Gold prices slip as stronger dollar, Fed rate uncertainty weigh

Introduction & Market Context

Gibraltar Industries (NASDAQ:ROCK) held its third quarter 2025 earnings call on October 30, presenting financial results that showed revenue growth despite challenging market conditions. The company’s stock showed resilience in the face of earnings that missed analyst expectations, trading up 0.94% to $67.76 following the presentation, after rising 1.83% in pre-market trading.

The building products manufacturer operates across three segments – Residential, Agtech, and Infrastructure – with varying performance across each division. The company’s results reflect broader market dynamics, particularly in the residential roofing sector, which has experienced a 5-10% decline in the overall market.

Quarterly Performance Highlights

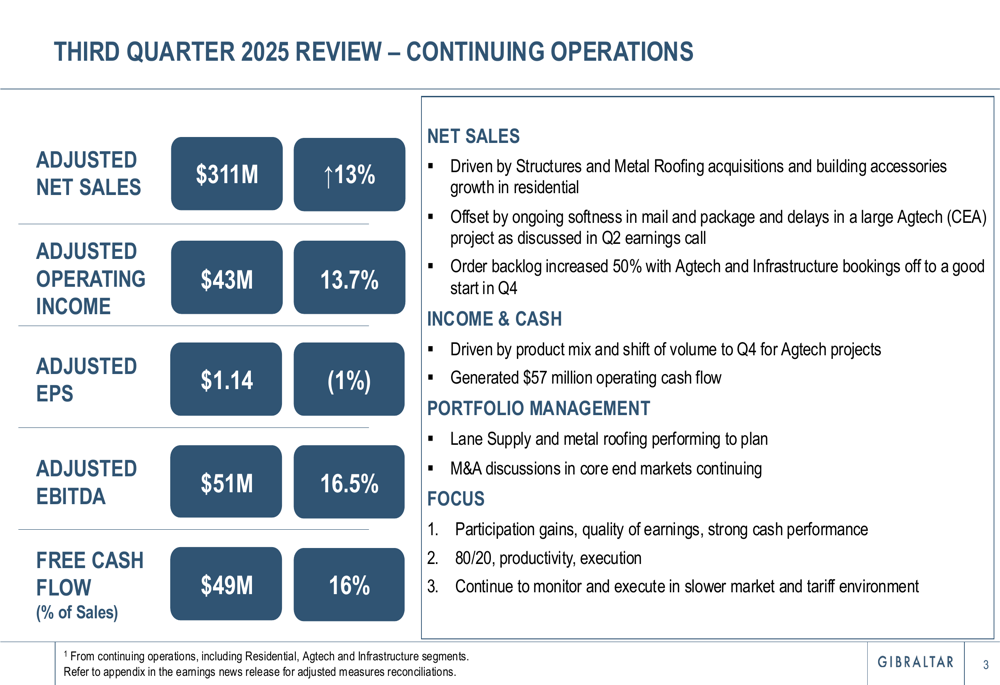

Gibraltar reported adjusted net sales of $311 million for Q3 2025, representing a 13% increase year-over-year. However, adjusted earnings per share came in at $1.14, down 1% compared to the same period last year and falling short of analyst expectations of $1.31.

Despite the earnings miss, the company demonstrated strong cash generation capabilities with $57 million in operating cash flow and $49 million in free cash flow, representing 16% of sales.

As shown in the following summary of Q3 2025 performance:

The company’s adjusted operating income reached $43 million with a 13.7% margin, while adjusted EBITDA totaled $51 million with a 16.5% margin. Key drivers of net sales growth included acquisitions in the Structures and Metal Roofing segments, along with residential building accessories growth, which was partially offset by softness in mail and package solutions and delays in Agtech projects.

Segment Analysis

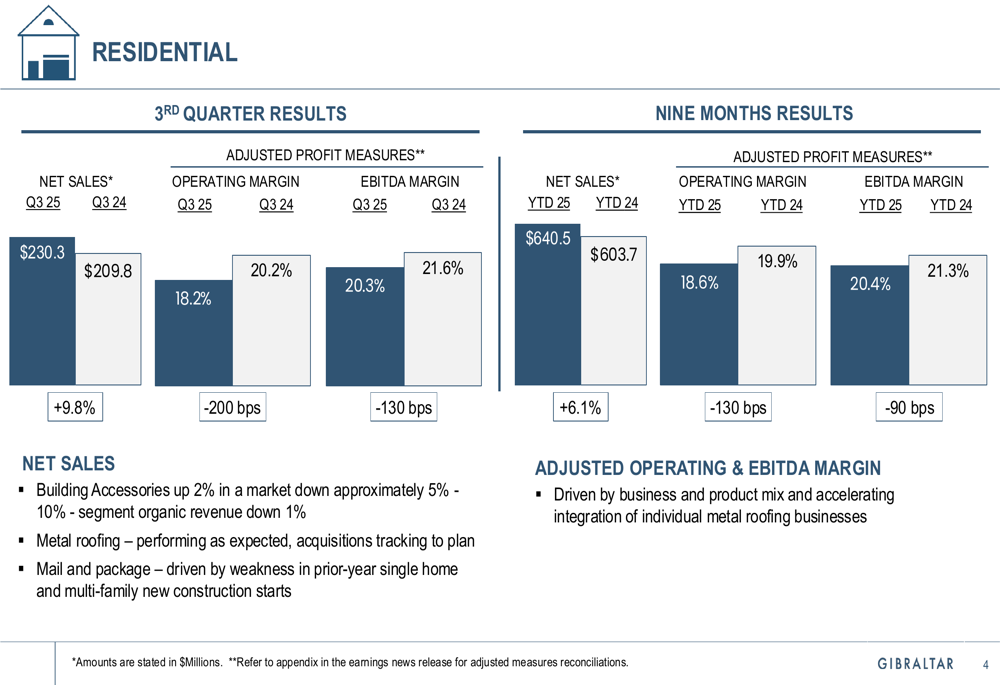

Residential Segment

Gibraltar’s Residential segment, the company’s largest division, posted net sales of $230.3 million in Q3 2025, compared to $209.8M in Q3 2024. Despite the sales increase, operating margins declined to 18.2% from 20.2% in the prior year period.

The following chart illustrates the segment’s performance:

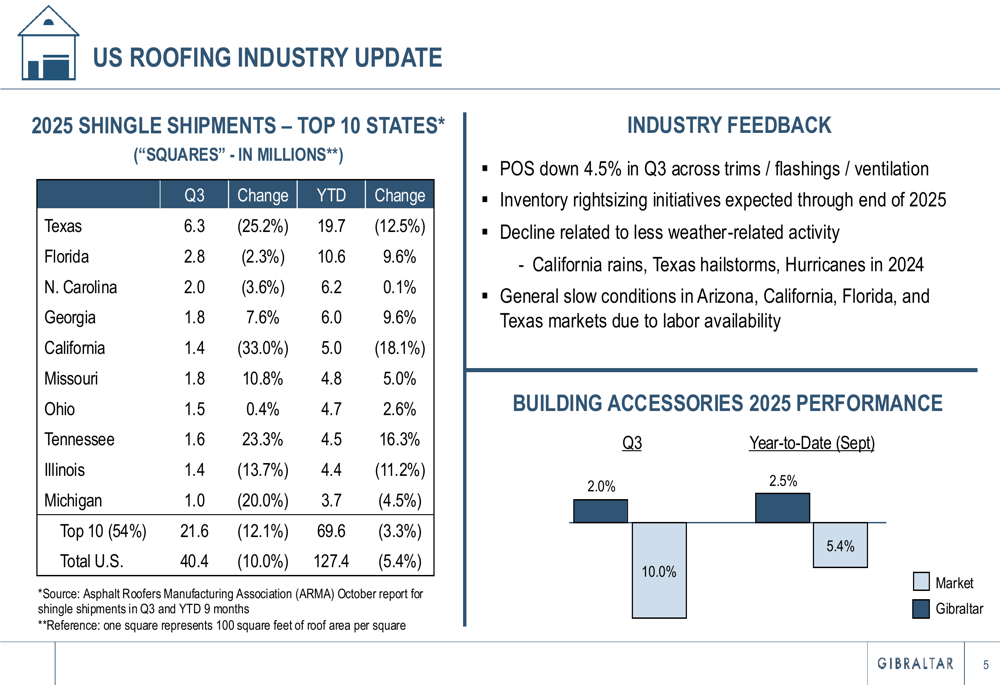

The residential building accessories business outperformed the broader market, growing 2% while the overall market declined 5-10%. This growth occurred despite significant challenges in the roofing industry, particularly in key states like Texas, which saw a 25.2% decline in shingle shipments during Q3.

The US roofing industry data presented by Gibraltar provides important context for the segment’s performance:

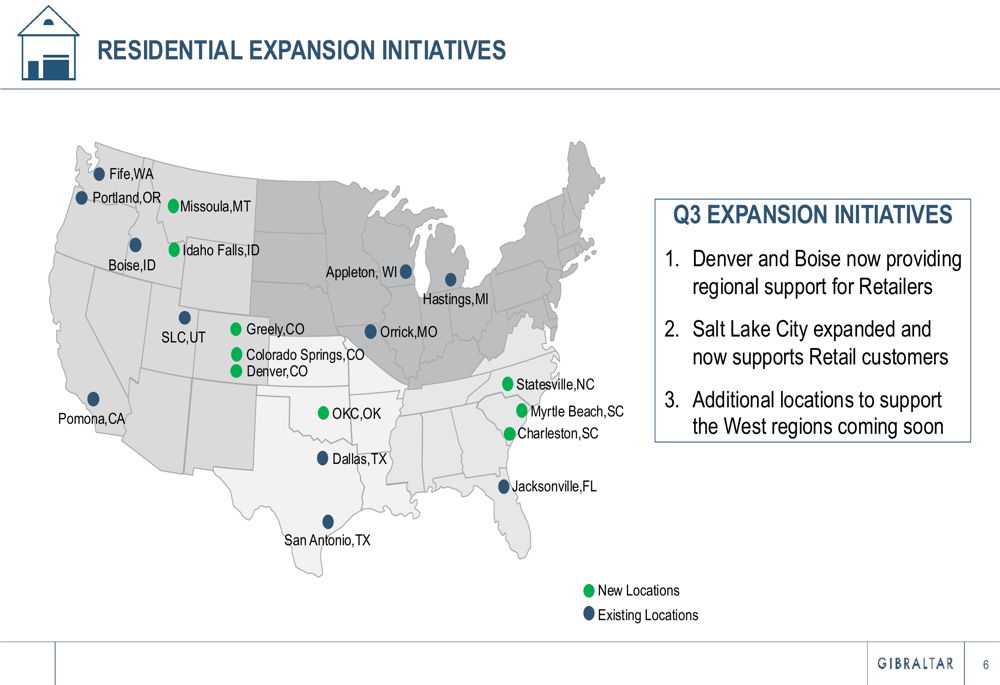

To strengthen its market position, Gibraltar is expanding its residential footprint with new facilities supporting retailers in Denver and Boise, while expanding operations in Salt Lake City:

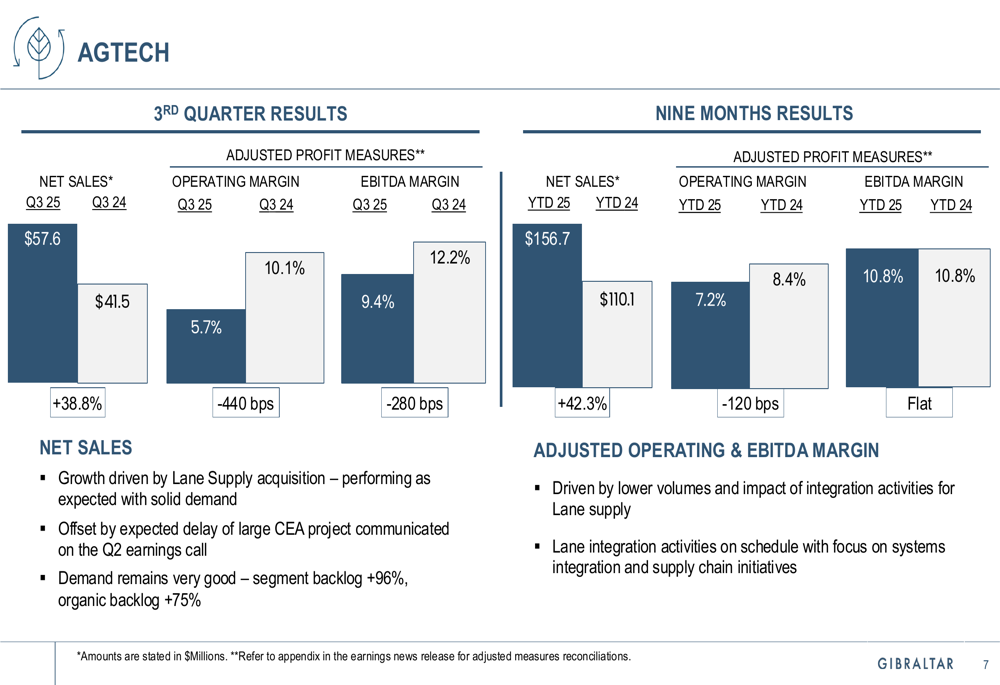

Agtech Segment

The Agtech segment showed substantial growth, with Q3 sales reaching $57.6 million compared to $41.5 million in Q3 2024, primarily driven by the Lane Supply acquisition. However, operating margins declined significantly to 5.7% from 10.1% in the prior year.

The segment’s performance is detailed in the following chart:

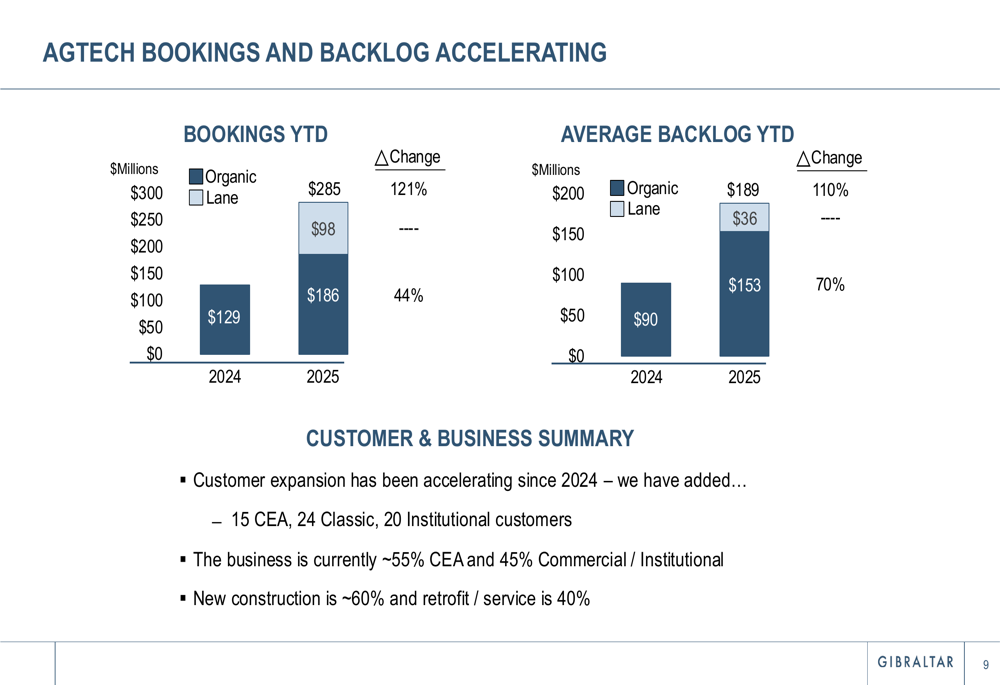

Despite margin pressures, Gibraltar highlighted accelerating bookings and backlog in the Agtech segment, indicating potential future growth. Year-to-date bookings reached $284 million (including $98 million from Lane), while the average backlog grew to $189 million (including $36 million from Lane).

The company also secured new commercial and institutional projects, including a $7.6 million design/build retrofit for Franklin Park Conservatory & Botanical Gardens and a $4.1 million new design/build facility for Kaplan Orchid Conservatory & Research Facility.

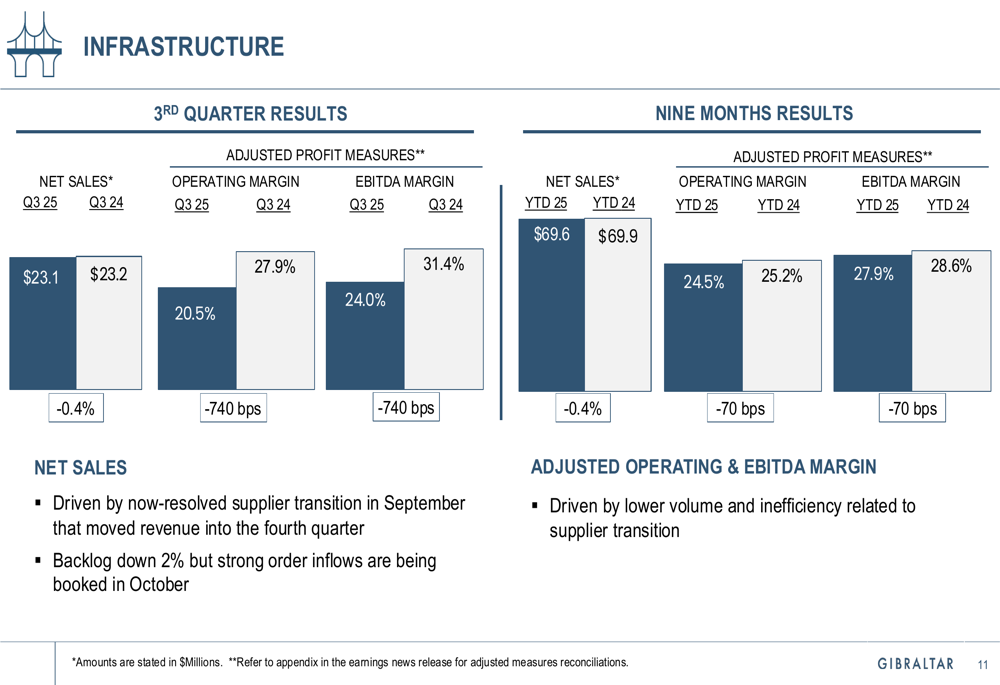

Infrastructure Segment

The Infrastructure segment reported relatively flat sales of $23.1 million compared to $23.2 million in Q3 2024, but experienced a significant decline in operating margin to 20.5% from 27.9% in the prior year. The company attributed this partly to a supplier transition in September that shifted revenue into the fourth quarter.

Financial Position & Outlook

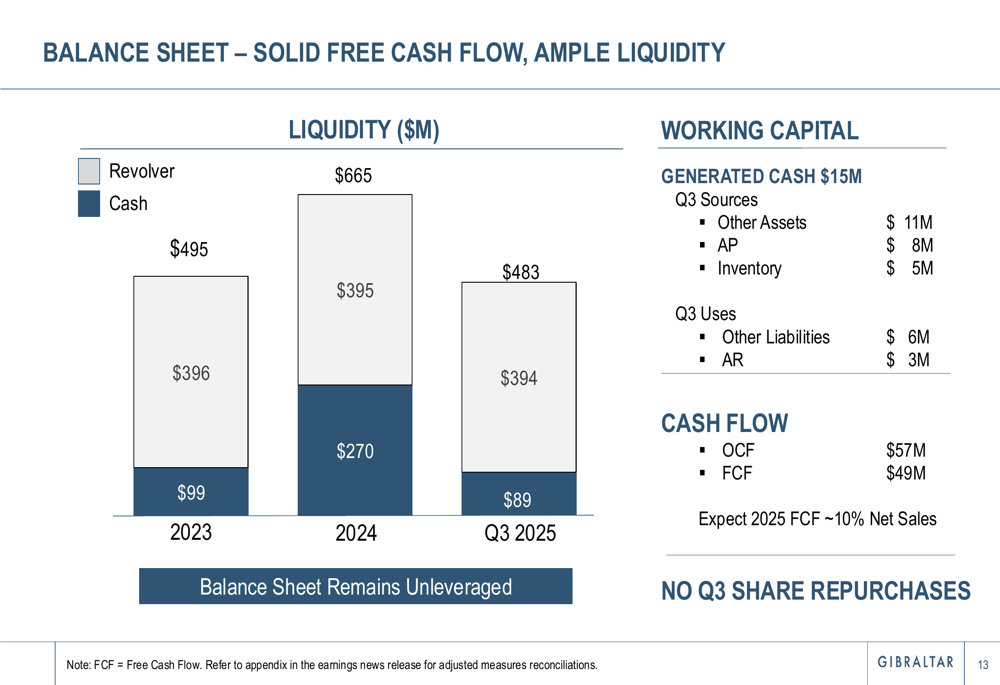

Gibraltar maintained a strong balance sheet with $394 million in cash and $89 million in revolver availability at the end of Q3 2025, providing total liquidity of $483 million. The company generated $57 million in operating cash flow and $49 million in free cash flow during the quarter.

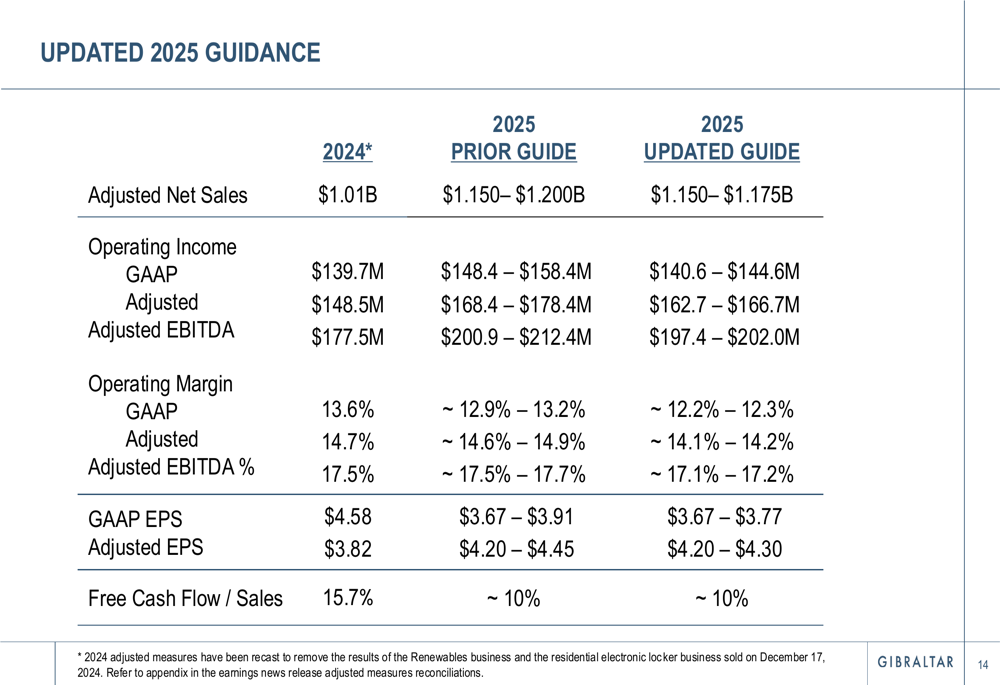

Looking ahead, Gibraltar narrowed its full-year 2025 guidance, reducing the upper end of its revenue range and lowering its profit expectations. The updated guidance calls for adjusted net sales of $1.150-$1.175 billion (narrowed from $1.150-$1.200 billion previously) and adjusted operating income of $162.7-$166.7 million (down from $168.4-$178.4 million).

Strategic Initiatives

Despite the mixed financial performance, Gibraltar continues to advance strategic initiatives across its segments. In the Residential segment, the company is expanding its geographic footprint to better serve retail customers. The Agtech segment is pursuing growth through both organic expansion and the integration of the Lane Supply acquisition.

In the Infrastructure segment, Gibraltar is introducing innovative products like its new micro-trenching seal technology for protecting telecom fiber-optic cables. Since March 2024, this patented solution has been installed across 350 miles in 13 states, offering advantages in installation speed, reduced roadway closures, and immediate trafficability.

While Gibraltar’s Q3 2025 results fell short of market expectations, the company’s continued sales growth, strong cash flow generation, and strategic initiatives appear to have maintained investor confidence, as reflected in the stock’s stable performance following the earnings release.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.