Fidelity Wise Origin Bitcoin Fund amends trust agreement to allow in-kind share transactions

Genworth Financial, Inc. (NYSE:GNW) released its first-quarter 2025 investor presentation on May 1, highlighting net income of $54 million, or $0.13 per diluted share, and adjusted operating income of $51 million, or $0.12 per diluted share. The company’s mortgage insurance subsidiary, Enact, continued to be the primary profit driver, while the long-term care and life insurance segments faced ongoing challenges.

Quarterly Performance Highlights

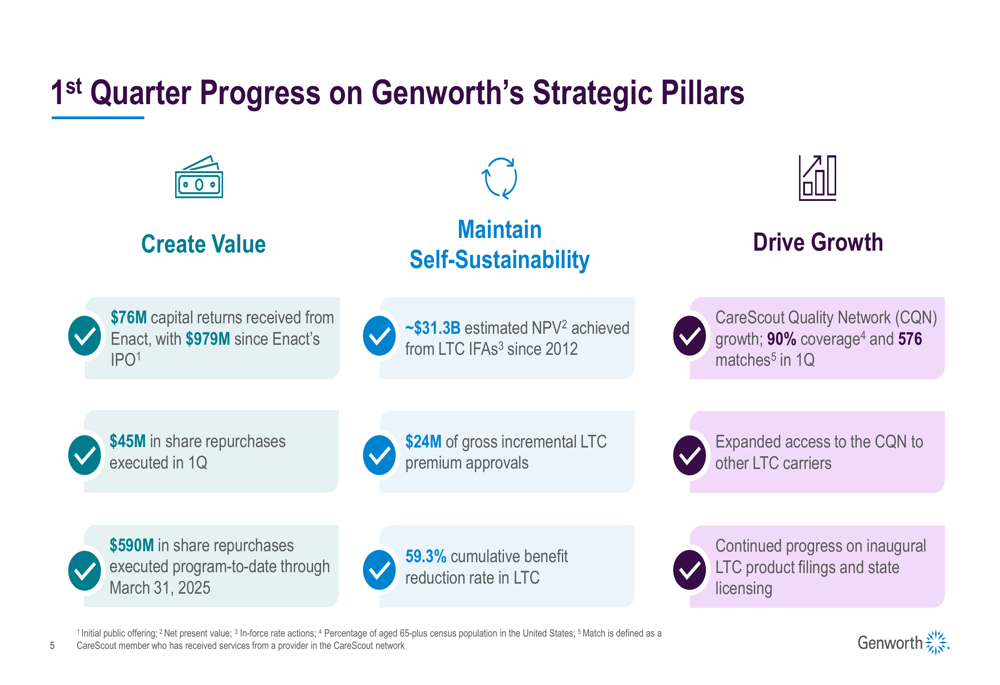

Genworth’s financial results for the first quarter of 2025 reflected the company’s continued focus on its three strategic pillars: creating shareholder value, maintaining self-sustainability of legacy businesses, and driving growth through new initiatives.

As shown in the following financial performance summary:

The company reported that Enact delivered $137 million in adjusted operating income and distributed $76 million in capital returns to Genworth during the quarter. The U.S. life insurance companies maintained an RBC ratio of 304%, reflecting higher required capital, while the holding company ended the quarter with $211 million in cash and liquid assets.

Segment Performance Analysis

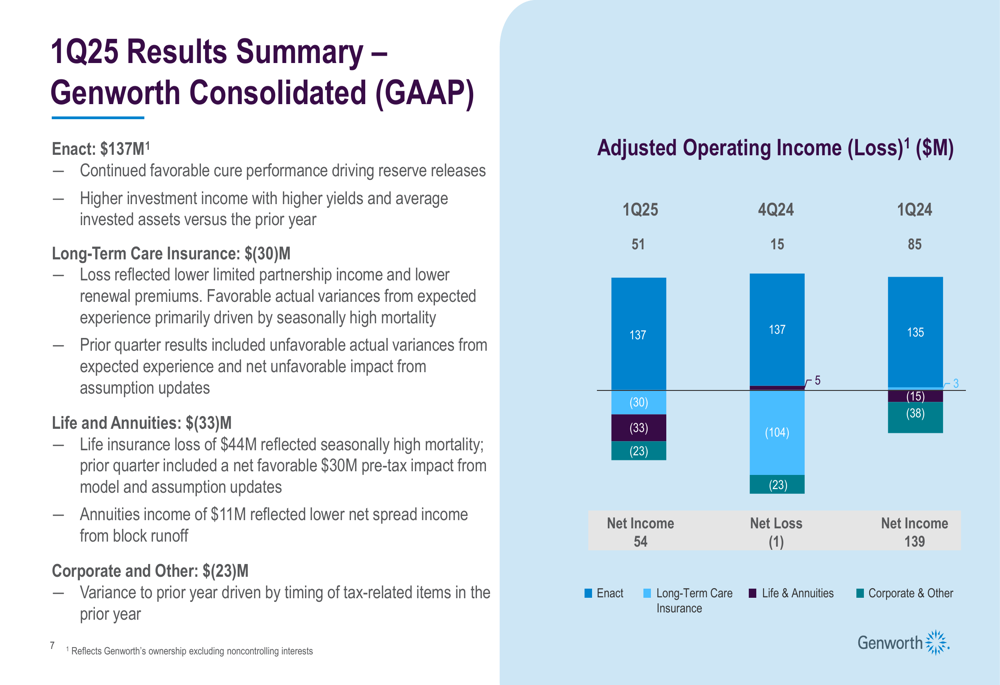

Genworth’s consolidated results revealed significant variations across business segments, with Enact continuing to outperform while other segments faced challenges.

The following chart illustrates the adjusted operating income (loss) by segment:

Enact’s strong performance was driven by favorable cure performance and higher investment income. However, the Long-Term Care Insurance segment reported a loss of $30 million, reflecting lower limited partnership income and renewal premiums. The Life and Annuities segment posted a $33 million loss, with life insurance losses of $44 million partially offset by annuities income of $11 million. The Corporate and Other segment recorded a $23 million loss, with the variance primarily driven by tax-related items.

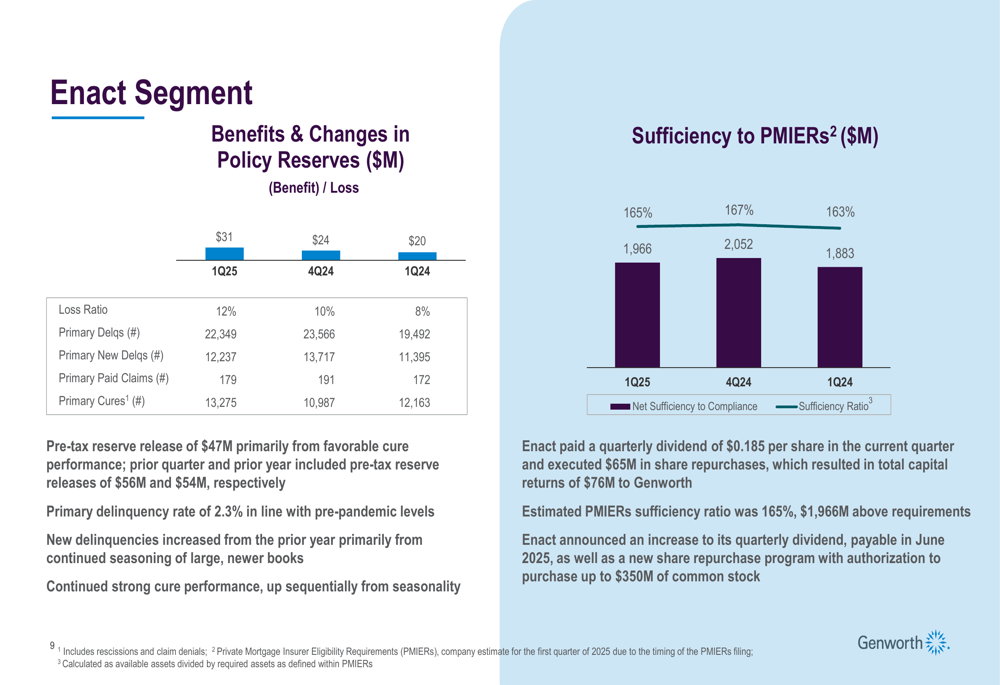

Enact’s Primary Insurance In Force (IIF) remained stable at $268 billion, while earned premiums were higher compared to the prior year, supported by higher assumed premiums and IIF growth, partially offset by higher ceded premiums.

The mortgage insurance business demonstrated strong capital metrics, as shown in the following chart:

Enact maintained a robust PMIERS sufficiency ratio of 165%, representing $1.966 billion above requirements. The business also benefited from a pre-tax reserve release of $47 million resulting from favorable cure performance, while the primary delinquency rate of 2.3% remained in line with pre-pandemic levels.

Strategic Initiatives and Growth Focus

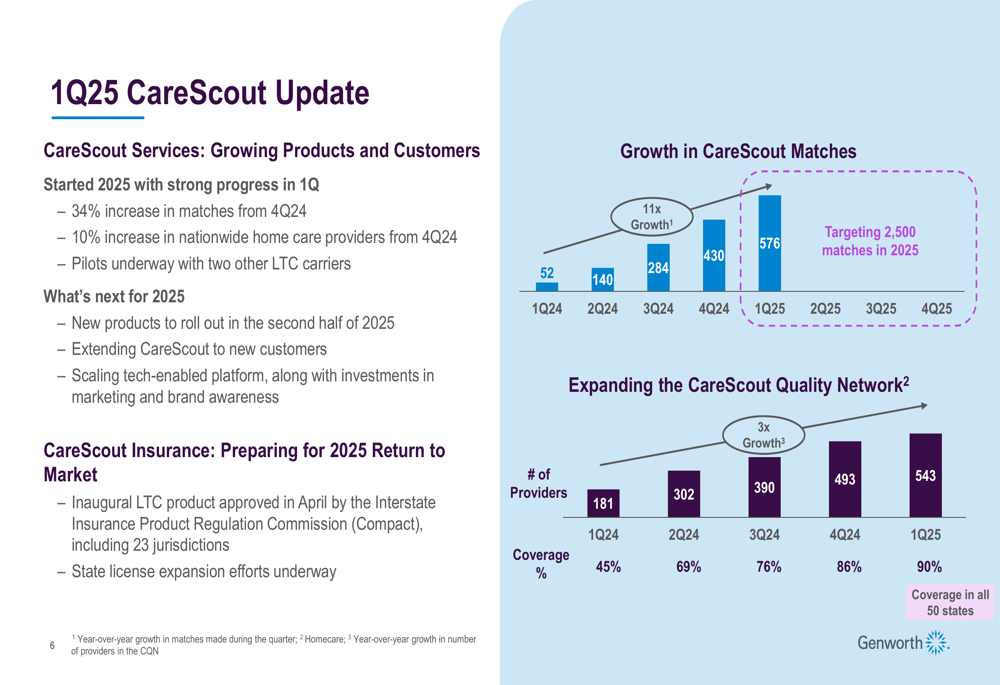

Genworth continued to make progress on its strategic pillars during the first quarter, with particular emphasis on growing its CareScout business while managing its legacy long-term care portfolio.

The following slide highlights the company’s progress across its strategic initiatives:

CareScout, positioned as Genworth’s growth engine, showed significant momentum in the first quarter of 2025:

CareScout matches increased 34% from the fourth quarter of 2024, reaching 576 matches in Q1 2025. The CareScout Quality Network expanded by 10%, achieving 90% coverage across all 50 states. The company also highlighted plans for 2025, including new product launches, customer expansion, and platform scaling. Notably, Genworth received approval for its inaugural LTC product from the Interstate Insurance Product Regulation Commission in April, marking a significant step toward reentering the LTC funding market.

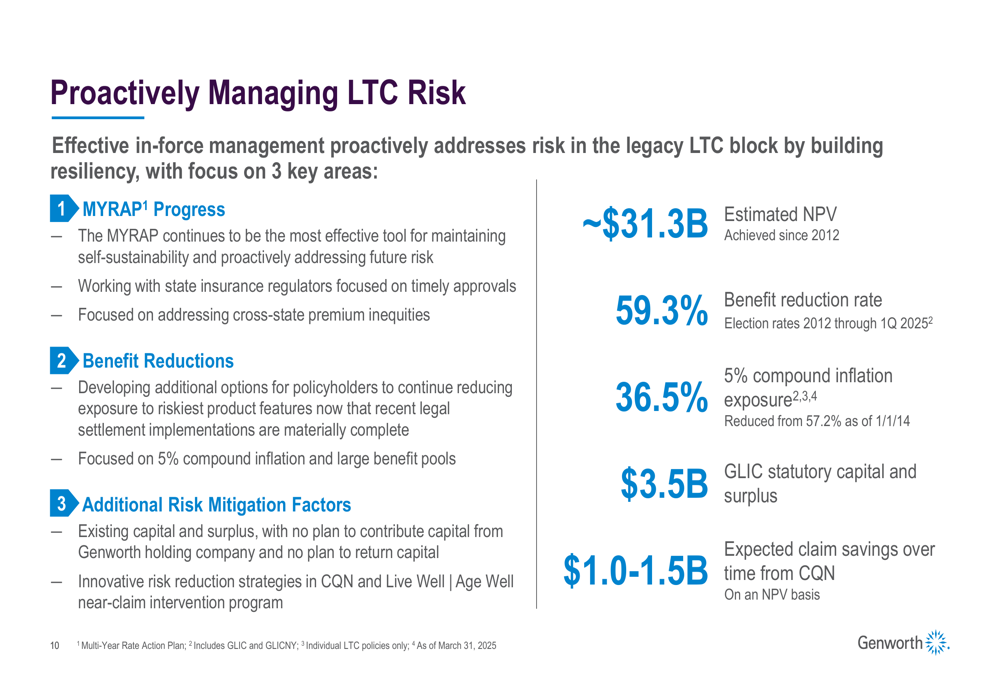

In the legacy long-term care business, Genworth continued its proactive risk management approach:

The company has achieved an estimated $31.3 billion in net present value since 2012 through its Multi-Year Rate Action (WA:ACT) Plan (MYRAP). The benefit reduction rate reached 59.3%, helping to mitigate the risk exposure in the LTC portfolio. Additionally, the company highlighted that only 36.5% of its LTC business carries 5% compound inflation exposure, further reducing risk.

Capital Position and Shareholder Returns

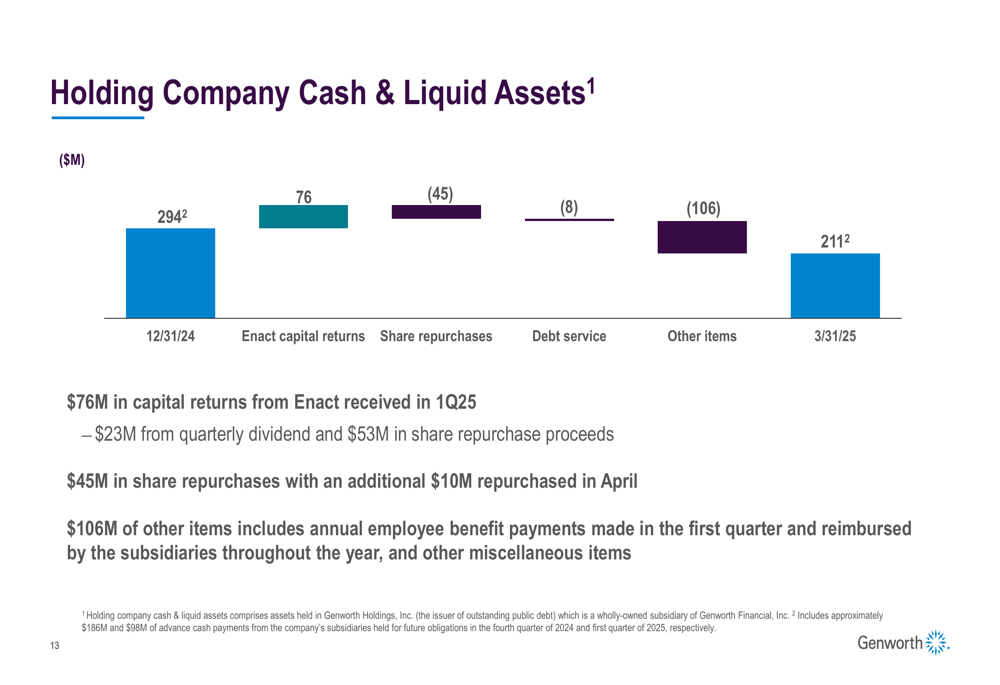

Genworth’s holding company cash and liquid assets decreased during the quarter, as illustrated in the following chart:

The holding company’s cash position declined from $294 million at the end of 2024 to $211 million as of March 31, 2025. This reduction was primarily due to $45 million in share repurchases, $8 million in debt service, and $106 million in other items, partially offset by $76 million in capital returns from Enact. The company noted that it repurchased an additional $10 million in shares during April 2025.

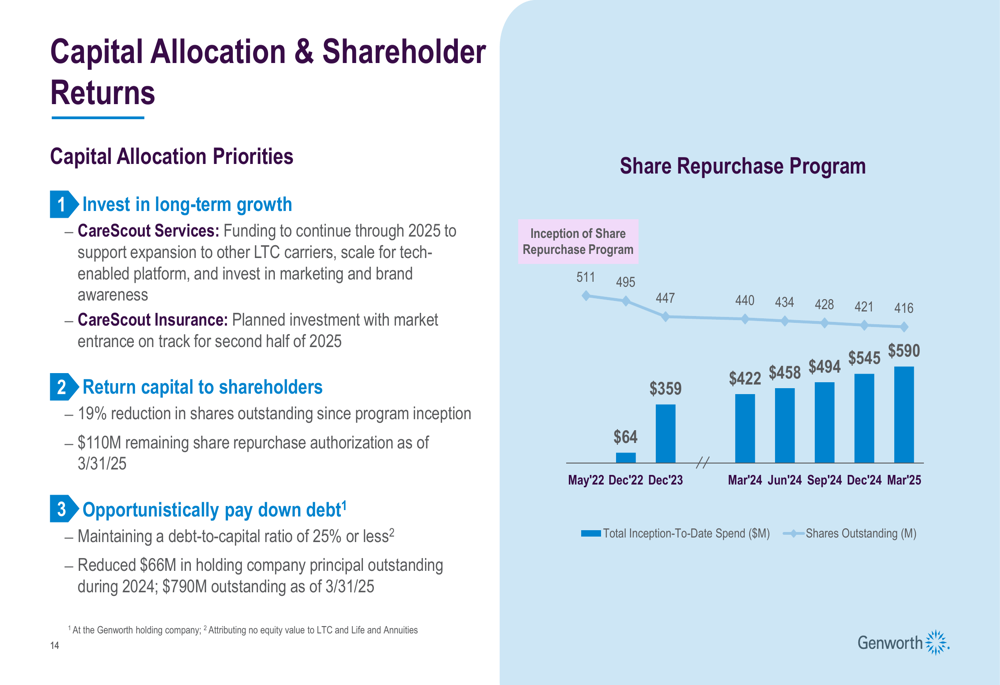

Genworth’s capital allocation strategy continues to balance investments in long-term growth with shareholder returns and debt reduction:

Since the inception of its share repurchase program, Genworth has spent a total of $590 million on share repurchases, demonstrating its commitment to returning capital to shareholders while also investing in CareScout’s growth and maintaining a prudent debt management approach.

Forward-Looking Statements

Looking ahead, Genworth remains focused on executing its three-pillar strategy: creating value through Enact, maintaining self-sustainability of its legacy insurance businesses, and driving growth through CareScout. The company continues to work toward reentering the long-term care insurance market with new products, while expanding the CareScout network to provide innovative aging care services and funding solutions.

The company’s investment portfolio of $60.6 billion, with 75% in fixed maturities, showed improvement with unrealized losses decreasing to $3.2 billion in Q1 2025 from $3.8 billion in Q4 2024. Approximately 97% of total fixed maturities are rated BBB or higher, reflecting the company’s conservative investment approach.

While Enact continues to be the primary profit driver, Genworth’s strategic focus on expanding CareScout and managing its legacy LTC business positions the company to address the growing needs of an aging population while working to deliver long-term shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.