Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

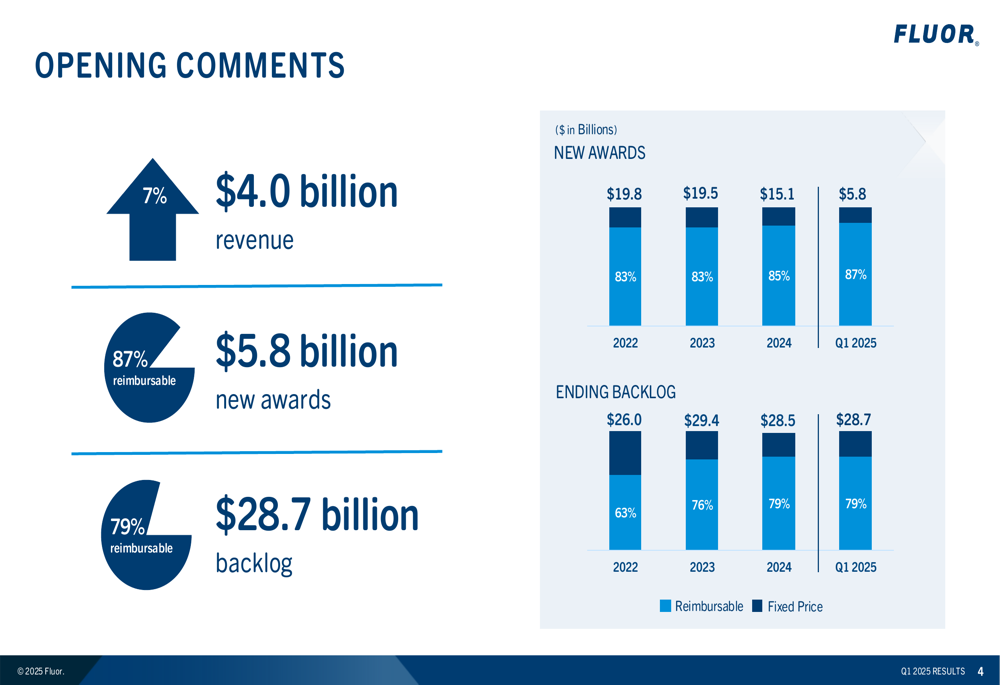

Fluor Corporation (NYSE:FLR) presented its first quarter 2025 results on May 2, showcasing revenue growth and a significant increase in new awards as the company transitions to its "Grow & Execute" strategic phase. The engineering and construction firm reported quarterly revenue of $4.0 billion, up 7% year-over-year, though slightly below analyst expectations of $4.18 billion.

Despite the revenue miss, Fluor’s adjusted earnings per share of $0.73 exceeded forecasts of $0.50 by 46%, driving the stock up nearly 8% in premarket trading following the announcement. Currently trading at $35.86, the stock remains well below its 52-week high of $60.10, suggesting potential upside according to some analysts.

The company’s presentation highlighted its strategic shift from the 2021-2024 "Fix & Build" phase to the 2025-2028 "Grow & Execute" phase, with an increasing focus on reimbursable contracts to reduce risk exposure.

As shown in the following strategic roadmap, Fluor is emphasizing financial discipline, balanced contract terms, portfolio growth, and a high-performance culture:

Quarterly Performance Highlights

Fluor reported $5.8 billion in new awards for Q1 2025, with 87% being reimbursable contracts, reflecting the company’s strategic focus on risk reduction. This contributed to a total backlog of $28.7 billion, of which 79% consists of reimbursable work. The shift toward reimbursable contracts represents a key element of Fluor’s risk management strategy.

The following chart illustrates the company’s new awards and backlog composition:

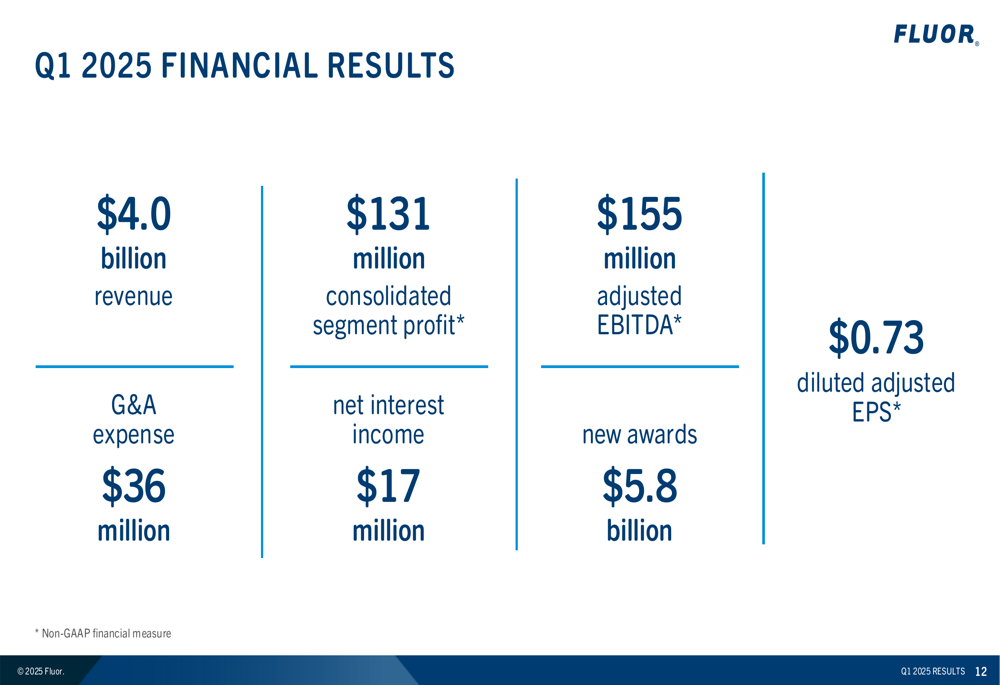

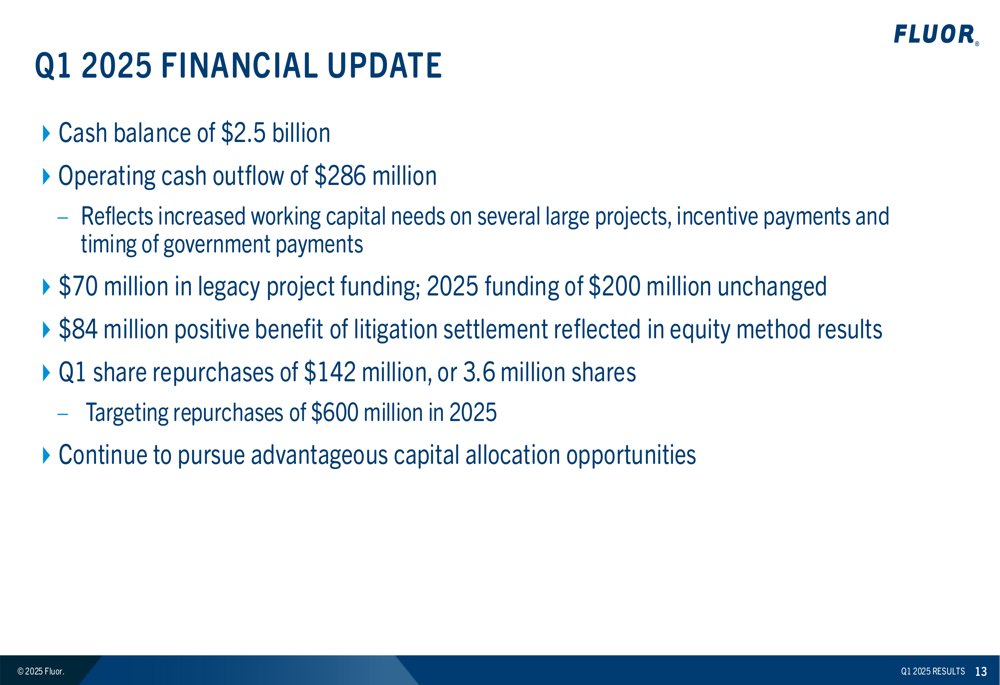

Financial results for the quarter showed consolidated segment profit of $131 million and adjusted EBITDA of $155 million, a substantial increase from $88 million in Q1 2024. The company maintained a strong cash position of $2.5 billion, despite an operating cash outflow of $286 million, which Fluor attributed to increased working capital needs on several large projects, incentive payments, and timing of government payments.

The comprehensive financial results are summarized in this slide:

During the quarter, Fluor continued its share repurchase program, buying back 3.6 million shares for $142 million as part of its target to repurchase $600 million in shares during 2025. This reflects management’s confidence in the company’s financial position and future prospects.

Segment Performance Analysis

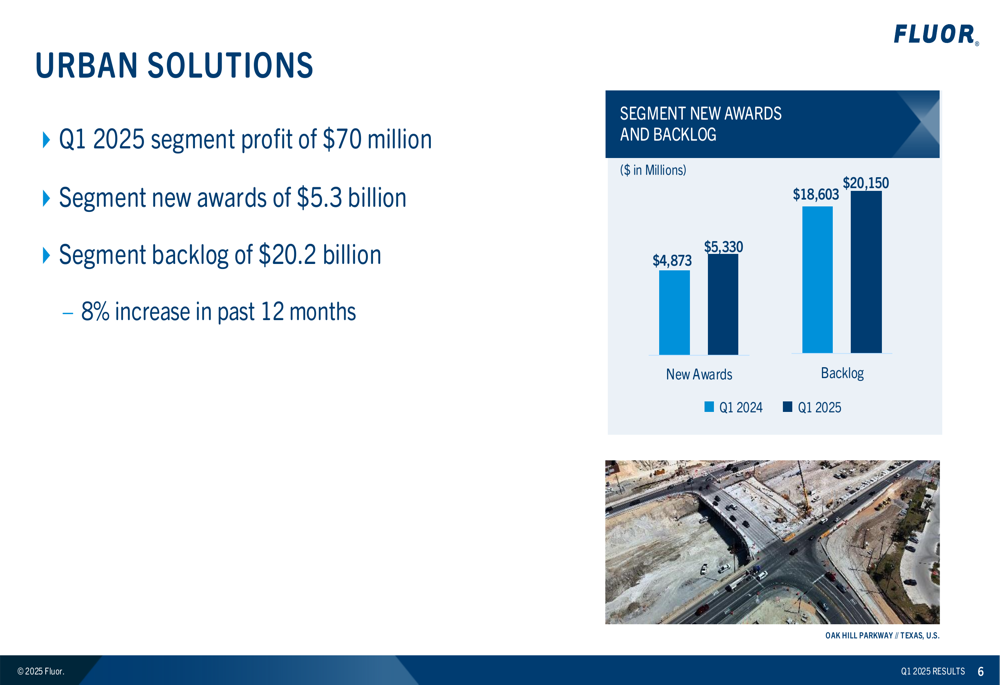

Fluor’s Urban Solutions segment emerged as the strongest performer in Q1 2025, reporting a segment profit of $70 million and new awards of $5.3 billion. The segment’s backlog increased 8% over the past 12 months to $20.2 billion, representing approximately 70% of the company’s total backlog.

Key developments in Urban Solutions included:

The segment secured several significant projects, including a multi-billion dollar pharmaceutical EPCM project and the $682 million construction contract for TxDOT near College Station. The company also highlighted progress on the Gordie Howe International Bridge project, which is now 96% complete.

In the Energy Solutions segment, Fluor reported a profit of $47 million and new awards of $315 million, maintaining a backlog of $6.2 billion. The company noted progress on key projects including the Dow Path2Zero project and LNG Canada, where 782 of 837 systems are mechanically complete.

The Mission Solutions segment faced challenges, with segment profit of only $5 million after including a $28 million reserve related to a recent ruling on a project completed in 2019. New awards for this segment totaled $164 million, primarily from DOE, FEMA, and Army contracts, with a backlog of $2.4 billion.

Strategic Initiatives

Fluor’s presentation emphasized its transition to the "Grow & Execute" phase of its strategic plan, focusing on generating cash and earnings while maintaining robust risk management principles. The company is targeting organic growth in select markets, including pharmaceuticals, advanced manufacturing, semiconductors, and data centers.

In the mining and metals sector, Fluor highlighted the awarded Reko Diq copper-gold project in Pakistan and increased focus on copper production in North and South America, aligning with global demand for materials essential to energy transition and electrification.

The company’s cash flow and capital allocation strategy focuses on maintaining financial flexibility while returning value to shareholders through the share repurchase program:

Financial Outlook & Guidance

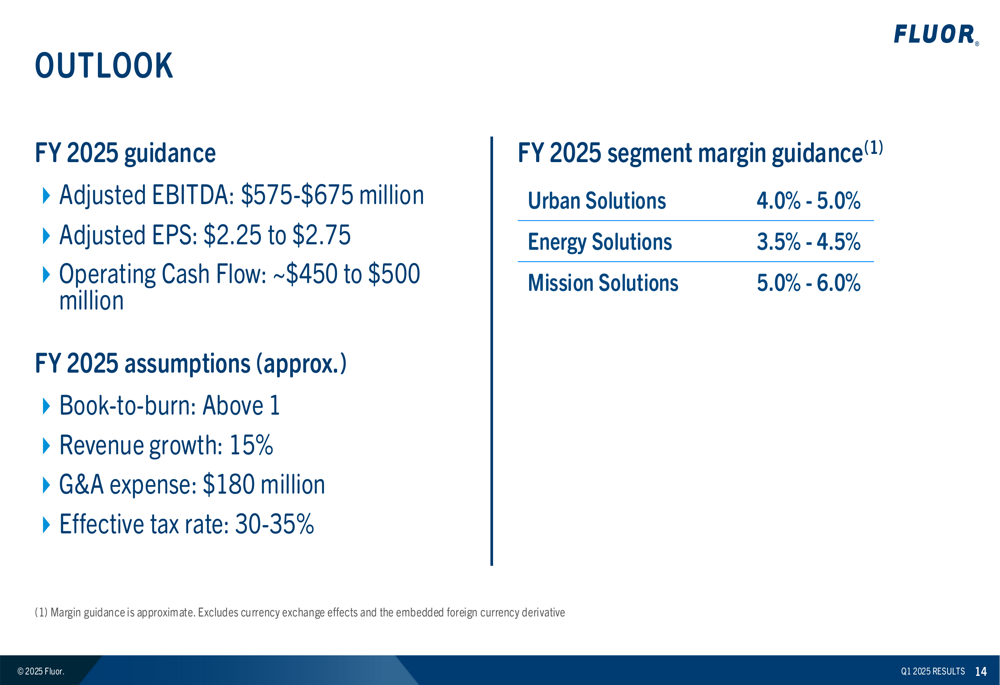

Fluor maintained its full-year 2025 guidance, projecting adjusted EBITDA of $575-$675 million and adjusted EPS of $2.25-$2.75. The company expects operating cash flow of approximately $450-$500 million and revenue growth of 15% for the year.

Segment margin guidance was provided as follows: Urban Solutions at 4.0-5.0%, Energy Solutions at 3.5-4.5%, and Mission Solutions at 5.0-6.0%. The company anticipates a book-to-burn ratio above 1, indicating continued backlog growth, and an effective tax rate of 30-35%.

The detailed guidance is presented in this slide:

CEO Jim Brewer emphasized during the earnings call that clients are moving forward with projects "where there is a clear time to market driver," particularly in high-demand sectors like pharmaceuticals and semiconductors. This strategic focus on high-growth markets, combined with the shift toward reimbursable contracts, positions Fluor to potentially capitalize on infrastructure and energy transition opportunities while managing project execution risks.

While the company faces challenges including negative operating cash flow in Q1 and foreign exchange impacts, the strong new awards and growing backlog suggest momentum for the remainder of 2025 as Fluor continues executing its strategic transition.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.