Raytheon awarded $71 million in Navy contracts for missile systems

Introduction & Market Context

Franklin BSP Realty Trust (NYSE:FBRT) reported negative distributable earnings for the first quarter of 2025, continuing the volatility seen in previous quarters while maintaining its dividend payout. The commercial real estate finance REIT is navigating a challenging market environment with a strategic focus on multifamily assets and strong liquidity position.

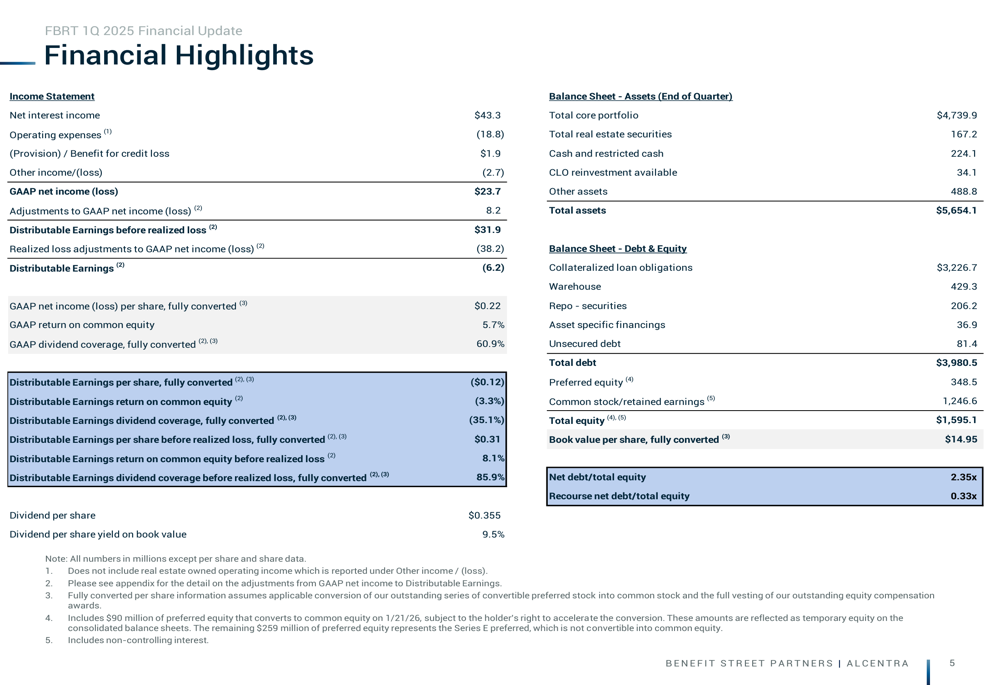

The company’s Q1 2025 supplemental information, released on April 29, 2025, reveals a mixed financial performance with GAAP net income of $23.7 million contrasting with negative distributable earnings of $6.2 million. This follows a similar pattern seen in Q3 2024, when the company also reported negative distributable earnings due to losses from REO assets.

Quarterly Performance Highlights

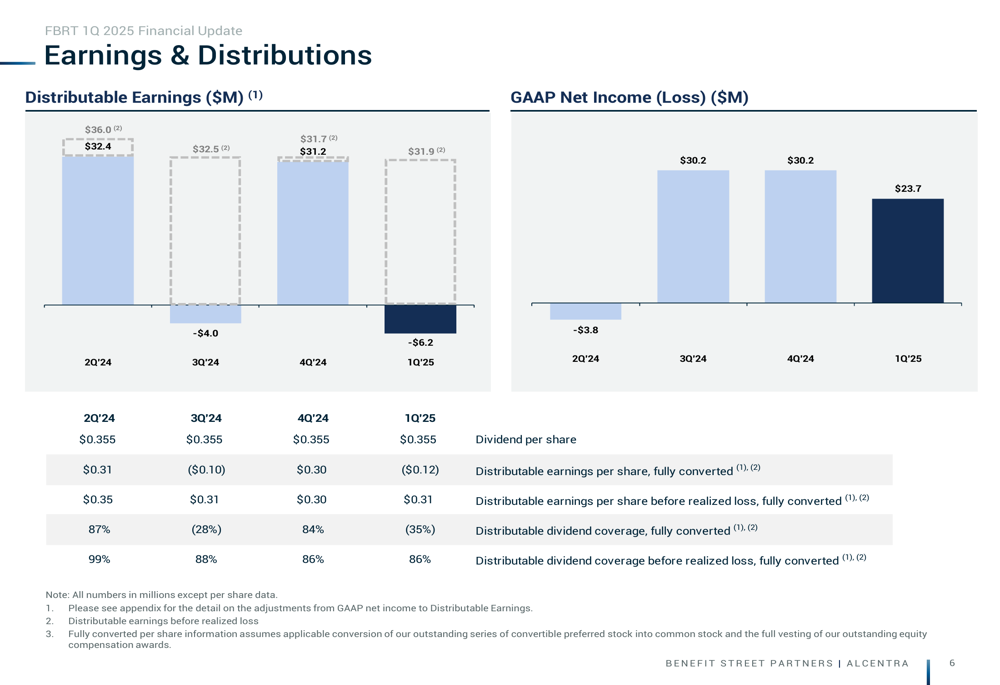

FBRT reported GAAP net income of $23.7 million ($0.20 per diluted share) for Q1 2025, while distributable earnings were negative at $6.2 million. The company maintained its quarterly cash dividend at $0.355 per share despite the earnings challenges.

As shown in the following financial highlights chart:

The negative distributable earnings represent a significant decline from the previous quarter’s positive $31.2 million. This volatility in earnings is clearly illustrated in the quarterly comparison:

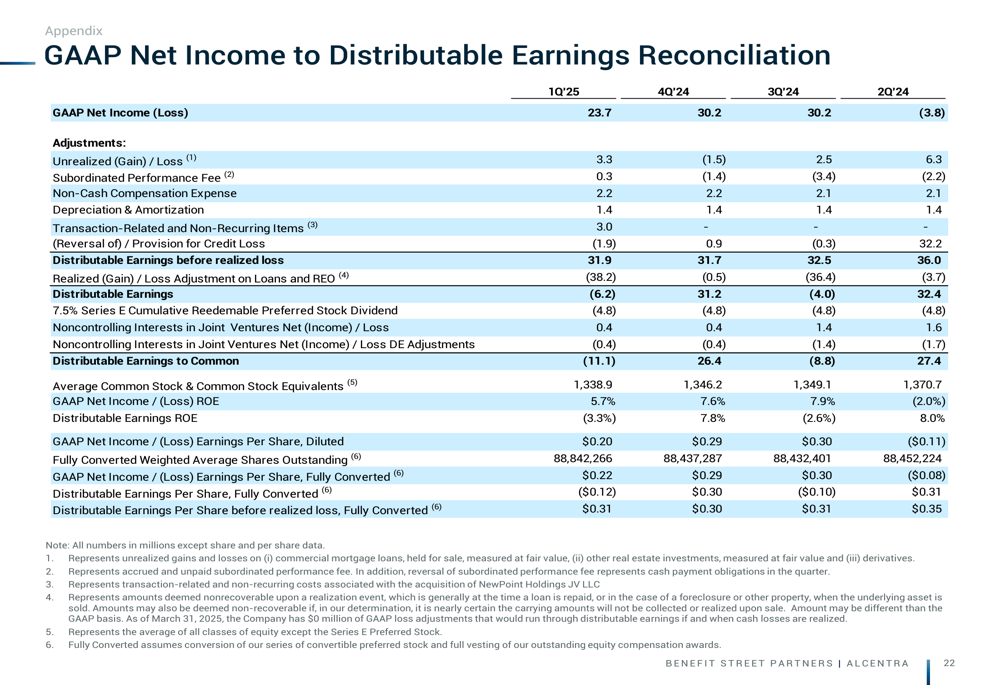

The reconciliation between GAAP net income and distributable earnings reveals significant adjustments, primarily related to realized losses:

Despite the earnings challenges, FBRT maintained a fully-converted book value per share of $14.95 as of March 31, 2025, compared to $15.12 at the end of the previous quarter. The company’s total equity stood at $1.59 billion.

Portfolio Composition and Strategy

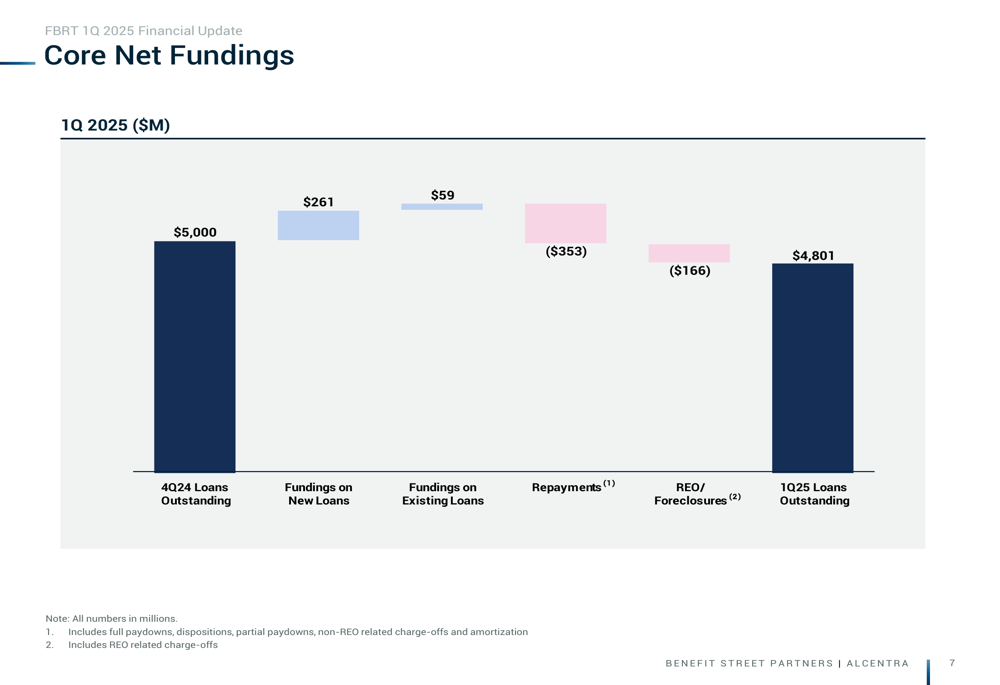

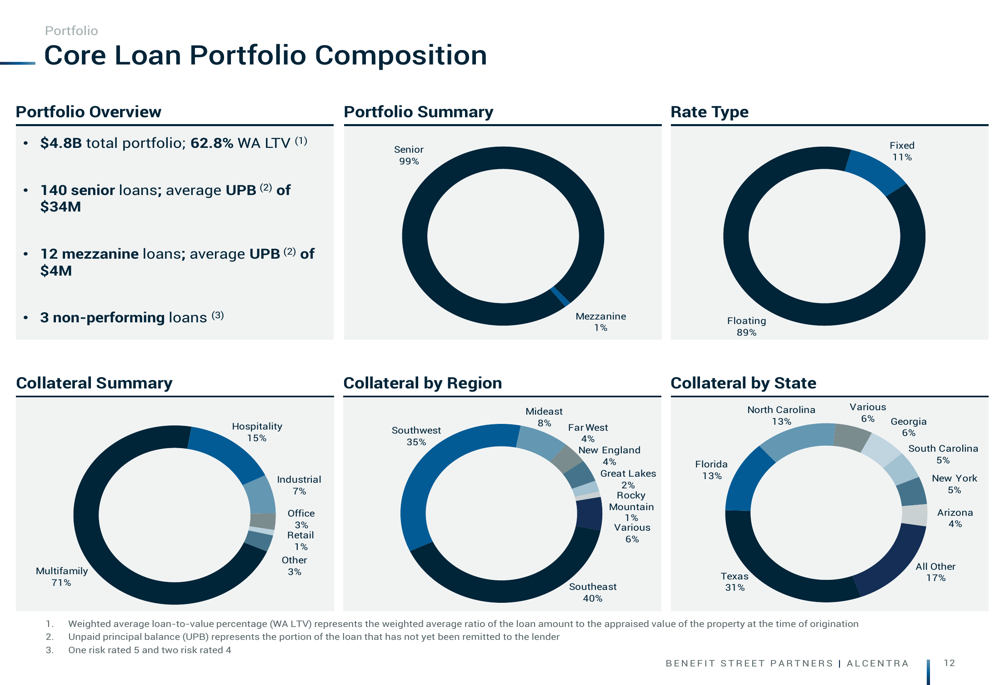

FBRT’s core loan portfolio decreased to $4.8 billion in principal balance by the end of Q1 2025, down from $5.0 billion in the previous quarter. This reduction is illustrated in the following waterfall chart:

The company continues to strategically position its portfolio with a strong emphasis on multifamily properties, which represent 71% of the collateral. This focus aligns with the company’s strategy of concentrating on more stable real estate segments amid market uncertainty.

The portfolio composition is broken down as follows:

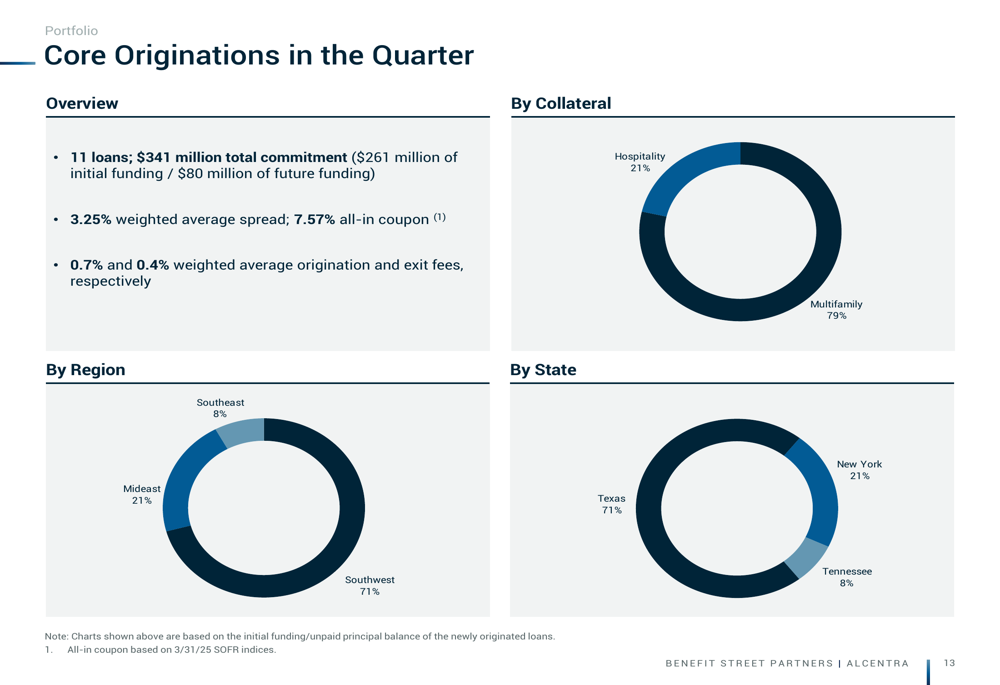

During Q1 2025, FBRT closed $341 million in new loan commitments with initial funding of $261 million. These new originations were primarily focused on multifamily assets (79%) and hospitality (21%), with a significant concentration in Texas (71%).

Capitalization and Liquidity

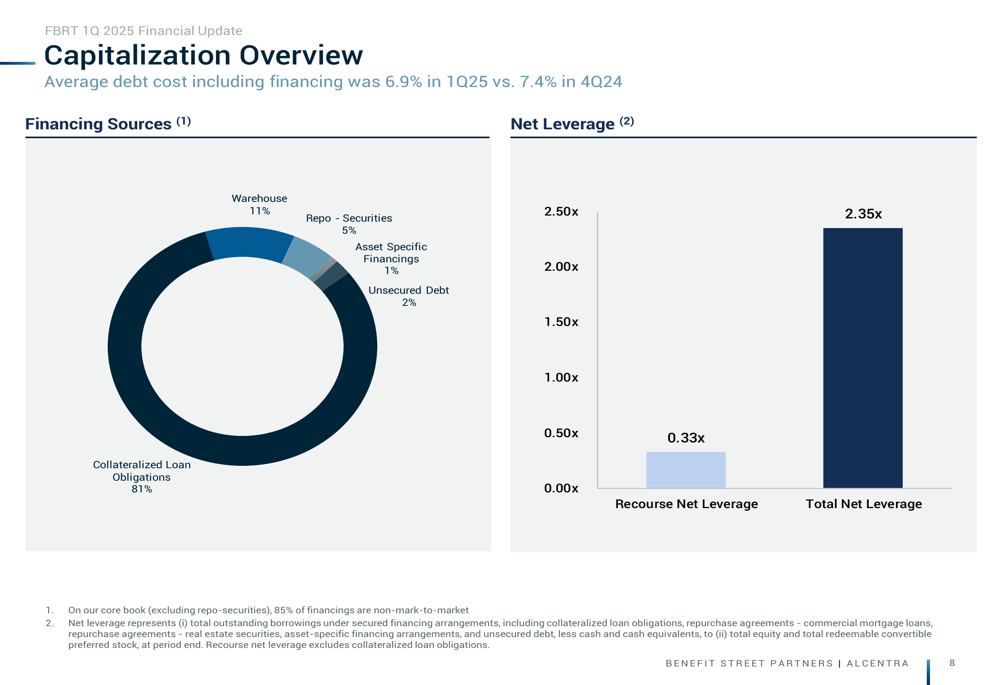

FBRT maintains a diversified financing structure with 81% of its debt in Collateralized Loan Obligations (CLOs), providing stability to its funding base. The company’s average debt cost was 6.9% in Q1 2025.

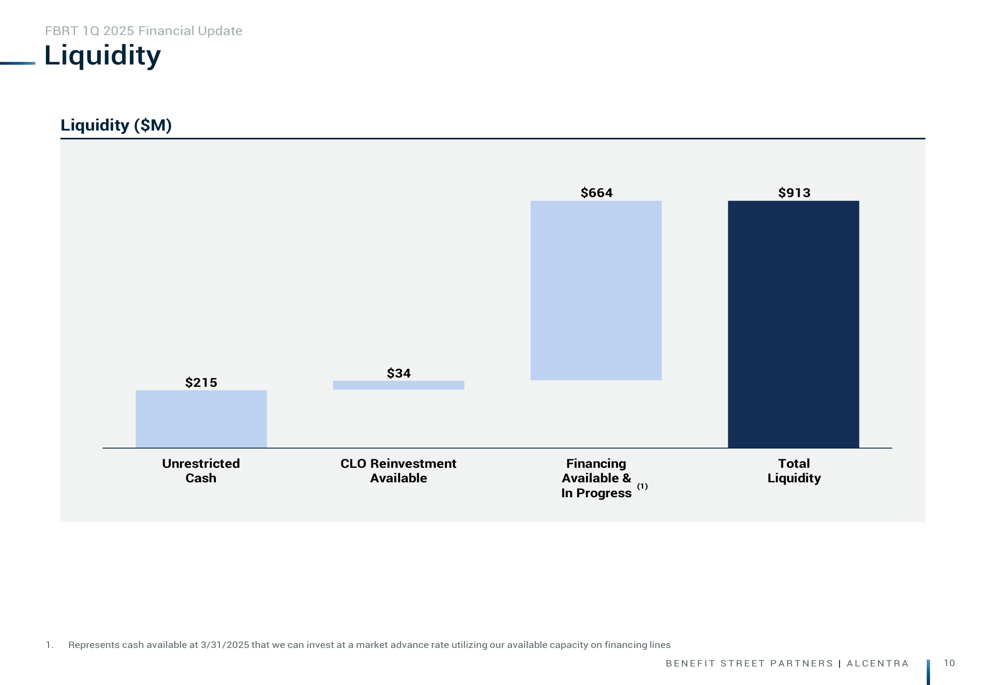

A key strength for FBRT is its substantial liquidity position of $913 million, which provides flexibility to navigate market challenges and capitalize on new opportunities:

The company’s net debt to equity ratio stands at 2.35x, with recourse net leverage at a more conservative 0.33x, indicating a relatively prudent approach to financial leverage despite market pressures.

Asset Quality and Risk Management

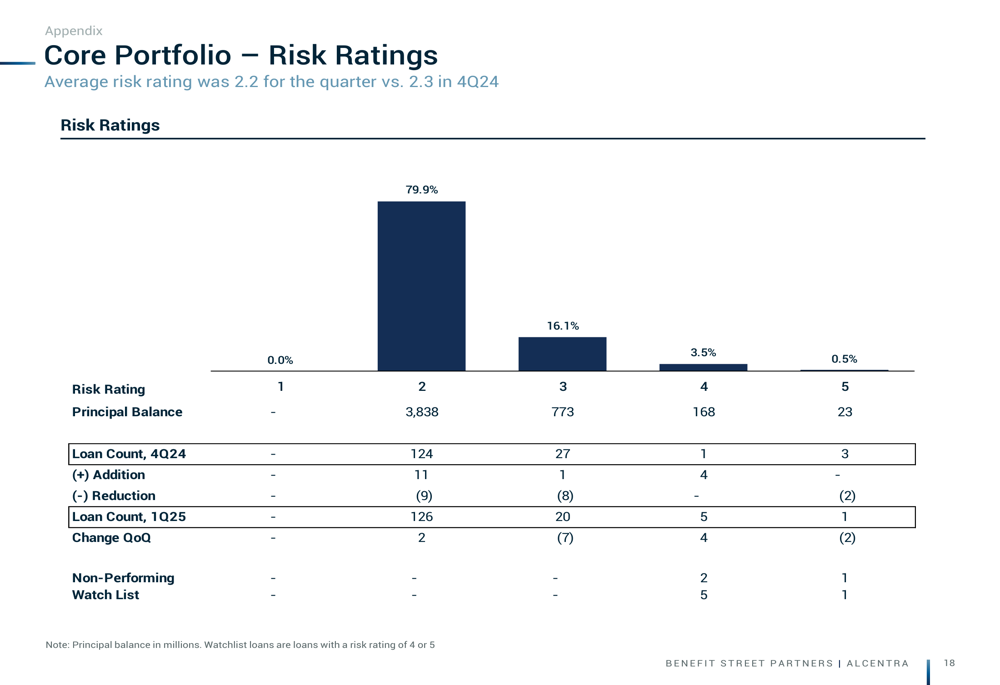

FBRT’s portfolio includes several watchlist loans with risk ratings of 4 or 5, primarily consisting of office and multifamily properties. These assets require close monitoring as they represent potential credit concerns.

The company is also managing twelve foreclosure real estate owned positions totaling $271 million, one investment real estate owned position of $122 million, and one equity investment position of $13 million. These non-performing assets continue to impact the company’s distributable earnings.

The risk rating distribution shows that 79.9% of the portfolio maintains a risk rating of 2, suggesting that despite the challenges with certain assets, the majority of the portfolio remains in stable condition:

Forward-Looking Statements

FBRT’s presentation indicates a continued focus on managing problem assets while maintaining its strategic emphasis on multifamily properties. The company’s strong liquidity position provides a buffer against market volatility and potential further deterioration in certain commercial real estate sectors.

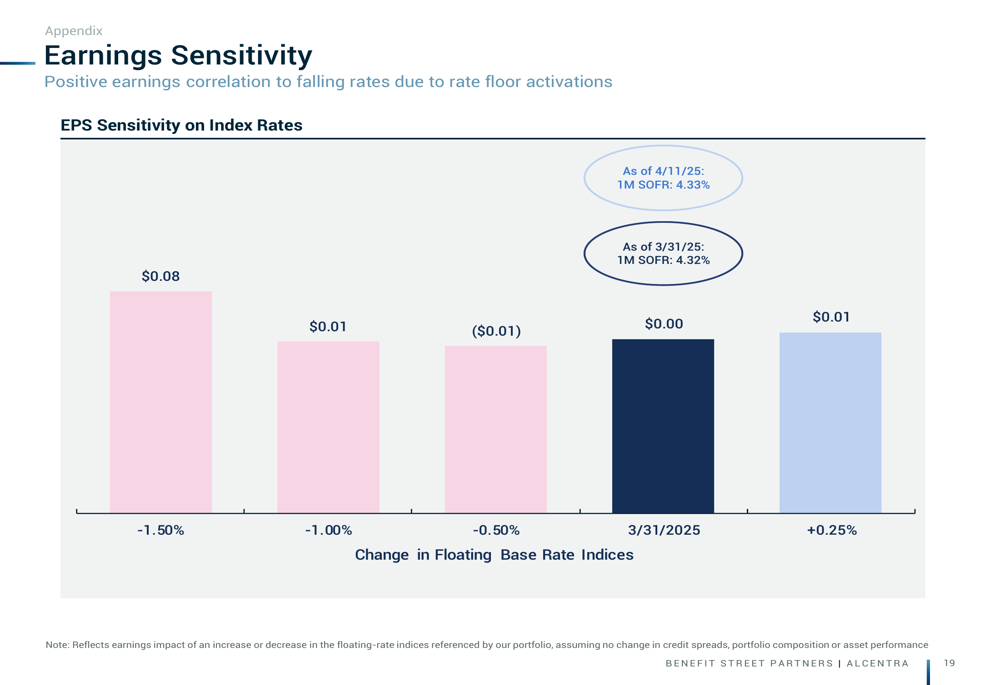

The company’s earnings sensitivity analysis suggests a positive correlation to falling interest rates due to rate floor activations, which could benefit FBRT if the Federal Reserve continues its easing cycle:

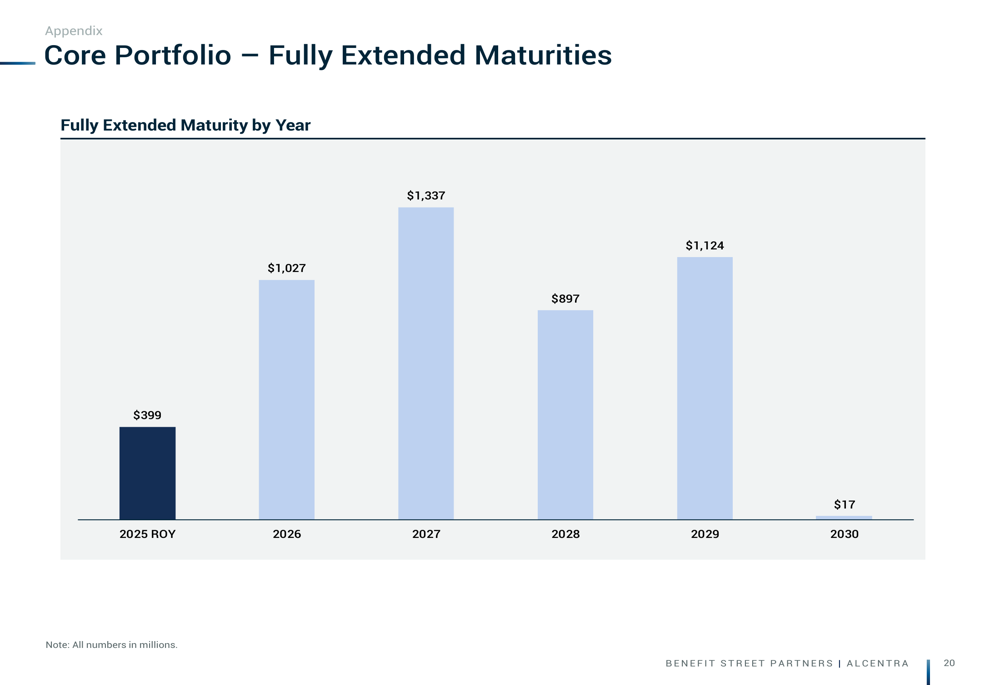

The maturity profile of FBRT’s loan portfolio shows a relatively balanced distribution over the coming years, which should help manage refinancing risk:

FBRT faces ongoing challenges in the commercial real estate market, particularly in the office sector, which represents a small but problematic portion of its portfolio. The company’s strategy of focusing on multifamily assets while maintaining strong liquidity appears designed to navigate these challenges while positioning for future growth opportunities.

The maintenance of the $0.355 quarterly dividend despite negative distributable earnings raises questions about dividend sustainability if earnings challenges persist. However, the company’s strong liquidity position and focus on resolving problem assets suggest a commitment to returning to positive distributable earnings in future quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.