TSX runs higher on rate cut expectations

Introduction & Market Context

Gannett Co Inc (NYSE:GCI), the diversified media company and publisher of USA Today, presented its second quarter 2025 financial results on July 31, showcasing significant progress in its digital transformation strategy and a return to profitability. The company reported total revenues of $584.9 million, with digital revenues now representing 45% of the total, signaling a milestone in Gannett’s evolution from a traditional print publisher to a digital-first media enterprise.

Following a challenging first quarter where the company reported a net loss of $7 million, Gannett has demonstrated a remarkable turnaround with a Q2 net income of $78.4 million. This improvement aligns with the company’s stated goal of stabilizing digital revenues in the second quarter, which they appear to have achieved.

Quarterly Performance Highlights

Gannett’s Q2 2025 results showed sequential improvement across several key metrics. Total (EPA:TTEF) revenues reached $584.9 million, up from $571.6 million in Q1. The company reported Total Adjusted EBITDA of $64.2 million, representing an 11.0% margin. Cash provided by operating activities was $32.6 million, showing a 39.7% sequential increase compared to Q1 2025, while free cash flow reached $17.6 million, up 73.1% sequentially.

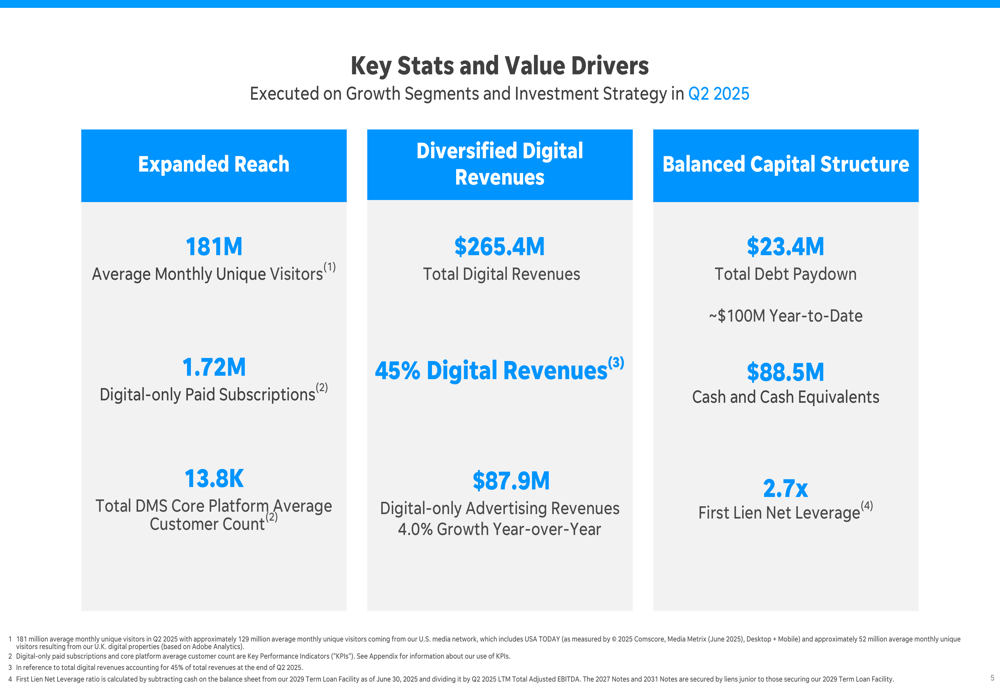

As shown in the following key statistics and value drivers chart:

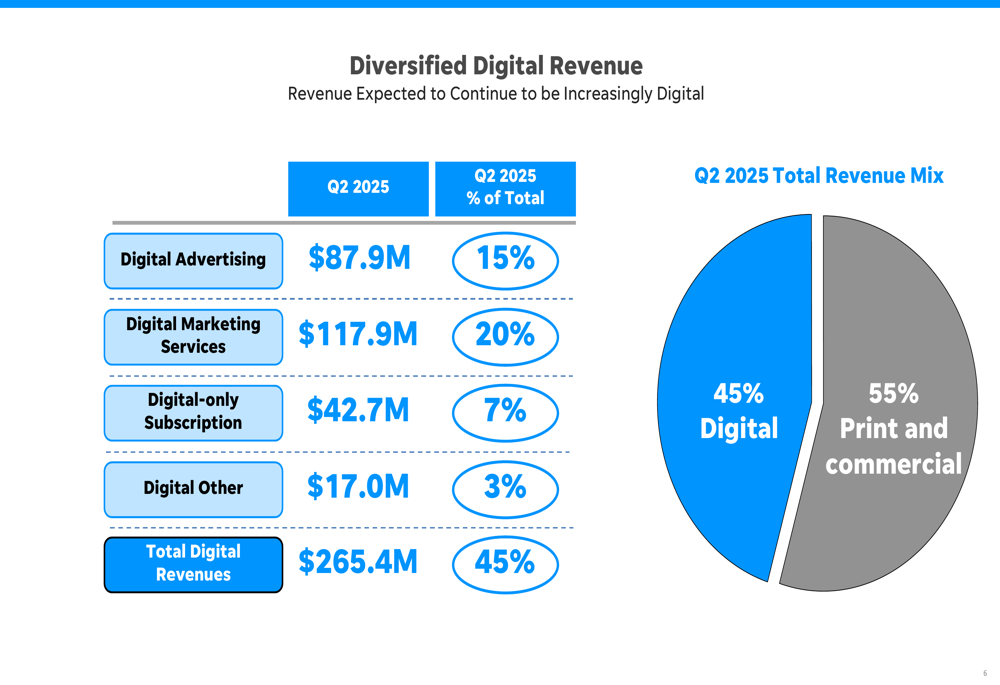

Digital revenues totaled $265.4 million in Q2, accounting for 45% of total revenues. Digital advertising revenues showed a positive growth of 4.0% year-over-year, reaching $87.9 million. This represents a significant improvement from the 1.3% decline reported in Q1 2025.

The breakdown of Gannett’s diversified digital revenue streams illustrates the company’s progress in building multiple digital income sources:

Digital Transformation Progress

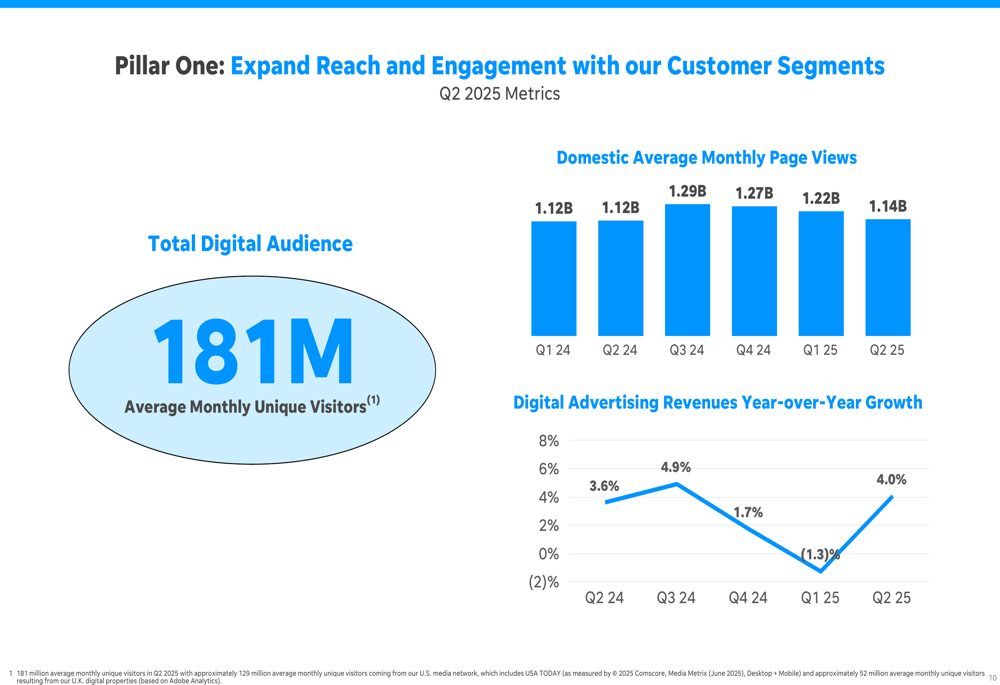

Gannett’s digital transformation strategy is centered around three key operating pillars: expanding reach and engagement, diversifying digital revenue, and strengthening the capital structure. The company reached 181 million average monthly unique visitors in Q2 2025, demonstrating its extensive digital audience reach.

The following chart shows the company’s digital advertising revenue growth trajectory, which has returned to positive territory in Q2 2025 after a decline in the previous quarter:

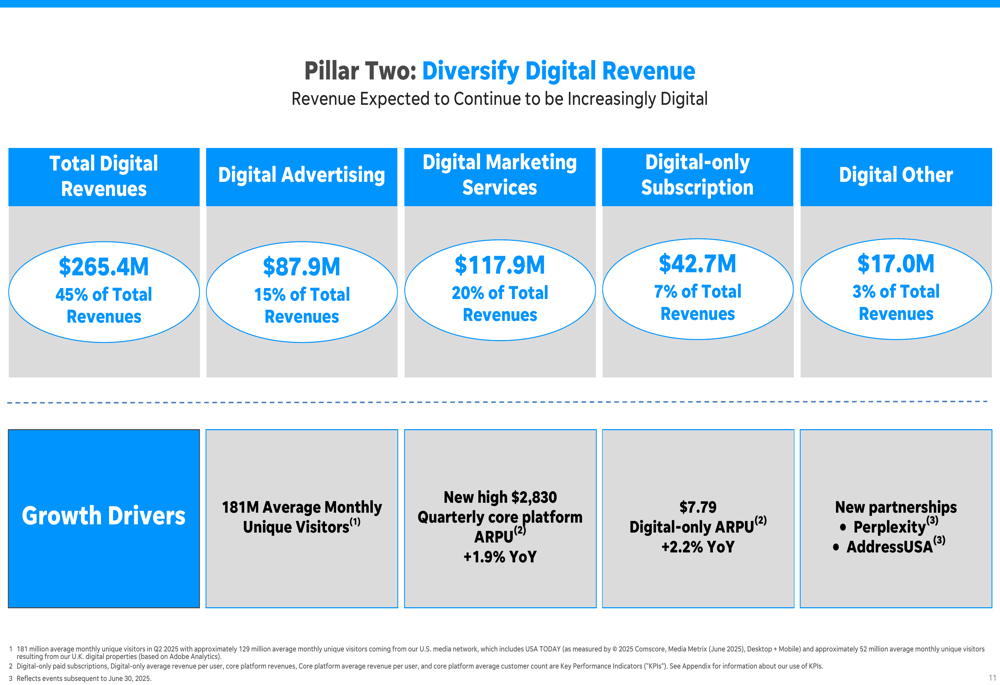

Digital-only paid subscriptions reached 1.72 million, while digital-only ARPU (Average Revenue Per User) increased 2.2% year-over-year to $7.79. The company also highlighted new partnerships with Perplexity and AddressUSA as part of its strategy to expand digital offerings.

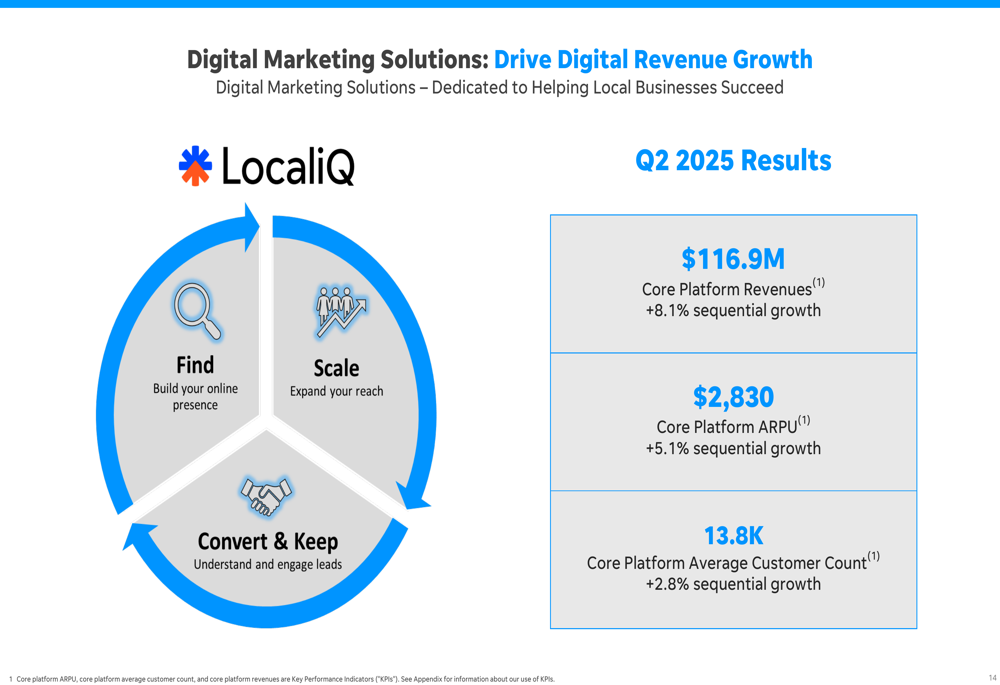

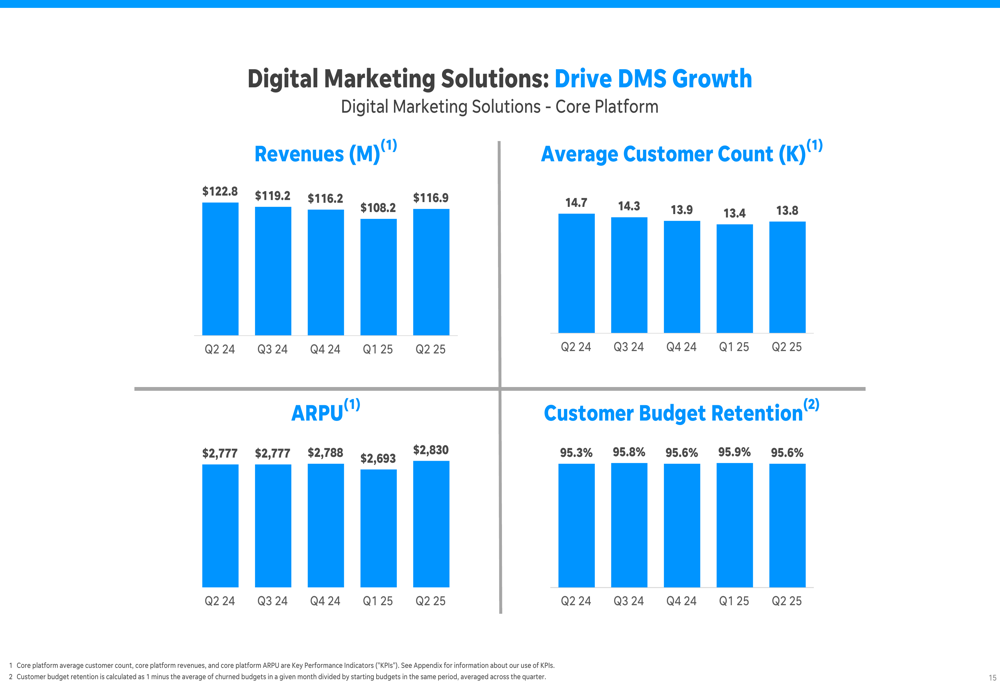

The Digital Marketing Solutions (DMS) segment showed particularly strong performance, with core platform revenues of $116.9 million, representing 8.1% sequential growth. Core platform ARPU increased to $2,830, up 5.1% sequentially and 1.9% year-over-year, while the core platform average customer count grew to 13.8K, a 2.8% sequential increase.

The following slide details the company’s digital revenue diversification strategy and key growth drivers:

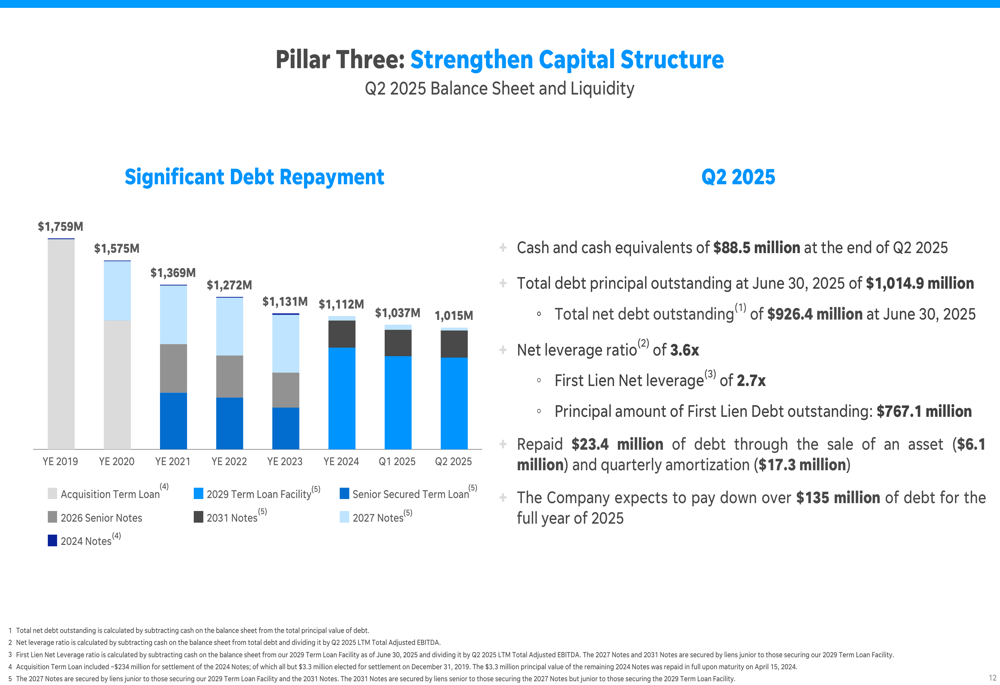

Capital Structure Improvements

Gannett continued to make progress in strengthening its balance sheet during Q2 2025. The company reduced its total debt by $23.4 million in the quarter, bringing the year-to-date debt reduction to approximately $100 million. As of June 30, 2025, Gannett reported cash and cash equivalents of $88.5 million and a first lien net leverage ratio of 2.7x.

The following chart illustrates Gannett’s progress in reducing its debt load:

Total debt principal outstanding at the end of Q2 stood at $1,014.9 million, with a net leverage ratio of 3.6x. This represents significant progress from the company’s debt position at the end of 2019, demonstrating management’s commitment to improving the capital structure.

Forward-Looking Statements

Looking ahead, Gannett provided an updated business outlook for the remainder of 2025. For the second half of the year, the company expects total digital revenues to grow approximately 3%-5% on a same store basis, while total revenues are projected to decline in the low single digits on a same store basis.

For the full year 2025, Gannett anticipates total digital revenues to be flat on a same store basis versus the prior year, with total revenues down in the low-mid single digits on a same store basis. The company expects to achieve flat same store revenue trends by early 2026, with digital revenues projected to make up more than 50% of total revenues during 2026.

The Digital Marketing Solutions segment is expected to continue driving growth, as shown in the following performance metrics:

Strategic Initiatives

Gannett’s strategy continues to focus on maximizing recurring digital revenue growth to achieve sustainable total revenue growth. The company is leveraging its extensive reach of 181 million average monthly unique visitors to drive digital advertising and subscription revenue.

The Digital Marketing Solutions segment, which includes the LocaliQ platform, remains a key growth driver with its "Find, Scale, and Convert & Keep" approach. The segment’s performance metrics show positive momentum:

In conclusion, Gannett’s Q2 2025 results demonstrate meaningful progress in its digital transformation journey and financial turnaround. With digital revenues now representing 45% of total revenues and on track to exceed 50% in 2026, the company appears to be successfully executing its strategy of evolving from a traditional print publisher to a digital-first media and marketing solutions provider. The return to profitability, sequential growth in key metrics, and continued debt reduction suggest that Gannett’s strategic initiatives are gaining traction, though challenges remain in achieving sustainable total revenue growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.