Hedge funds cut NFLX, keep big bets on MSFT, AMZN, add NVDA

Introduction & Market Context

G Mining Ventures Corp (TSX:GMIN | OTCQX:GMINE) delivered solid first-quarter 2025 results while advancing its ambitious growth strategy, according to the company’s May 2025 investor presentation. The gold producer, which operates the Tocantinzinho mine in Brazil and is developing the Oko West project in Guyana, saw its stock close at $18.64 on May 15, down 2.68% for the day, but still trading significantly higher than its 52-week low of $7.40.

The company’s "Buy. Build. Operate." strategy has delivered impressive returns for shareholders, with the stock up 489% since its formal investment decision and 856% since its 2020 RTO. GMIN was recently added to three major indices (S&P/TSX, GDX (NYSE:GDX), and GDXJ), reflecting its growing market presence.

As shown in the following slide, G Mining’s strategy focuses on three key assets across mining-friendly jurisdictions in South America, with a vision to become the next intermediate gold producer:

Quarterly Performance Highlights

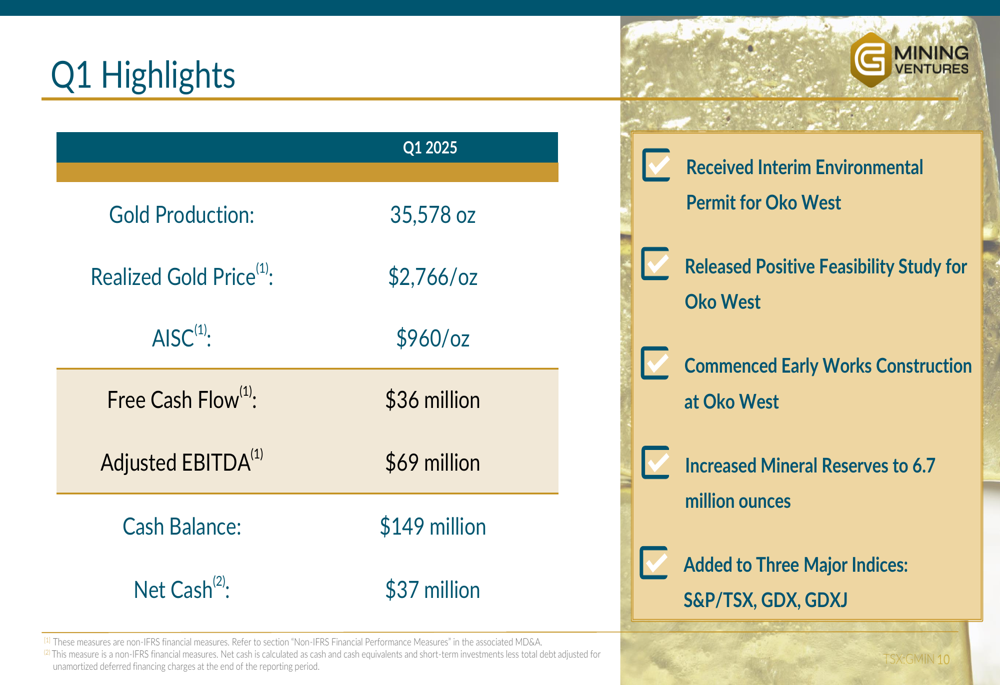

G Mining reported gold production of 35,578 ounces in Q1 2025 at its Tocantinzinho mine, with a realized gold price of $2,766 per ounce. The company achieved all-in sustaining costs (AISC) of $960 per ounce, positioning it in the first quartile of the global cost curve. This operational efficiency translated to strong financial results, with free cash flow of $36 million and adjusted EBITDA of $69 million for the quarter.

The following slide highlights key Q1 2025 metrics, including the company’s healthy cash balance of $149 million and net cash position of $37 million:

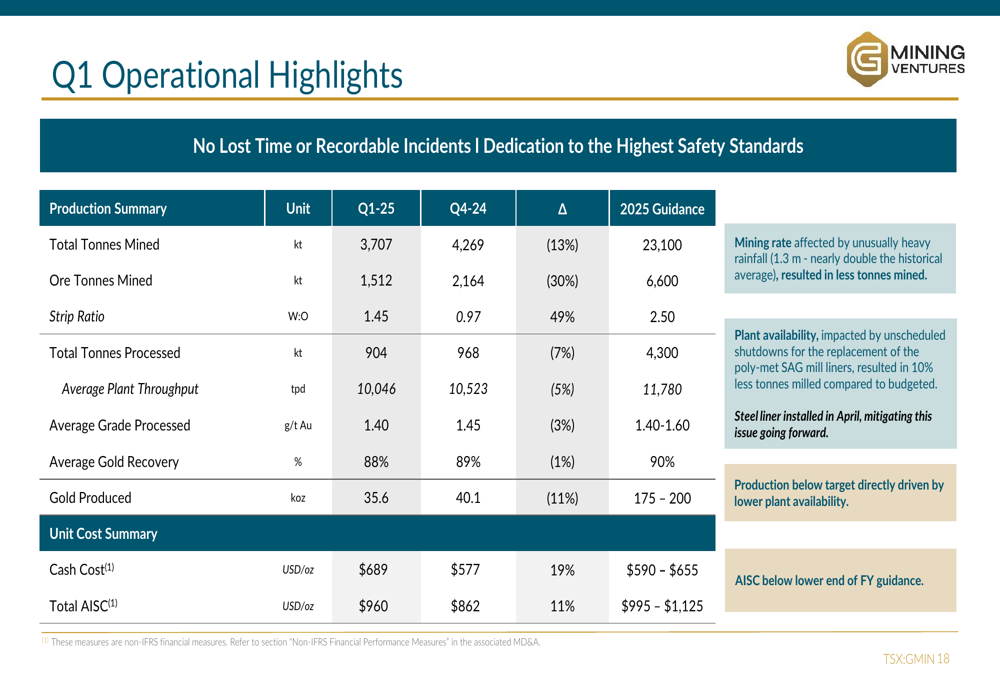

Despite these solid results, Q1 production was 11% lower than Q4 2024, primarily due to unusually heavy rainfall affecting mining rates and lower plant availability. The company processed 904,000 tonnes at an average grade of 1.40 g/t gold with an 88% recovery rate. Cash costs increased 19% quarter-over-quarter to $689 per ounce, while AISC rose 11% to $960 per ounce.

As illustrated in the following operational highlights, the company remains well-positioned to meet its 2025 guidance despite these temporary challenges:

Strategic Initiatives

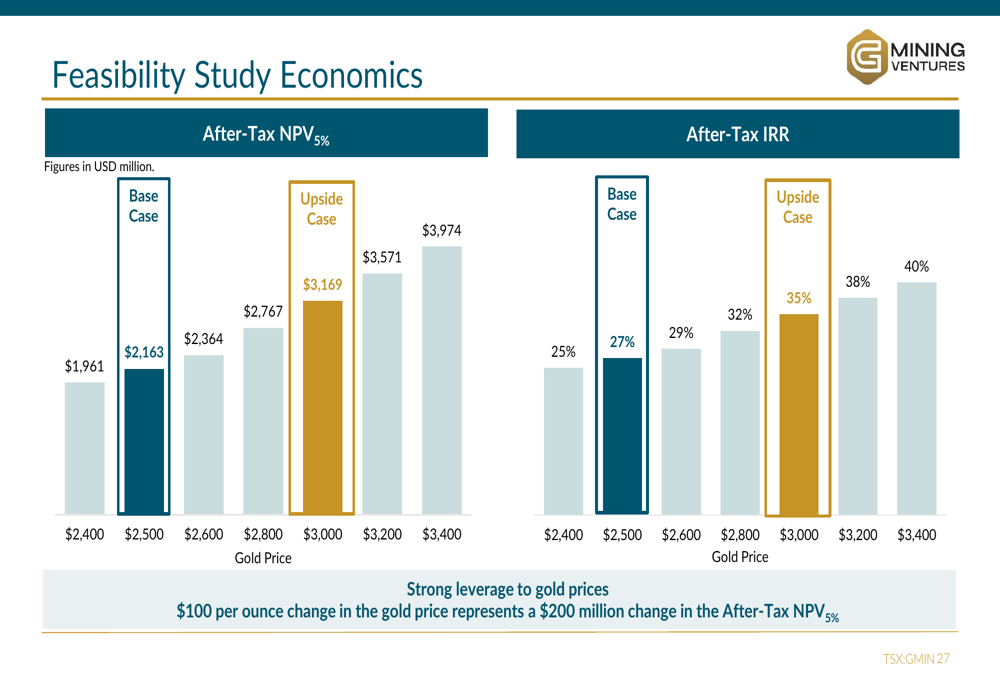

G Mining’s growth strategy centers on developing the Oko West Gold Project in Guyana, which completed its Definitive Feasibility Study in April 2025. The project boasts 4.6 million ounces of gold reserves and is expected to produce an average of 350,000 ounces annually at an AISC of $1,123 per ounce over a 12-year mine life.

The following slide showcases the project’s impressive economics, with an after-tax NPV5% of $2.16 billion and IRR of 27% at the base case gold price:

The company has outlined an accelerated timeline to production for Oko West, with early works construction already underway and a final construction decision expected in the second half of 2025. First production is targeted for Q4 2027, which would double the company’s annual gold production to over 500,000 ounces by 2028.

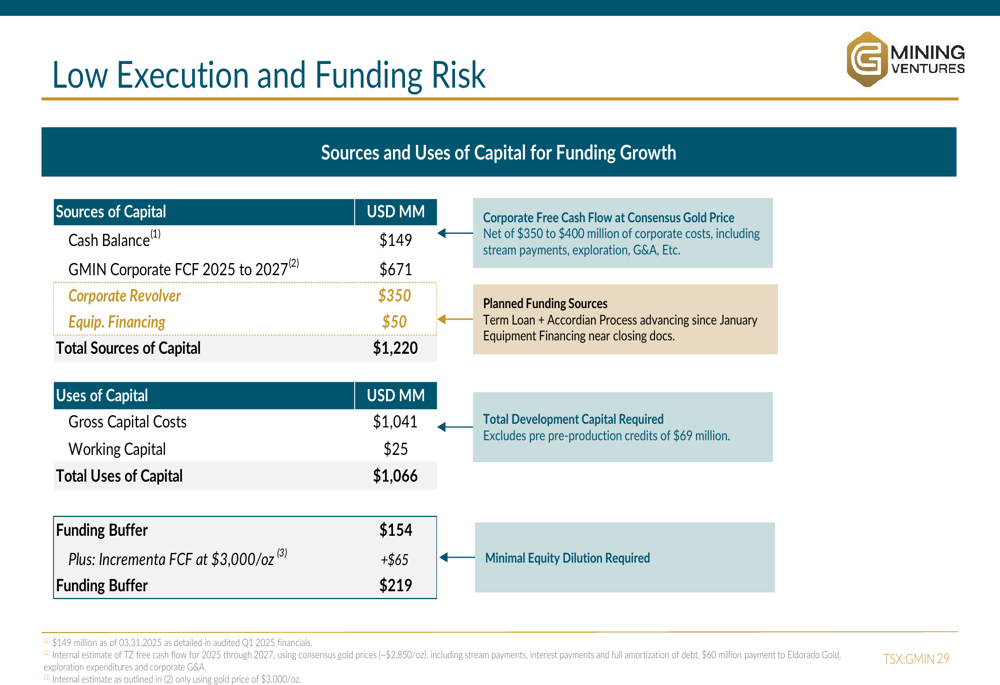

G Mining’s funding strategy for Oko West appears robust, with planned sources of capital totaling $1.22 billion against uses of $1.07 billion, providing a funding buffer of $154 million. The company expects to finance the project primarily through operating cash flow from Tocantinzinho, supplemented by debt facilities.

The following slide details the company’s funding plan for Oko West:

In addition to Tocantinzinho and Oko West, G Mining is advancing exploration at its Gurupi Project in Brazil, which it acquired from BHP in Q4 2024. The project has 1.8 million ounces of indicated and 0.8 million ounces of inferred gold resources, with exploration activities planned to restart in H1 2025.

Forward-Looking Statements

For 2025, G Mining has provided guidance of 175,000-200,000 ounces of gold production at Tocantinzinho, with site-level AISC of $903-$1,033 per ounce. The company expects to reach nameplate processing capacity of 12,890 tonnes per day in early Q2 2025.

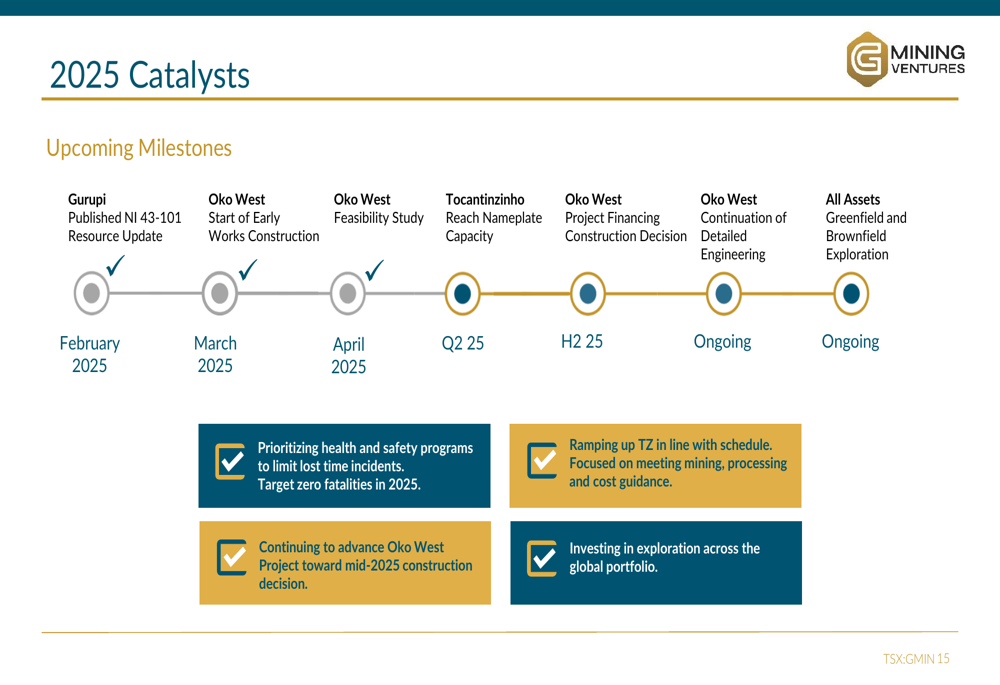

The following slide outlines key catalysts for 2025, including the ramp-up of Tocantinzinho to nameplate capacity, advancement of Oko West toward a construction decision, and continued exploration across the portfolio:

Management emphasized its focus on health and safety programs, meeting production and cost guidance at Tocantinzinho, advancing Oko West toward a mid-2025 construction decision, and investing in exploration across its global portfolio.

Competitive Industry Position

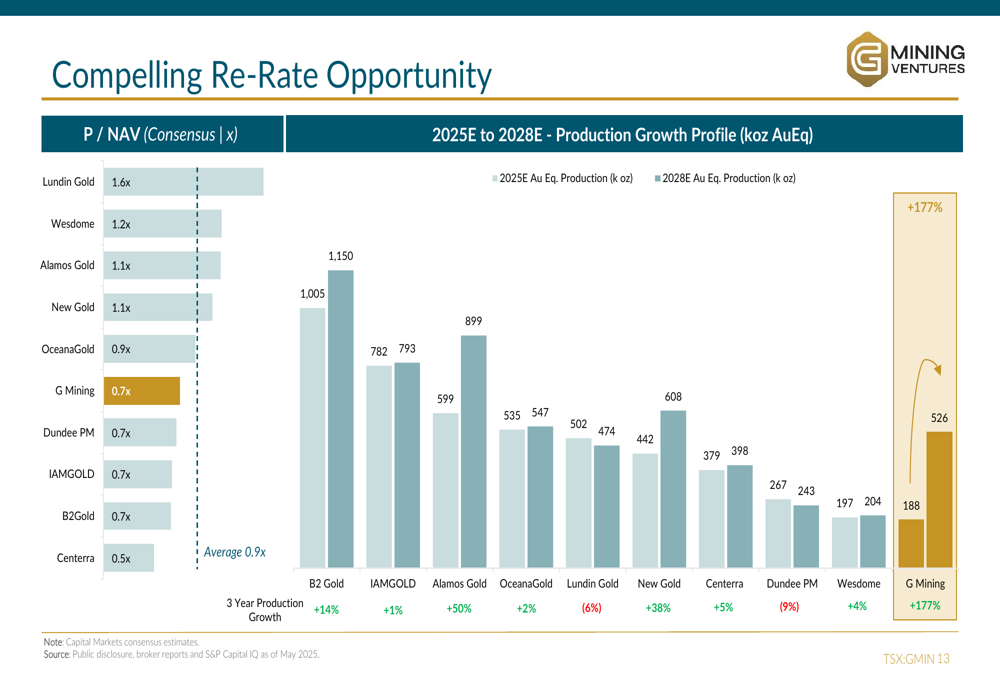

G Mining positions itself as an emerging intermediate gold producer with a compelling valuation opportunity. The company’s P/NAV ratio of 0.7x compares favorably to the intermediate producer average of 0.93x, suggesting potential for share price appreciation as the company executes its growth strategy.

The following slide illustrates G Mining’s exceptional three-year production growth profile of 177% compared to peers, highlighting its unique position in the market:

The company’s competitive advantage stems from its management team’s track record of delivering mining projects on time and on budget. The Gignac family, which leads G Mining, has successfully built multiple mines for companies including IAMGold (TSX:IMG), Newmont, and Lundin Gold (OTC:LUGDF).

As shown in the following slide, this expertise in mine building provides a significant edge in project execution:

G Mining’s strategy of acquiring projects during their "orphan period" and creating value through de-risking and execution has proven successful with Tocantinzinho and is being applied to Oko West. With strong operational performance, a clear growth strategy, and experienced leadership, G Mining Ventures appears well-positioned to achieve its goal of becoming a leading intermediate gold producer.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.