Fed’s Powell opens door to potential rate cuts at Jackson Hole

Introduction & Market Context

Ferroglobe PLC (NASDAQ:GSM), a leading producer of silicon metal, silicon-based alloys, and manganese-based alloys, presented its first quarter 2025 results on May 8, 2025. Despite reporting negative adjusted EBITDA for the quarter, the company maintained its full-year guidance, citing expectations for significant improvement in the coming quarters.

The specialty metals producer faced a challenging market environment in Q1, characterized by soft pricing and weak demand, particularly in the silicon metal segment. However, management highlighted several positive developments, including favorable trade decisions in the U.S. and EU, which are expected to benefit the company throughout the remainder of the year.

Quarterly Performance Highlights

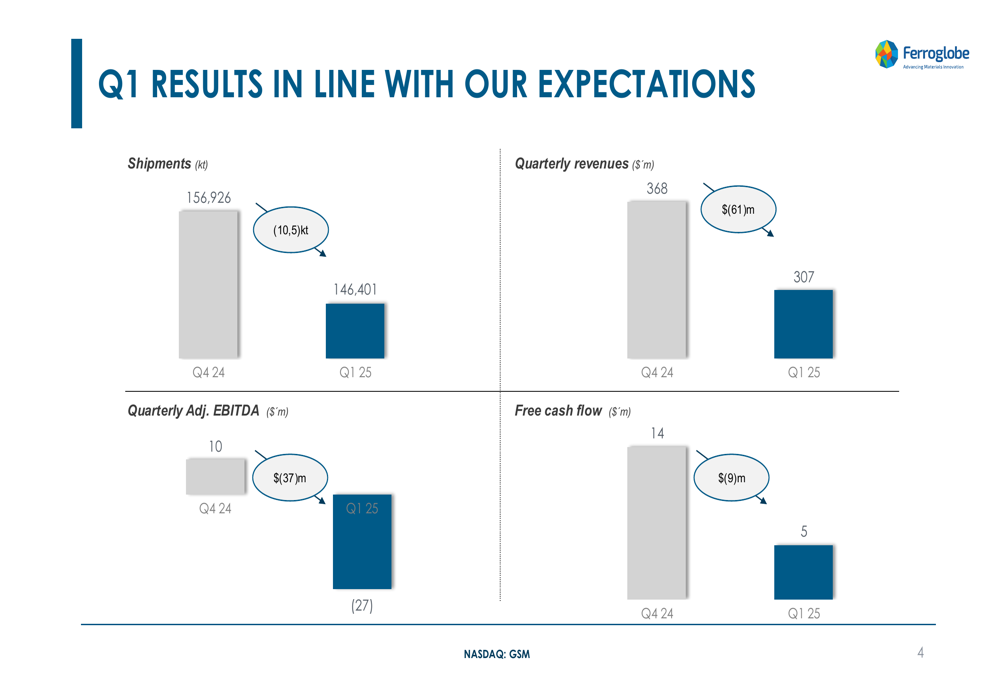

Ferroglobe reported Q1 2025 revenue of $307.2 million, down 16.4% from $367.5 million in the previous quarter. The company posted an adjusted EBITDA loss of $26.8 million, compared to a positive $9.8 million in Q4 2024, resulting in an adjusted EBITDA margin of -9%.

As shown in the following chart comparing Q1 2025 results with Q4 2024, shipments declined by 10.5kt, while revenues fell by $61 million and adjusted EBITDA decreased by $37 million:

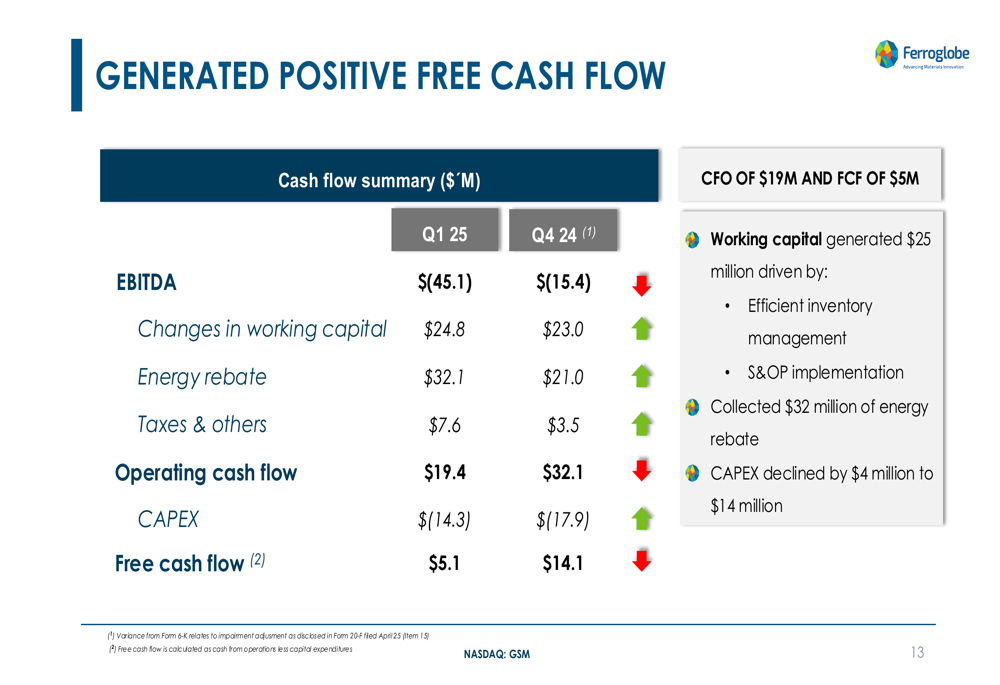

Despite these challenges, Ferroglobe generated positive free cash flow of $5.1 million, down from $14.1 million in the previous quarter. This was achieved through efficient working capital management, which released $25 million, and the collection of a $32 million energy rebate.

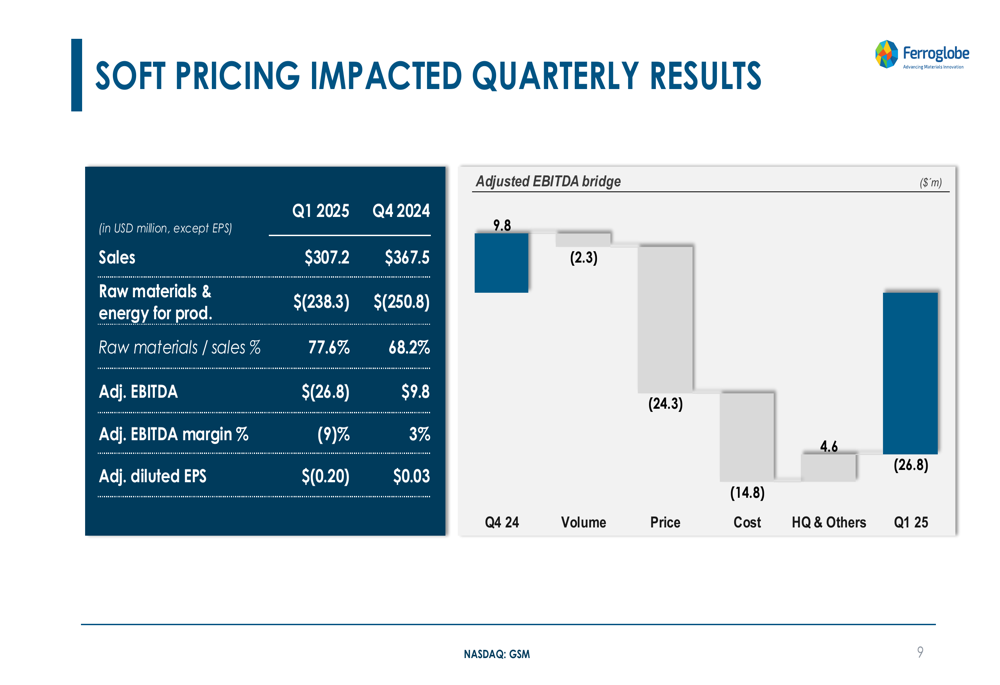

The company’s financial performance breakdown reveals how soft pricing significantly impacted quarterly results:

Detailed Financial Analysis

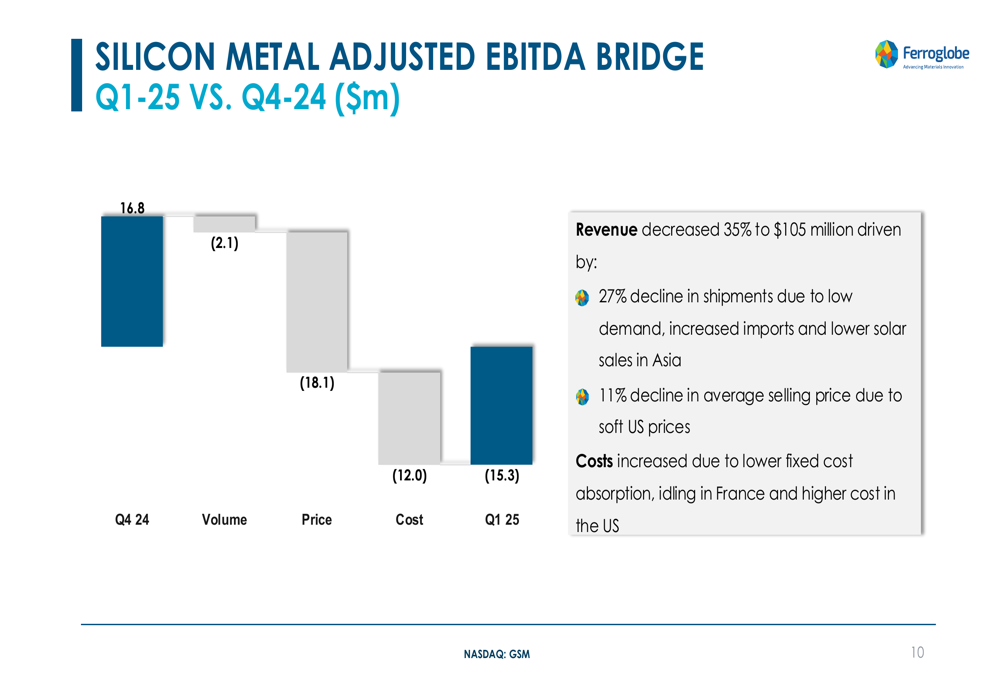

Looking at segment performance, the Silicon Metal division was particularly hard hit, with revenue decreasing 35% to $105 million. This decline was driven by a 27% reduction in shipments due to low demand, increased imports, and lower solar sales in Asia, combined with an 11% decline in average selling price.

The Silicon Metal segment’s adjusted EBITDA bridge illustrates the transition from a positive $16.8 million in Q4 2024 to a negative $15.3 million in Q1 2025:

By contrast, the Silicon Based Alloys segment showed some resilience, with revenue increasing 7% to $91 million, driven by a 9% increase in shipments, primarily in North America. This was partially offset by a 1.8% decline in average selling price due to a higher proportion of lower-grade FeSi standard sales.

The Manganese Based Alloys segment saw revenue decrease by 5% to $74 million, resulting from a 1% decline in shipments and a 4% decline in average selling price due to product mix changes.

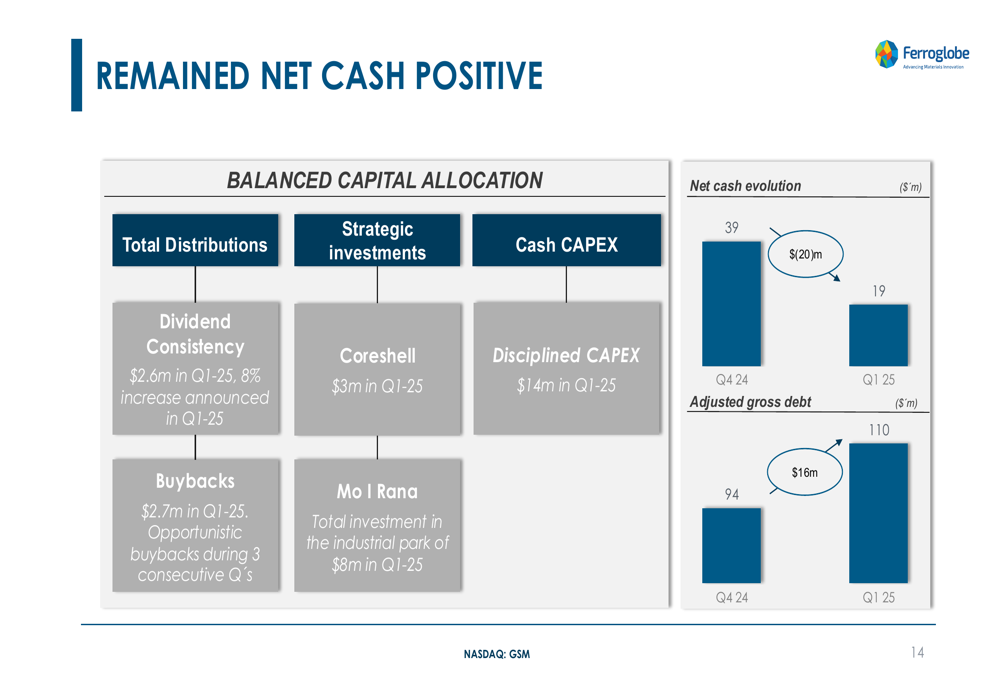

Despite the challenging quarter, Ferroglobe maintained positive free cash flow through disciplined financial management:

The company also remained net cash positive, though net cash declined from $39 million in Q4 2024 to $19 million in Q1 2025. Ferroglobe continued its balanced capital allocation strategy, increasing quarterly dividends by 8% while conducting opportunistic share buybacks for the third consecutive quarter.

Strategic Initiatives & Outlook

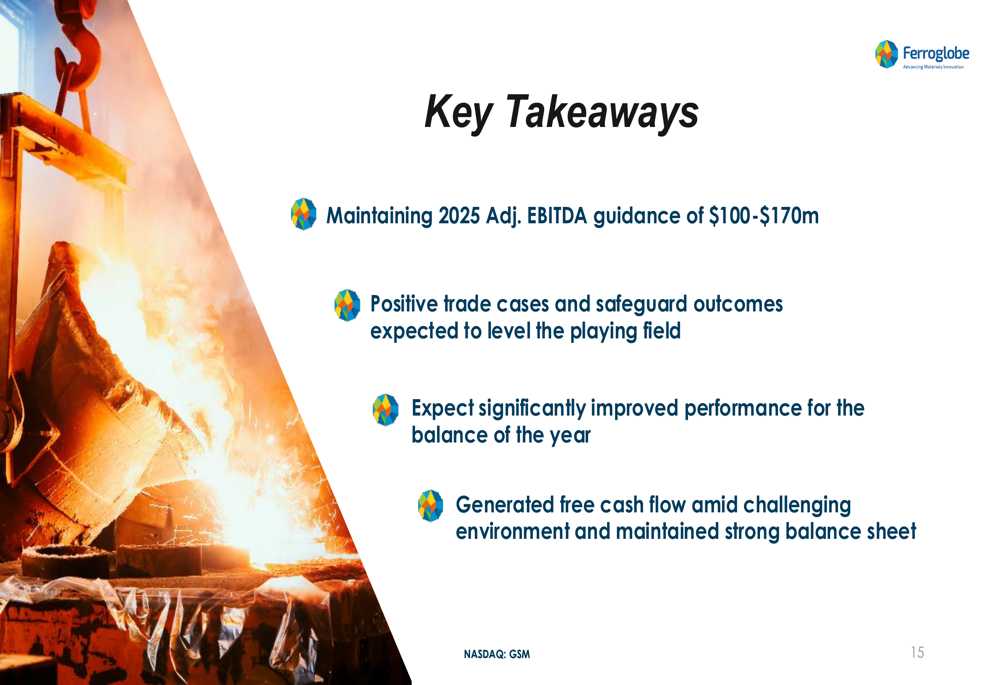

Ferroglobe maintained its 2025 adjusted EBITDA guidance of $100-$170 million, suggesting management expects significant improvement in the remaining quarters. The company indicated that Q1 likely marked the "trough" of sales for the year, with volume expected to increase significantly in Q2.

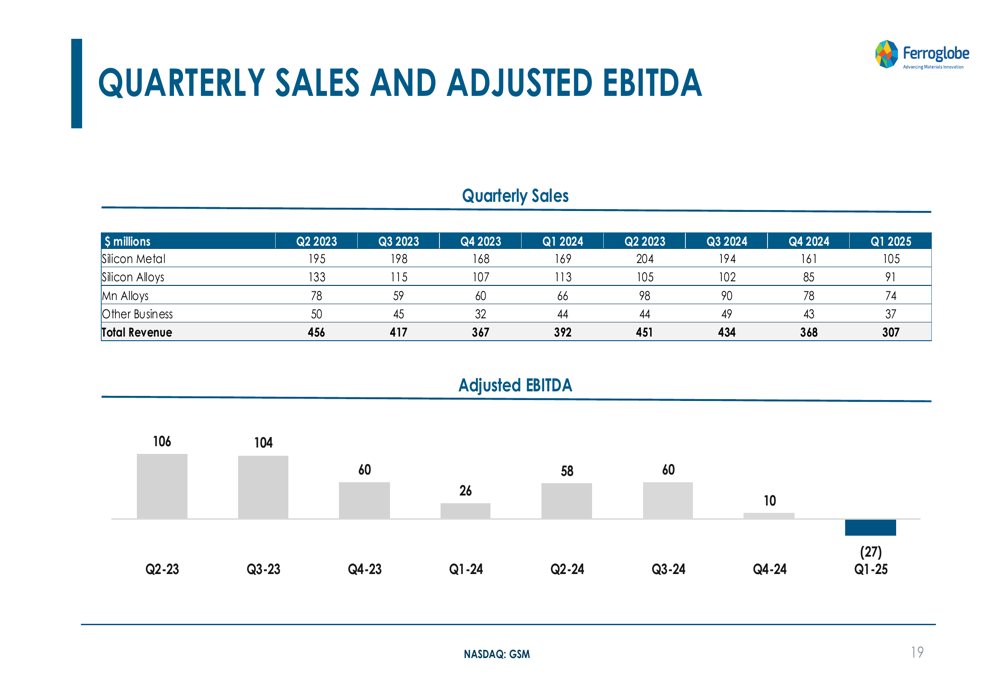

The historical quarterly performance chart shows the volatility in the company’s results over the past two years, with the recent quarter representing a notable downturn:

Management highlighted several factors expected to drive improvement:

1. Favorable trade decisions in the U.S. and EU that should "level the playing field"

2. Initial signs of positive impact from the U.S. trade case, with a 17% increase in U.S. FeSi index prices since early April

3. Potential benefits from EU safeguard implementation

4. Anticipated recovery in demand across key markets

Forward-Looking Statements

Ferroglobe’s key takeaways emphasized its confidence in achieving the full-year guidance despite the challenging start to 2025:

The company’s ability to generate positive free cash flow and maintain a strong balance sheet during a difficult quarter demonstrates financial discipline. However, the significant gap between current performance and full-year targets suggests substantial improvement will be needed in subsequent quarters.

For investors, the critical question remains whether the anticipated benefits from trade cases and market improvements will materialize quickly enough and with sufficient impact to achieve the projected annual results. The company’s maintained guidance indicates management’s confidence, but execution in the coming quarters will be crucial to meeting these targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.