TSX runs higher on rate cut expectations

Introduction & Market Context

Granite Point Mortgage Trust Inc . (NYSE:GPMT) released its first quarter 2025 earnings presentation on May 7, revealing continued challenges in its commercial real estate loan portfolio, though with signs of stabilization. The company reported a GAAP net loss of $10.6 million, or $0.22 per share, as it continues to work through problem loans, particularly in the office sector.

The commercial mortgage REIT maintained a substantial credit loss reserve of $180.2 million, representing 8.8% of its total loan portfolio commitments, as it navigates ongoing pressures in commercial real estate markets. In after-hours trading, GPMT shares rose 4.21% to $1.98, suggesting investors may see some positive signs in the company’s gradual progress.

Quarterly Performance Highlights

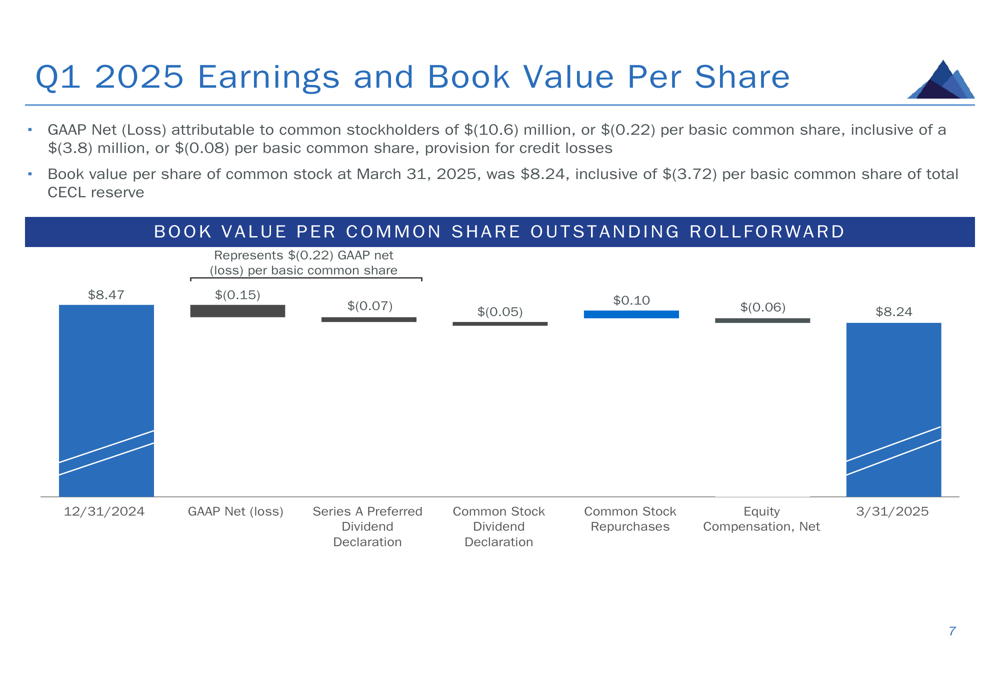

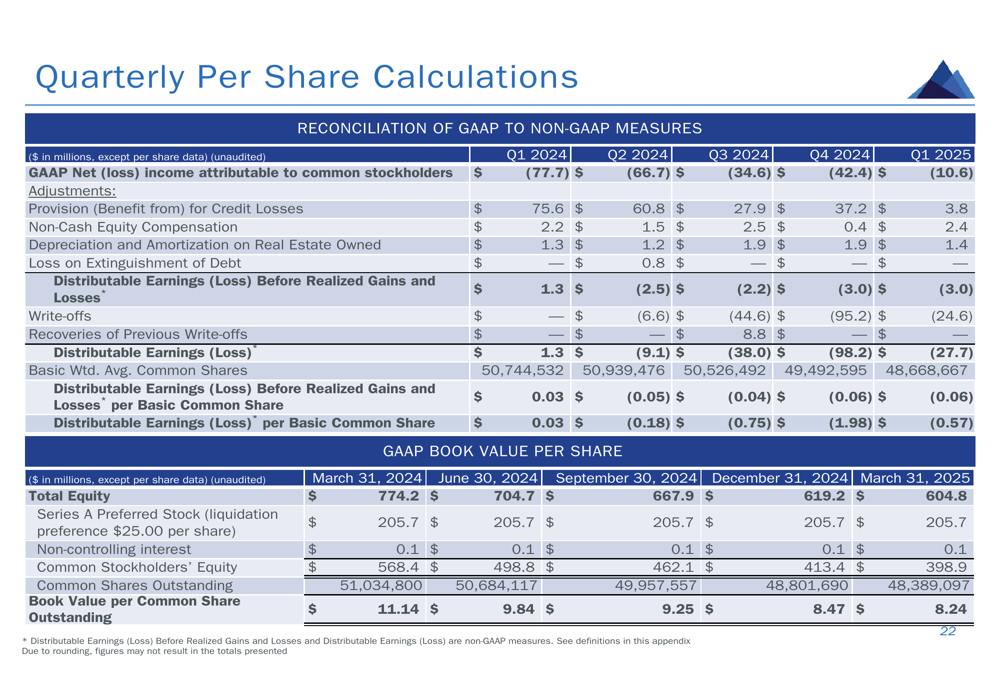

Granite Point reported a GAAP net loss of $10.6 million, or $0.22 per share, for the first quarter of 2025. Distributable earnings, a non-GAAP measure that excludes certain non-cash items, showed a loss of $27.7 million, or $0.57 per share. The company maintained its dividend at $0.05 per share, representing a 7.7% annualized yield based on current share prices.

Book value per common share declined slightly to $8.24 as of March 31, 2025, from $8.47 at the end of 2024. This decline was driven primarily by the net loss, preferred dividends, and common stock dividends, partially offset by accretion from share repurchases.

As shown in the following chart detailing the company’s earnings and book value per share changes:

The company’s total CECL (Current Expected Credit Losses) reserve of $180.2 million represents 8.8% of the total loan portfolio commitments, with 75% ($134.3 million) allocated to specific reserves for troubled loans. This marks a decrease from previous quarters, potentially indicating that the company is working through its problem loans.

The following chart illustrates the trend in CECL reserves over recent quarters:

Detailed Financial Analysis

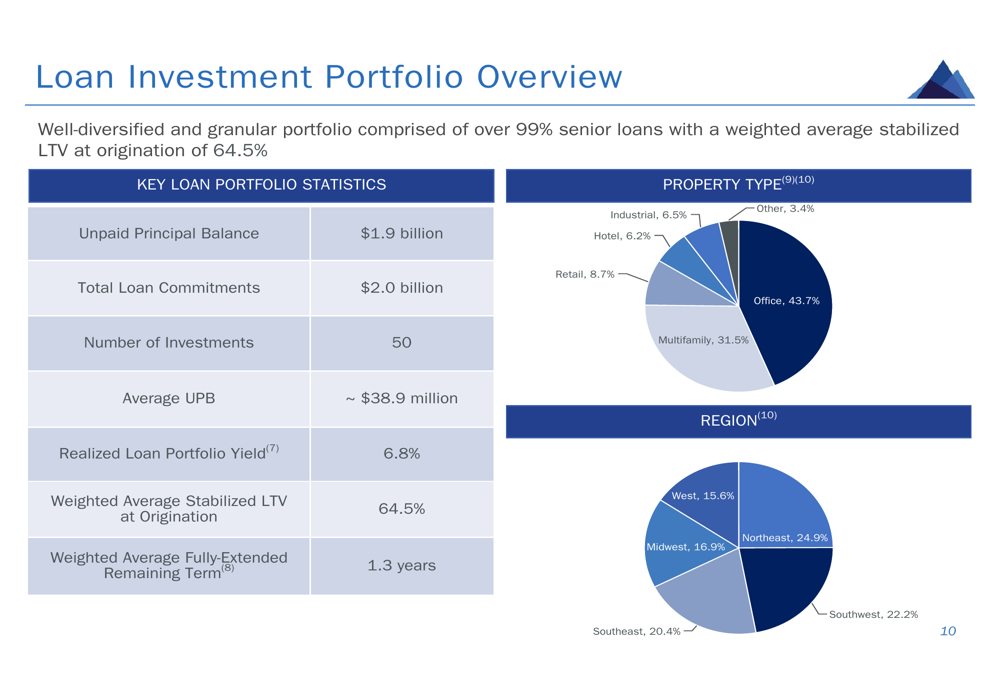

Granite Point’s loan portfolio stood at $2.0 billion in total commitments across 50 investments as of March 31, 2025. The portfolio remains well-diversified with 99% senior loans, of which 98% are floating rate. The weighted average stabilized loan-to-value (LTV) ratio at origination was 64.5%, with an average unpaid principal balance of $38.9 million per loan.

The portfolio diversification by property type and region is illustrated in the following chart:

Net loan portfolio activity for the quarter was negative $161.4 million in unpaid principal balance, resulting from two full loan repayments and partial repayments totaling $74.5 million, two loan resolutions of $97.4 million (including $24.6 million in write-offs), and fundings of $10.5 million on existing commitments.

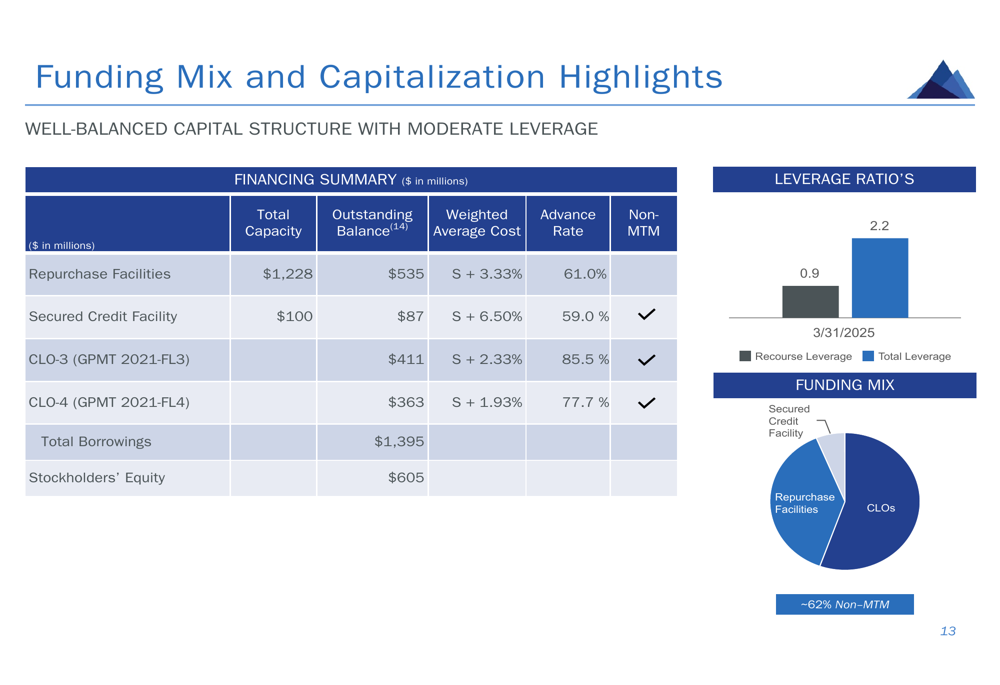

The company’s capitalization remains stable with $2.1 billion in total financing capacity, of which $1.4 billion is outstanding. Importantly, 62% of the company’s borrowings are non-mark-to-market, providing stability in volatile market conditions. Granite Point maintained $85.7 million in unrestricted cash and an additional $123.8 million in real estate owned (REO) assets.

The following chart details the company’s funding mix and capitalization:

Portfolio Management Strategy

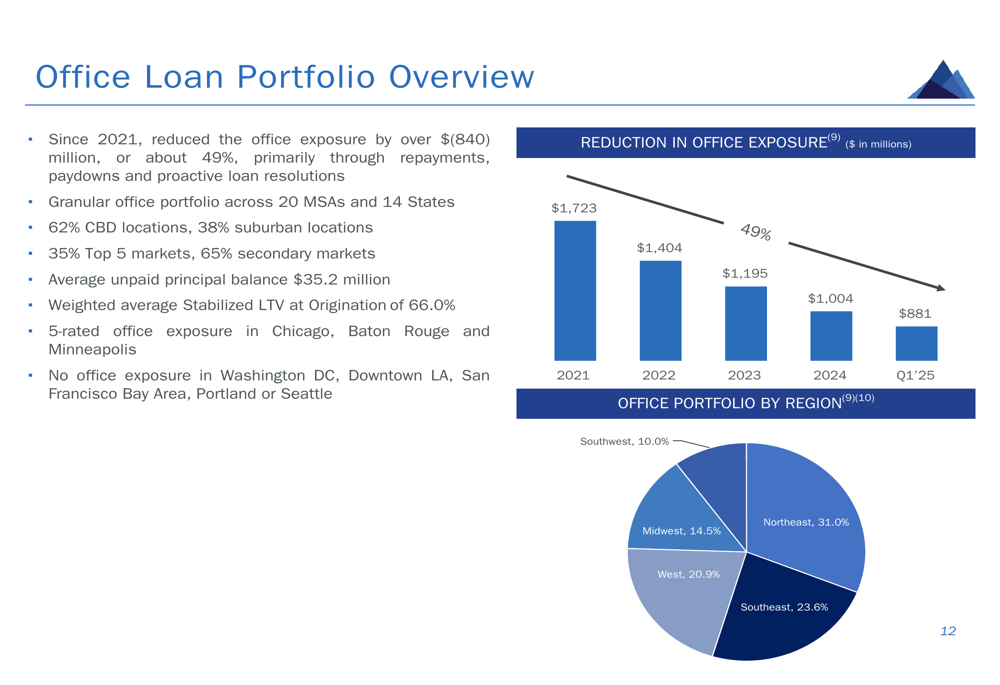

A key focus for Granite Point has been managing its office loan exposure, which still represents 43.7% of the portfolio. Since 2021, the company has reduced its office exposure by over $840 million, or approximately 49%, primarily through repayments, paydowns, and proactive loan resolutions.

The company’s office portfolio strategy is illustrated in the following chart:

Granite Point identified five loans rated "5" (the highest risk category) with an aggregate unpaid principal balance of $354.9 million. These loans have specific CECL reserves of approximately 38% of their unpaid principal balance, indicating significant expected losses. The company is actively pursuing resolution options for these loans, including foreclosure, deed-in-lieu arrangements, loan restructuring, or collateral sales.

The weighted average risk rating for the overall portfolio stands at 3.0 on a scale of 1-5, with 18.2% of loans rated as "5" and an additional 8.9% rated as "4" (watch list).

Forward-Looking Statements

After the end of the first quarter, Granite Point provided several business updates that will impact future results. The company extended its repurchase facilities maturities by approximately one year, enhancing its liquidity position.

The company anticipates the resolution of a hotel property-secured loan in Minneapolis with an unpaid principal balance of $52.2 million, which is expected to result in a write-off of approximately $15.4 million. Additionally, in May, the company resolved a mixed-use office and retail property-secured loan in Baton Rouge with an unpaid principal balance of $79.9 million, expecting a write-off of approximately $21.5 million.

On a positive note, Granite Point has realized full repayments on two office property-secured loans for a combined $32.1 million in the second quarter to date and funded approximately $3.0 million on existing loan commitments.

The following chart shows the company’s quarterly performance metrics, including distributable earnings and book value per share trends:

While Granite Point continues to face challenges with problem loans and credit losses, the pace of deterioration appears to be slowing. The company’s focus on maintaining liquidity, resolving troubled loans, and managing its office exposure positions it to potentially benefit from any stabilization in commercial real estate markets, particularly as it works through its highest-risk assets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.