U.S. stocks mixed ahead of Fed decision

Introduction & Market Context

Groupe Dynamite Inc. (TSX:GRGD) released its Q2 2025 investor presentation on September 10, 2025, showcasing exceptional financial performance that significantly exceeded market expectations. The Canadian fashion retailer, which operates the Garage and Dynamite brands, saw its stock close at $41.29 on September 9, representing a substantial rise from the $19.20 recorded after its Q1 earnings announcement earlier this year.

The company’s strong performance comes amid a challenging retail environment, with GRGD demonstrating remarkable resilience through its differentiated brand strategy and efficient inventory management systems. The stock has seen impressive momentum, trading near its 52-week high of $41.34, up substantially from its 52-week low of $10.35.

Quarterly Performance Highlights

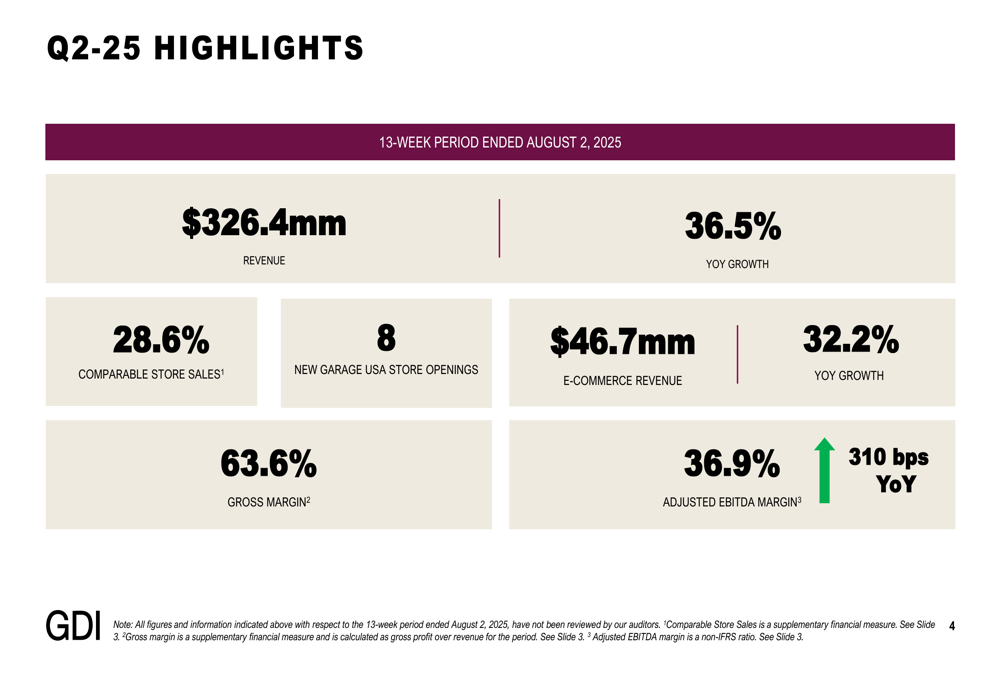

Groupe Dynamite reported exceptional financial results for the second quarter of fiscal 2025, with revenue reaching $326.4 million, representing a 36.5% year-over-year increase. This acceleration in growth is particularly notable compared to the 20% revenue growth reported in Q1 2025.

As shown in the following quarterly highlights:

Comparable store sales growth was equally impressive at 28.6%, more than doubling the 13% reported in Q1. The company’s e-commerce business continued to thrive, with revenue of $46.7 million, up 32.2% year-over-year.

Profitability metrics were equally strong, with gross margin reaching 63.6%, an improvement from the 62.1% reported in Q1, suggesting that the margin pressures mentioned in the previous earnings call have been successfully addressed. Adjusted EBITDA margin expanded by 310 basis points year-over-year to 36.9%.

The company also continued its US expansion strategy, opening 8 new Garage stores during the quarter.

Detailed Financial Analysis

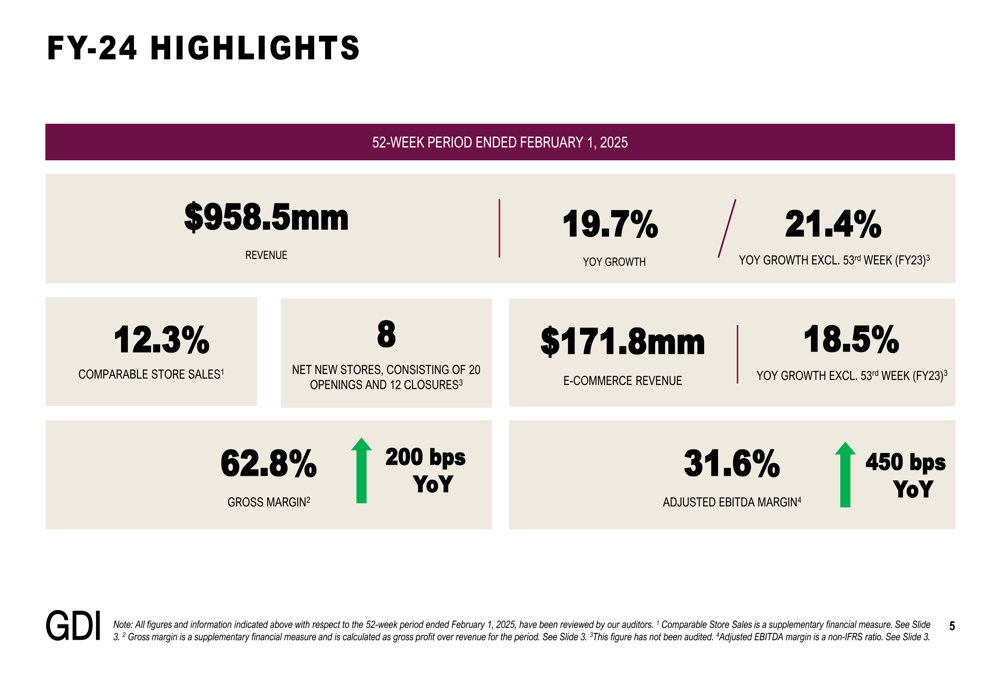

The strong Q2 performance builds on solid results from fiscal 2024, which saw annual revenue of $958.5 million, representing 19.7% year-over-year growth. The following slide details the company’s full-year 2024 performance:

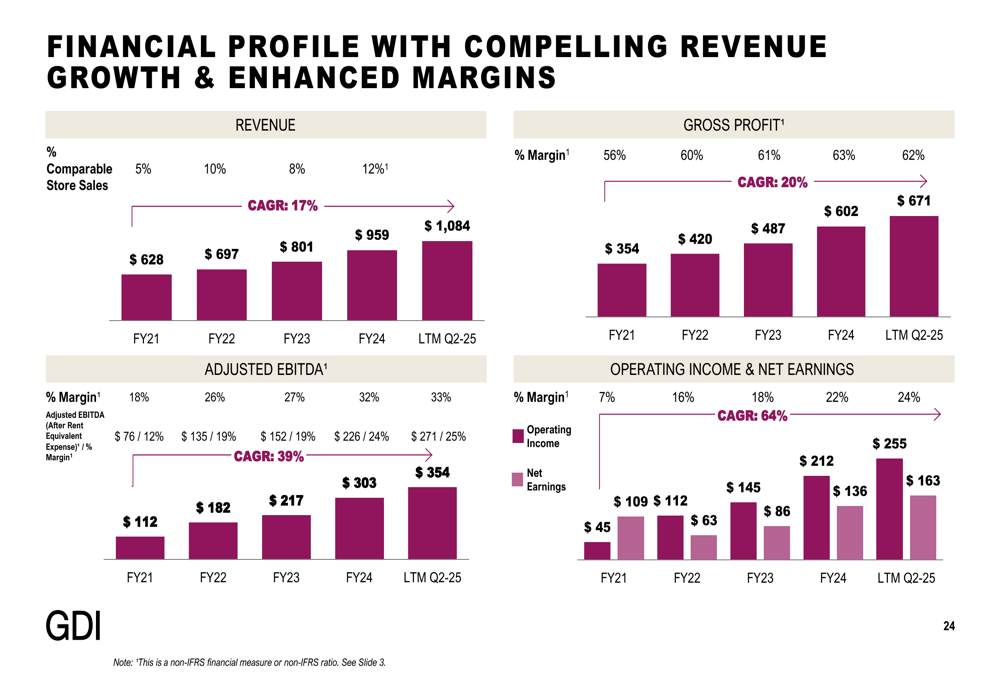

Groupe Dynamite’s financial profile demonstrates compelling revenue growth trends, with significant improvements in profitability metrics over recent years:

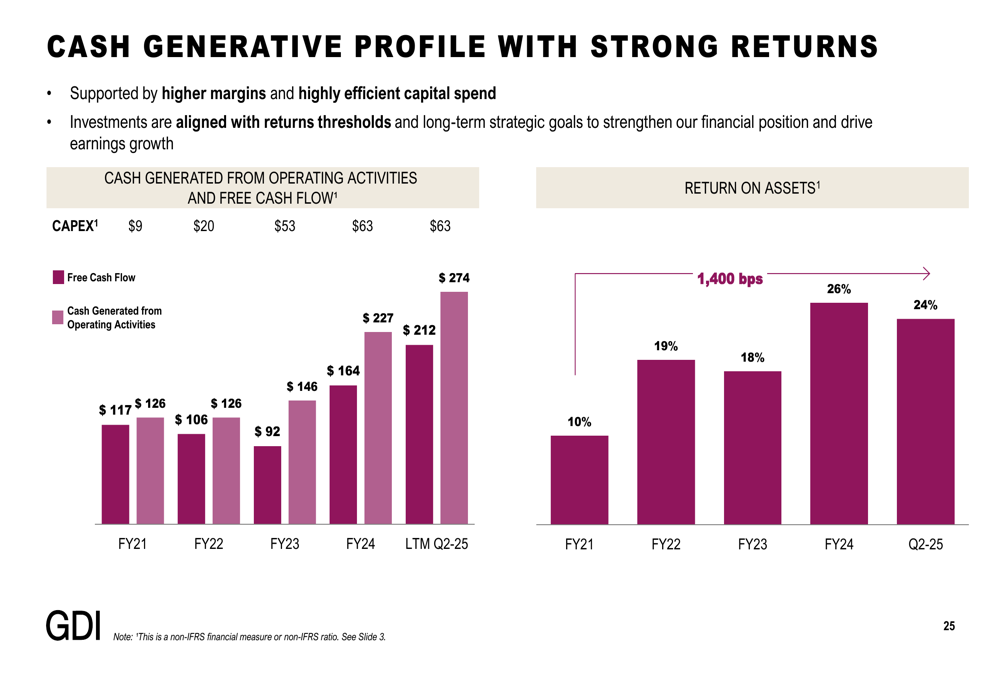

The company has maintained a cash-generative business model with strong returns on assets, reaching 26% in FY2024:

Key performance indicators highlight Groupe Dynamite’s operational efficiency, including:

- Average Unit Retail CAGR of approximately 11% from FY19-24

- Inventory turnover of approximately 8.5x in FY24

- Low markdown rate of approximately 6% in FY24

- 50% of purchasing decisions made in-season

- Product design to distribution center in under 8 weeks

These metrics underscore the company’s ability to efficiently manage inventory and respond quickly to changing consumer preferences, contributing to its strong financial performance.

Strategic Initiatives

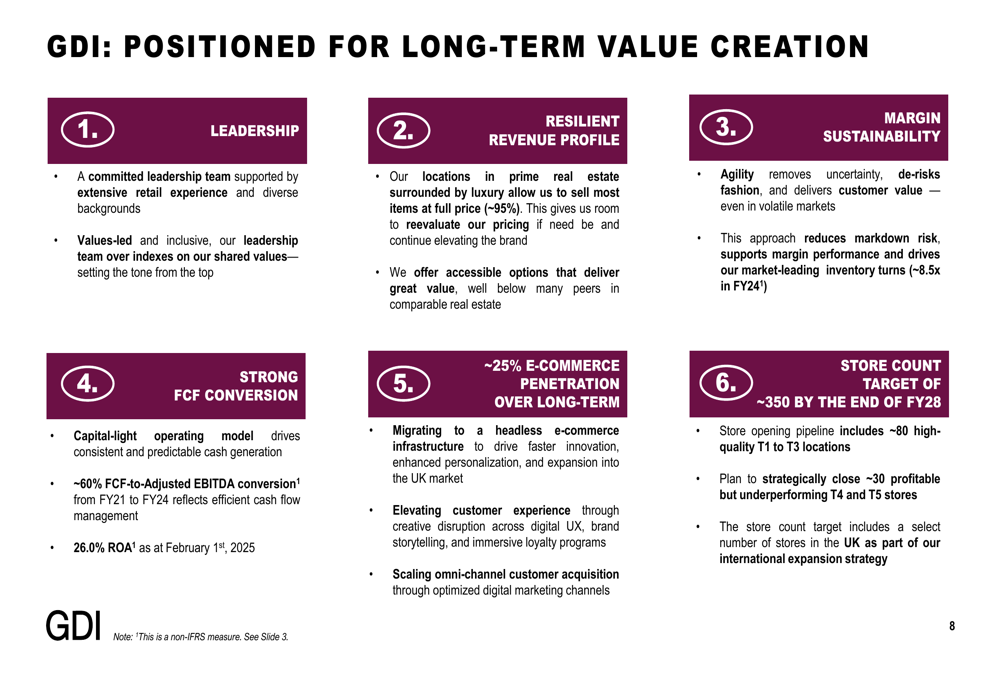

Groupe Dynamite’s presentation outlined several strategic initiatives driving its growth and positioning it for long-term value creation:

The company’s store expansion strategy remains a key growth driver, with a current portfolio of 299 stores across North America. Garage, which targets a younger demographic, has 220 locations (100 in Canada and 120 in the US), while Dynamite, focused on an older demographic, has 79 stores (76 in Canada and 3 in the US).

US operations have become increasingly important to the company’s financial performance, with US stores (representing approximately 37% of the store network) contributing approximately 56% of 4-Wall EBITDA in FY24.

The company has identified four key levers for future growth:

Groupe Dynamite’s omnichannel strategy is proving effective, with the company noting that while only about 20% of identifiable customers shop across both online and physical channels, these omnichannel shoppers generate approximately 40% of revenue from identifiable customers, highlighting their higher lifetime value.

Forward-Looking Statements

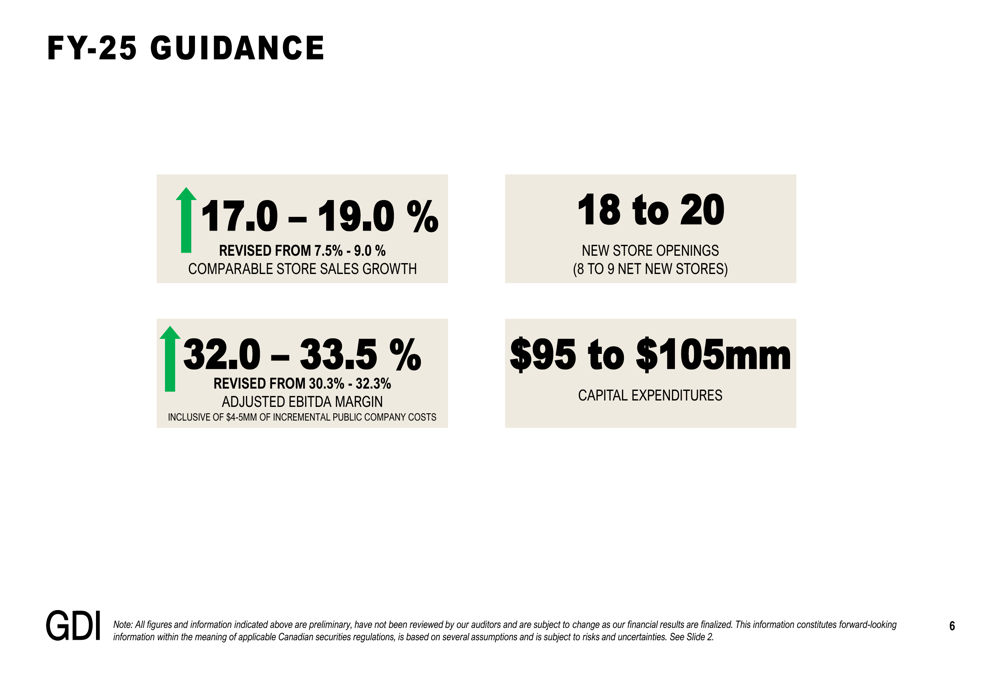

Based on its strong performance, Groupe Dynamite has significantly raised its full-year guidance for fiscal 2025:

The company now expects comparable store sales growth of 17.0-19.0%, more than double its previous guidance of 7.5-9.0%. Adjusted EBITDA margin guidance has also been raised to 32.0-33.5% from the previous 30.3-32.3%.

Groupe Dynamite plans to open 18-20 new stores in fiscal 2025 (resulting in 8-9 net new stores after closures), with capital expenditures projected at $95-105 million. The company has set an ambitious target of reaching approximately 350 stores by the end of fiscal 2028, representing a significant expansion from its current 299-store footprint.

International expansion is also on the horizon, with plans to enter the UK market starting in fiscal 2026, diversifying the company’s geographic presence beyond North America.

The company’s long-term strategy includes growing e-commerce penetration to approximately 25%, supported by investments in its digital platform and omnichannel capabilities.

With its strong financial performance, clear growth strategy, and efficient operational model, Groupe Dynamite appears well-positioned to continue its growth trajectory and deliver value to shareholders in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.