Raytheon awarded $71 million in Navy contracts for missile systems

Introduction & Market Context

Granite Construction Incorporated (NYSE:GVA) delivered a strong second quarter performance in 2025, highlighted by strategic acquisitions and record committed and awarded projects (CAP). The company’s stock has responded positively to these developments, with shares climbing 8.14% to $100.94 following the earnings release on August 7, 2025, according to market data.

The infrastructure construction and materials company is capitalizing on robust public funding and increasing infrastructure needs, particularly in the Southeast and West regions. Granite’s vertical integration strategy continues to be a key differentiator in a competitive market environment where the Infrastructure Investment and Jobs Act (IIJA) spending is expected to peak in 2026-2027.

Quarterly Performance Highlights

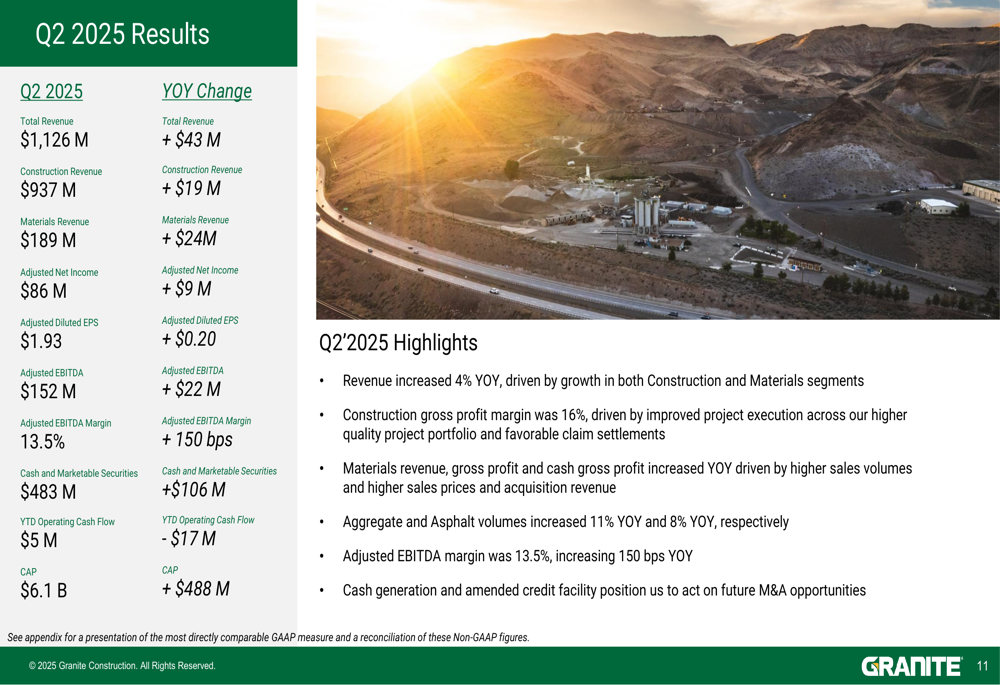

Granite reported total revenue of $1.126 billion for Q2 2025, representing a 4% increase year-over-year. The company’s adjusted diluted earnings per share reached $1.93, exceeding analyst expectations of $1.66 by 16.27%, despite a slight revenue shortfall compared to market forecasts.

As shown in the following comprehensive results summary, both the construction and materials segments contributed to the company’s growth:

Adjusted EBITDA grew to $152 million, up $22 million or 17% compared to the same period last year, with adjusted EBITDA margin expanding by 150 basis points to 13.5%. The construction segment, which accounts for approximately 83% of total revenue, generated $937 million, while the materials segment contributed $189 million, increasing by $19 million and $24 million year-over-year, respectively.

The materials segment showed particularly strong performance with improved gross profit margins. The following chart illustrates the product level gross profit margins for both aggregate and asphalt:

Aggregate cash gross profit margin improved to 32.5% in Q2 2025 from 31.9% in Q2 2024, while asphalt cash gross profit margin increased to 18.2% from 17.0% in the same period. These improvements reflect Granite’s successful vertical integration strategy and operational efficiencies.

Strategic Acquisitions

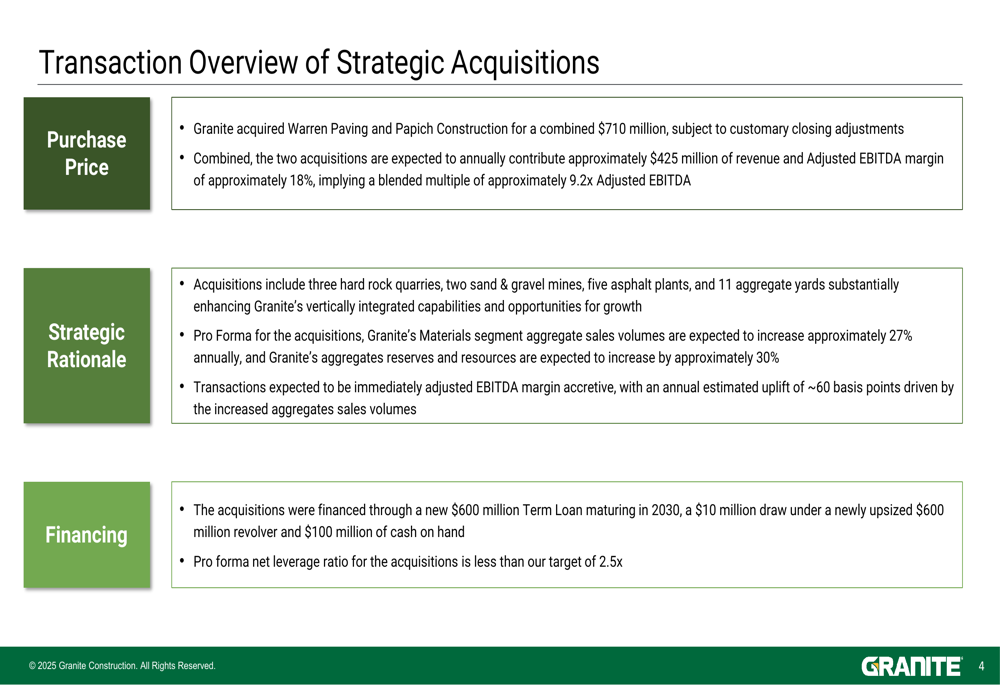

A major highlight from Granite’s presentation was the announcement of two strategic acquisitions: Warren Paving and Papich Construction, for a combined $710 million. These acquisitions align with Granite’s long-term growth strategy and are expected to significantly enhance the company’s materials capabilities and geographic footprint.

The following transaction overview details the strategic rationale and financial implications of these acquisitions:

The acquisitions are expected to contribute approximately $425 million in annual revenue with an adjusted EBITDA margin of about 18%, implying a 9.2x adjusted EBITDA multiple. Importantly, these transactions are expected to be immediately EBITDA margin accretive, with an estimated uplift of approximately 60 basis points.

Warren Paving, a leading aggregates producer with vertically integrated operations in the Mississippi River and Gulf Coast regions, brings substantial reserves and strategic positioning in the Southeast market. The company operates one quarry, one sand and gravel operation, 11 aggregate yards, three asphalt plants, and 168 owned and leased barges.

Papich Construction specializes in infrastructure projects and is a leading producer of heavy materials in Central California. The acquisition creates notable synergies with Granite’s existing construction operations in the Paso Robles-San Luis Obispo market.

Forward-Looking Statements

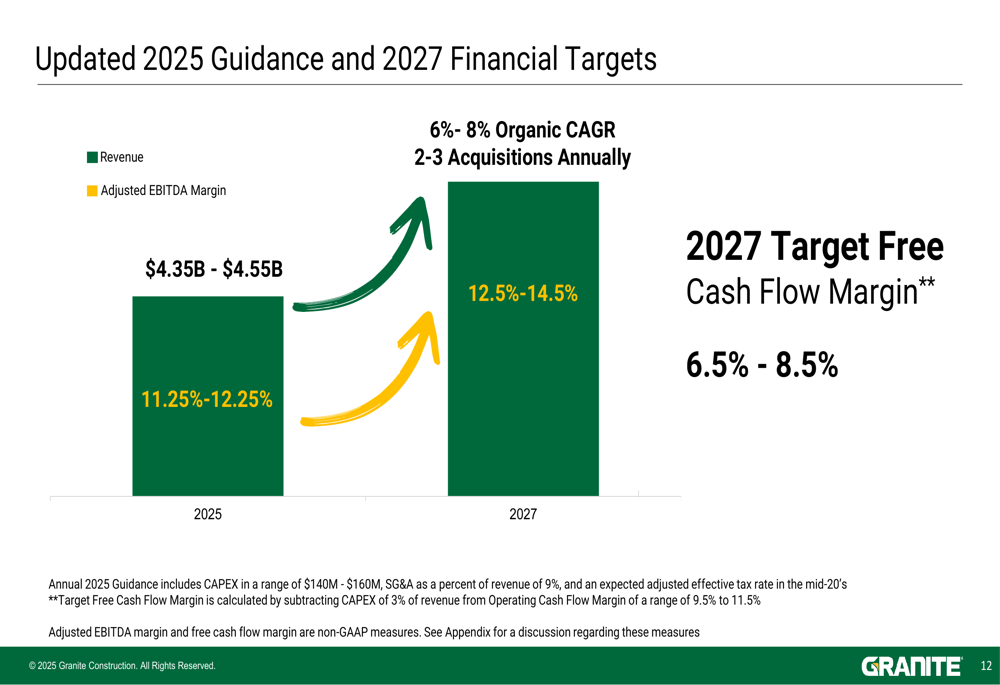

Granite has updated its 2025 guidance and provided ambitious targets for 2027, reflecting confidence in its growth trajectory and the positive impact of recent acquisitions. The following chart outlines these financial projections:

For 2025, Granite now expects revenue between $4.35 billion and $4.55 billion, with an adjusted EBITDA margin of 11.25% to 12.25%. Looking further ahead to 2027, the company targets 6-8% organic CAGR, plans to complete 2-3 acquisitions annually, and aims to achieve an adjusted EBITDA margin of 12.5-14.5%.

Capital expenditure for 2025 is projected to be between $140 million and $160 million, with SG&A expenses expected to remain at approximately 9% of revenue. The company anticipates an adjusted effective tax rate in the mid-20s.

Competitive Industry Position

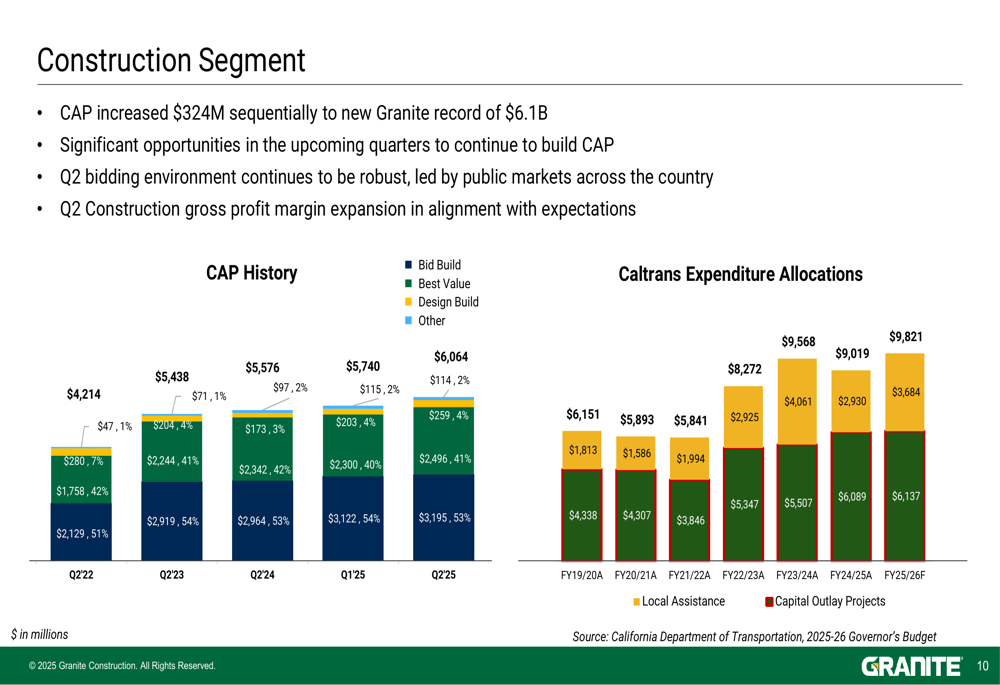

Granite’s record CAP of $6.1 billion underscores its strong competitive position in the infrastructure construction market. The following chart illustrates the CAP history and Caltrans expenditure allocations, highlighting the robust bidding environment:

The CAP increased by $324 million sequentially to reach a new company record of $6.1 billion. The composition of the CAP includes a mix of bid-build, best value, design-build, and other procurement types, reflecting Granite’s diversified approach to project acquisition.

Caltrans expenditure allocations show a positive trend, with projected spending increasing from $5.841 billion in FY21/22 to an estimated $9.019 billion in FY25/26. This growth in state infrastructure spending, combined with federal funding through the IIJA, provides a favorable market environment for Granite’s continued expansion.

The company’s vertically integrated model and home market strategy continue to be key differentiators. By controlling materials production and construction operations, Granite can maximize productivity, ensure quality, and leverage lower production costs compared to external pricing.

Granite’s strong cash position of $483 million, up $106 million, positions the company well for future growth opportunities through both organic expansion and strategic acquisitions. The recent financing of the Warren Paving and Papich Construction acquisitions through a new $600 million term loan, a $10 million draw under a newly upsized $600 million revolver, and $100 million of cash on hand, maintains a conservative pro forma net leverage ratio of less than 2.5x.

As infrastructure spending continues to accelerate, particularly with IIJA funding expected to peak in 2026-2027, Granite appears well-positioned to capitalize on these market opportunities while maintaining financial discipline and strategic focus on high-margin projects and materials operations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.