Bitcoin price today: slides below $100k, enters bear market amid valuation jitters

Introduction & Market Context

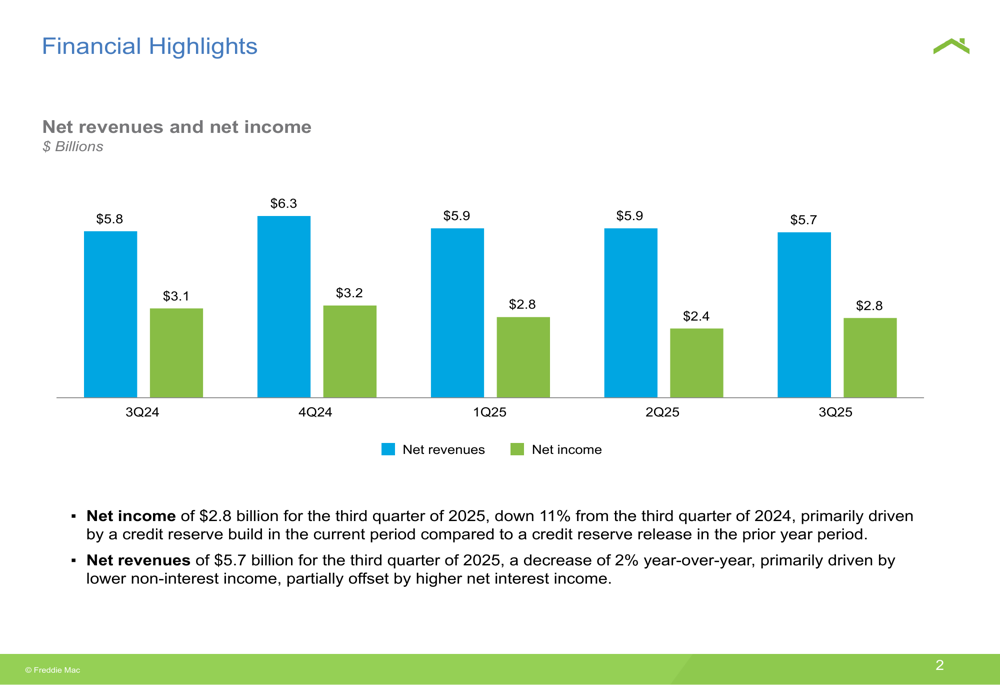

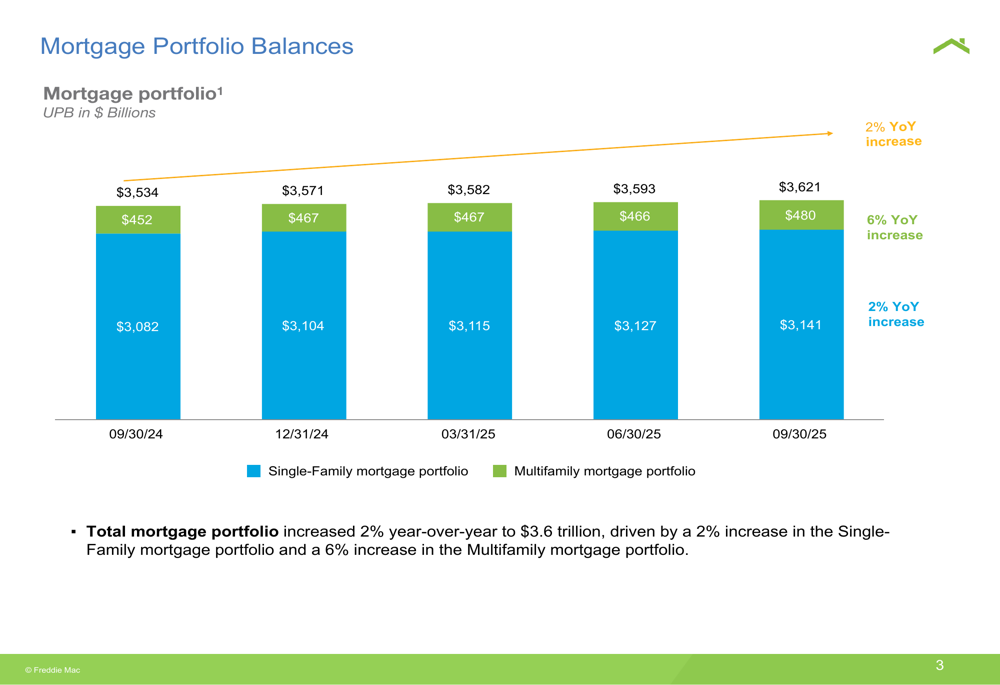

Freddie Mac (OTC:FMCC) released its third quarter 2025 financial results on October 30, revealing a mixed performance characterized by declining net income but steady growth in its mortgage portfolio. The government-sponsored enterprise reported net income of $2.8 billion, down 11% year-over-year, while its total mortgage portfolio reached $3.62 trillion, reflecting a 2% increase from the same period last year.

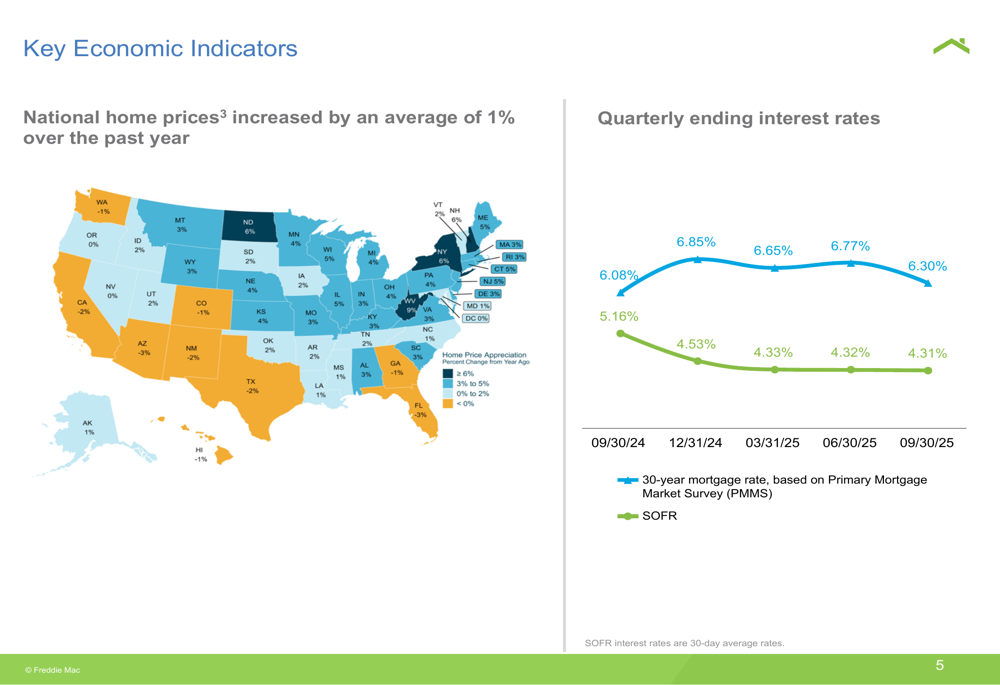

The financial results come amid a housing market characterized by elevated mortgage rates, with 30-year fixed rates fluctuating between 6.08% and 6.85% during the quarter. Despite these challenging conditions, Freddie Mac’s stock saw a modest pre-market increase of 0.88% to $10.30 following the announcement.

Quarterly Performance Highlights

Freddie Mac reported net revenues of $5.7 billion for Q3 2025, representing a 2% year-over-year decrease. Net income declined more significantly, falling 11% to $2.8 billion compared to Q3 2024. According to the earnings call transcript, this decline was partly attributable to a $175 million provision for credit losses and a substantial 66% drop in non-interest income to $284 million.

As shown in the following chart of quarterly financial performance, net revenues have remained relatively stable over the past five quarters, while net income has shown more variability:

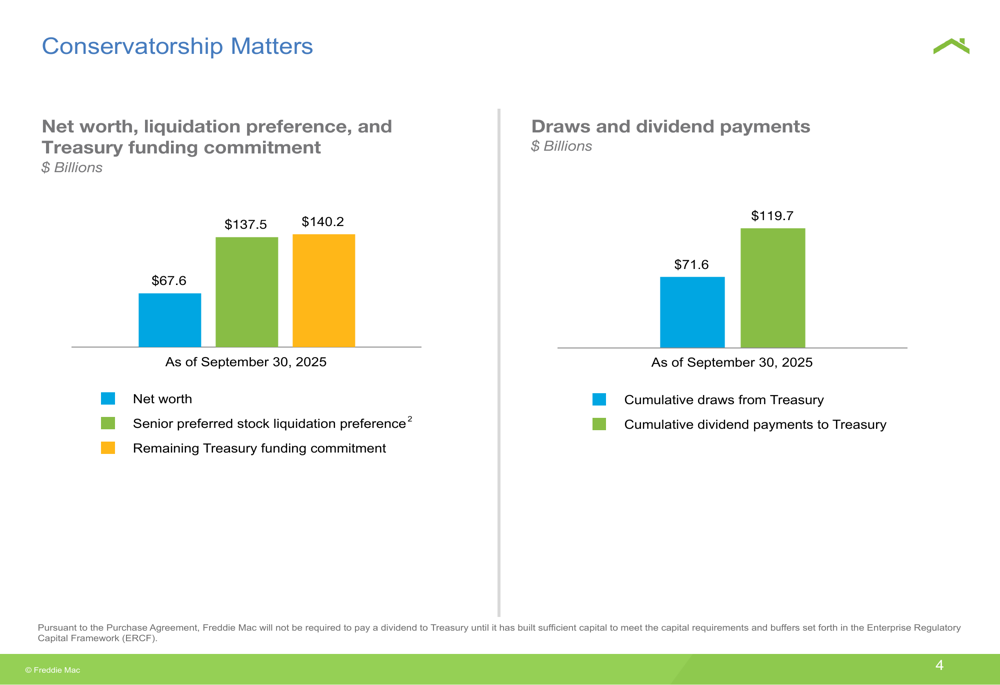

The company’s net worth reached $67.6 billion as of September 30, 2025, a significant improvement from previous years. Under the terms of its conservatorship agreement, Freddie Mac is not required to pay dividends to the Treasury until it meets capital requirements set forth in the Enterprise Regulatory Capital Framework (ERCF).

Mortgage Portfolio Growth

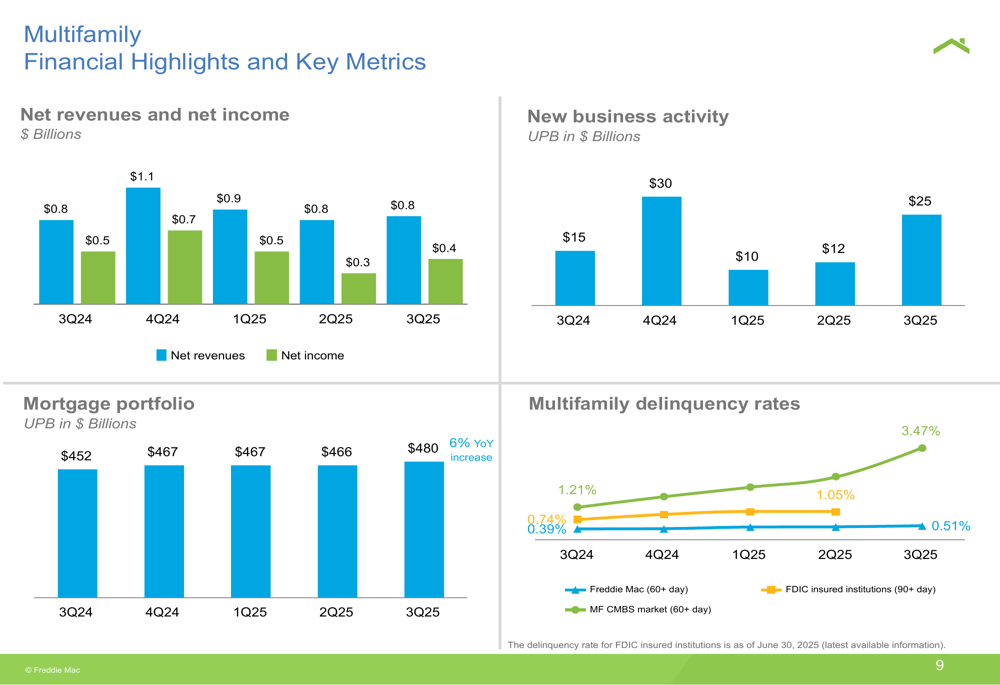

Despite the challenging interest rate environment, Freddie Mac’s mortgage portfolio continued to grow steadily. The total mortgage portfolio reached $3.62 trillion, with the single-family segment growing 2% year-over-year to $3.14 trillion and the multifamily portfolio increasing 6% to $480 billion.

The following chart illustrates the consistent growth in both segments of Freddie Mac’s mortgage portfolio:

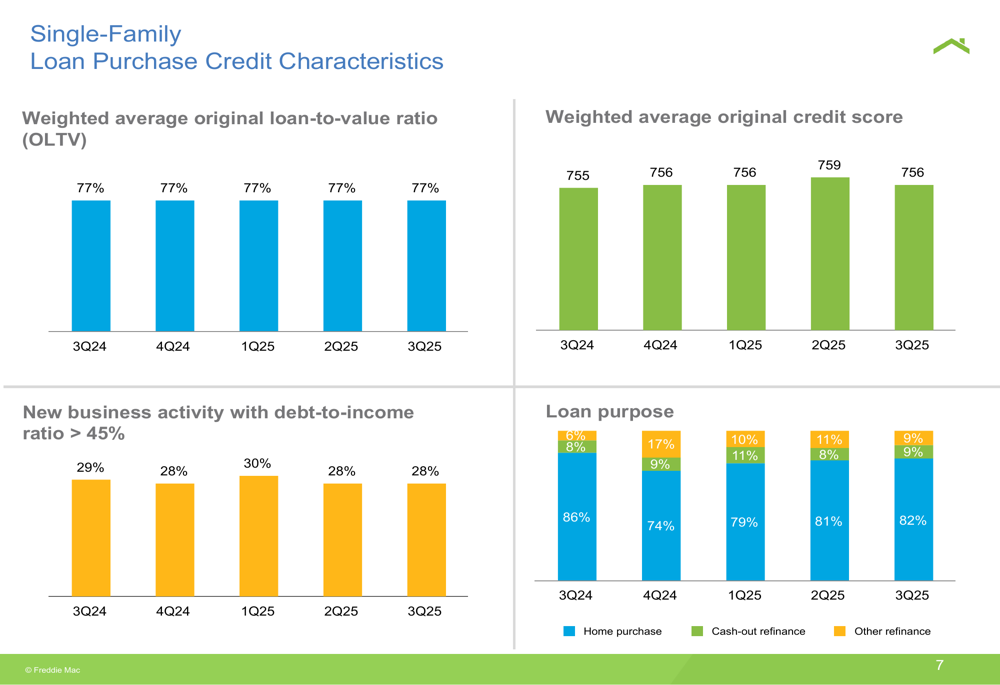

In the single-family segment, Freddie Mac maintained strong credit quality in its new loan purchases. The weighted average original credit score remained high at 755-759 throughout the past year, while the weighted average original loan-to-value ratio held steady at 77%.

The multifamily business also showed growth, though with some challenges. While the portfolio expanded to $480 billion, delinquency rates in this segment increased from 0.39% to 0.51% year-over-year, potentially signaling some stress in the commercial real estate market.

Credit Risk Management

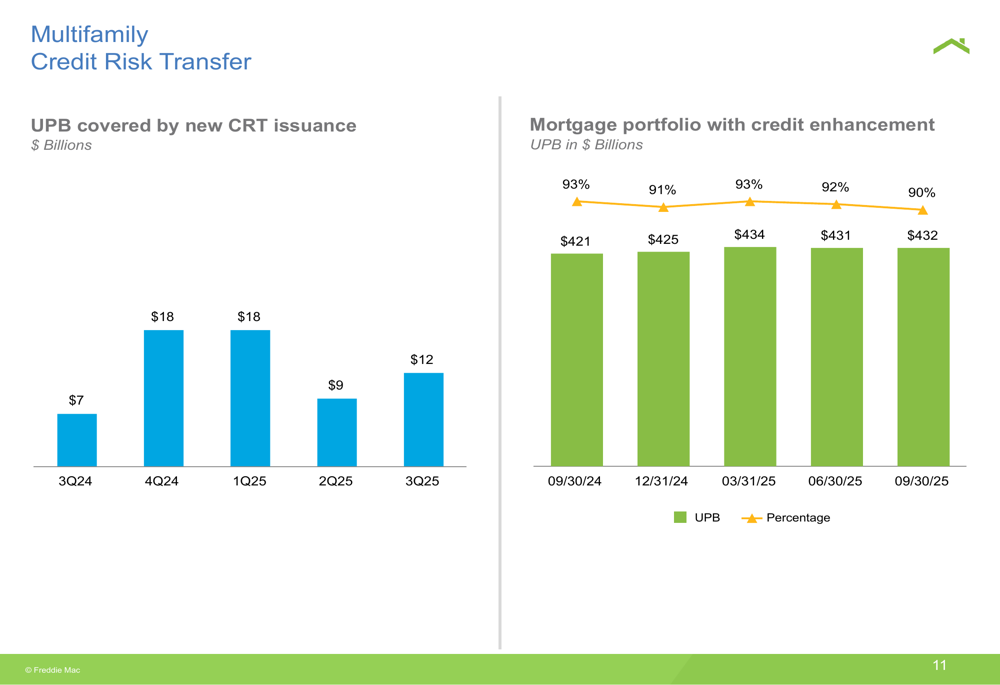

Freddie Mac continued to transfer credit risk to private investors through its Credit Risk Transfer (CRT) programs in both the single-family and multifamily segments. These initiatives are designed to reduce taxpayer exposure while maintaining Freddie Mac’s ability to support the housing market.

In the single-family business, the UPB (unpaid principal balance) covered by new CRT issuance fluctuated between $31 billion and $63 billion per quarter, with a total of $1.94 trillion of the portfolio now having some form of credit enhancement, representing approximately 62% coverage.

The multifamily segment showed even stronger risk transfer activity, with 90% of the portfolio covered by credit enhancements. The UPB covered by new multifamily CRT issuance increased from $7 billion in Q3 2024 to $12 billion in Q3 2025.

Housing Market Support

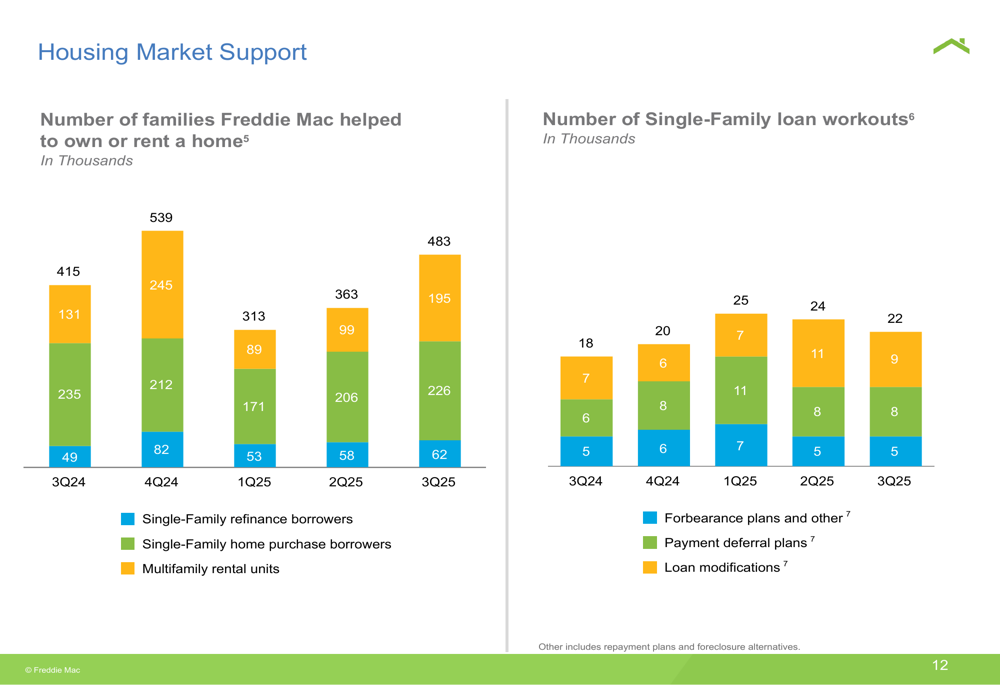

Despite financial challenges, Freddie Mac continued its mission to support affordable housing. The company’s presentation highlighted its efforts to help families own or rent homes, with particular emphasis on first-time homebuyers and affordable rental units.

The following chart shows the number of families Freddie Mac helped through various programs, including home purchases, refinances, and rental housing support:

According to the earnings call, Freddie Mac facilitated $124 billion in housing market liquidity during the quarter, representing a 33% increase. CFO Jim Whitlinger emphasized the company’s commitment to the "American dream," stating, "That’s the American dream and our work helps make it true for more than 1,000 families every day."

Forward-Looking Statements

Looking ahead, Freddie Mac plans to continue expanding affordable housing options and enhancing digital mortgage tools. The company’s presentation included a U.S. map showing home price changes and interest rate trends, providing context for its strategic focus areas.

Revenue forecasts for fiscal years 2025 and 2026 stand at $20.7 billion and $21.8 billion respectively, indicating expectations for modest growth despite current challenges. The company’s substantial remaining Treasury funding commitment of $140.2 billion provides a significant cushion against potential market disruptions.

While Freddie Mac faces headwinds from elevated interest rates and potential credit quality concerns, its growing mortgage portfolio and strong capital position suggest resilience in its core business. Investors will be watching closely to see if the company can reverse the trend of declining net income while continuing to fulfill its mission of supporting affordable housing in the United States.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.