Microvast Holdings announces departure of chief financial officer

Gates Industrial Corporation plc (NYSE:GTES) reported solid second-quarter 2025 results on July 30, demonstrating resilience in a challenging demand environment while raising its full-year earnings guidance. The company maintained strong margins and continued to strengthen its balance sheet, positioning itself for future growth opportunities in strategic markets.

Quarterly Performance Highlights

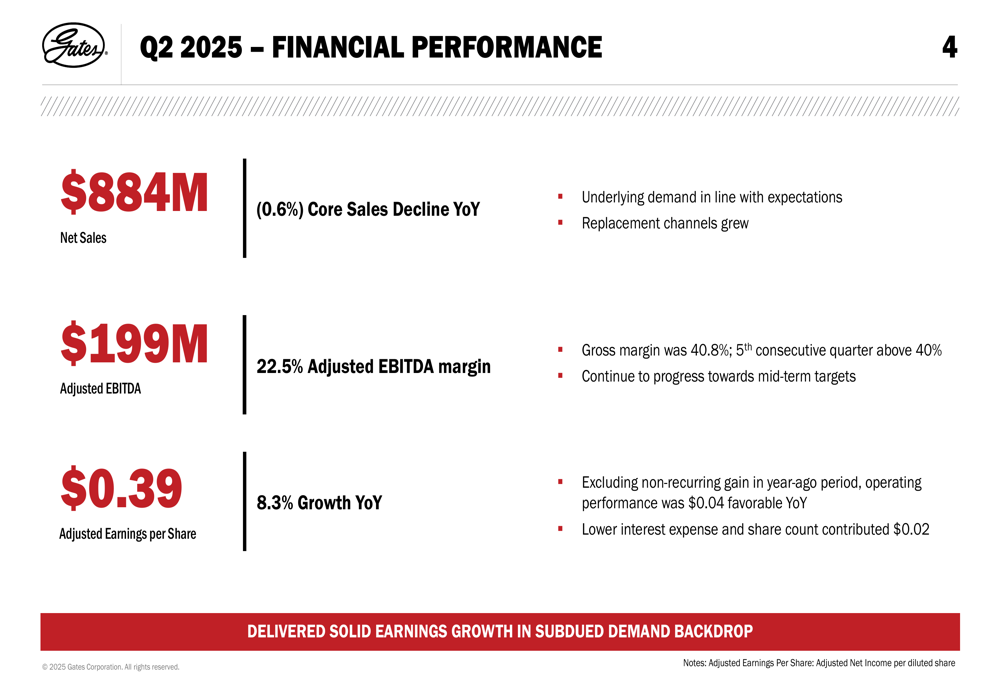

Gates Industrial delivered $884 million in net sales for Q2 2025, representing a modest core sales decline of 0.6% year-over-year. Despite this slight revenue contraction, the company achieved an adjusted EBITDA of $199 million with a 22.5% margin and grew adjusted earnings per share by 8.3% to $0.39.

"Sales and profitability were consistent with expectations," the company noted, highlighting that underlying demand aligned with forecasts while replacement channels showed growth. Gates also maintained its gross margin strength at 40.8%, marking the fifth consecutive quarter above 40%.

As shown in the following financial performance summary:

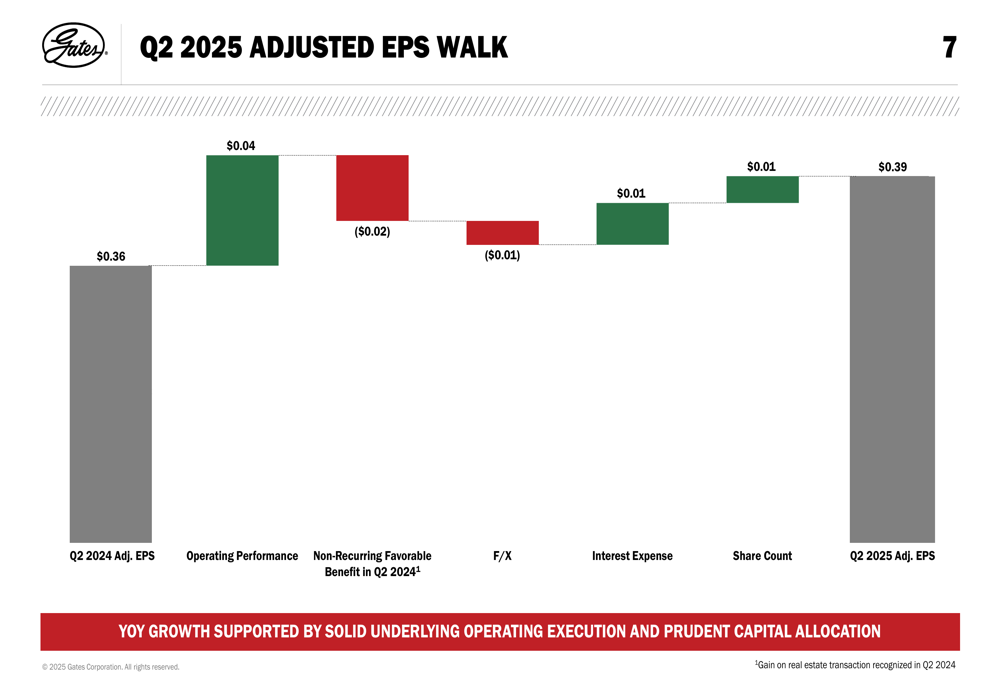

The company’s earnings growth was supported by solid operating execution and prudent capital allocation, offsetting a non-recurring gain in the year-ago period. A detailed breakdown of the adjusted EPS walk shows how various factors contributed to the $0.03 increase from Q2 2024:

Segment and Regional Performance

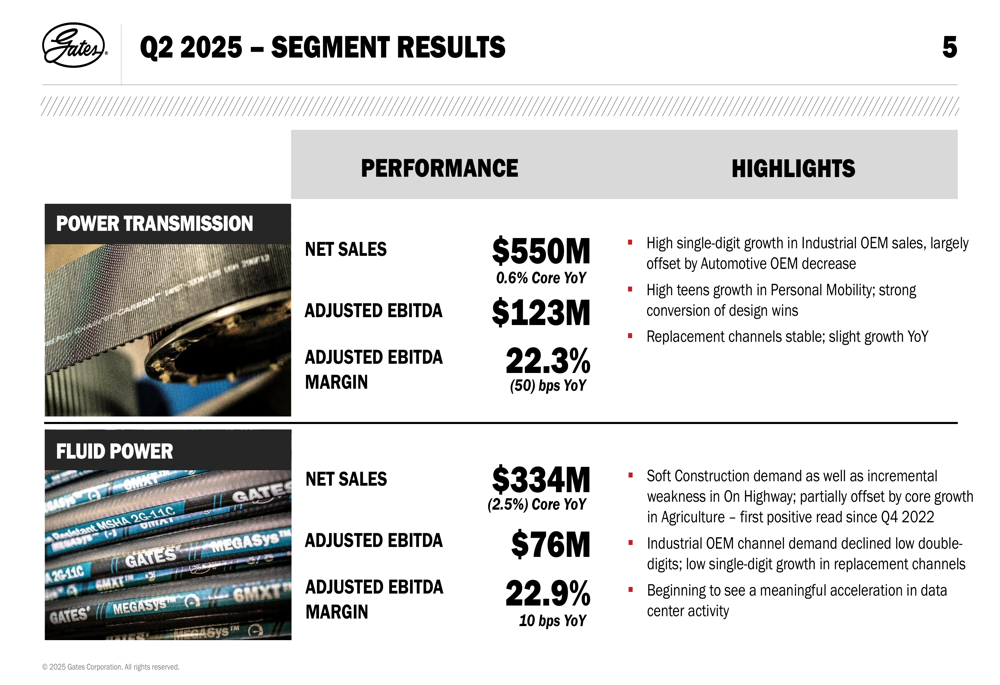

Gates Industrial’s performance varied across its two main business segments. The Power Transmission segment recorded $550 million in net sales with a slight core growth of 0.6% year-over-year, while the Fluid Power segment generated $334 million in net sales with a 2.5% core decline.

The Power Transmission segment benefited from high single-digit growth in Industrial OEM sales and high teens growth in Personal Mobility, which helped offset decreases in Automotive OEM. Meanwhile, the Fluid Power segment faced challenges from soft construction demand and weakness in On Highway applications, though it saw growth in Agriculture and began experiencing "meaningful acceleration in data center activity."

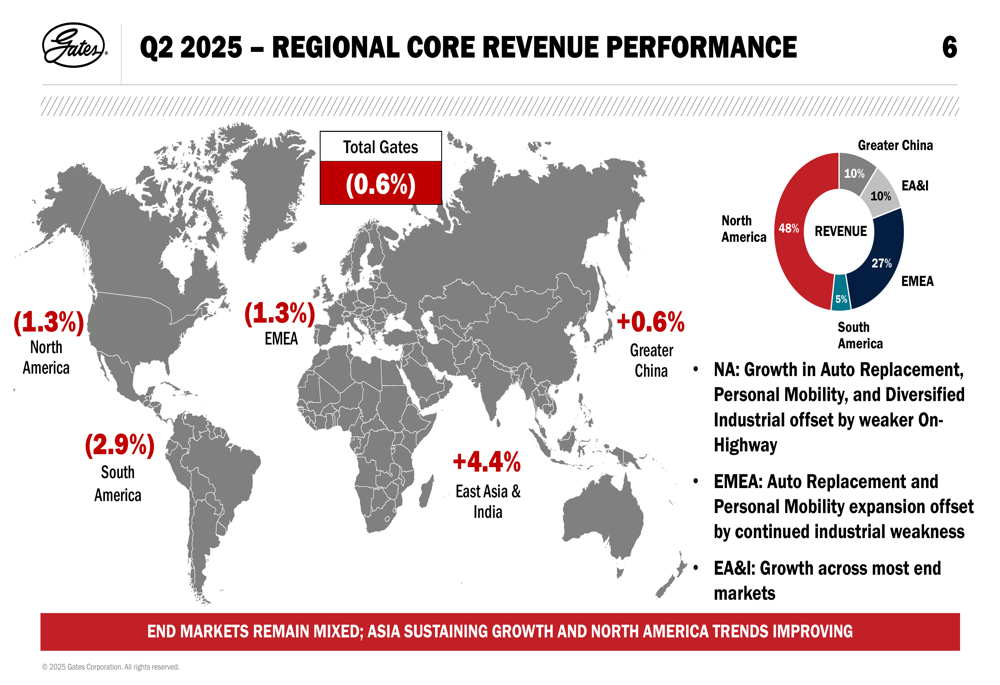

Geographically, Gates’ performance reflected regional economic conditions, with Asian markets outperforming Western markets. East Asia & India led with 4.4% core growth, while North America and EMEA both experienced 1.3% declines.

Strategic Growth Initiatives

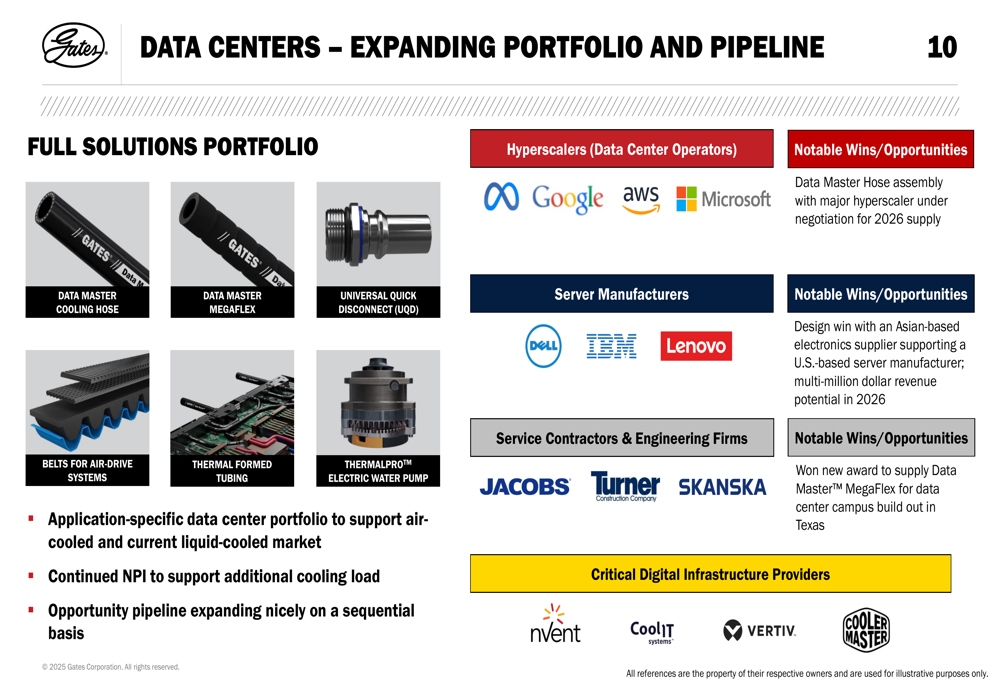

Gates highlighted two key strategic growth areas during its presentation: data centers and personal mobility. The company is expanding its portfolio of cooling solutions for data centers, with particular focus on both air-cooled and liquid-cooled applications. Management noted a significant design win with an Asian-based electronics supplier supporting a U.S.-based server manufacturer, which has "multi-million dollar revenue potential in 2026."

"We’re beginning to see a meaningful acceleration in data center activity," the company stated, positioning itself to capitalize on the growing demand for cooling solutions in this sector.

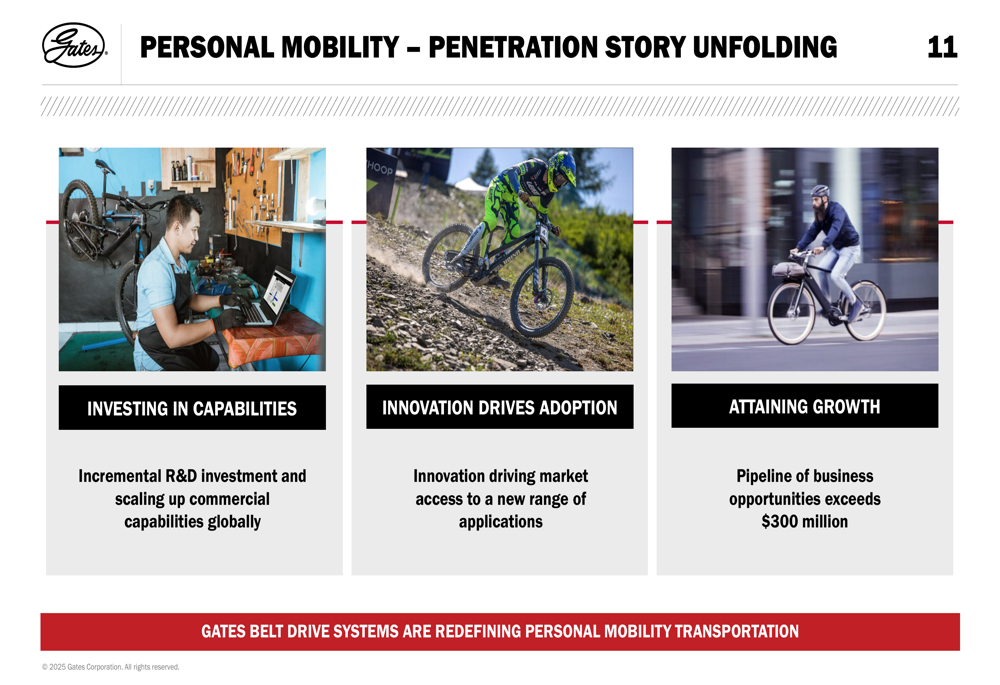

In the personal mobility segment, Gates reported high teens growth and an expanding pipeline of business opportunities exceeding $300 million. The company is investing in R&D and scaling up commercial capabilities globally to drive innovation and market adoption.

Updated Guidance & Outlook

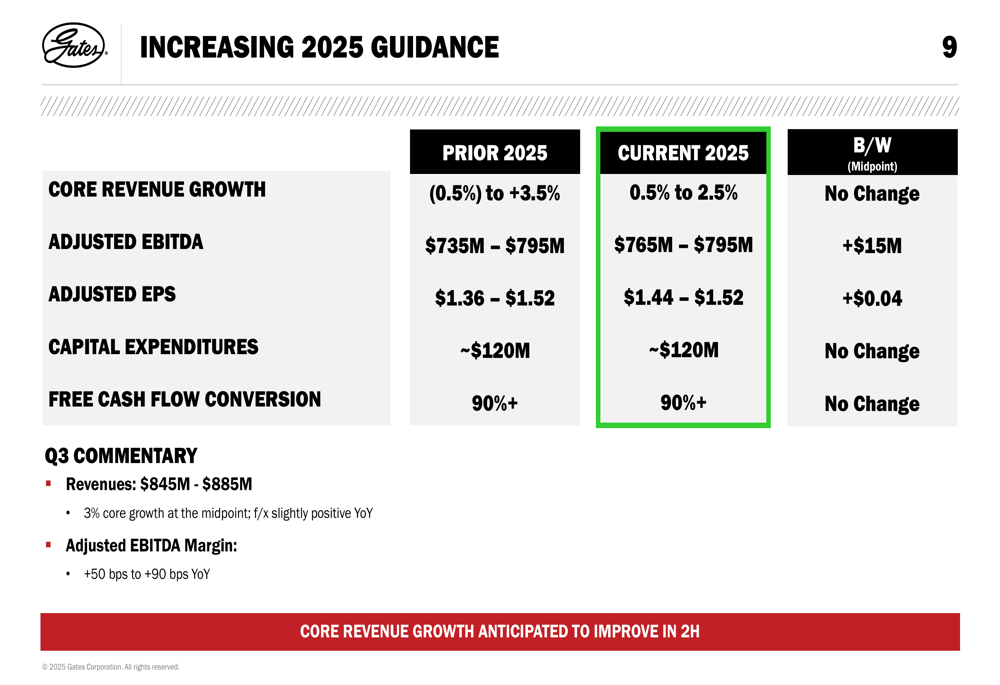

Based on its first-half performance and improving outlook, Gates Industrial raised its full-year 2025 guidance for adjusted EBITDA and adjusted EPS. The company narrowed its core revenue growth range to 0.5%-2.5% (from previous -0.5% to +3.5%), increased its adjusted EBITDA midpoint by $15 million to $765M-$795M, and raised its adjusted EPS guidance by $0.04 at the midpoint to $1.44-$1.52.

For Q3 2025, Gates expects revenues between $845 million and $885 million, representing 3% core growth at the midpoint, with adjusted EBITDA margin improvement of 50 to 90 basis points year-over-year.

"Core revenue growth is anticipated to improve in the second half," the company stated, suggesting increasing confidence in its business trajectory for the remainder of the year.

Financial Position & Capital Allocation

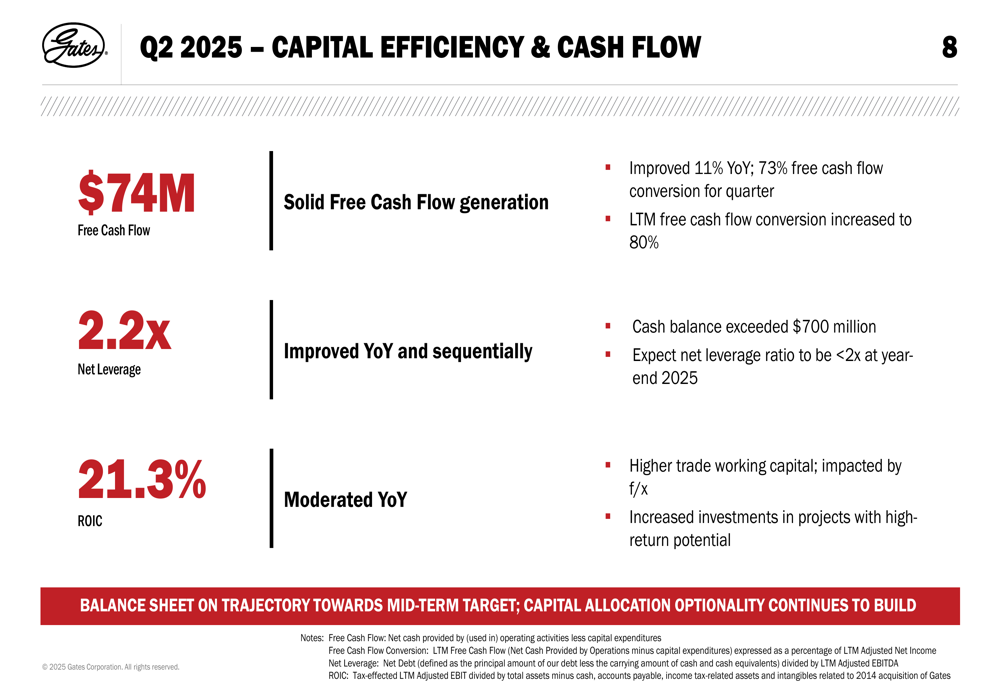

Gates Industrial continued to strengthen its balance sheet in Q2, generating $74 million in free cash flow (a 11% year-over-year improvement) with 73% free cash flow conversion for the quarter. The company’s net leverage ratio declined to 2.2x and is expected to fall below 2x by year-end 2025.

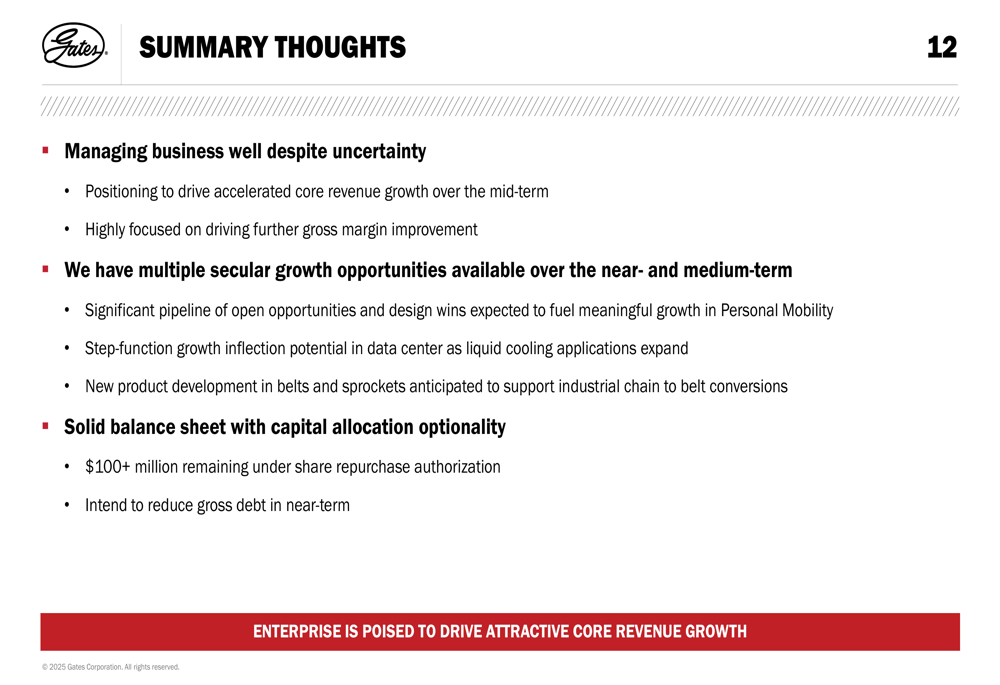

With a cash balance exceeding $700 million and improving leverage metrics, Gates highlighted its "capital allocation optionality." The company noted it has over $100 million remaining under its share repurchase authorization and intends to reduce gross debt in the near term.

In its summary, Gates Industrial emphasized that it is "managing business well despite uncertainty" and is "positioned to drive accelerated core revenue growth over the mid-term." The company remains focused on further gross margin improvement while pursuing multiple secular growth opportunities in personal mobility, data centers, and industrial chain-to-belt conversions.

The stock closed at $24.76 on July 29, 2025, representing significant appreciation from the $17.98 closing price following its Q1 2025 results. This upward trajectory reflects growing investor confidence in the company’s strategic direction and operational execution despite challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.