Street Calls of the Week

Introduction & Market Context

Graham Corporation (NYSE:GHM) released its fourth quarter and full-year fiscal 2025 financial results on June 9, 2025, showcasing record annual revenue and significant margin improvement. The company’s shares jumped 9.79% in premarket trading to $46.11, reflecting positive investor sentiment following the strong results.

The industrial equipment manufacturer, which specializes in mission-critical fluid, power, vacuum, and heat transfer solutions, has successfully completed the "Stabilize Phase" of its strategic plan and is now advancing into its "Improve" and "Growth" phases with clear financial targets through fiscal 2027.

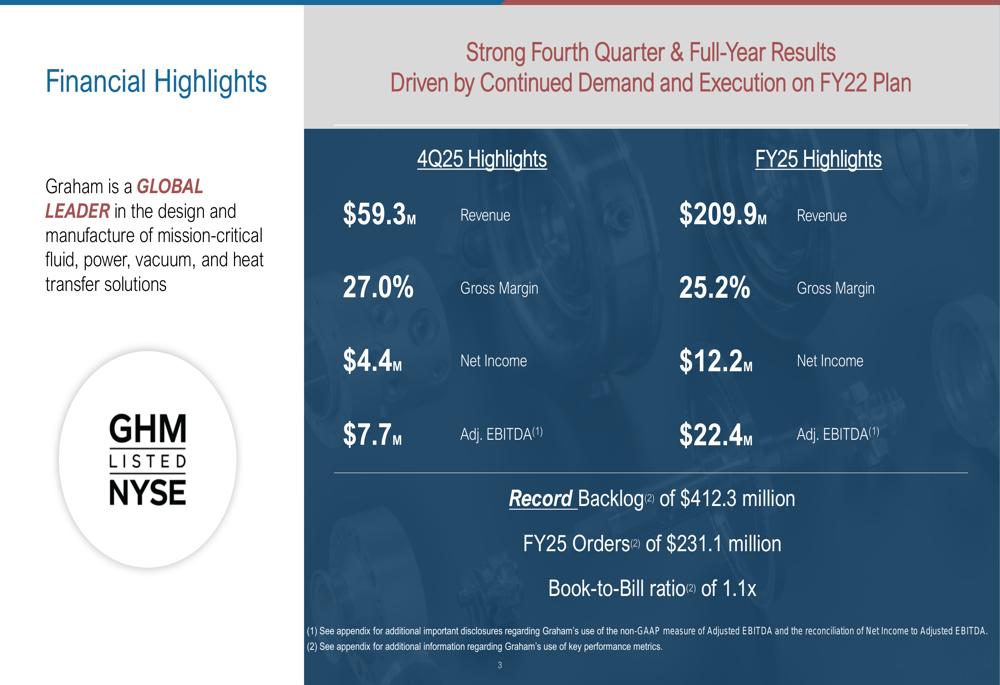

As shown in the following financial highlights, Graham achieved notable improvements across key metrics:

Quarterly Performance Highlights

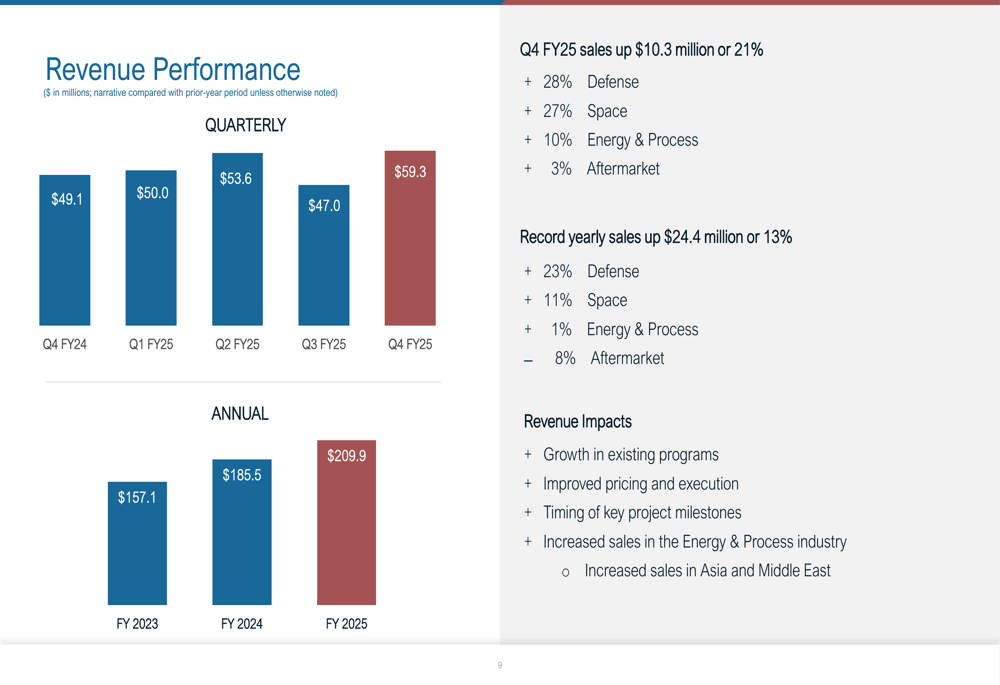

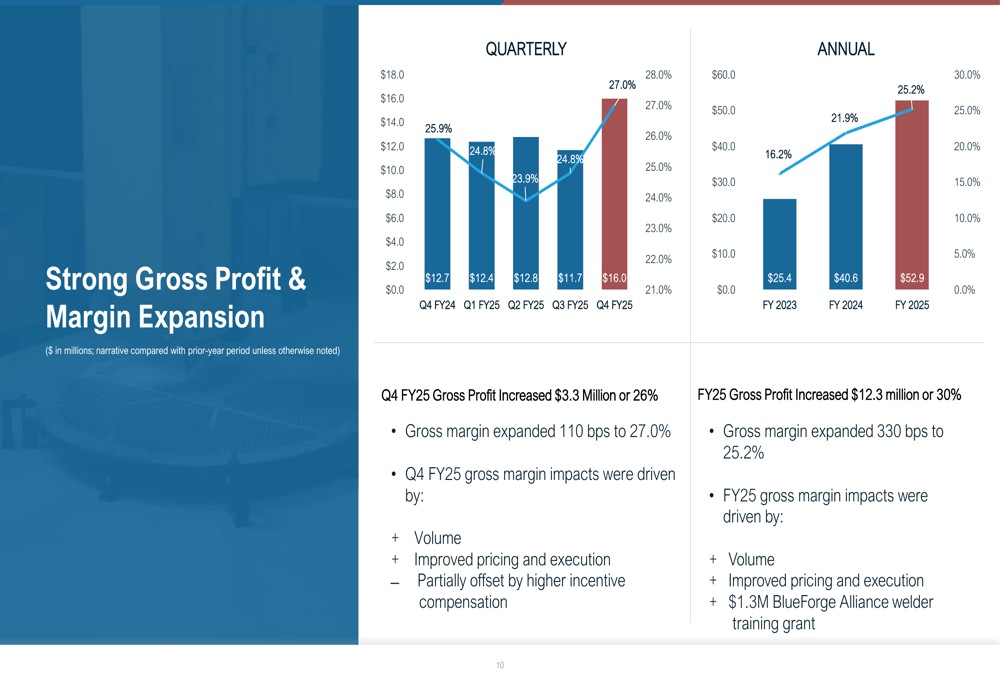

Graham’s fourth quarter fiscal 2025 revenue reached $59.3 million, representing a 21% increase compared to the same period last year. This growth was driven by strong performance across all segments, with Defense up 28%, Space up 27%, and Energy & Process up 10%. The company’s gross margin expanded 110 basis points to 27.0%, contributing to a net income of $4.4 million or $0.40 per diluted share.

The following chart illustrates Graham’s quarterly revenue performance, showing consistent growth throughout fiscal 2025:

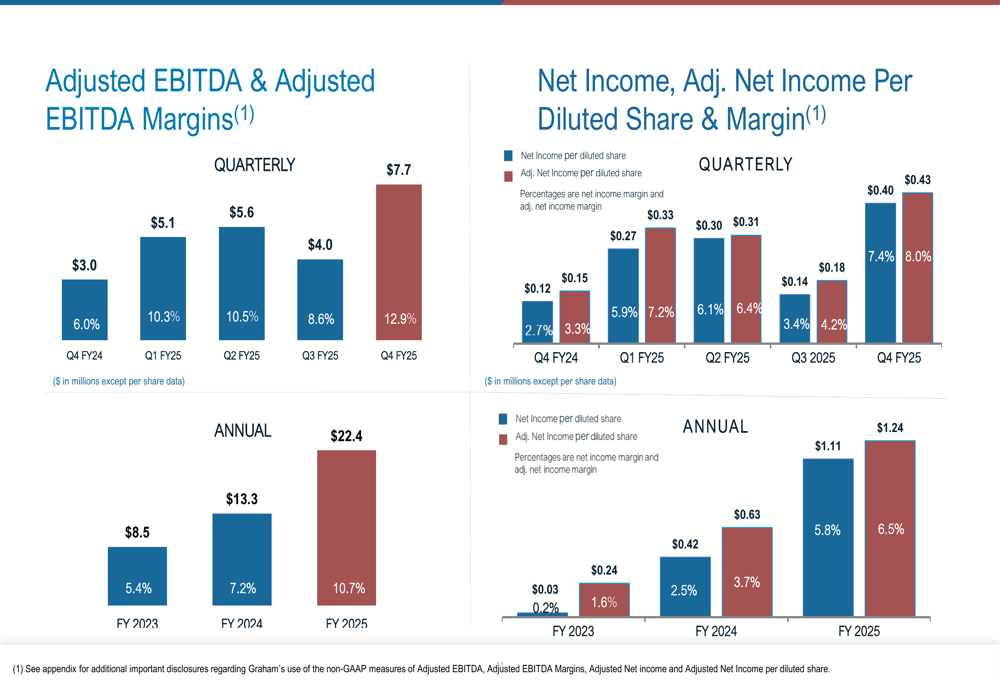

Adjusted EBITDA for Q4 FY25 reached $7.7 million, representing a margin of 12.9% compared to 6.0% in the prior-year period. This substantial margin expansion reflects improved pricing, better execution, and increased volume. The company’s adjusted net income per diluted share more than doubled to $0.43 from $0.15 in Q4 FY24.

The margin improvement trajectory is clearly demonstrated in the following chart:

Full-Year Financial Analysis

For the full fiscal year 2025, Graham achieved record revenue of $209.9 million, a 13% increase from $185.5 million in fiscal 2024. This growth was primarily driven by a 23% increase in Defense revenue and an 11% increase in Space revenue, partially offset by an 8% decline in Aftermarket sales.

The company’s profitability metrics showed significant improvement, with adjusted EBITDA increasing to $22.4 million (10.7% margin) from $13.3 million (7.2% margin) in the prior year. Net income nearly tripled to $12.2 million, representing 5.8% of sales compared to 2.5% in fiscal 2024.

The following chart details the progression of adjusted EBITDA and net income:

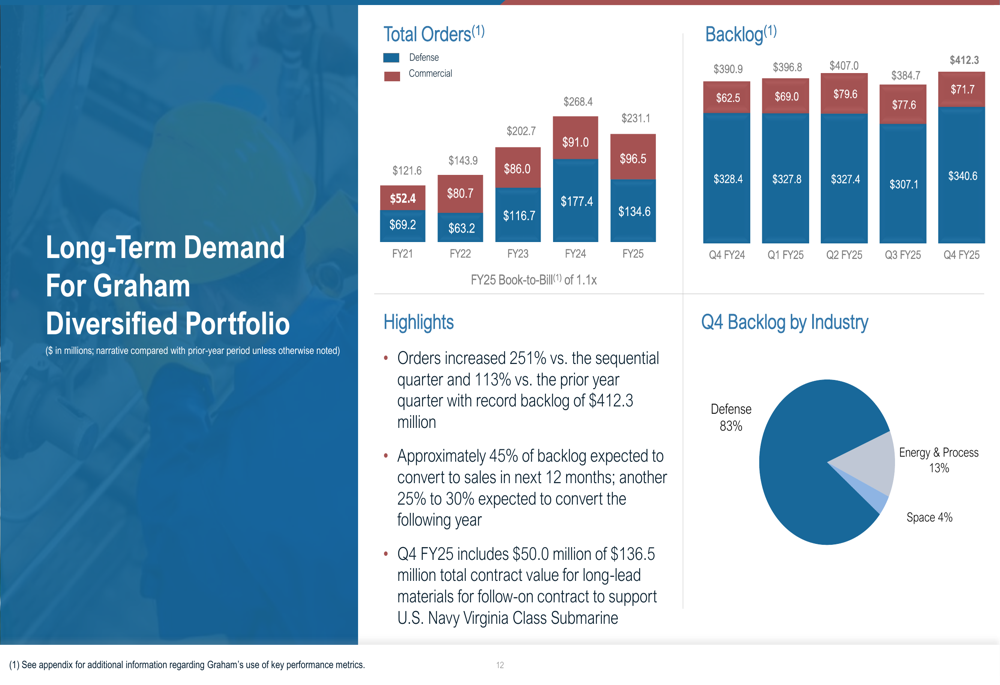

Graham ended fiscal 2025 with a record backlog of $412.3 million, up from $328.4 million at the end of fiscal 2024. The company’s book-to-bill ratio for the year was 1.1x, indicating continued strong demand for its products and services. Defense orders represented 83% of the backlog, highlighting Graham’s strong position in this sector.

The following chart illustrates the company’s order intake and backlog growth:

Strategic Initiatives and Growth Outlook

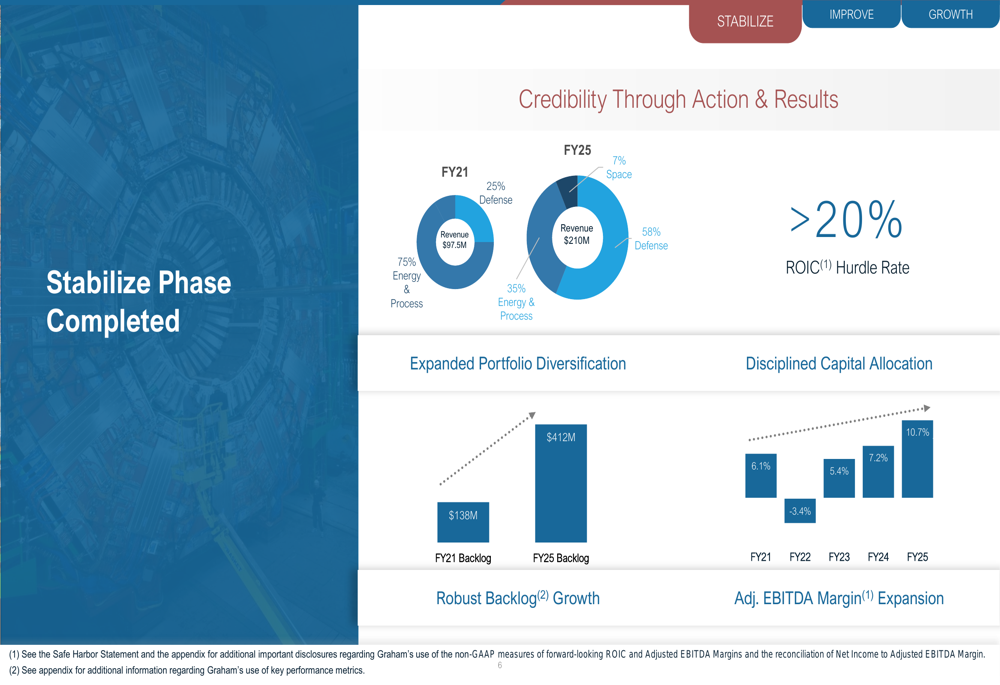

Graham has successfully completed the "Stabilize Phase" of its strategic plan, which has transformed the company’s revenue composition. In fiscal 2021, Energy & Process accounted for 75% of revenue and Defense for 25%. By fiscal 2025, Defense had grown to 58% of revenue, Energy & Process represented 35%, and Space had emerged as a new segment contributing 7%.

This strategic transformation is illustrated in the following chart:

The company’s financial position remains strong, with $21.6 million in cash and no debt outstanding as of the end of fiscal 2025. Graham generated $24.3 million in cash from operating activities during the year and invested $19.0 million in capital expenditures to support future growth.

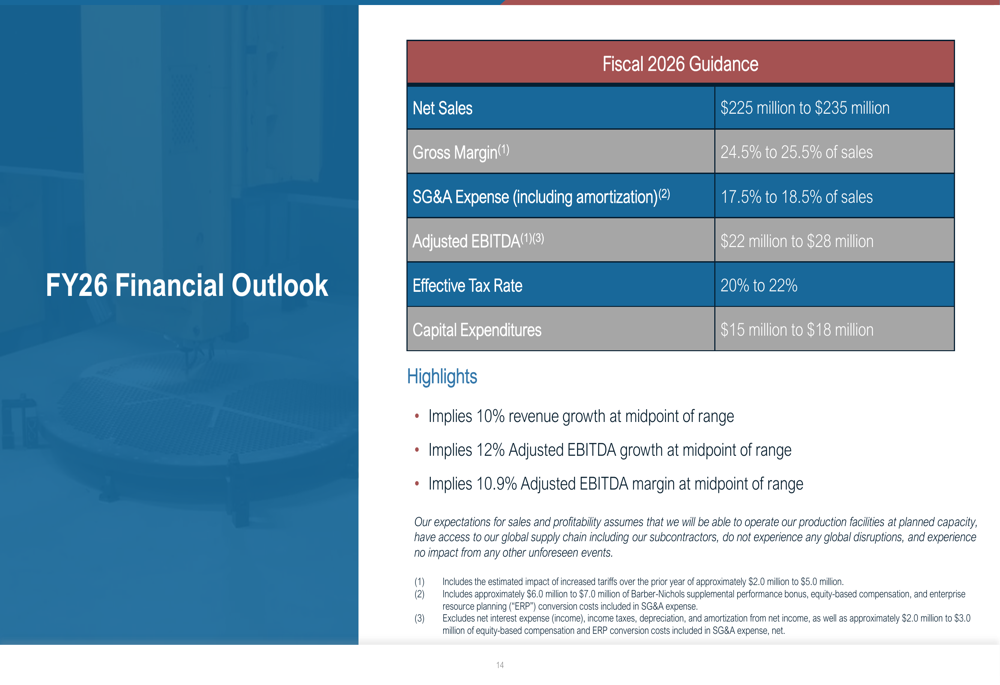

For fiscal 2026, Graham provided guidance for revenue between $225 million and $235 million, representing approximately 10% growth at the midpoint. The company expects adjusted EBITDA of $22 million to $28 million, implying a 10.9% margin at the midpoint and 12% growth over fiscal 2025.

The detailed fiscal 2026 guidance is presented in the following chart:

Forward-Looking Statements

Looking beyond fiscal 2026, Graham has established clear financial targets for fiscal 2027, aiming for revenue between $245 million and $255 million and adjusted EBITDA margins of 13% to 15%. The company noted that the completion of the Barber-Nichols earnout bonus expense at the end of fiscal 2026 is expected to contribute approximately 200 basis points to the adjusted EBITDA margin in fiscal 2027.

The company’s multi-year financial trajectory and future goals are illustrated in the following chart:

Graham has outlined a phased approach to sustainable, long-term growth across its three main sectors: Defense, Energy & Process, and Space. In the Defense sector, the company is focusing on naval ship and submarine demand acceleration, while in Energy & Process, it is addressing rising grid demand from AI and data centers. The Space segment is expanding due to geopolitical factors, with investments in cryogenic test facilities and expanded cleanroom capabilities.

The company also maintains an opportunistic M&A strategy to supplement its expected 8-10% annual organic growth. Graham is targeting U.S.-based, privately held companies in the fluid/power sectors supporting aerospace, defense, cryogenic, and niche industrial markets, with purchase prices ranging from $20 million to $80 million and target multiples below 10x EBITDA.

With a strong backlog, improving margins, and clear strategic direction, Graham Corporation appears well-positioned to continue its growth trajectory in fiscal 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.