SoFi CEO enters prepaid forward contract on 1.5 million shares

Introduction & Market Context

Ferroglobe PLC (NASDAQ:GSM) presented its second quarter 2025 financial results on August 6, showcasing a substantial improvement over the first quarter despite ongoing market challenges. The specialty metals producer has withdrawn its guidance due to market uncertainty but remains optimistic about a potential rebound in 2026.

The company cited changing trade dynamics, delays in EU safeguard decisions, and increased Chinese imports as key factors creating limited visibility in the market. Despite these headwinds, Ferroglobe was added to the Russell 2000 and 3000 indexes on June 30, 2025, marking an important milestone for the company.

As shown in the following slide highlighting key market challenges and the company’s positioning:

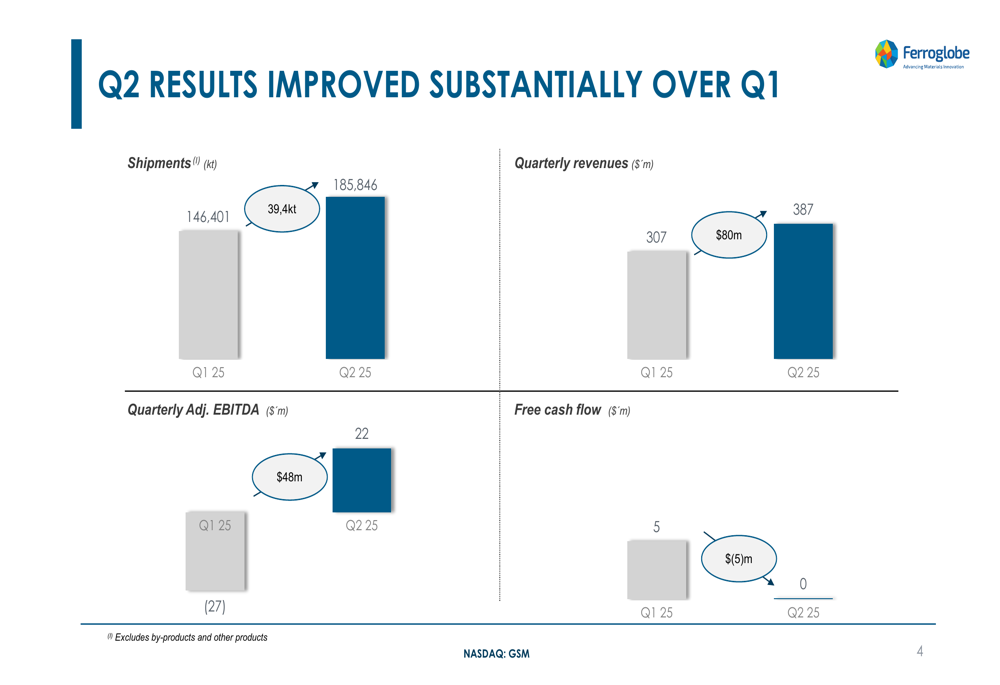

Quarterly Performance Highlights

Ferroglobe reported a significant improvement in its second quarter performance compared to Q1 2025. Shipments increased from 146,401kt in Q1 to 185,846kt in Q2, representing a 27% increase. This volume growth drove quarterly revenues up from $307 million to $387 million, while adjusted EBITDA turned positive at $22 million compared to a $27 million loss in the previous quarter.

The following chart illustrates the substantial quarter-over-quarter improvements across key metrics:

The company’s adjusted EBITDA margin improved from -9% in Q1 to 6% in Q2, while adjusted diluted EPS improved from -$0.20 to -$0.08. Free cash flow reached breakeven, up from -$5 million in the first quarter.

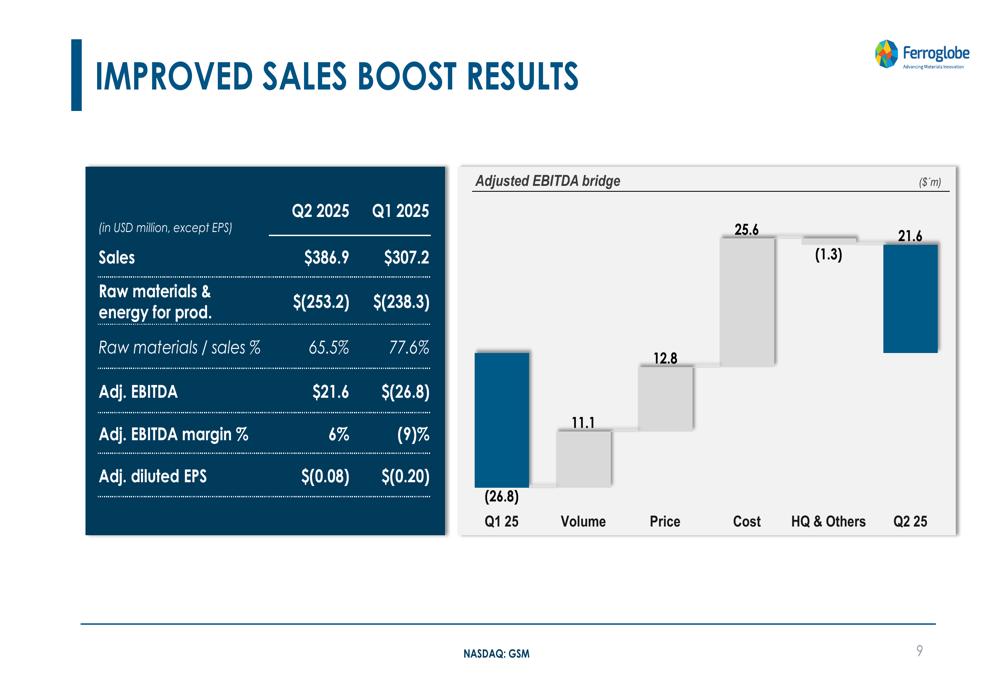

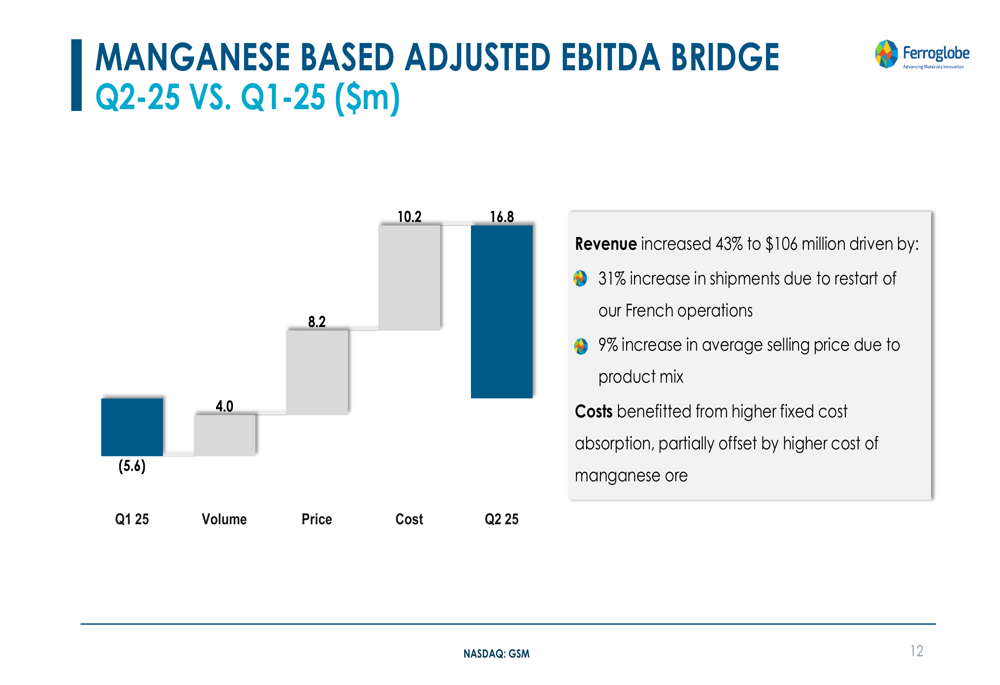

The financial improvement was driven by a combination of higher volumes, better pricing in some segments, and improved cost management, as illustrated in this EBITDA bridge:

Detailed Financial Analysis

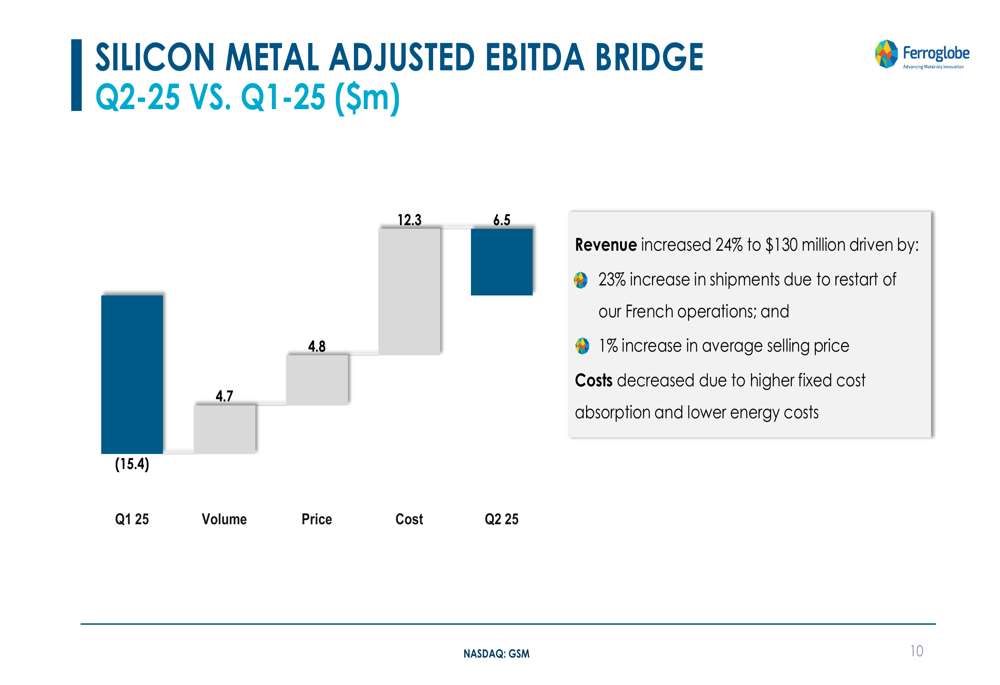

Ferroglobe’s recovery was evident across all three of its major product segments. The Silicon Metal division showed the most dramatic turnaround, improving from a $15.4 million EBITDA loss in Q1 to a positive $6.5 million in Q2. This improvement was driven by a 23% increase in shipments, particularly from French operations, and a slight 1% increase in average selling price.

The following chart breaks down the factors contributing to the Silicon Metal segment’s improvement:

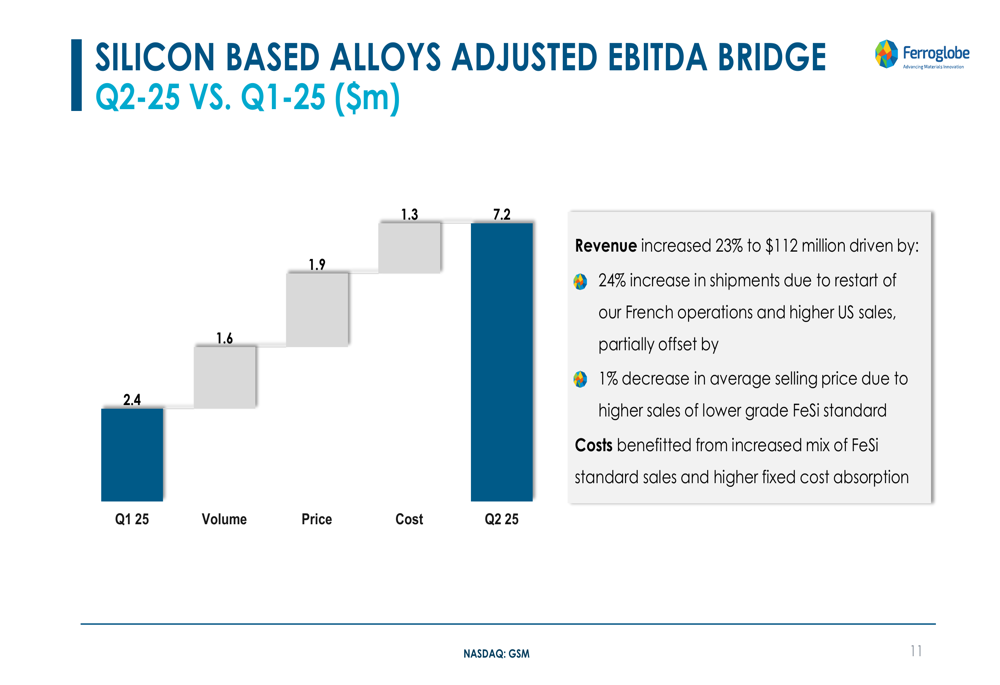

The Silicon-Based Alloys segment also showed strong performance, with EBITDA increasing from $2.4 million in Q1 to $7.2 million in Q2. Revenue increased 23% to $112 million, driven by a 24% increase in shipments, though this was partially offset by a 1% decrease in average selling price due to higher sales of lower-grade FeSi standard.

The Manganese-Based Alloys segment delivered the strongest improvement, with EBITDA increasing from a $5.6 million loss to a $16.8 million profit. Revenue increased 43% to $106 million, driven by a 31% increase in shipments and a 9% increase in average selling price.

Strategic Initiatives & Outlook

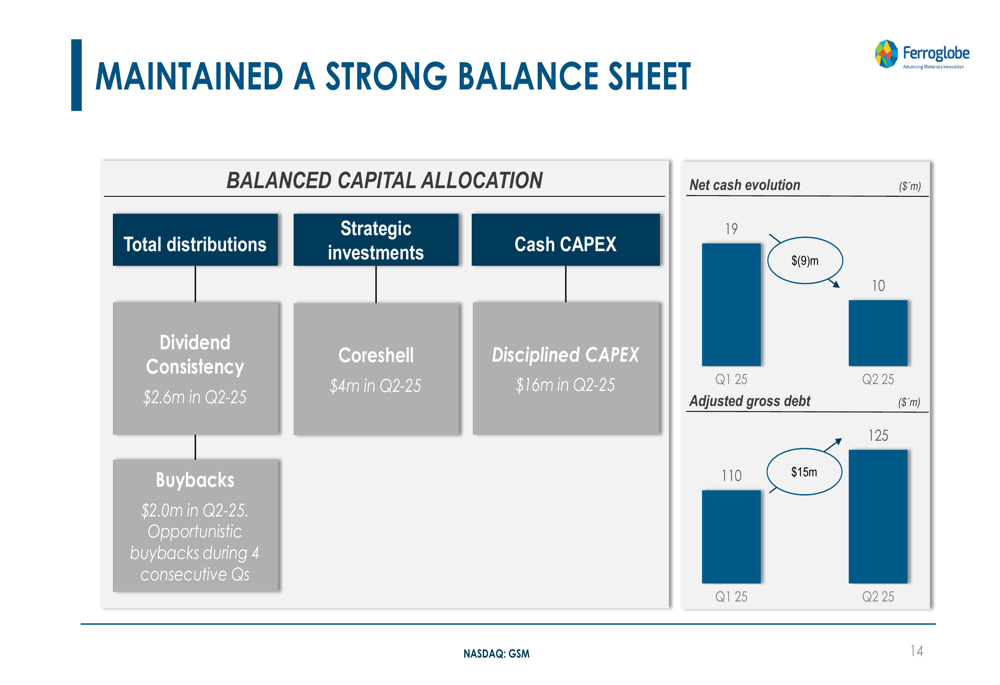

Despite challenging market conditions, Ferroglobe maintained a strong balance sheet and implemented strategic initiatives to enhance operational efficiency. The company’s S&OP (Sales and Operations Planning) implementation helped generate $14 million in working capital during the quarter.

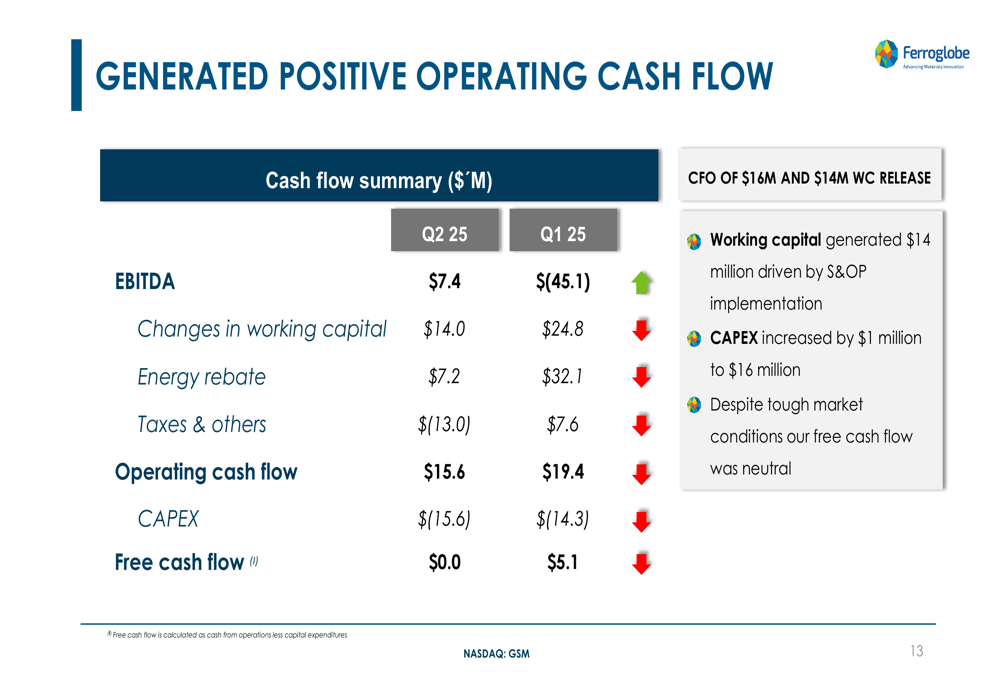

The company’s cash flow showed resilience, with operating cash flow of $15.6 million in Q2 compared to $19.4 million in Q1. Capital expenditures increased slightly to $15.6 million, resulting in neutral free cash flow for the quarter.

The following slide details the company’s cash flow performance:

Ferroglobe maintained its balanced capital allocation strategy, continuing its dividend program with $2.6 million in distributions and $2.0 million in share buybacks during Q2. The company also made a strategic investment of $4 million in Coreshell. Net cash position declined from $19 million in Q1 to $10 million in Q2, while adjusted gross debt increased from $110 million to $125 million.

Forward-Looking Statements

Ferroglobe has withdrawn its guidance due to increased uncertainty and limited visibility in the market. However, the company remains optimistic about its long-term prospects, particularly with expected improvements in 2026.

Management highlighted several factors that could positively impact future performance:

1. Ongoing EU safeguard investigation expected to reduce import-driven price pressure in the European market

2. U.S. trade policy and antidumping actions anticipated to further improve the U.S. market

3. Strong operational positioning to capitalize on market improvements as trade clarity emerges

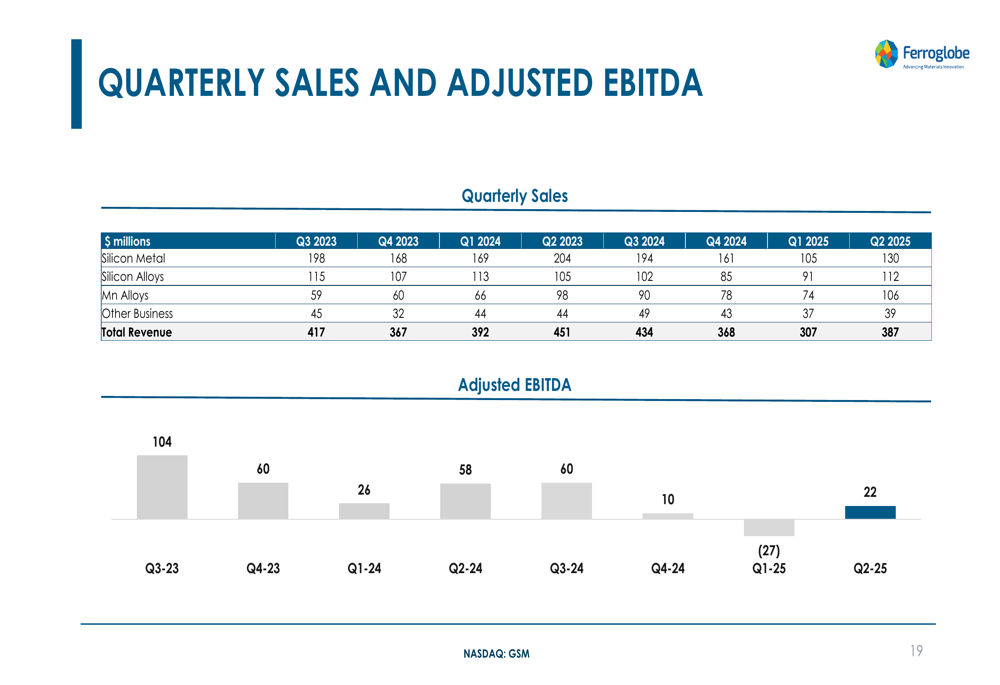

The following historical data shows the company’s quarterly sales and adjusted EBITDA performance, providing context for the recent improvement:

In summary, while Ferroglobe faces near-term market uncertainties, its Q2 2025 results demonstrate the company’s ability to execute effectively under challenging conditions. Management remains focused on maintaining financial strength while positioning for an expected market rebound in 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.