TSX futures tick up after index logs fresh record high close

Introduction & Market Context

Guild Holdings Company (NYSE:GHLD) released its fourth quarter and full year 2024 investor presentation on March 6, 2025, revealing a significant turnaround from the previous year. The mortgage lender demonstrated strong performance despite ongoing market volatility, with its focus on purchase mortgages proving to be a successful strategy in navigating interest rate fluctuations.

The company’s stock has shown resilience, currently trading at $19.95, near its 52-week high of $20.15, reflecting investor confidence in Guild’s business model and financial performance. This represents a substantial recovery from its 52-week low of $10.78.

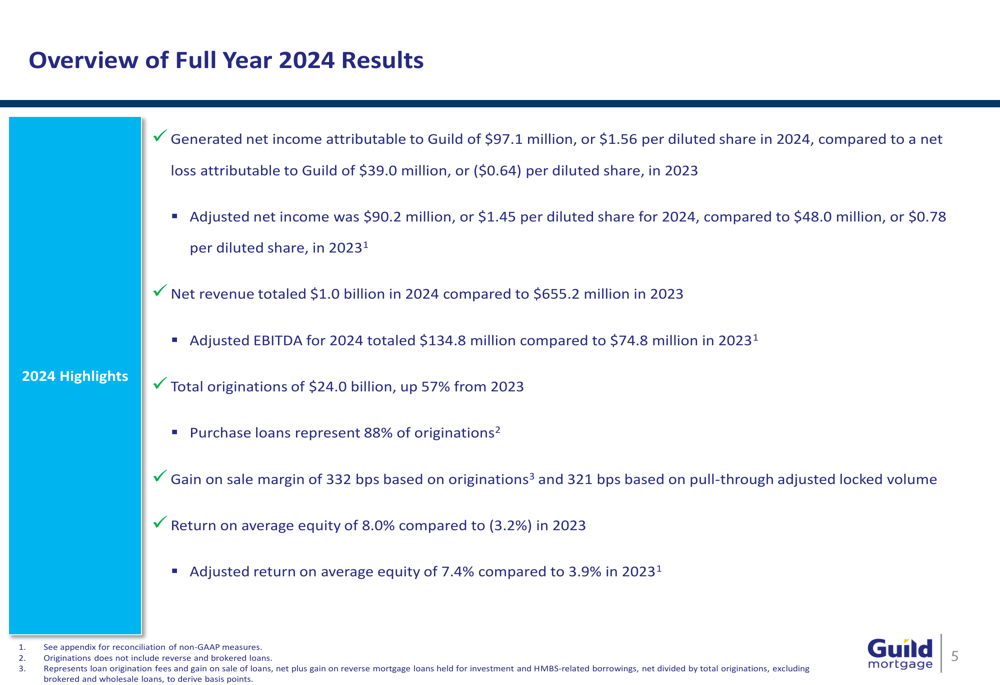

Full Year 2024 Performance Highlights

Guild Holdings reported a remarkable turnaround in 2024, generating net income attributable to Guild of $97.1 million ($1.56 per diluted share), compared to a net loss of $39.0 million in 2023. Adjusted net income nearly doubled to $90.2 million ($1.45 per diluted share) from $48.0 million in 2023.

The company’s net revenue surged to $1.0 billion, up significantly from $655.2 million in 2023, while adjusted EBITDA increased to $134.8 million from $74.8 million in the previous year. Total (EPA:TTEF) originations reached $24.0 billion, representing a 57% increase from 2023, with purchase loans accounting for 88% of originations.

As shown in the following overview of Guild’s 2024 results, the company achieved substantial improvements across key financial metrics:

The company’s return on average equity improved dramatically to 8.0% compared to -3.2% in 2023, while adjusted return on average equity rose to 7.4% from 3.9%. These metrics demonstrate Guild’s ability to generate stronger returns for shareholders following its strategic initiatives.

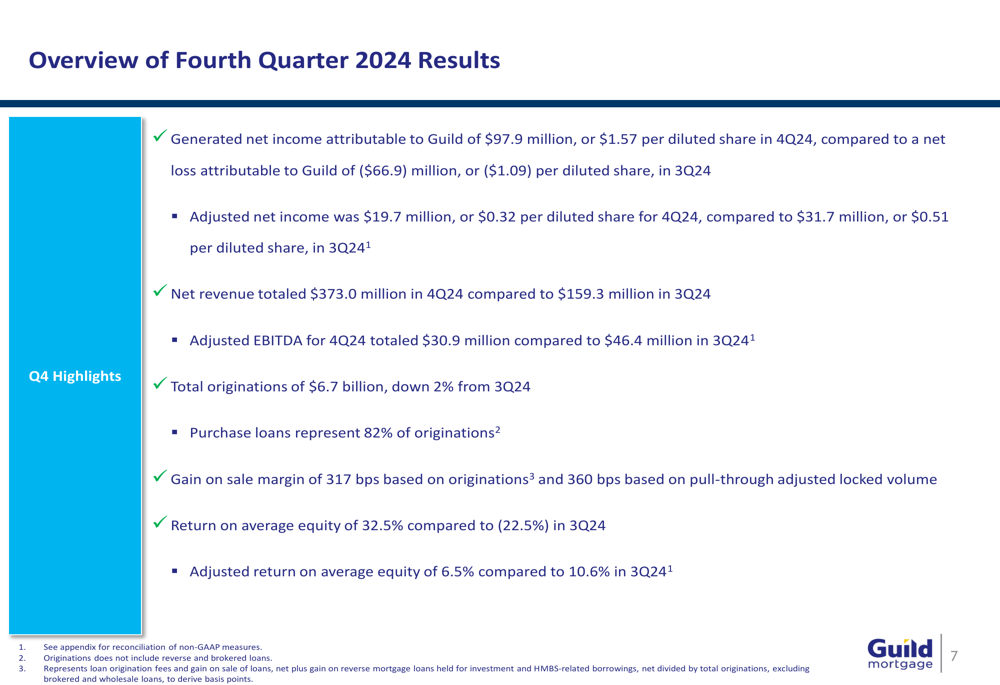

Fourth Quarter 2024 Results

For the fourth quarter of 2024, Guild reported net income attributable to Guild of $97.9 million ($1.57 per diluted share), a significant improvement from a net loss of $66.9 million in the third quarter. However, adjusted net income decreased to $19.7 million ($0.32 per diluted share) from $31.7 million in Q3 2024.

Net revenue for Q4 more than doubled to $373.0 million from $159.3 million in the previous quarter, though adjusted EBITDA declined to $30.9 million from $46.4 million. Total originations were $6.7 billion, down slightly by 2% from Q3, with purchase loans representing 82% of originations.

The following chart details Guild’s fourth quarter performance metrics:

The quarter-over-quarter decline in adjusted net income and EBITDA, despite higher net revenue, suggests some operational challenges or one-time factors affecting the company’s profitability in Q4. However, the overall return on average equity improved substantially to 32.5% compared to -22.5% in Q3 2024.

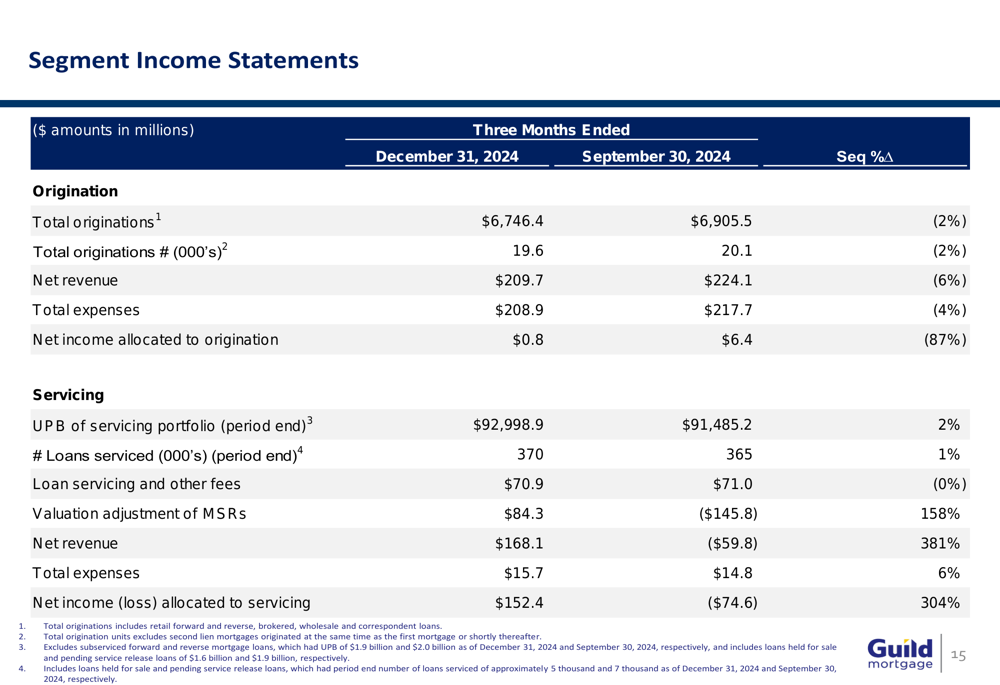

Segment Performance Analysis

Guild’s business operates through two primary segments: Origination and Servicing. The Origination segment showed mixed results in Q4, with net income of $0.8 million, down from $6.4 million in Q3. The gain on sale margin based on originations decreased to 317 basis points from 333 basis points in the previous quarter, though the margin based on pull-through adjusted locked volume improved to 360 basis points from 321 basis points.

The Servicing segment demonstrated remarkable improvement, with net income of $152.4 million in Q4 compared to a net loss of $74.6 million in Q3. The in-house servicing portfolio increased 2% to $93.0 billion, and the company retained servicing rights on 64% of loans sold.

The detailed segment performance for Q4 2024 compared to Q3 2024 is illustrated below:

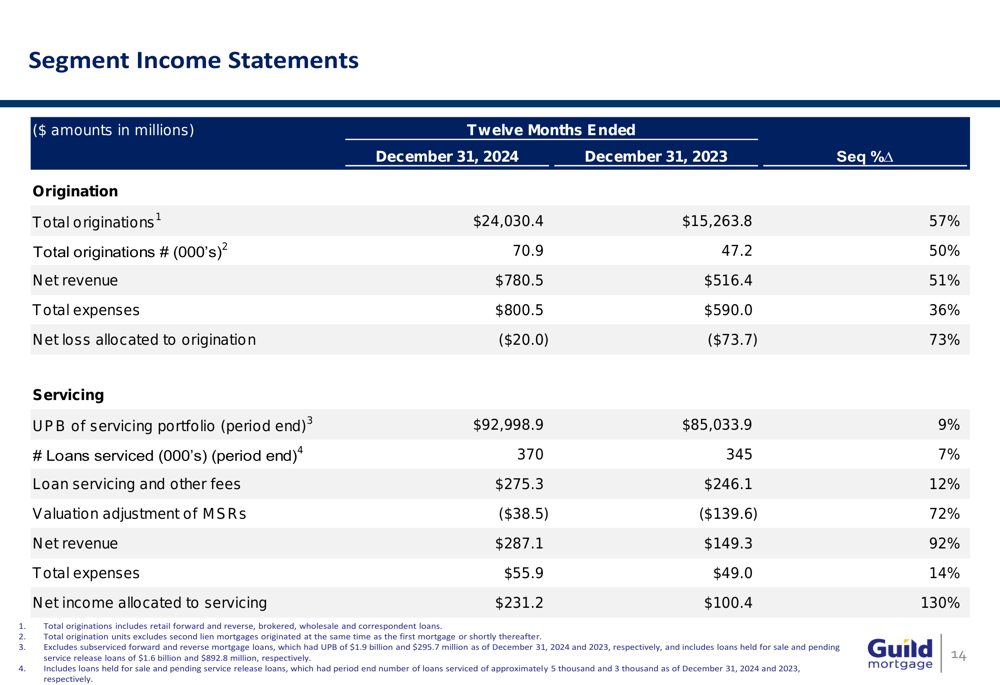

For the full year 2024, the Origination segment reported a net loss of $20.0 million, a significant improvement from the $73.7 million loss in 2023. The Servicing segment generated net income of $231.2 million, more than double the $100.4 million from 2023. The in-house servicing portfolio grew 9% year-over-year to $93.0 billion.

The annual segment performance comparison reveals the substantial improvements achieved in 2024:

Strategic Positioning and Business Model

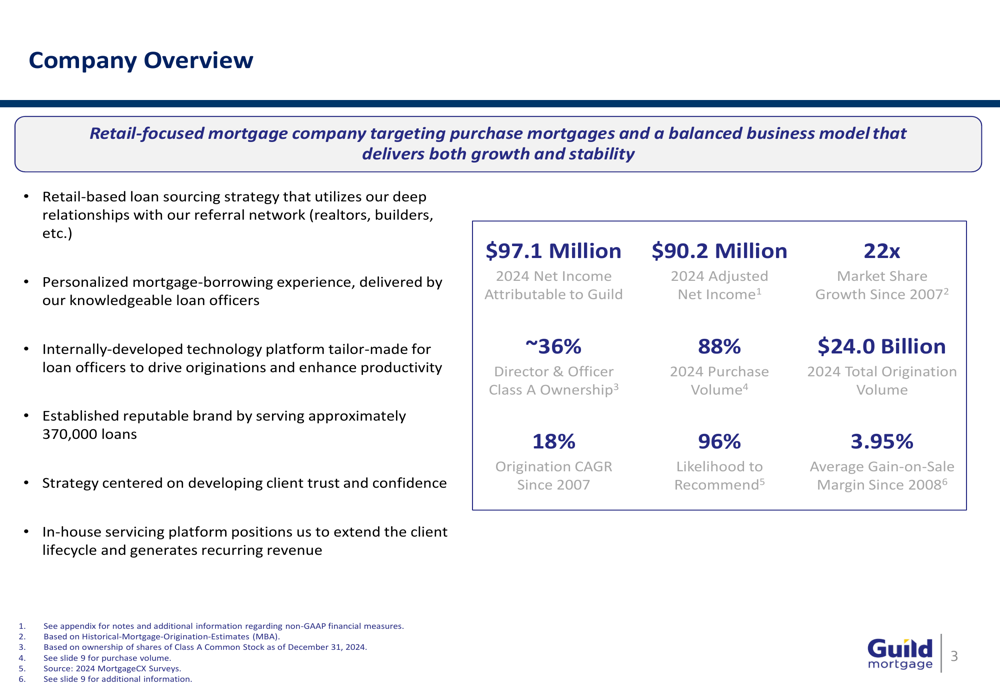

Guild’s investor presentation emphasized its retail-focused mortgage business model targeting purchase mortgages, which has provided stability through market cycles. The company’s strategy has enabled more durable originations and consistent returns compared to competitors who rely more heavily on refinancing activity.

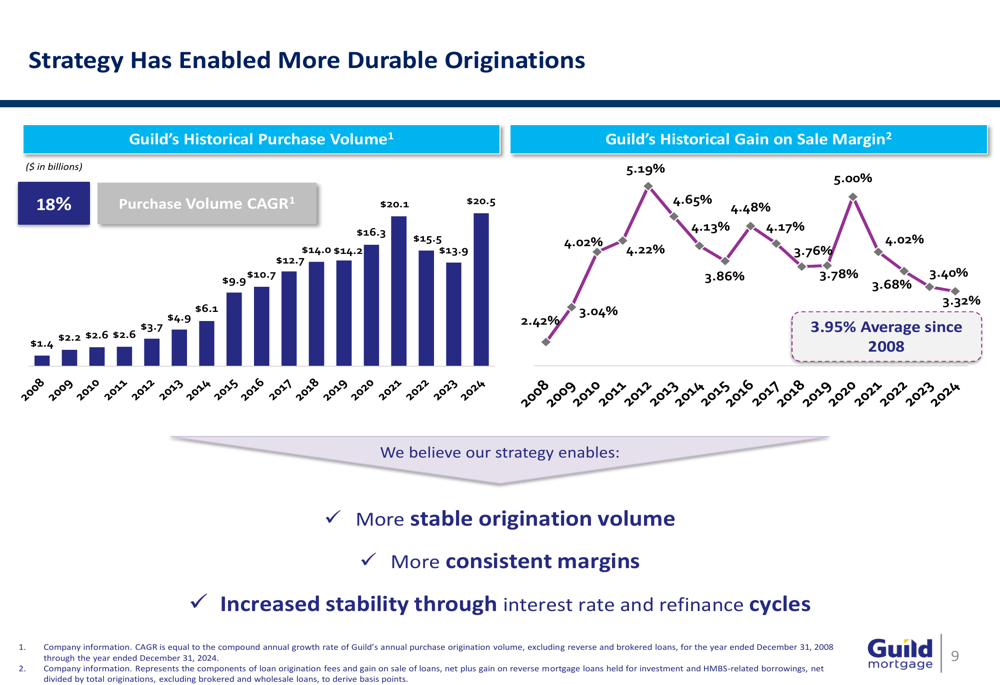

The following chart illustrates Guild’s historical purchase volume growth and gain on sale margin stability:

As shown in the chart, Guild has achieved an 18% compound annual growth rate in purchase volume since 2008, growing from $1.4 billion to $20.5 billion in 2024. The company has maintained an average gain on sale margin of 3.95% since 2008, demonstrating resilience through various interest rate environments.

Guild’s business model leverages relationships with a referral network, providing a personalized mortgage experience through knowledgeable loan officers. The company’s internally-developed technology platform drives originations and enhances productivity, while its in-house servicing platform extends the client lifecycle and generates recurring revenue.

Forward-Looking Statements

Looking ahead, Guild appears well-positioned to continue its growth trajectory. Recent earnings reports from Q1 2025 indicate the company has maintained its momentum, with loan originations increasing by 35% year-over-year to $5.2 billion and the servicing portfolio growing to $94 billion.

The company’s focus on first-time homebuyers and expansion of its loan officer headcount (doubled since the end of 2020) suggests a continued emphasis on the purchase mortgage market. While market volatility remains a concern, Guild’s balanced business model and focus on purchase mortgages should provide relative stability compared to competitors more dependent on refinancing activity.

Guild’s ability to maintain gain on sale margins around 330-340 basis points, as indicated in recent guidance, aligns with its historical performance. The company’s exploration of strategic acquisitions could provide additional growth opportunities in the coming years.

With a strong capital position and improved profitability, Guild Holdings appears well-equipped to navigate the challenges of the mortgage market while continuing to expand its market share and enhance shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.