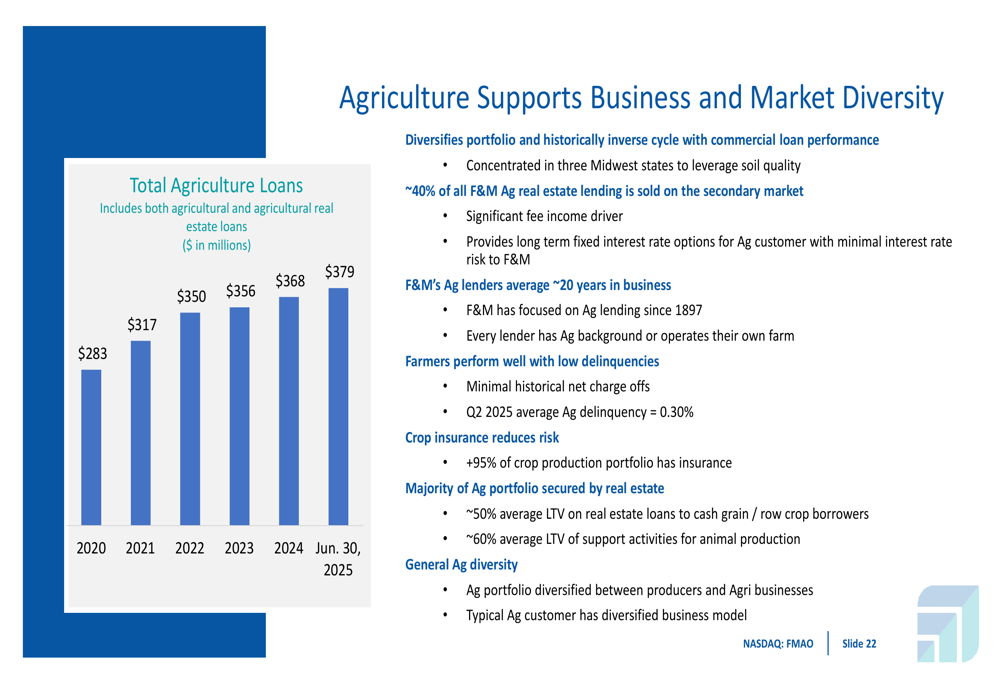

Agricultural lending remains a key differentiator for F&M, with total agricultural loans reaching $379 million as of June 30, 2025. The agricultural portfolio has historically demonstrated an inverse cycle with commercial loan performance, providing valuable diversification benefits.

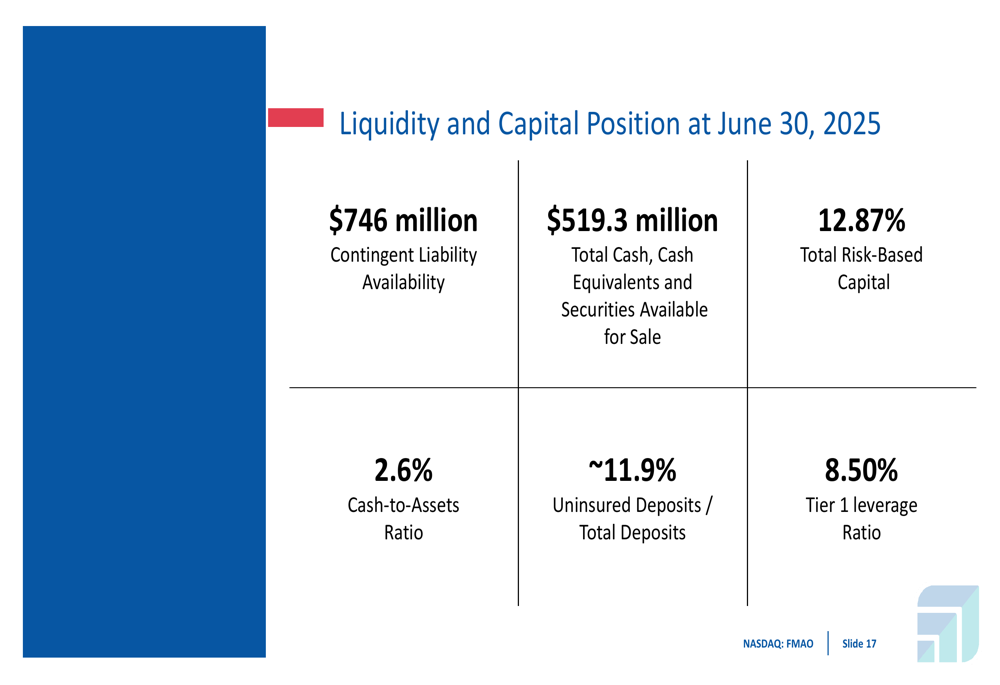

The bank maintains a strong liquidity and capital position, with $746 million in contingent liability availability and $519.3 million in total cash, cash equivalents, and securities available for sale. Capital ratios remain robust, with a total risk-based capital ratio of 12.87% and a Tier 1 leverage ratio of 8.50%.

Forward-Looking Statements

Looking ahead, F&M is focused on four key priorities for 2025: enhancing profitability by leveraging prior investments, controlling growth with a focus on low-cost deposits, continuous innovation to improve customer experience, and operational efficiency.

The bank is well-positioned to benefit from loan repricing opportunities, with approximately 36% of its loan portfolio subject to repricing within the next 12 months. This should support net interest margin expansion in a stable or declining rate environment.

F&M’s strategic focus on digital transformation is already showing results, with significant increases in digital engagement across multiple channels. The bank reported a 32% increase in Positive Pay customers, a 29% increase in digital wallet cards enrolled, and a 27% increase in mobile app customers.

With its strong market position, consistent financial performance, and conservative risk management approach, Farmers & Merchants Bancorp appears well-positioned to continue its growth trajectory while maintaining its 30-year tradition of increasing dividends for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.