Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

GeneDx Holdings Corp (NASDAQ:WGS) reported strong second-quarter 2025 results on July 29, marking a significant turnaround from its disappointing first-quarter performance. The genetic testing company’s shares surged 25.27% in premarket trading to $106.37, recovering substantial ground after falling 34.78% following its Q1 earnings miss.

The company’s presentation revealed robust revenue growth, continued margin expansion, and a significant upward revision to its full-year guidance. This performance comes as GeneDx continues to strengthen its position in the genetic testing market, particularly in exome and genome sequencing for rare disease diagnosis.

Quarterly Performance Highlights

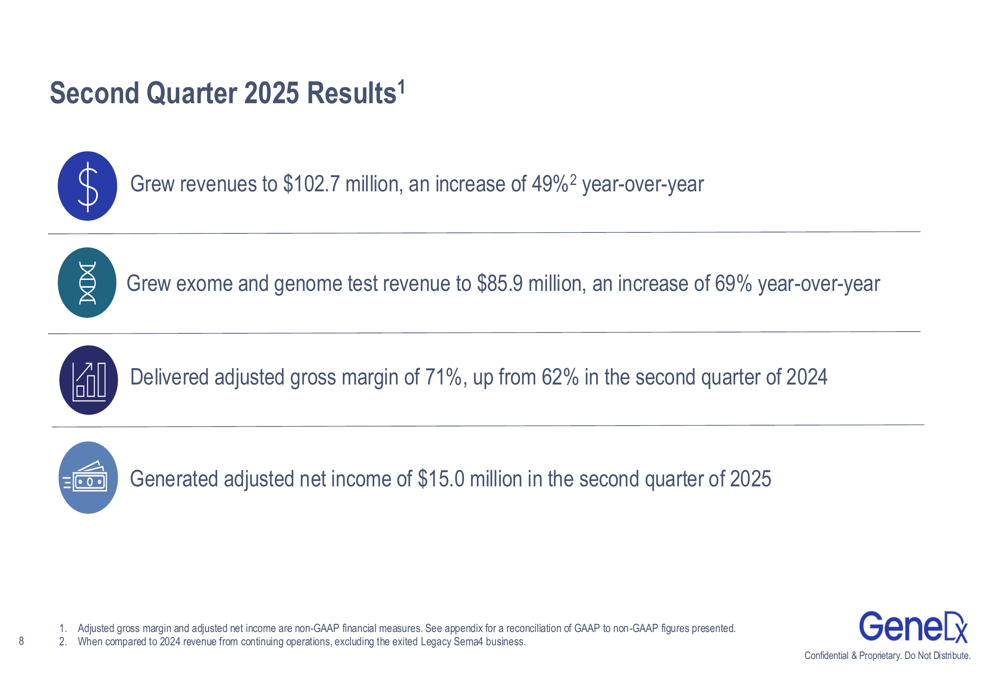

GeneDx reported second-quarter revenue of $102.7 million, representing a 49% year-over-year increase. Notably, exome and genome test revenue grew even faster at 69% year-over-year, reaching $85.9 million.

As shown in the following financial highlights slide, the company delivered an adjusted gross margin of 71%, up from 62% in the second quarter of 2024, while generating adjusted net income of $15.0 million:

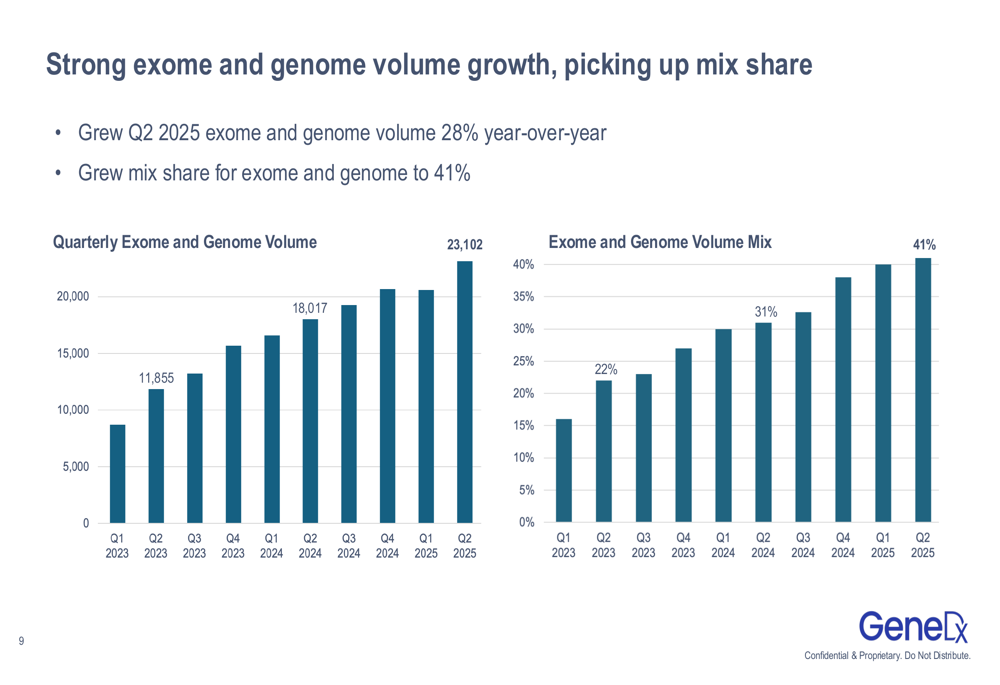

The company’s exome and genome testing volume grew 28% year-over-year in Q2 2025, with these high-value tests now representing 41% of GeneDx’s testing mix, up from lower percentages in previous quarters. This shift toward higher-margin genomic testing has been a key driver of the company’s improving financial performance.

The following chart illustrates the consistent growth in exome and genome testing volume over the past two years:

Profitability Milestone (WA:MMD)

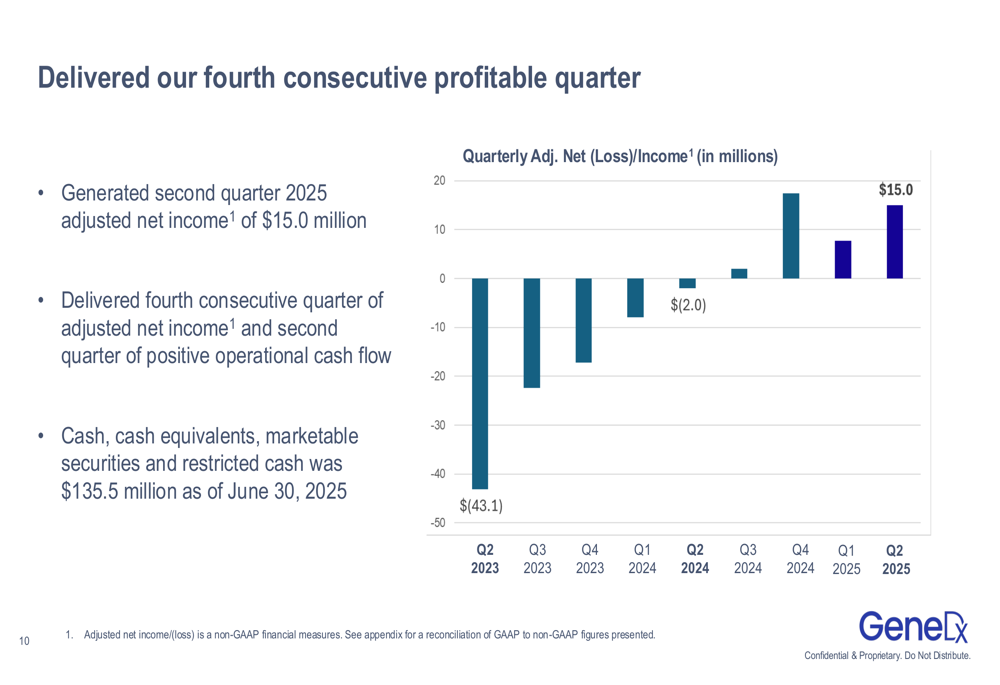

GeneDx achieved its fourth consecutive quarter of positive adjusted net income, marking a substantial improvement from the $43.1 million loss reported in Q2 2023. The company also reported its second quarter of positive operational cash flow, with cash, cash equivalents, marketable securities, and restricted cash totaling $135.5 million as of June 30, 2025.

The following chart demonstrates the company’s impressive journey to profitability:

This sustained profitability represents a significant achievement for GeneDx, especially considering the company’s Q1 2025 earnings per share miss that triggered a sharp stock decline. The Q2 results suggest the company has successfully addressed the operational challenges that affected its first-quarter performance.

Competitive Industry Position

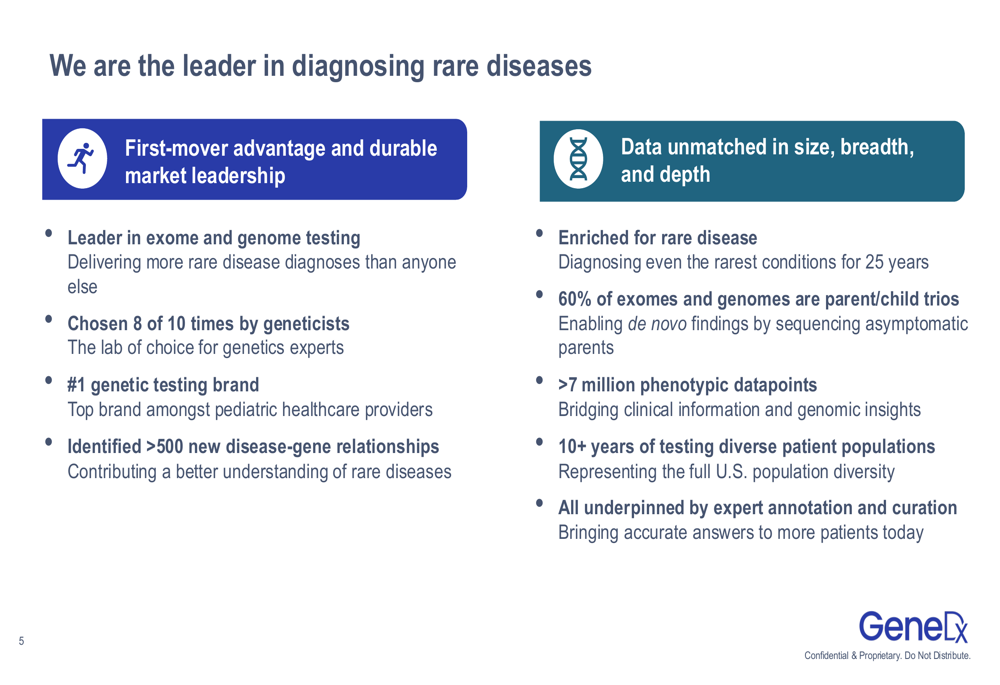

GeneDx emphasized its leadership position in diagnosing rare diseases, highlighting several competitive advantages in its presentation. The company claims to be the #1 genetic testing brand and a first-mover with durable market leadership in rare disease diagnosis.

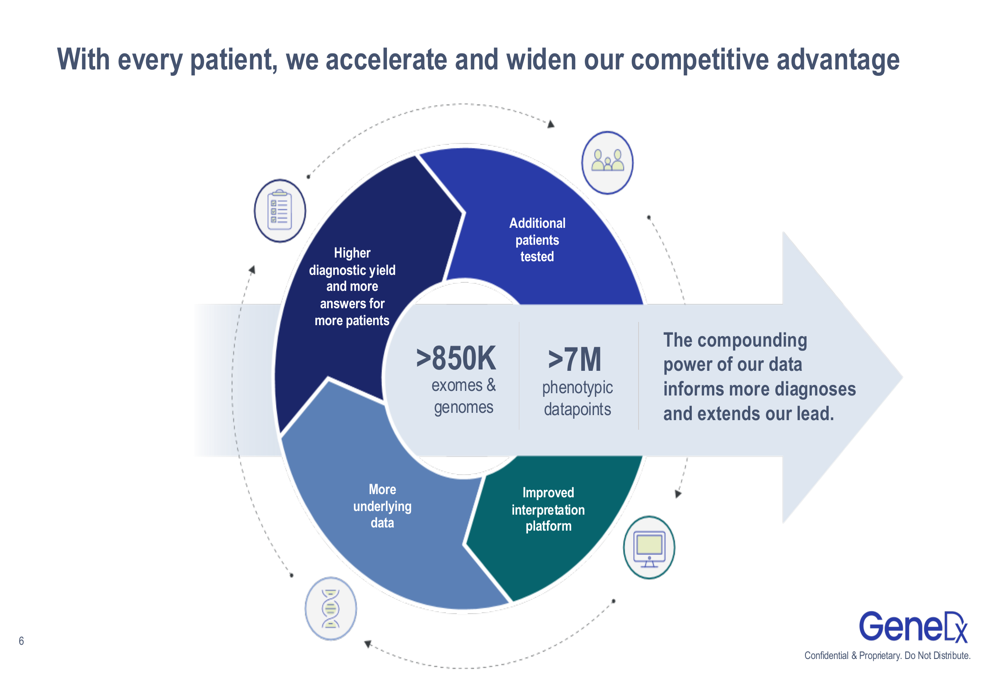

The company’s competitive advantage is built on its extensive database, which includes over 850,000 exomes and genomes and more than 7 million phenotypic datapoints. GeneDx has identified over 500 new disease-gene relationships and maintains that 60% of its exomes and genomes are parent/child trios, which provide more comprehensive genetic information.

As illustrated in the following slide, the company’s leadership position in rare disease diagnosis is supported by multiple factors:

GeneDx’s presentation also highlighted how its data creates a self-reinforcing competitive advantage, with each additional patient tested improving the company’s diagnostic capabilities:

Market Opportunity (SO:FTCE11B)

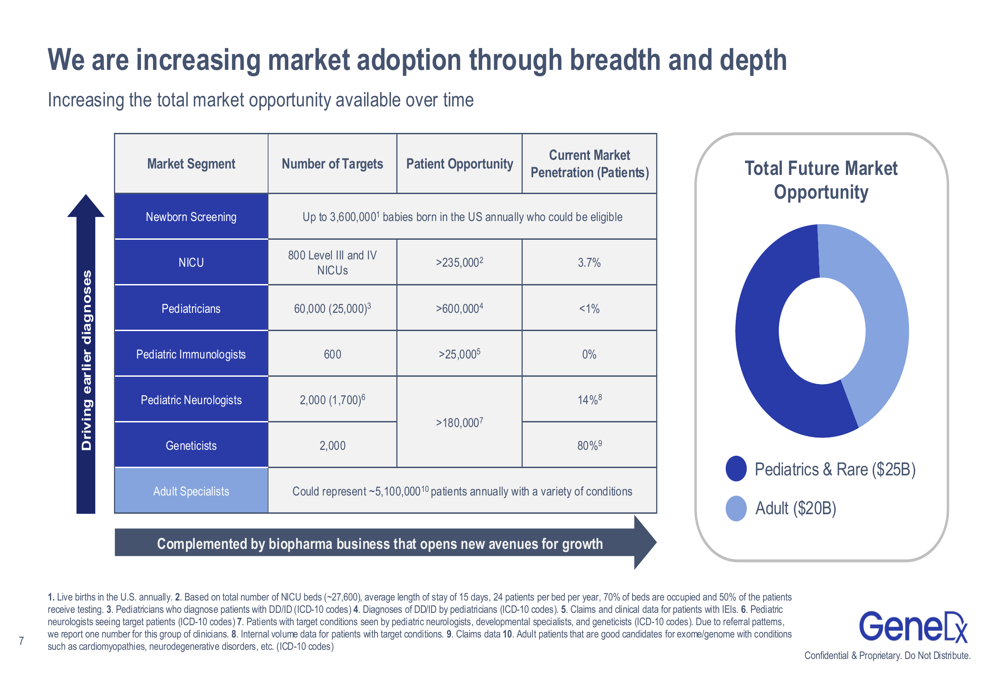

The company identified significant untapped market potential across various segments, particularly in pediatric care settings. While GeneDx has achieved approximately 80% market penetration among geneticists, its penetration in other segments remains much lower, with pediatric neurologists at 14% and pediatricians below 1%.

The following slide details the company’s current market penetration and future opportunities:

GeneDx estimates its total future market opportunity at approximately $45 billion, split between pediatrics and rare diseases ($25 billion) and adult applications ($20 billion). The company’s presentation emphasized the potential to significantly reduce the diagnostic journey for patients with genetic disorders, which currently takes an average of 16 tests and 5 years before an accurate diagnosis.

Forward-Looking Statements

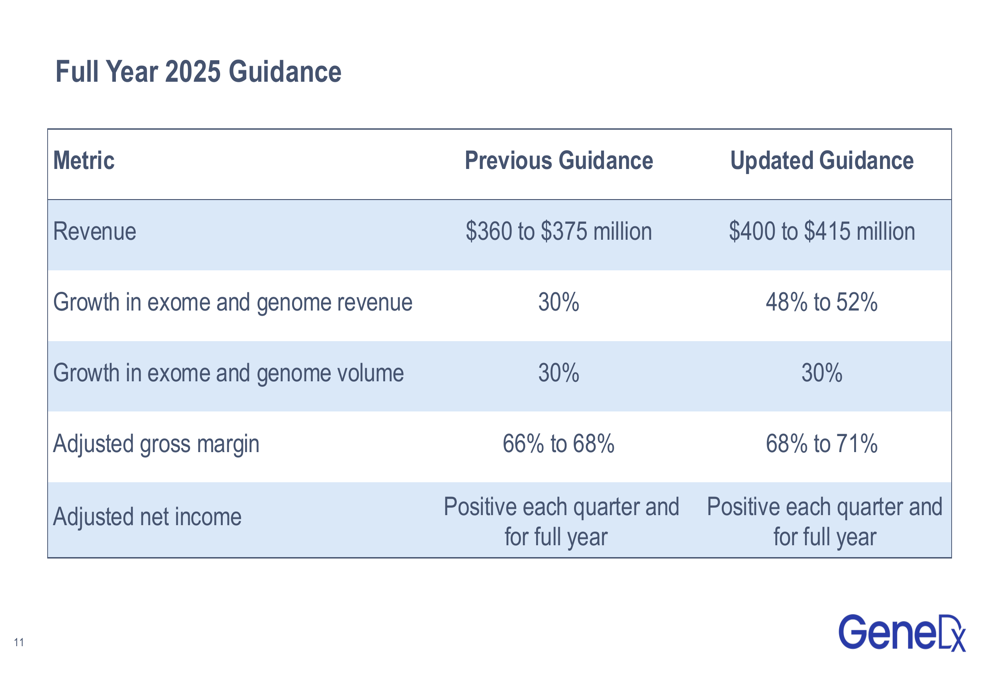

Following its strong second-quarter performance, GeneDx significantly raised its full-year 2025 guidance. The company now expects revenue between $400 million and $415 million, up from its previous guidance of $360 million to $375 million.

The updated guidance also projects exome and genome revenue growth of 48% to 52%, a substantial increase from the previous projection of 30%. The company maintained its forecast of 30% growth in exome and genome volume while raising its adjusted gross margin guidance to 68% to 71%, up from 66% to 68%.

The following table details the company’s updated guidance:

This upward revision reflects management’s confidence in continued strong performance through the remainder of 2025, despite the challenges faced in the first quarter.

Executive Summary

GeneDx’s Q2 2025 results demonstrate a company gaining momentum in the genetic testing market, with strong revenue growth, expanding margins, and sustained profitability. The significant upward revision to full-year guidance suggests management expects this positive trajectory to continue.

The company’s focus on expanding its market penetration beyond geneticists into other medical specialties presents substantial growth opportunities. Meanwhile, its extensive database of genetic and phenotypic information provides a competitive advantage that strengthens with each additional patient tested.

The market’s positive reaction to these results, with shares up over 25% in premarket trading, indicates investors are reassured after the disappointing Q1 performance. As GeneDx continues to execute on its strategy of expanding access to genetic testing while improving operational efficiency, it appears well-positioned to maintain its leadership in the growing market for genomic diagnostics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.