Palantir shares slip premarket despite posting record revenue in third quarter

Flushing Financial Corporation (NASDAQ:FFIC) presented its third-quarter 2025 earnings results on October 30, showing continued improvement in profitability metrics while maintaining its conservative credit approach. The bank’s stock closed at $12.86, up 2.72% following the earnings release that exceeded analyst expectations with EPS of $0.35 compared to the forecasted $0.30.

Quarterly Performance Highlights

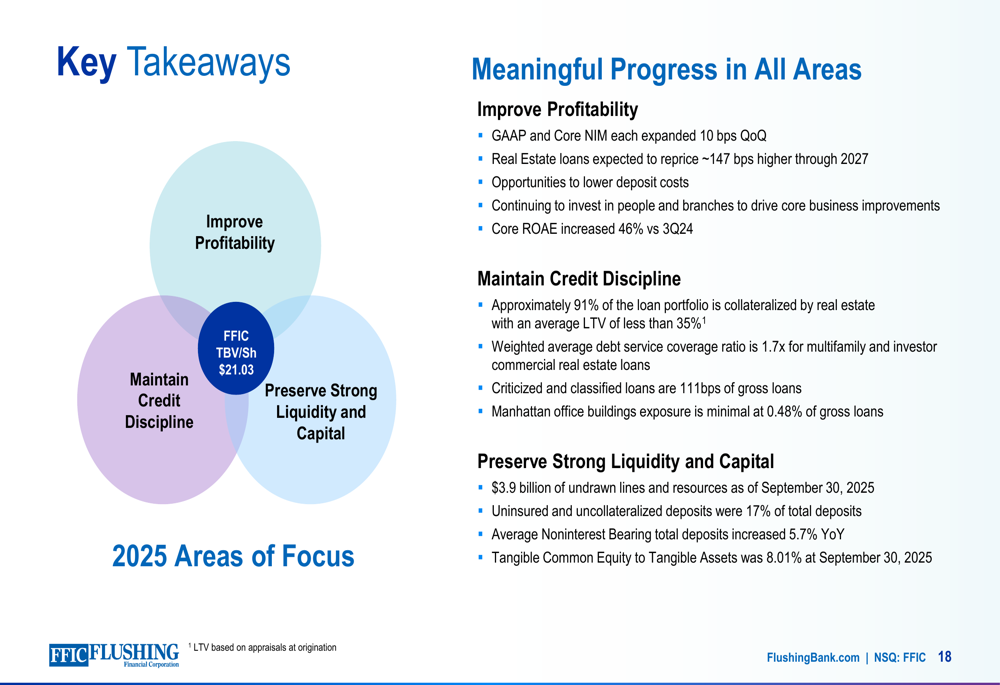

Flushing Financial reported significant improvements in its net interest margin (NIM), with both GAAP and core NIM expanding by 10 basis points quarter-over-quarter to 2.64% and 2.62% respectively. Core net interest income increased by $8.6 million or 19.1% year-over-year, demonstrating the bank’s ability to enhance its interest-earning capabilities in the current rate environment.

As shown in the following chart of quarterly net interest income and margin growth:

The bank’s credit quality metrics showed improvement, with net charge-offs totaling just 7 basis points in Q3 2025, down significantly from 18 basis points in Q3 2024 and 15 basis points in Q2 2025. Non-performing assets to total assets stood at 70 basis points, up from 59 basis points year-over-year but down from 75 basis points in the previous quarter.

A key driver of profitability improvement has been the bank’s deposit mix, with noninterest-bearing deposits increasing 7.2% quarter-over-quarter, accelerating from 4.2% growth in Q2 2025. Average noninterest-bearing deposits increased 2.1% quarter-over-quarter and 5.7% year-over-year, helping to reduce funding costs.

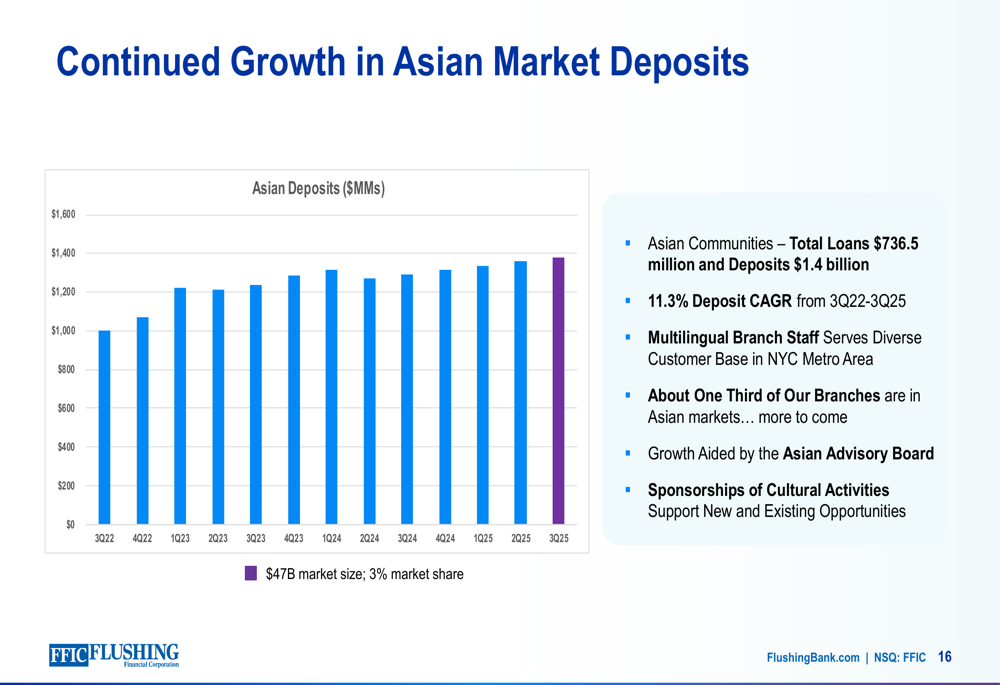

Strategic Focus on Asian Banking Communities

Flushing Financial continues to see strong results from its strategic focus on Asian banking communities in the New York metropolitan area. The presentation highlighted an 11.3% compound annual growth rate in Asian deposits from Q3 2022 to Q3 2025, with total Asian deposits reaching $1.4 billion against $736.5 million in loans to these communities.

The following chart illustrates the consistent growth in Asian market deposits:

The bank attributes this success to its multilingual branch staff and cultural engagement through its Asian Advisory Board and sponsorship of cultural activities. Approximately one-third of Flushing’s branches are located in Asian markets, with plans for further expansion in this segment.

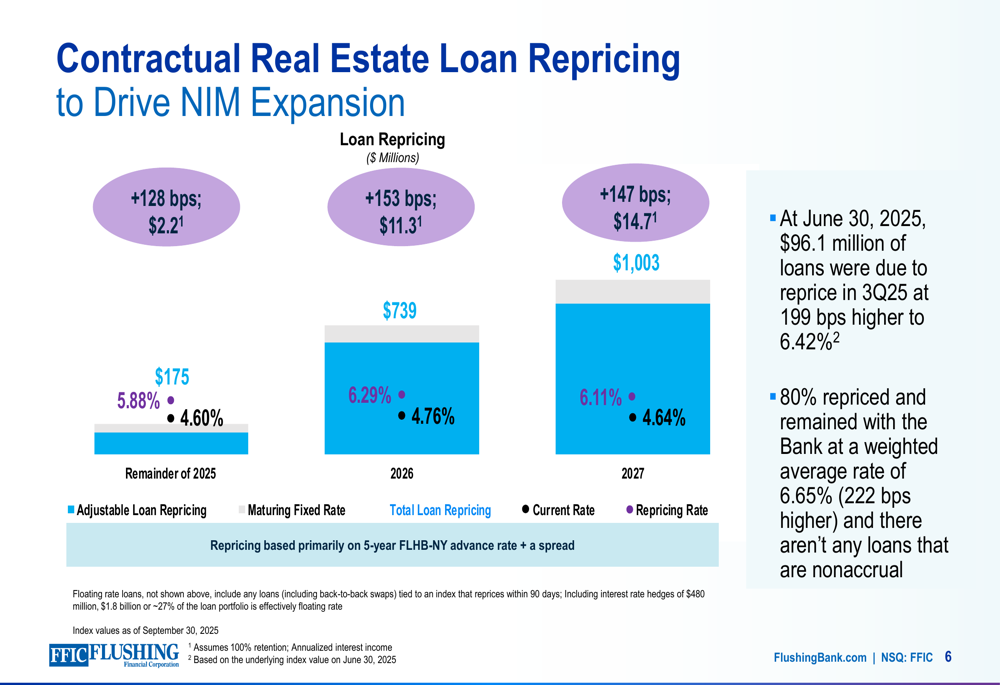

NIM Expansion and Loan Repricing Opportunities

A significant opportunity for continued NIM expansion comes from the bank’s real estate loan portfolio, which is scheduled to reprice at higher rates through 2027. According to the presentation, these loans are expected to reprice approximately 147 basis points higher, providing a substantial boost to interest income.

The following chart details the contractual real estate loan repricing schedule:

Management noted that in the third quarter, 80% of loans due to reprice remained with the bank at a weighted average rate of 6.65%, which was 222 basis points higher than their previous rate. For the remainder of 2025, $175 million of loans are scheduled to mature or reprice upwards by 128 basis points.

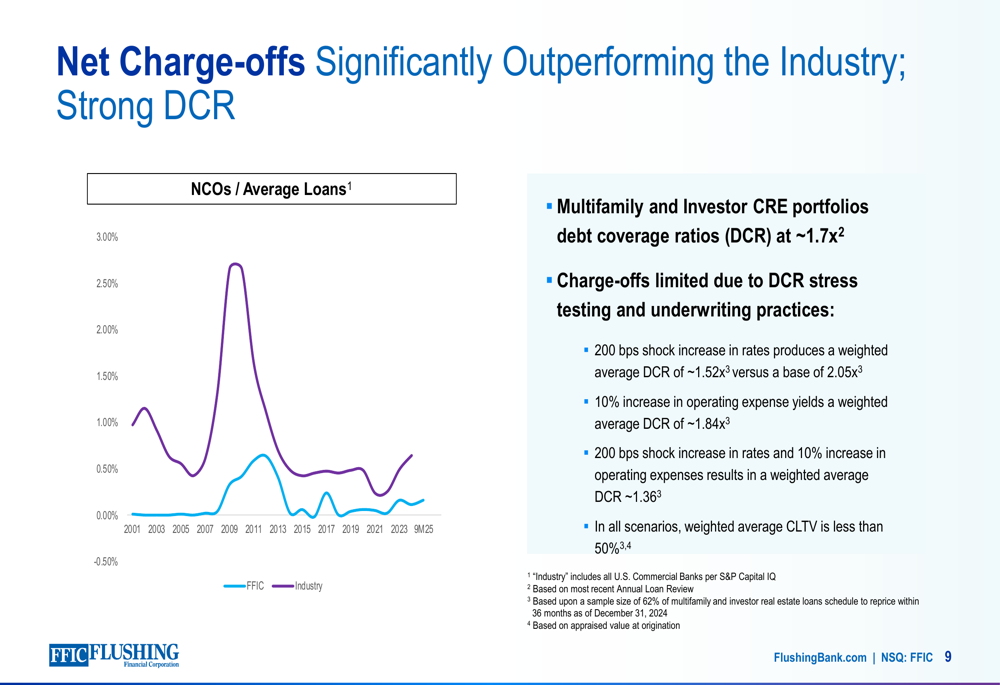

Conservative Credit Approach Outperforms Industry

Flushing Financial emphasized its conservative underwriting standards, which have resulted in credit quality metrics consistently outperforming industry averages. The bank’s net charge-offs and noncurrent loans have remained well below industry benchmarks over multiple credit cycles.

The following comparison demonstrates how Flushing’s noncurrent loans have consistently outperformed the industry:

The bank’s multifamily and commercial real estate portfolios maintain weighted average debt coverage ratios of approximately 1.7x, providing significant cushion against potential market stress. Approximately 91% of the loan portfolio is collateralized by real estate with an average loan-to-value ratio of less than 35%.

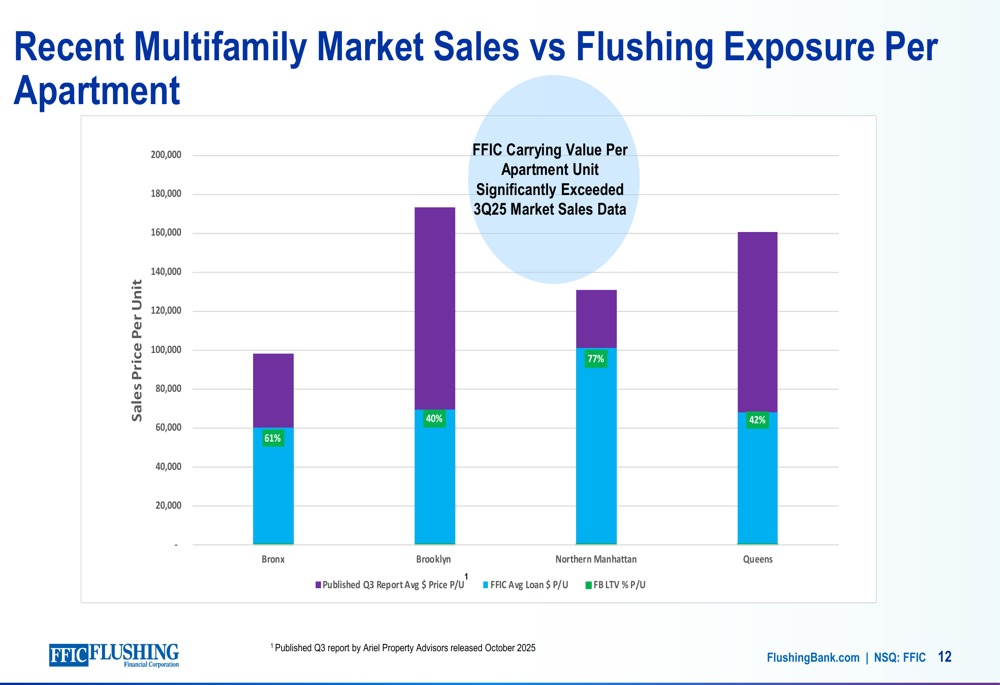

Flushing’s exposure to multifamily properties in New York City boroughs shows significantly lower loan values per apartment unit compared to recent market sales data:

Capital Position and Liquidity

The bank reported a tangible common equity ratio of 8.01% as of September 30, 2025, up 101 basis points year-over-year. Liquidity remains strong with $3.9 billion of undrawn lines and resources at quarter end. Uninsured and uncollateralized deposits represented only 17% of total deposits, reflecting a stable funding base.

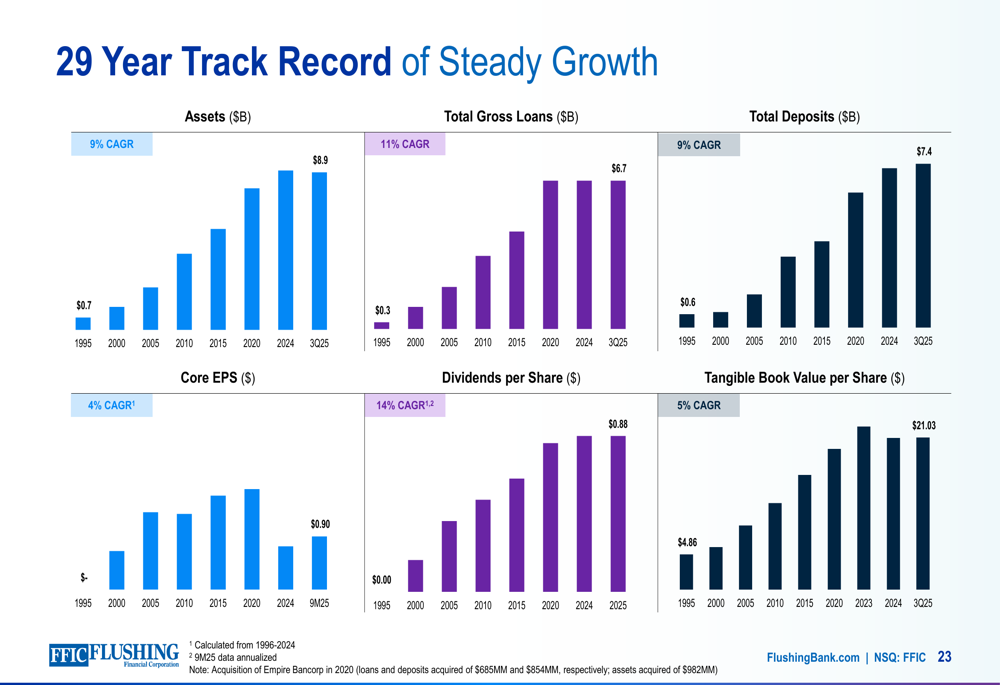

The presentation highlighted Flushing Financial’s 29-year track record of steady growth, with 9% CAGR in assets, 11% CAGR in loans, and 9% CAGR in deposits since becoming a public company:

Outlook for Remainder of 2025

For the fourth quarter of 2025, Flushing Financial expects total assets to remain stable, with loan growth dependent on market conditions. The bank has $770.2 million of retail CDs at a weighted average rate of 3.98% maturing in Q4, with September 2025 CD retention rates at 3.54%, providing an opportunity to reduce funding costs.

Management anticipates normal seasonal deposit inflows in Q4 and expects core noninterest expense to increase 4.5%-5.5% from the 2024 base of $159.6 million as the bank continues to invest in growth initiatives. The effective tax rate is projected at 24.5%-26.5% for the remainder of 2025.

The company summarized its progress and strategic priorities in the following key takeaways slide:

CEO John R. Buran stated in the earnings call, "Our third quarter results clearly show that we’ve executed on our 2025 plan in all areas of focus," emphasizing the company’s strong path towards improving return metrics. CFO Susan K. Cullen noted that deposit repricing betas would likely remain similar to what the bank has experienced so far in the current rate cycle.

With its expanding net interest margin, growing noninterest-bearing deposits, and conservative credit approach, Flushing Financial appears well-positioned to continue its profitability improvement while maintaining strong asset quality through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.