Apple investigating outages affecting Apple TV+, Apple Music services

Introduction & Market Context

First Interstate BancSystem, Inc. (NASDAQ:FIBK) presented its second quarter 2025 results on July 29, showcasing improved profitability metrics despite strategic balance sheet contraction. The Billings, Montana-based regional bank, which operates 301 banking offices across the Northwest and Midwest, reported net income of $71.7 million, or $0.69 per share, representing a significant improvement from the first quarter’s $50.2 million, or $0.49 per share.

The bank’s stock has responded positively to its strategic initiatives and improved earnings trajectory, with shares closing at $31.21 following the earnings announcement, representing a 3.49% increase. Over the past six months, FIBK has gained more than 30%, signaling growing investor confidence in the company’s strategic direction.

Quarterly Performance Highlights

First Interstate BancSystem delivered solid financial performance in Q2 2025, with net interest margin (NIM) expanding to 3.30%, a 10 basis point improvement from the previous quarter. This NIM expansion occurred despite a $1.02 billion reduction in loans and a $102.2 million decrease in deposits, highlighting the company’s focus on improving profitability over balance sheet growth.

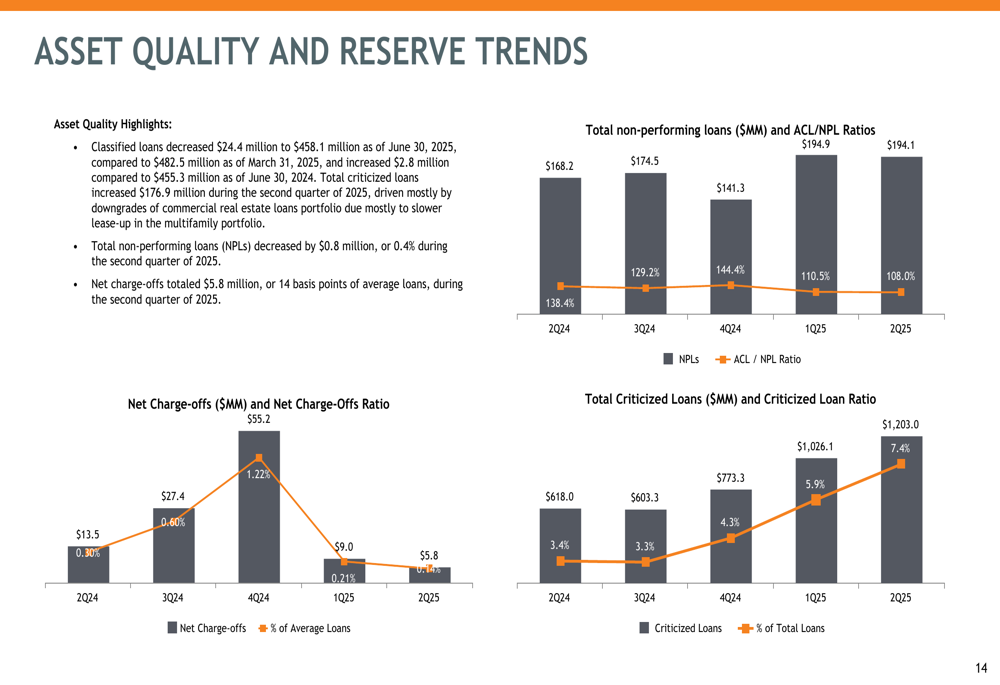

The bank maintained strong asset quality metrics, with non-performing loans decreasing by 0.4% during the quarter. Net charge-offs totaled $5.8 million, representing just 14 basis points of average loans. The allowance for credit losses increased to 1.28% of loans from 1.24% in the prior quarter, reflecting a prudent approach to credit risk management.

As shown in the following chart of asset quality and reserve trends:

The efficiency ratio improved to 61.1%, reflecting the company’s ongoing expense management efforts. This improvement in operational efficiency, combined with the expansion in net interest margin, contributed to the significant increase in quarterly earnings.

Strategic Initiatives

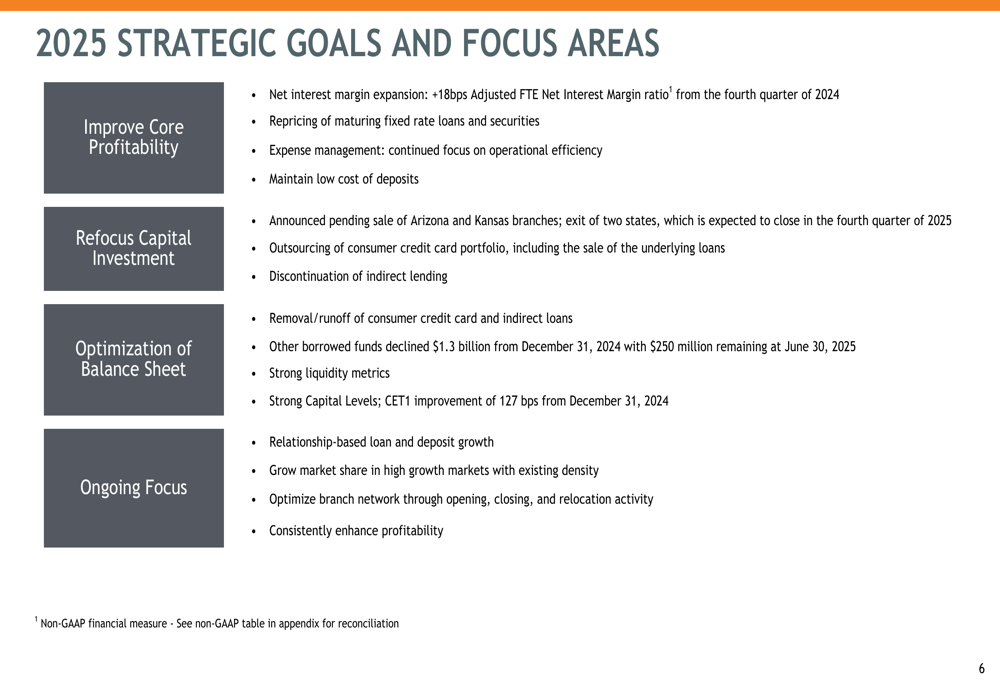

First Interstate BancSystem is implementing a comprehensive strategic repositioning to enhance core profitability and optimize its balance sheet. Key elements of this strategy include the pending sale of branches in Arizona and Kansas, outsourcing the consumer credit card portfolio, and discontinuing indirect lending operations.

The company’s strategic goals for 2025 focus on four key areas as illustrated in their presentation:

These strategic shifts are designed to refocus capital investments on higher-return opportunities while maintaining the bank’s strong capital and liquidity position. The company is prioritizing relationship-based lending and deposit growth in its core markets, where it holds dominant market positions.

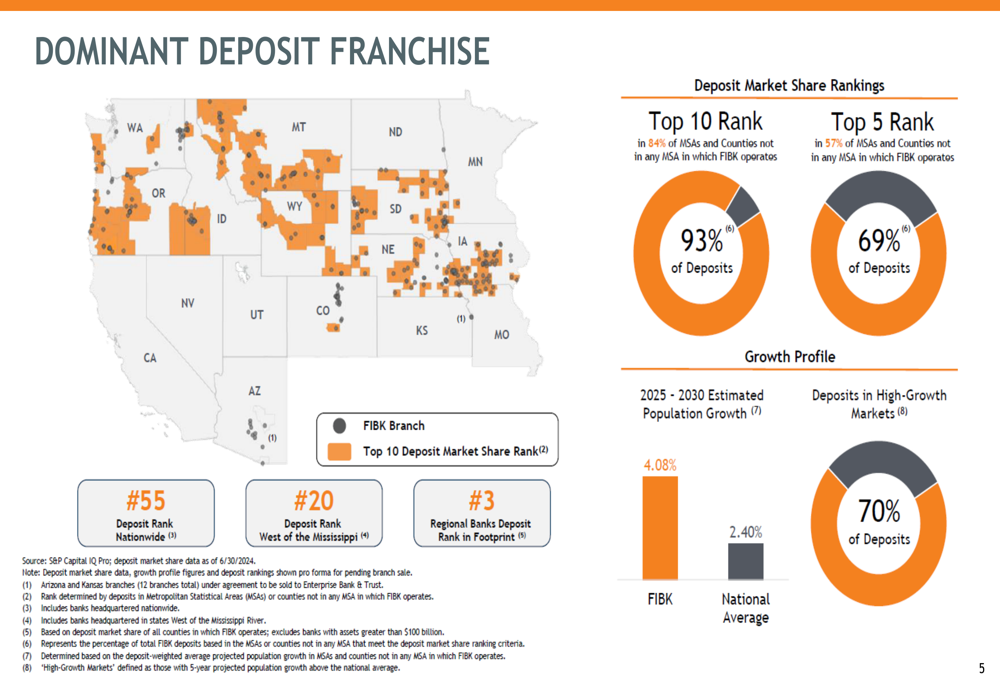

First Interstate maintains top 10 deposit market share rankings in 84% of the MSAs and counties in which it operates, and top 5 rankings in 57% of these markets. This strong competitive positioning is illustrated in the following slide:

Deposit and Loan Portfolio Analysis

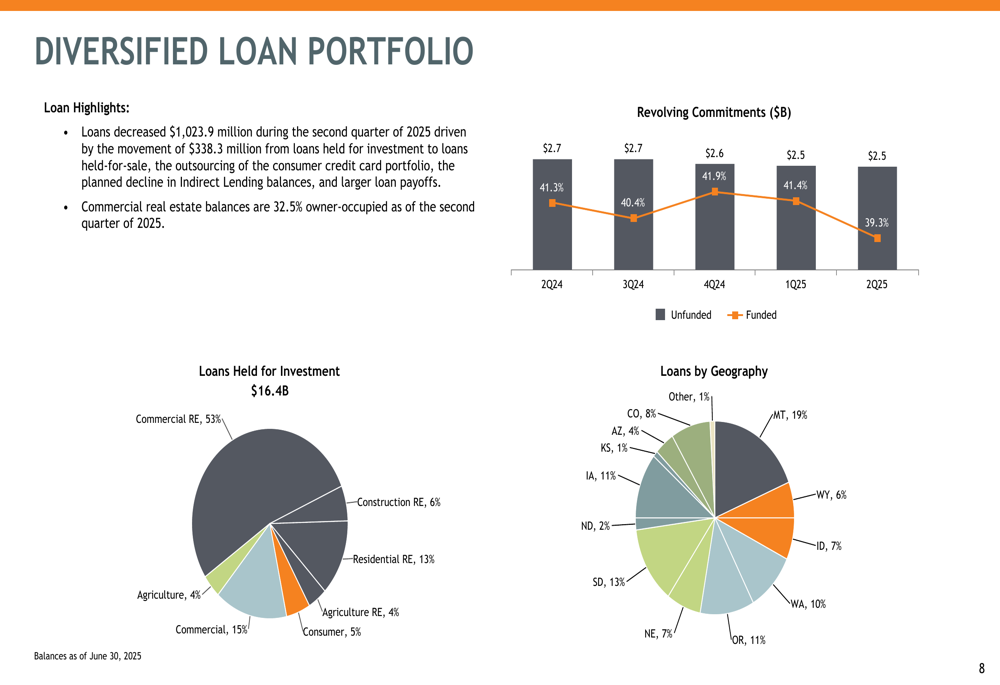

First Interstate BancSystem’s loan portfolio decreased by $1.02 billion during Q2 2025, largely reflecting the strategic decision to exit indirect lending and prepare for the sale of Arizona and Kansas operations. The company maintains a well-diversified loan portfolio, with commercial real estate representing 53% of total loans, residential real estate at 13%, commercial loans at 25%, agricultural loans at 4%, and consumer loans at 5%.

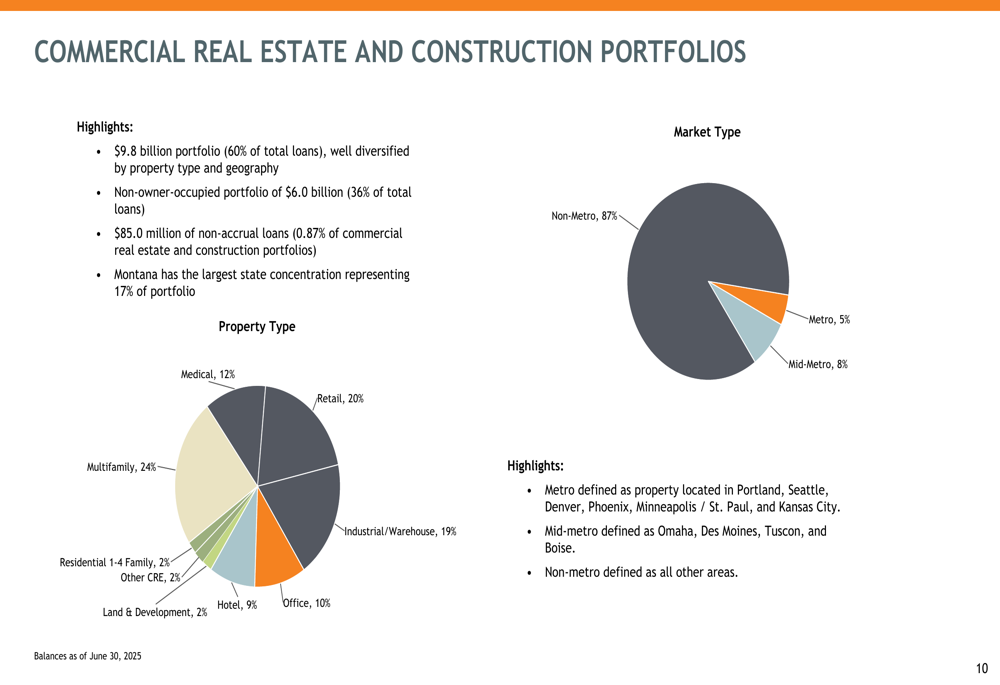

The geographic distribution of the loan portfolio is also well-diversified across the bank’s footprint, with Montana representing the largest concentration at 19% of total loans. The following chart illustrates the diversification of the loan portfolio:

The commercial real estate portfolio, which represents 60% of total loans, is well-diversified by property type and geography. Non-owner-occupied commercial real estate represents 36% of total loans, with multifamily (24%), retail (20%), and industrial/warehouse (19%) being the largest segments by property type.

On the deposit side, total deposits decreased by $102.2 million during Q2 2025, while deposit costs declined by 1 basis point from the previous quarter. The bank maintains a strong core deposit base, which supports its low funding costs and contributes to the improved net interest margin.

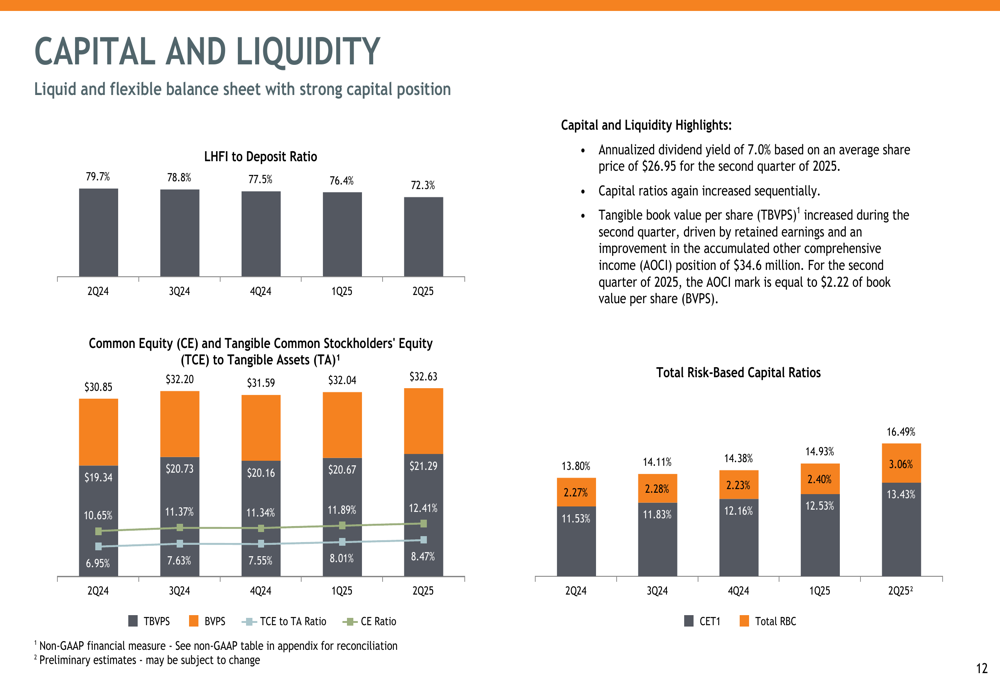

Capital Position and Shareholder Value

First Interstate BancSystem maintains robust capital ratios, with Common Equity Tier 1 (CET1) capital at 13.43% and total risk-based capital at 16.49%. The tangible common equity to tangible assets ratio stood at a healthy 8.47%. These strong capital levels provide significant flexibility to navigate the current strategic repositioning while continuing to return capital to shareholders.

The company’s capital strength and liquidity position are illustrated in the following chart:

The bank declared a quarterly dividend of $0.47 per share, representing an annualized yield of 7.0% based on the average share price of $26.95 during Q2 2025. This attractive dividend yield positions FIBK as a compelling option for income-focused investors in the regional banking sector.

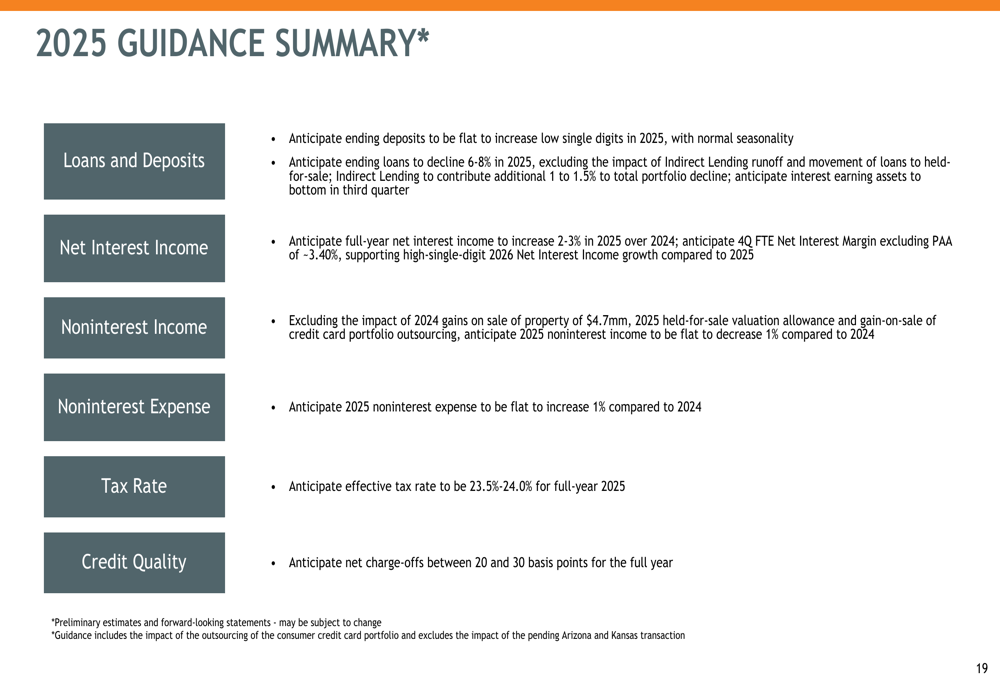

Forward-Looking Guidance

Looking ahead, First Interstate BancSystem provided guidance for the remainder of 2025, anticipating that ending loans will decline by 6-8% for the full year as the company exits certain business lines and markets. However, deposits are expected to be flat to slightly up in the low single digits.

The bank anticipates net charge-offs between 20 and 30 basis points for the full year, reflecting continued strong credit quality. Management expects high single-digit growth in net interest income in 2026, with net interest margin projected to reach 3.4% by the fourth quarter of 2025.

CEO Jim Reuter expressed confidence in the company’s future trajectory during the earnings call, stating, "We believe earnings will continue to improve through 2026 and into 2027." He emphasized that the company is "now on offense" with specific promotional activities generating positive pipeline momentum.

First Interstate BancSystem’s strategic repositioning, combined with its strong market position in high-growth regions and robust capital base, positions the bank for improved profitability and shareholder returns in the coming years, despite near-term balance sheet contraction as it exits non-core markets and business lines.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.