Stock market today: S&P 500 falls as government shutdown, trade jitters persist

Introduction & Market Context

Genuine Parts Company (NYSE:GPC) released its second quarter 2025 earnings presentation on July 22, 2025, revealing mixed results and a downward revision to its full-year guidance. The Atlanta-based automotive and industrial parts distributor reported sales growth but faced profitability challenges across its business segments.

The company’s stock was trading down 2.33% in premarket at $121.00, reflecting investor concerns about the lowered outlook and margin pressures. This follows a previous close of $123.89, which had represented a 0.8% gain in the prior session.

Quarterly Performance Highlights

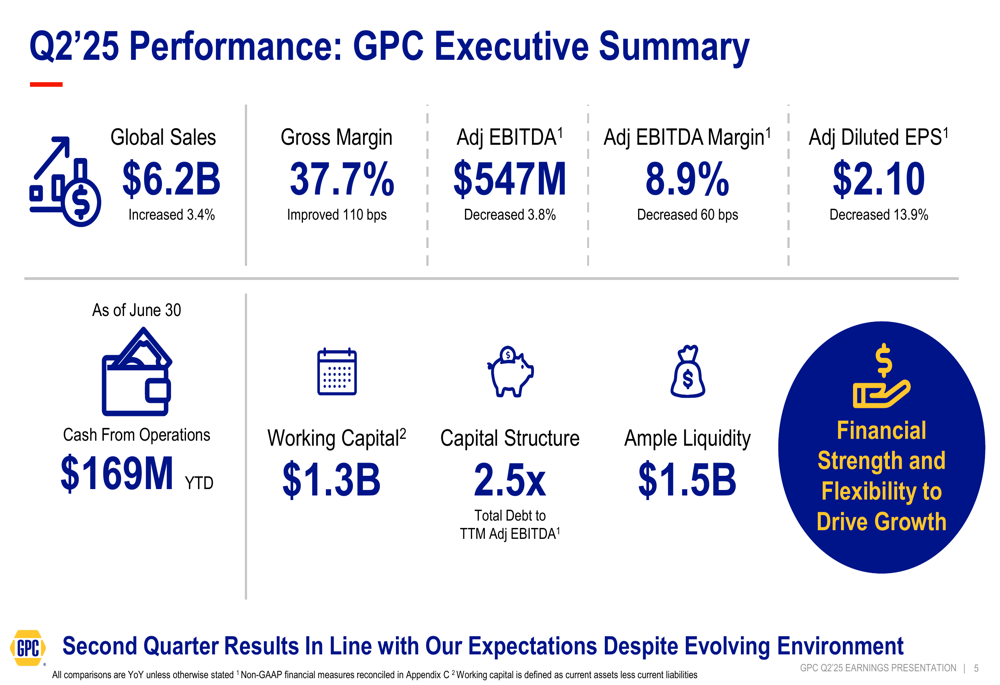

GPC reported global sales of $6.2 billion for Q2 2025, representing a 3.4% increase compared to the same period last year. While the company achieved gross margin improvement of 110 basis points to 37.7%, its profitability metrics showed signs of pressure.

Adjusted EBITDA declined 3.8% to $547 million, with adjusted EBITDA margin contracting 60 basis points to 8.9%. More concerning for investors, adjusted diluted earnings per share fell 13.9% to $2.10, reflecting the challenging operating environment.

As shown in the following comprehensive performance summary:

The company’s year-to-date cash from operations stood at $169 million, with working capital of $1.3 billion. GPC maintains a solid capital structure with a total debt to TTM adjusted EBITDA ratio of 2.5x and ample liquidity of $1.5 billion.

Segment Analysis

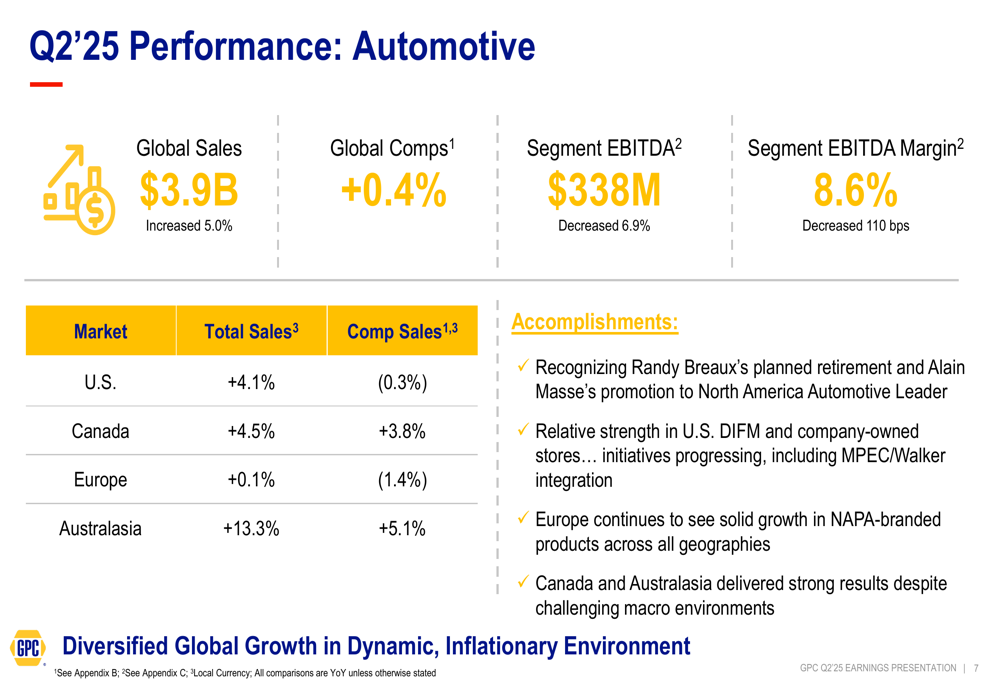

GPC’s performance varied significantly between its two main business segments. The Automotive segment, which accounts for approximately 63% of total revenue, reported global sales of $3.9 billion, an increase of 5.0%. However, comparable sales growth was modest at just 0.4%. More concerning was the 6.9% decrease in segment EBITDA to $338 million, with margin compression of 110 basis points to 8.6%.

The following slide details the Automotive segment’s performance across regions:

Regional performance within Automotive showed considerable variation, with Australasia leading at 13.3% growth and 5.1% comparable sales, while Europe struggled with just 0.1% growth and negative 1.4% comparable sales. The U.S. market showed 4.1% growth but negative comparable sales of 0.3%.

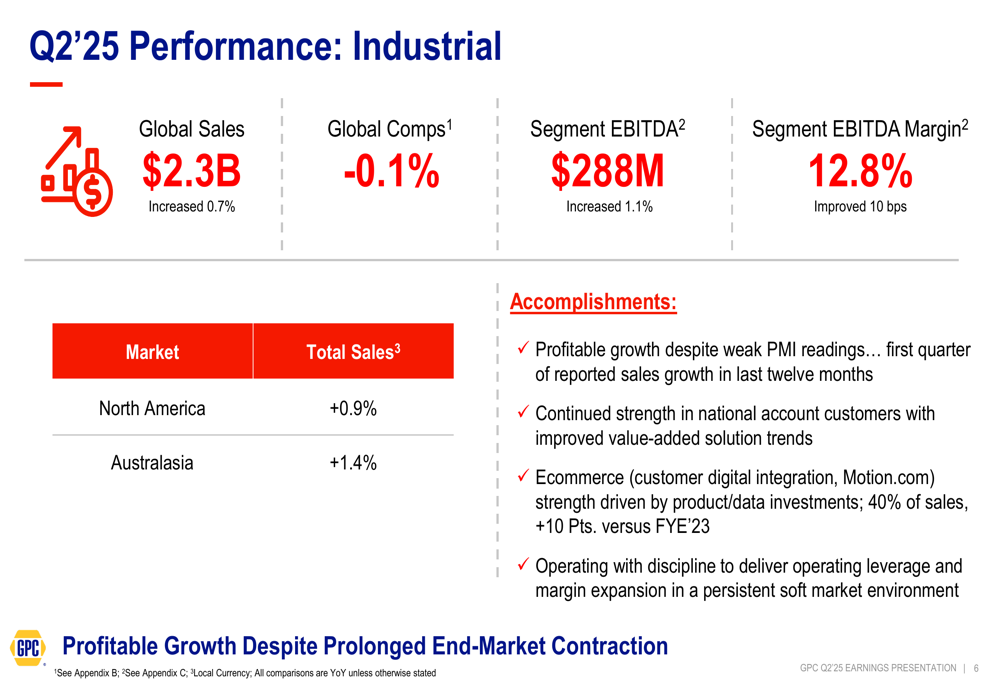

In contrast, the Industrial segment delivered more stable profitability despite slower sales growth. Global sales for Industrial reached $2.3 billion, up just 0.7%, with comparable sales slightly negative at -0.1%. However, segment EBITDA increased 1.1% to $288 million, with a slight margin improvement of 10 basis points to 12.8%.

The Industrial segment’s performance is illustrated in the following slide:

Management highlighted the segment’s ability to maintain profitable growth despite weak PMI readings, noting continued strength in national account customers and e-commerce initiatives.

Revised Outlook and Guidance

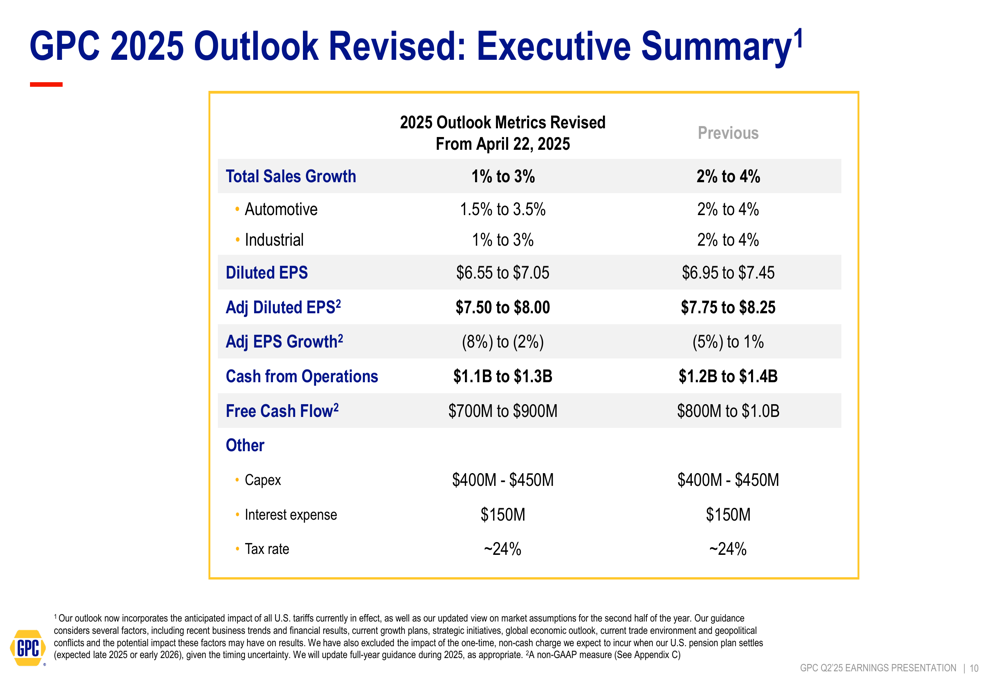

In a significant development, GPC revised its full-year 2025 guidance downward across all key metrics. The company now expects total sales growth of 1% to 3%, down from the previous guidance of 2% to 4%. Both the Automotive and Industrial segments saw similar downward revisions.

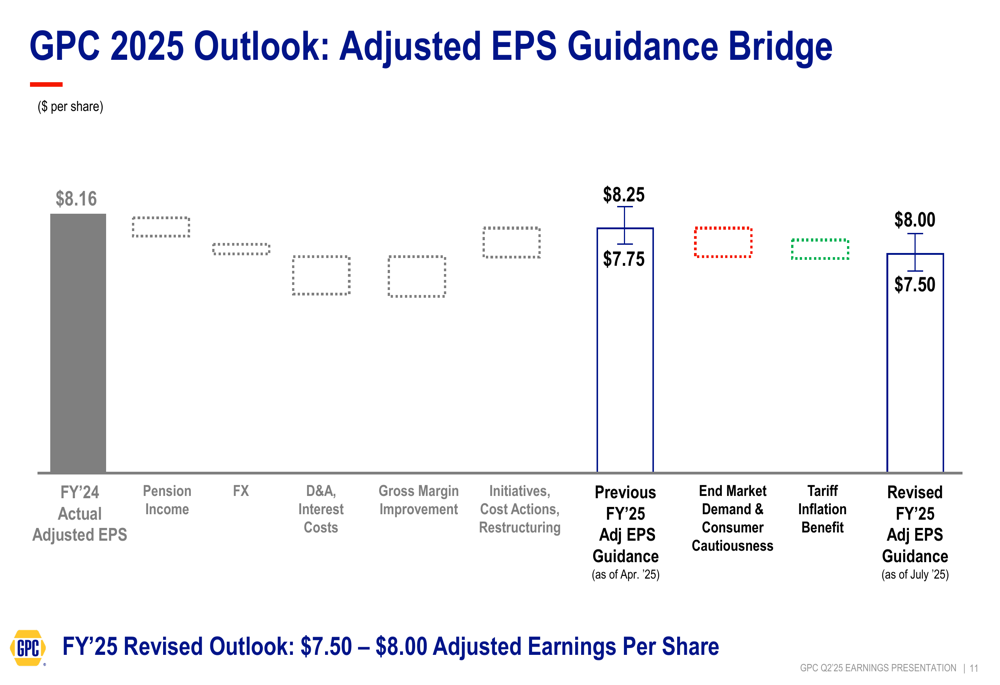

The adjusted diluted EPS outlook was reduced to a range of $7.50 to $8.00, compared to the previous guidance of $7.75 to $8.25. This represents an expected year-over-year decline of 2% to 8%, compared to the previous expectation of -5% to +1% growth.

The revised guidance is detailed in the following comprehensive outlook summary:

To provide further context for the guidance revision, GPC presented an adjusted EPS bridge that illustrates the various factors impacting its earnings outlook:

The bridge highlights how pension income, foreign exchange impacts, depreciation and amortization, gross margin improvement, and end market challenges are collectively affecting the company’s earnings trajectory.

Strategic Initiatives and Capital Allocation

Despite the challenging environment, GPC continues to execute on its strategic initiatives. The company outlined its investment priorities, including talent development, sales effectiveness, supply chain modernization, emerging technology leadership, data and digital capabilities enhancement, and strategic acquisitions.

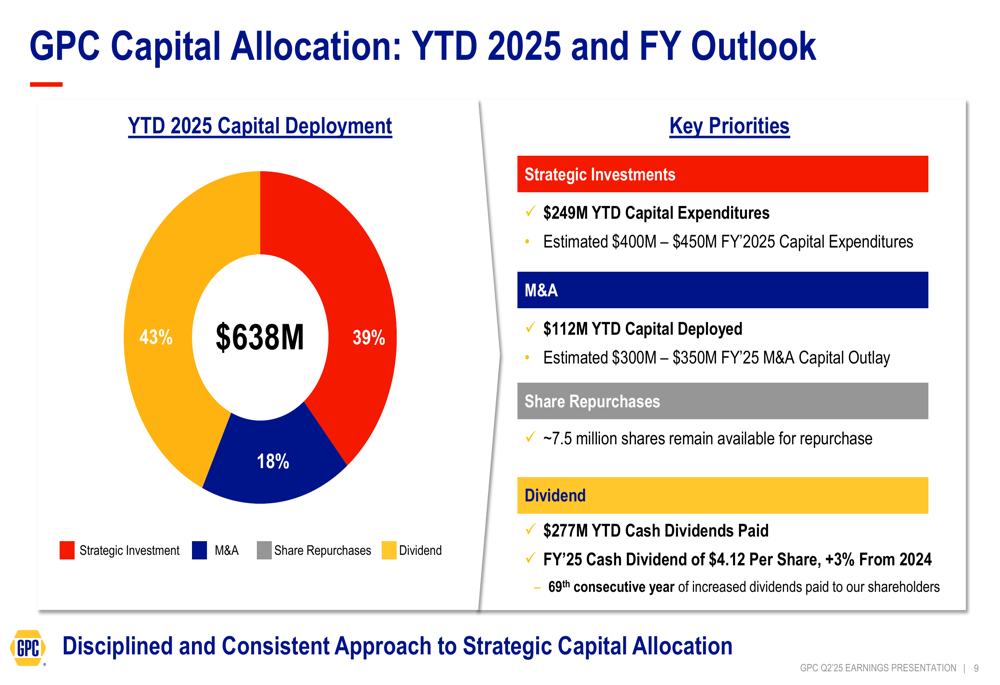

GPC’s capital allocation strategy remains balanced, with year-to-date capital deployment of $638 million distributed across strategic investments (43%), M&A (18%), and share repurchases (39%). The company has paid $277 million in dividends year-to-date and has announced a full-year 2025 cash dividend of $4.12 per share, representing a 3% increase from 2024.

The following slide illustrates GPC’s capital allocation strategy:

Market Reaction and Analysis

The premarket decline in GPC’s stock price suggests investors are concerned about the company’s ability to navigate the current challenging environment. The reduction in full-year guidance, particularly the expected decline in adjusted EPS, appears to be weighing on investor sentiment.

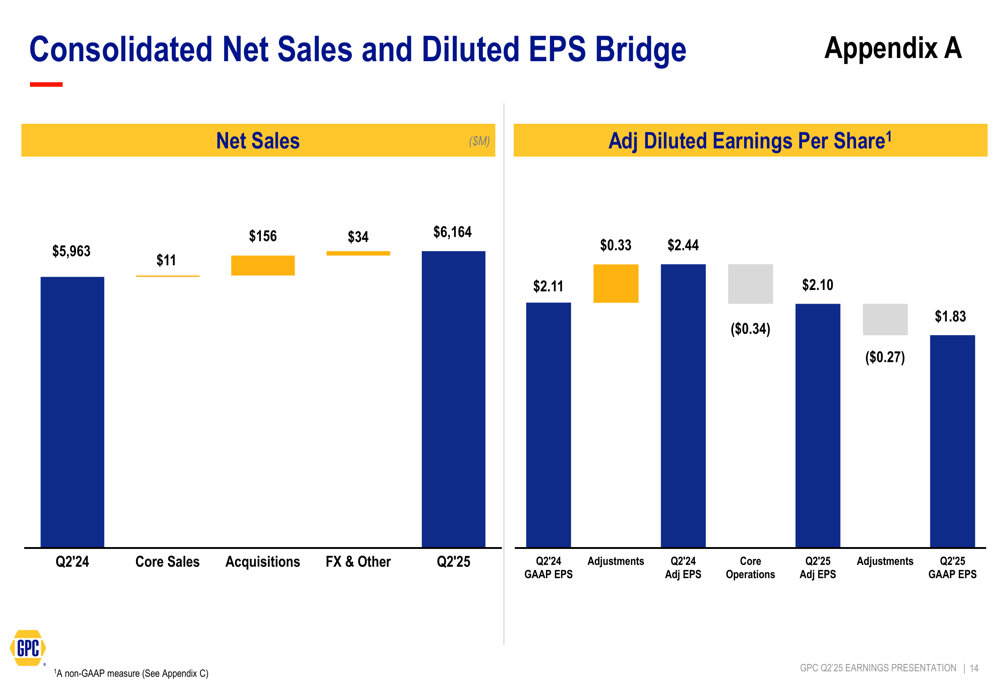

A detailed bridge analysis of the company’s consolidated net sales and diluted EPS provides further insight into the factors driving GPC’s performance:

The bridge shows that while acquisitions contributed $156 million to net sales growth, core sales added just $11 million, highlighting the challenging organic growth environment. The adjusted diluted EPS declined from $2.11 in Q2 2024 to $1.83 in Q2 2025, with core business performance accounting for a $0.34 reduction.

In its presentation, GPC acknowledged the challenges it faces but emphasized its focus on "controlling what can be controlled while proactively managing the external environment." The company’s ability to improve gross margins amid sales pressure demonstrates some success in this approach, but the overall profitability decline suggests continued headwinds.

For investors, GPC’s consistent dividend growth (now at 3% year-over-year) and ongoing share repurchases provide some positive signals amid the operational challenges. However, the revised outlook and margin pressures indicate that the company may face a more difficult path through the remainder of 2025 than previously anticipated.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.