Raytheon awarded $71 million in Navy contracts for missile systems

Introduction & Market Context

Fidelity National Information Services (NYSE:FIS) presented its second quarter 2025 earnings results on August 5, showing stronger-than-expected revenue growth that prompted management to raise its full-year outlook. Despite the positive results, the stock was trading down 1.09% in premarket at $78.10, suggesting investors may have concerns about the company’s modest earnings growth and margin pressure.

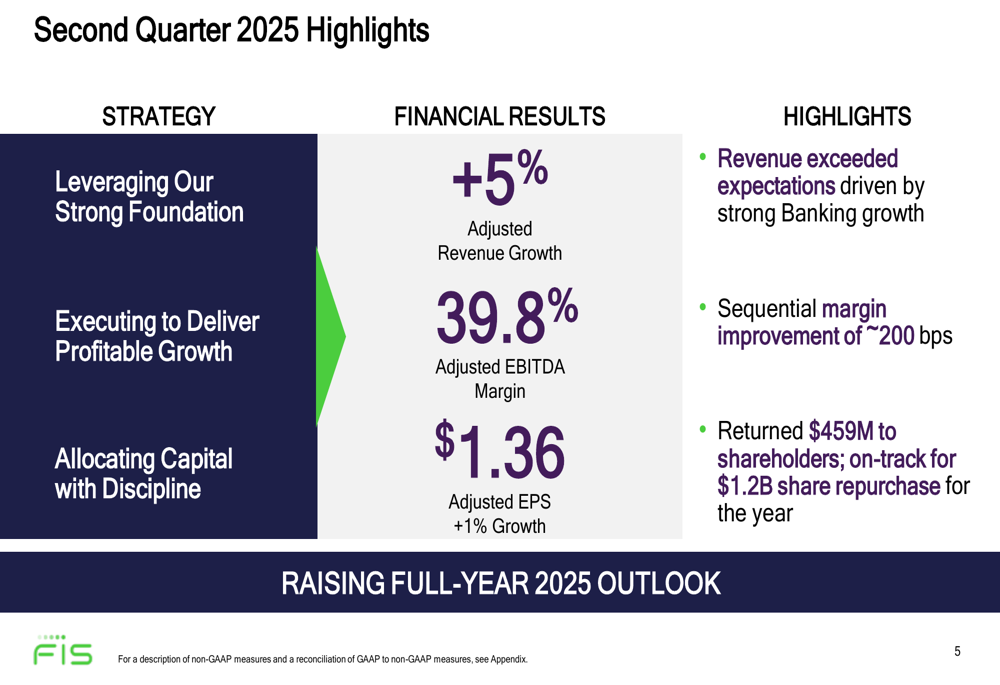

The financial technology provider reported 5% adjusted revenue growth, exceeding the previous quarter’s 4% growth rate, while adjusted earnings per share increased by just 1% year-over-year to $1.36. The company’s performance was particularly strong in its Banking Solutions segment, which grew 6% compared to just 2% in Q1.

As shown in the following comprehensive overview of the quarter’s performance:

Quarterly Performance Highlights

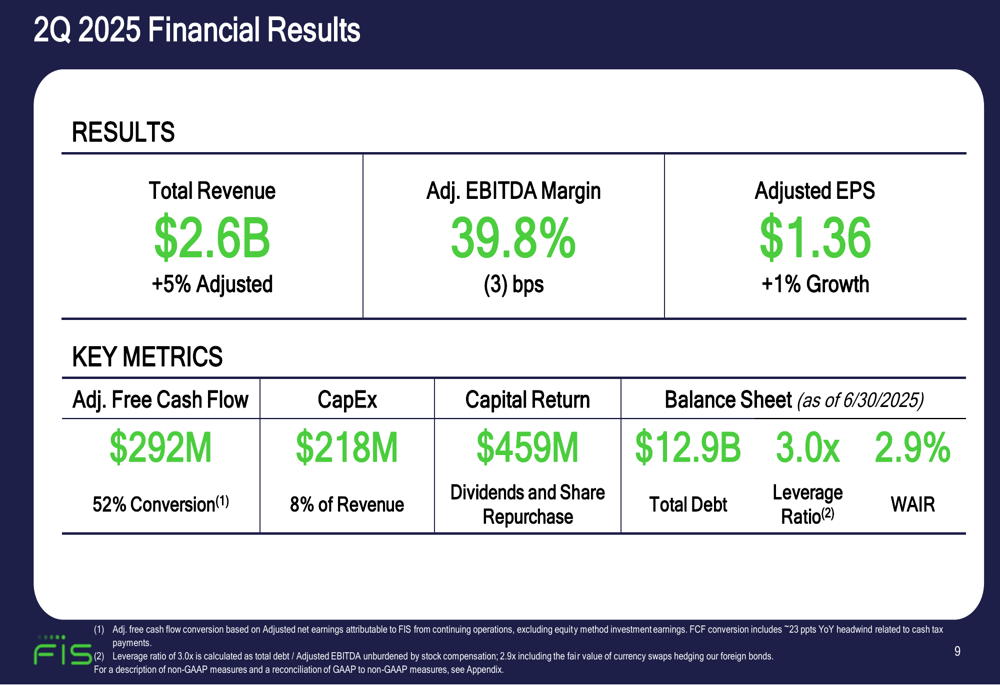

FIS reported total revenue of $2.6 billion for Q2 2025, representing 5% adjusted growth year-over-year. The company’s adjusted EBITDA margin came in at 39.8%, a slight decrease of 3 basis points compared to the same period last year, though management highlighted a sequential improvement of approximately 200 basis points from Q1 2025.

Adjusted earnings per share reached $1.36, representing modest growth of 1% compared to Q2 2024, significantly lower than the 11% EPS growth reported in the first quarter. The company generated $292 million in adjusted free cash flow, achieving a 52% conversion rate, while returning $459 million to shareholders through dividends and share repurchases.

The detailed financial results for the quarter are illustrated in the following slide:

FIS continues to focus on its recurring revenue streams, which grew 6% and now represent 81% of total revenue. This emphasis on stable, predictable revenue sources is a key element of the company’s strategy to build resilience across economic cycles.

Segment Analysis

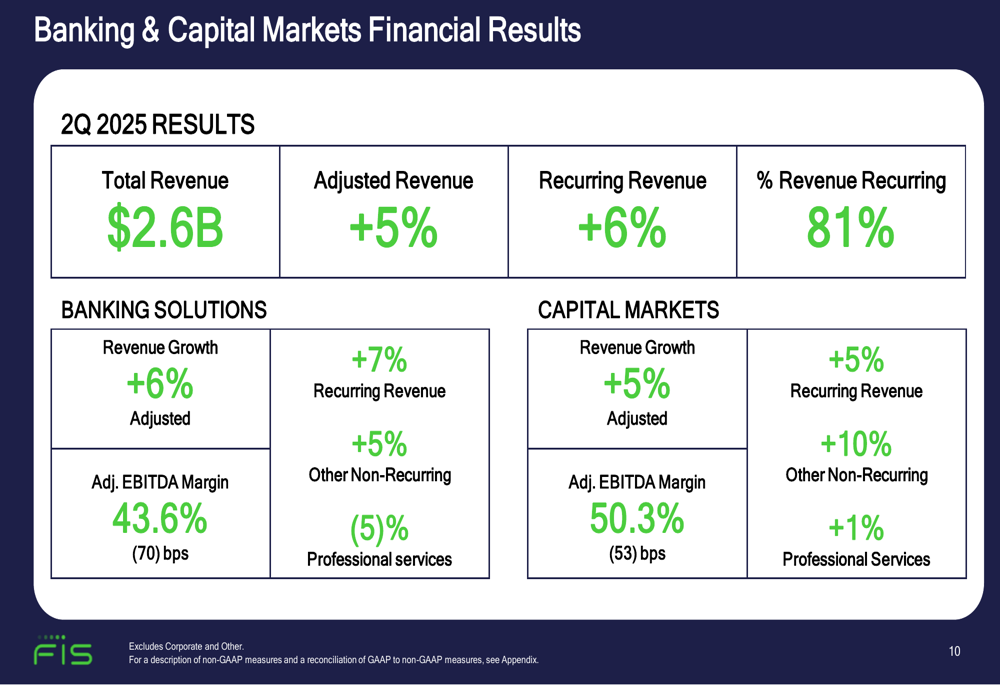

The Banking Solutions segment was the standout performer in Q2, delivering 6% adjusted revenue growth, with recurring revenue increasing by 7%. However, the segment faced some margin pressure with adjusted EBITDA margin declining 70 basis points to 43.6%. Professional services revenue in this segment declined by 5%, indicating potential challenges in new implementation projects.

The Capital Markets segment maintained steady performance with 5% adjusted revenue growth and a 50.3% adjusted EBITDA margin, though this represented a 53 basis point decline year-over-year. Recurring revenue in this segment grew 5%, while other non-recurring revenue increased by 10%.

The detailed segment performance is shown in the following slide:

Looking at year-to-date performance, Banking Solutions has grown 4% overall, with recurring revenue up 5% but professional services down 5%. Capital Markets has shown stronger year-to-date growth at 7%, driven particularly by a 27% increase in non-recurring revenue, while its recurring revenue grew 5%. The Capital Markets segment has improved its adjusted EBITDA margin by 16 basis points year-to-date, contrasting with the 220 basis point decline in Banking Solutions margins.

Revised Outlook and Guidance

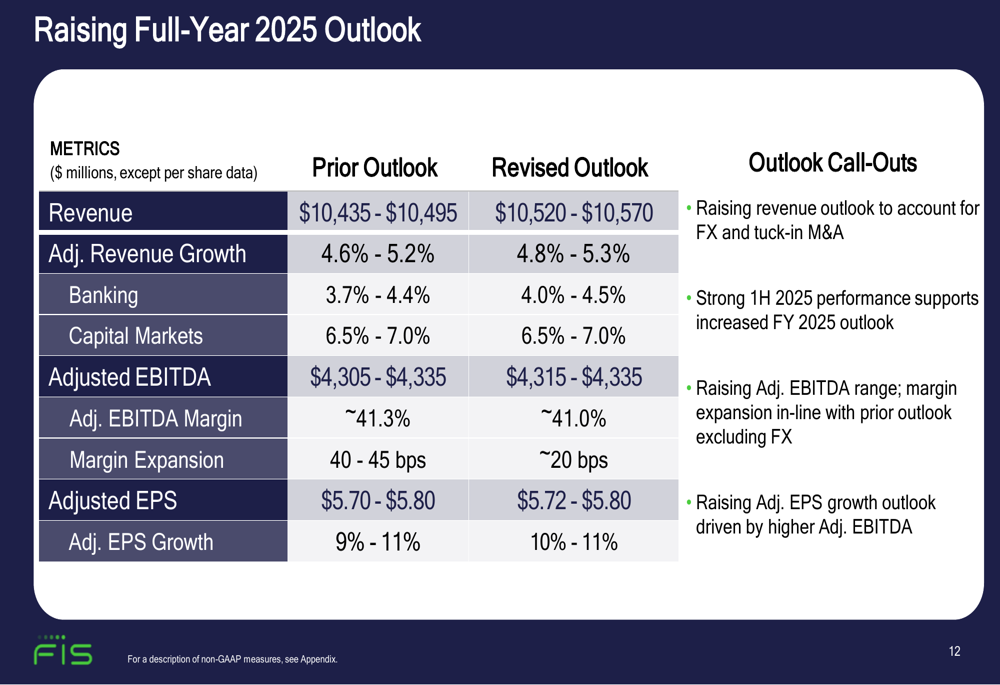

Based on the strong first-half performance, FIS raised its full-year 2025 outlook across several key metrics. The company now expects revenue between $10,520 million and $10,570 million, up from the previous range of $10,435 million to $10,495 million. Adjusted revenue growth is now projected at 4.8% to 5.3%, compared to the previous 4.6% to 5.2%.

Banking segment growth expectations were raised to 4.0%-4.5% from 3.7%-4.4%, while Capital Markets growth guidance remained unchanged at 6.5%-7.0%. The company also raised its adjusted EBITDA range slightly to $4,315-$4,335 million, though it lowered its margin expansion expectation to approximately 20 basis points from the previous 40-45 basis points.

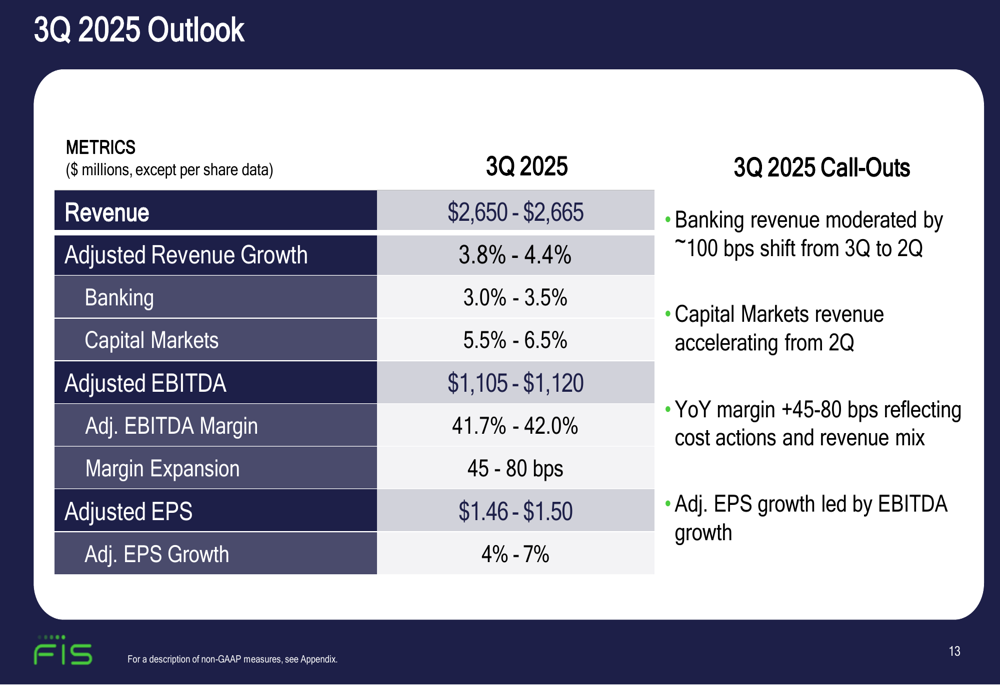

The revised full-year outlook is detailed in the following slide:

For the third quarter of 2025, FIS projects revenue of $2,650-$2,665 million, representing adjusted growth of 3.8%-4.4%. Banking revenue growth is expected to moderate to 3.0%-3.5%, which management attributed to approximately 100 basis points of revenue shifting from Q3 to Q2. Capital Markets revenue is expected to accelerate to 5.5%-6.5% growth. The company anticipates Q3 adjusted EBITDA margin expansion of 45-80 basis points and adjusted EPS of $1.46-$1.50, representing growth of 4%-7%.

Strategic Initiatives

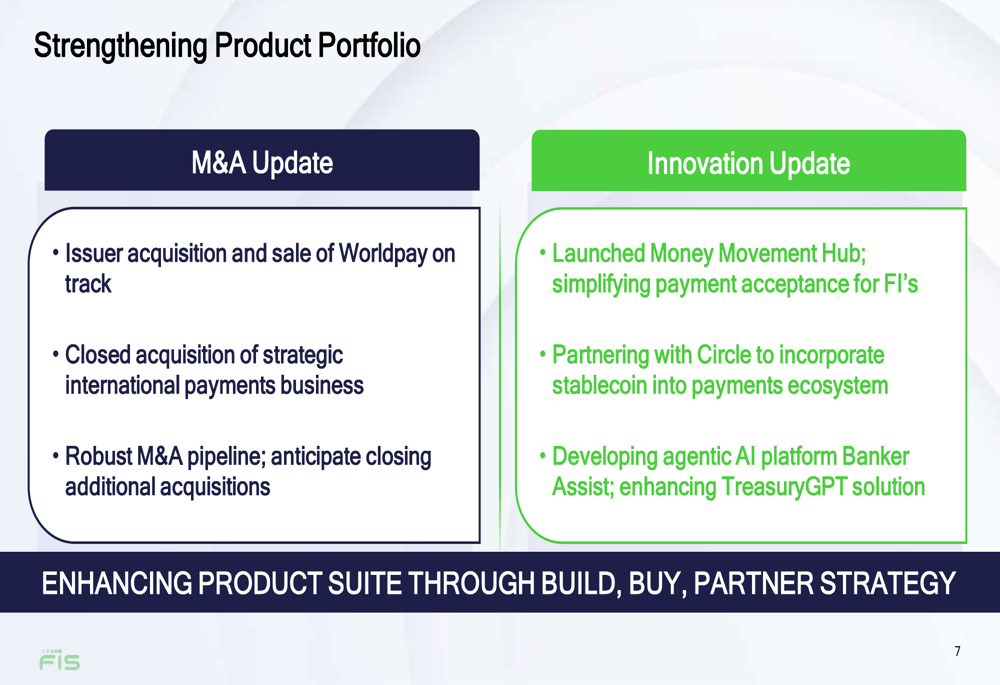

FIS highlighted several strategic initiatives aimed at strengthening its product portfolio and competitive positioning. The company reported that its acquisition of Issuer Solutions and the sale of Worldpay remain on track, while it has already closed an acquisition of a strategic international payments business.

On the innovation front, FIS launched its Money Movement Hub to simplify payment acceptance for financial institutions and announced a partnership with Circle to incorporate stablecoins into its payments ecosystem. The company is also developing an AI platform called Banker Assist and enhancing its TreasuryGPT solution, demonstrating its commitment to incorporating artificial intelligence into its product offerings.

The company’s product portfolio strategy is illustrated in the following slide:

FIS continues to execute on its client acquisition strategy, reporting wins across various segments. The company secured two premier Northeast financial institutions for its IBS Core solution, a global energy technology company for treasury services, and a leading financial services technology firm for private equity services.

Market Reaction and Conclusion

Despite the raised guidance and revenue outperformance, FIS shares were trading down 1.09% in premarket at $78.10. This negative reaction may reflect concerns about the modest 1% EPS growth and reduced margin expansion expectations for the full year.

The company’s financial summary emphasized that operational results were ahead of outlook, with management expressing confidence in second-half revenue acceleration and margin expansion. FIS remains on track for approximately $2 billion in capital return for fiscal year 2025, including the $459 million returned to shareholders in Q2.

CEO Stephanie Ferris and CFO James Kehoe presented a positive outlook for the company, highlighting the strength of FIS’s operating model across economic cycles. The company’s focus on recurring revenue, global distribution, and best-of-breed solutions positions it well for continued growth, though investors appear to be taking a cautious approach as they evaluate the sustainability of the company’s margin improvement and earnings growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.