Fed Governor Adriana Kugler to resign

Introduction & Market Context

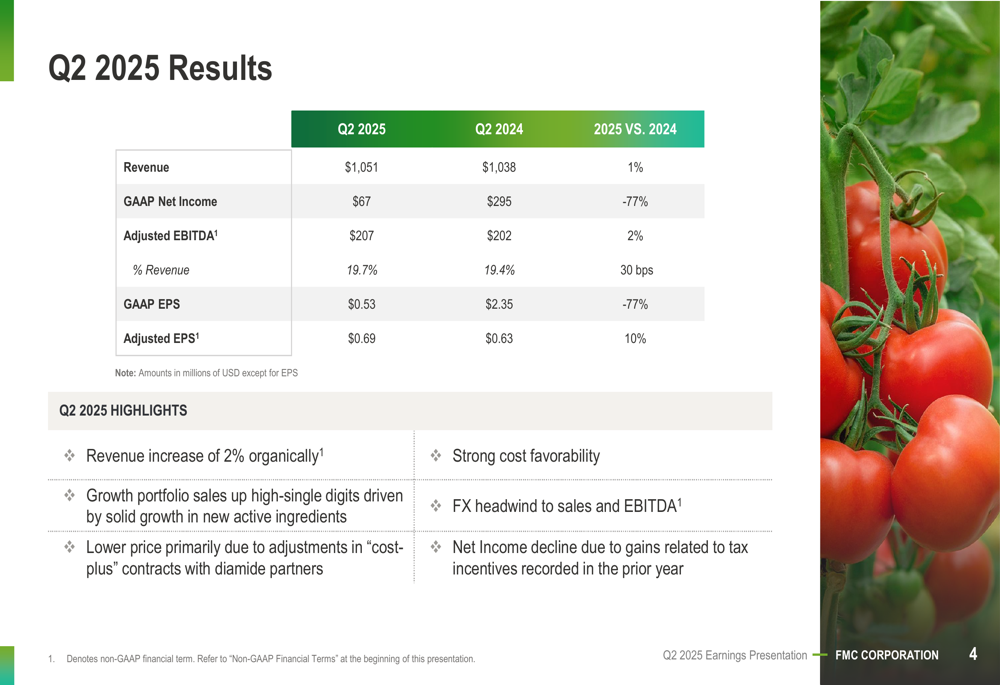

FMC Corporation (NYSE:FMC) released its Q2 2025 earnings presentation on July 31, 2025, showing signs of stabilization with modest revenue growth after a challenging first quarter. The agricultural sciences company reported a 1% year-over-year revenue increase, reaching $1,051 million, though GAAP net income declined significantly due to one-time tax benefits recorded in the prior year.

The results come after a difficult Q1 2025 when the company experienced a 14% sales decline, which led to a 6.31% stock drop. FMC’s current share price of $42.07 reflects continued investor caution, with the stock trading well below its 52-week high of $68.55 but above its 52-week low of $32.83.

Q2 2025 Financial Performance

FMC’s Q2 2025 financial results showed mixed performance across key metrics. While revenue grew slightly, GAAP net income fell substantially compared to the same period last year.

As shown in the following quarterly results summary:

The company’s adjusted metrics painted a more positive picture, with adjusted EBITDA increasing 2% to $207 million and adjusted EPS rising 10% to $0.69. The significant 77% decline in GAAP net income to $67 million was primarily attributed to tax incentives recorded in Q2 2024 that created a high comparison base.

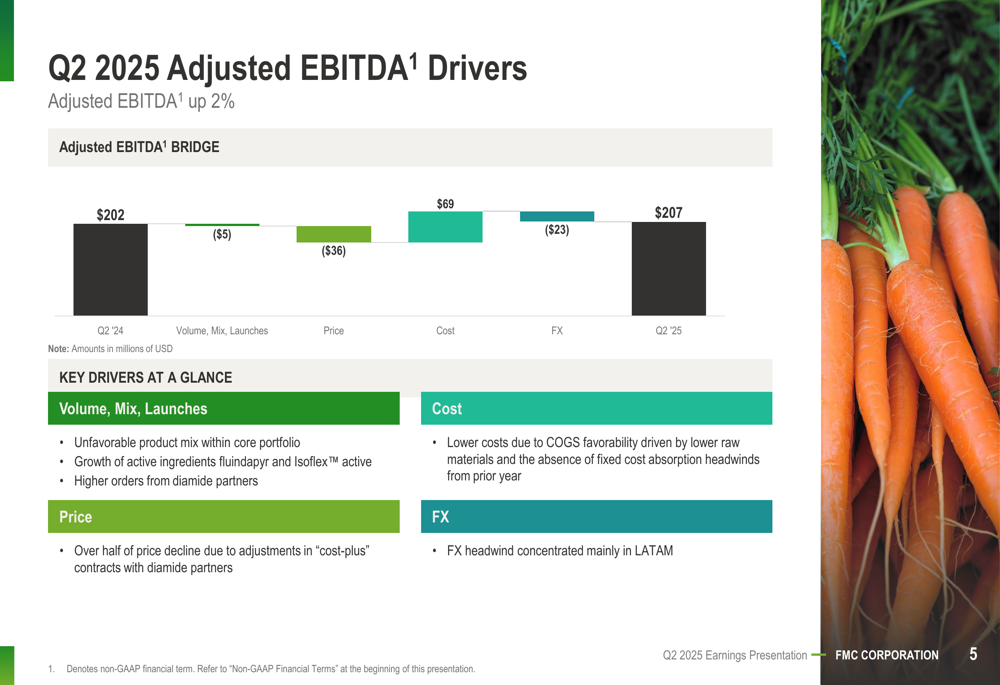

Several factors contributed to the adjusted EBITDA performance, as illustrated in this breakdown:

Cost favorability was the standout positive driver, contributing $69 million to EBITDA growth. This gain was partially offset by price declines (-$36 million) and foreign exchange headwinds (-$23 million). Over half of the price decline was attributed to adjustments in "cost-plus" contracts with diamide partners.

Regional Performance Analysis

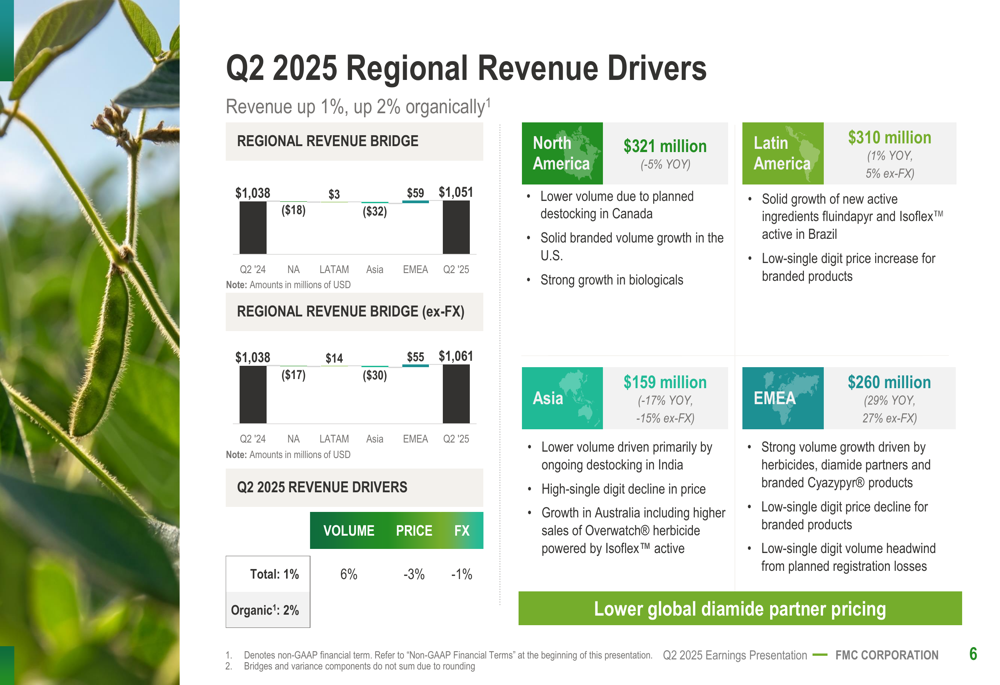

FMC’s performance varied significantly across regions, with EMEA showing strong growth while other regions faced challenges.

The regional revenue breakdown demonstrates these geographic variations:

EMEA emerged as the strongest performer with 29% revenue growth, driven by herbicides, diamide partners, and branded Cyazypyr® products. Latin America achieved modest 1% growth (5% excluding FX effects), supported by new active ingredients in Brazil.

North America revenue declined 5%, affected by planned destocking in Canada, though the U.S. saw solid branded volume growth and strong performance in biologicals. Asia experienced the steepest decline at 17%, primarily due to ongoing destocking in India, where the company is now pursuing a sale of its commercial business.

Strategic Initiatives and Focus Areas

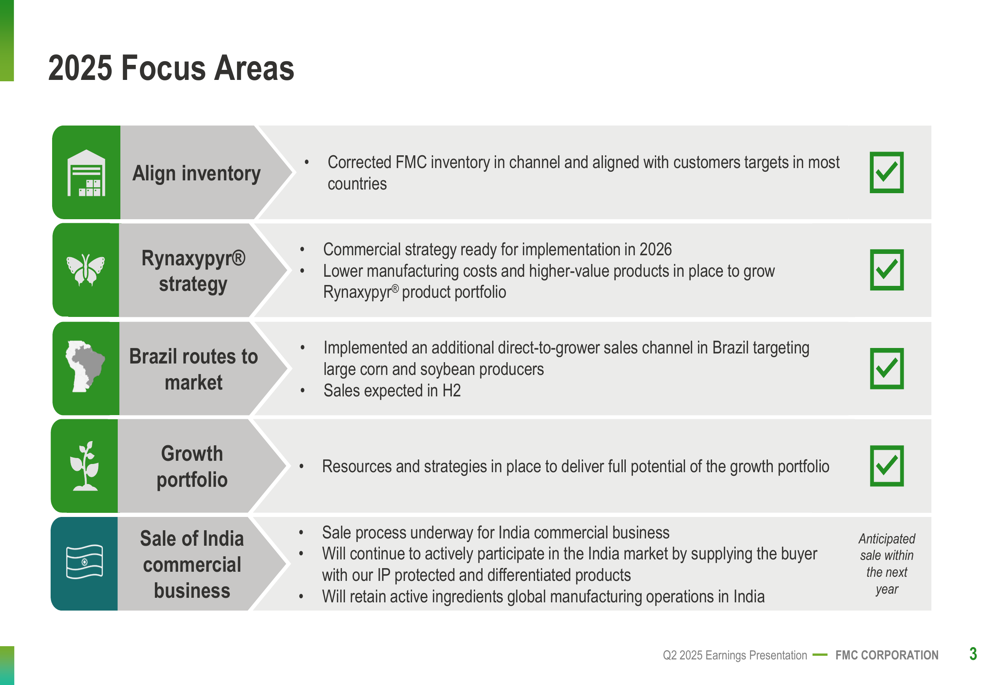

FMC outlined five key strategic focus areas for 2025, highlighting progress in inventory management and market expansion efforts.

The company’s strategic priorities for the year are detailed in this overview:

Notable progress includes corrected inventory levels in most countries and implementation of an additional direct-to-grower sales channel in Brazil targeting large corn and soybean producers. The company has also prepared its Rynaxypyr® commercial strategy for 2026 implementation and positioned resources to maximize the potential of its growth portfolio.

The sale process for FMC’s India commercial business is underway, though the company plans to continue participating in the Indian market by supplying its IP-protected products to the buyer while retaining active ingredients manufacturing operations in the country.

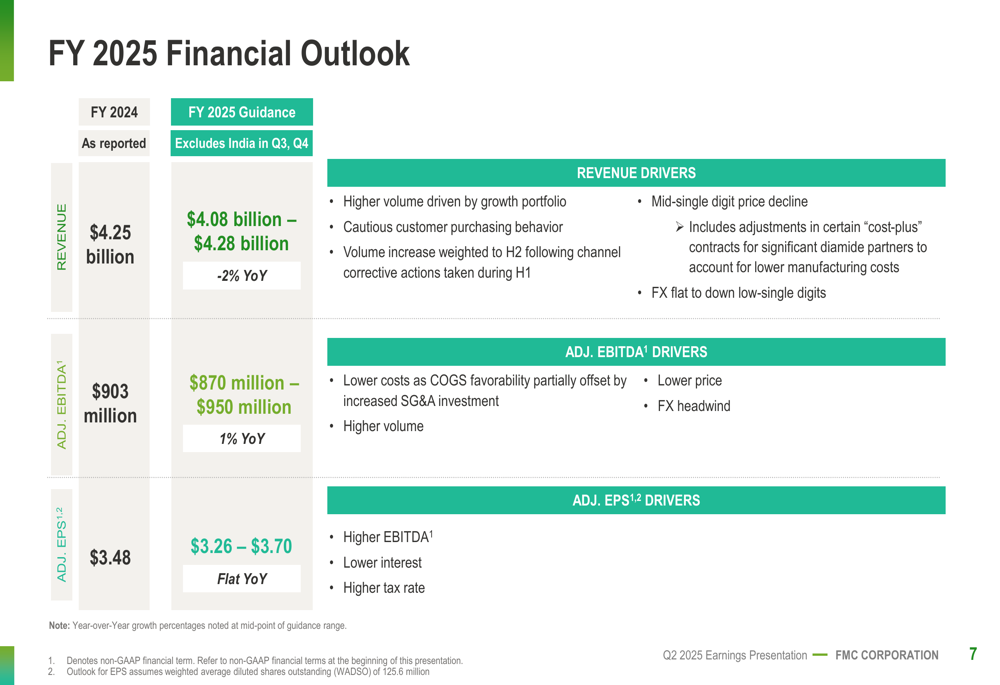

Full-Year and Quarterly Outlook

FMC’s full-year 2025 guidance reflects cautious optimism, with stronger performance expected in the second half of the year.

The company’s financial outlook for fiscal year 2025 is summarized here:

For the full year, FMC expects revenue between $4.08-4.28 billion, representing a 2% year-over-year decline at the midpoint. Adjusted EBITDA is projected to reach $870-950 million, up 1% from 2024, while adjusted EPS is expected to remain flat at $3.26-3.70.

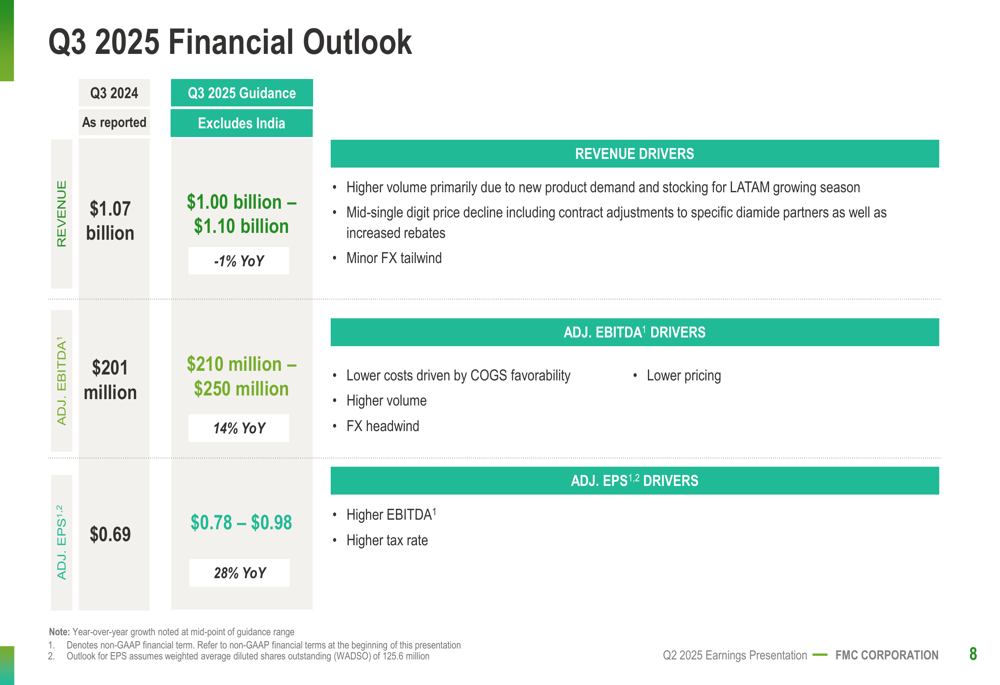

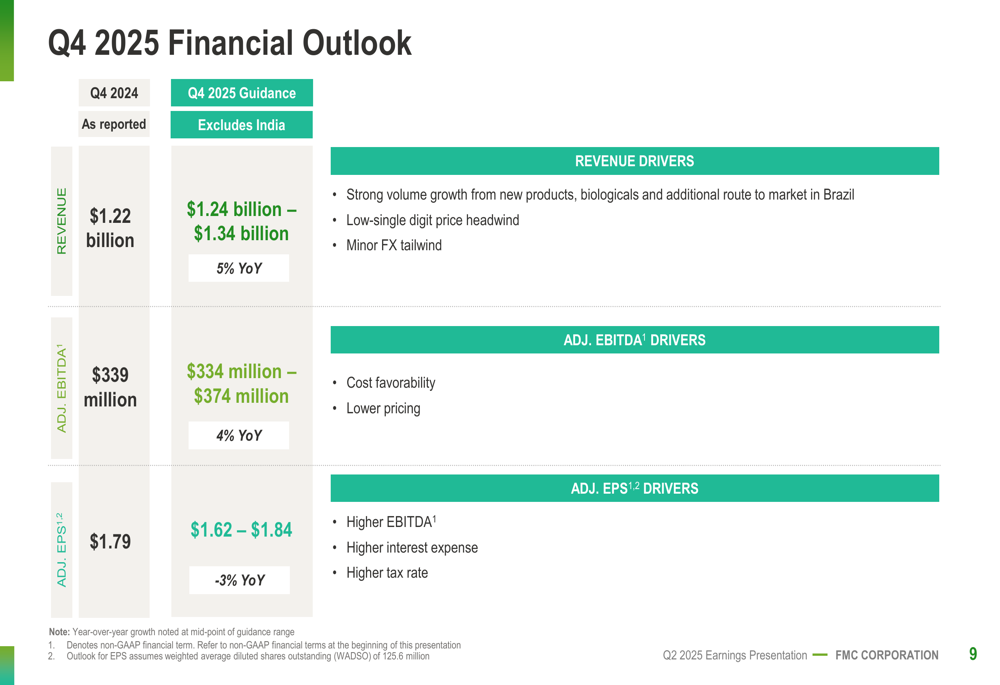

The quarterly guidance shows improving momentum as the year progresses:

Q3 2025 revenue is projected to decline slightly by 1% year-over-year to $1.00-1.10 billion, but adjusted EBITDA is expected to increase by 14% to $210-250 million. Q4 2025 shows the strongest outlook with anticipated 5% revenue growth to $1.24-1.34 billion and 4% adjusted EBITDA growth to $334-374 million, driven by new products, biologicals, and the additional route to market in Brazil.

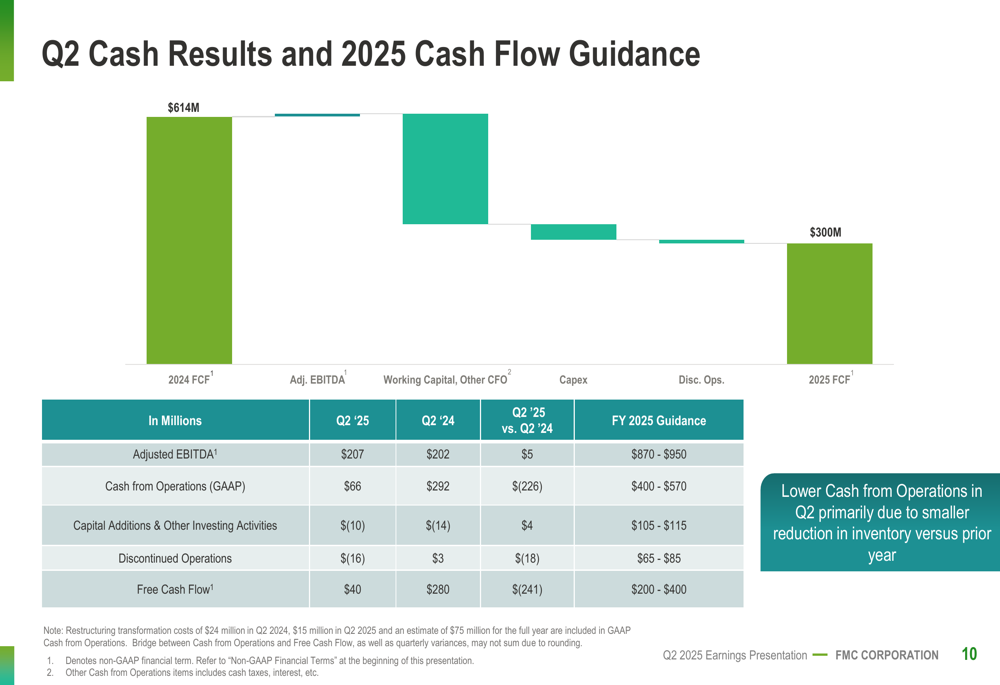

Cash Flow and Financial Health

FMC’s cash flow performance in Q2 2025 showed significant decline compared to the prior year, though the company maintains a solid financial position.

The cash flow results and guidance are detailed in this summary:

Free cash flow for Q2 2025 was $40 million, down substantially from $280 million in Q2 2024. This decline was primarily attributed to a smaller reduction in inventory compared to the prior year. For the full year 2025, FMC expects free cash flow between $200-400 million, a significant decrease from the $614 million generated in 2024.

The company’s financial modeling assumptions include interest expense of $215-235 million, an adjusted tax rate of 13-15%, and capital additions of $105-115 million for 2025.

Conclusion

FMC’s Q2 2025 results indicate a stabilizing business after a challenging start to the year, with modest revenue growth and improved adjusted metrics despite significant GAAP income decline. The company’s strategic focus on inventory alignment, new routes to market, and product portfolio optimization positions it for stronger performance in the second half of 2025.

While pricing pressures and foreign exchange headwinds continue to impact results, cost favorability and volume growth in key segments provide some counterbalance. Investors will likely focus on whether FMC can deliver on its projected second-half improvement, particularly the anticipated 5% revenue growth in Q4, as the company navigates through its strategic repositioning and the sale of its India commercial business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.