Sterling holds ground amid stabilizing U.K. debt market

Introduction & Market Context

Gulfport Energy (OTC:GPORQ) Operating Corp (NYSE:GPOR) released its Q2 2025 investor presentation on August 6, 2025, highlighting the company’s financial performance, operational efficiencies, and strategic initiatives focused on shareholder returns. The natural gas producer, with assets in the Utica/Marcellus and SCOOP basins, has seen its stock trade at $166.85 as of the most recent close, with shares rising 1.47% in the most recent session and showing additional 1.12% gains in after-hours trading.

The company’s presentation comes after a Q1 2025 earnings report that showed mixed results, with EPS of $5.61 exceeding analyst expectations of $5.20, while revenue of $255.95 million fell short of the $325 million forecast. Despite revenue challenges, Gulfport continues to emphasize its operational efficiency improvements and strong free cash flow generation.

Quarterly Performance Highlights

Gulfport reported solid Q2 2025 operational results, with total net production of 1,006.3 MMcfe/day, including 19.2 MBbls/day of liquids production. The company generated $64.6 million in adjusted free cash flow during the quarter while incurring $124.2 million in capital expenditures. Per unit operating costs were $1.22 per Mcfe, showing improvement from the first half average of $1.26 per Mcfe.

As shown in the following quarterly results summary:

The company turned 14 gross wells to sales during the quarter and maintained its full-year 2025 guidance of 1.04-1.065 Bcfe/day of total net production. Notably, Gulfport continued its shareholder return program, repurchasing $65 million of common stock during Q2 while maintaining a leverage ratio of 0.85x.

Strategic Initiatives

A central focus of Gulfport’s strategy is returning capital to shareholders through an aggressive share repurchase program. Since March 2022, the company has returned approximately $709 million to shareholders at an average price of $113.48 per share, reducing outstanding shares by approximately 18%.

The following chart illustrates Gulfport’s capital return strategy and NAV upside potential compared to peers:

Gulfport is now accelerating its shareholder return strategy by planning to redeem its preferred equity. This move is expected to simplify the capital structure, eliminate preferred dividends, and be accretive to per-share cash flow metrics while maintaining a strong balance sheet.

As shown in this analysis of the preferred redemption impact:

The company plans to allocate substantially all of its 2025 adjusted free cash flow toward the redemption of preferred equity and common stock repurchases, excluding discretionary acreage acquisitions. This aligns with its historical practice of returning 96-99% of adjusted free cash flow to shareholders in 2023 and 2024.

Operational Efficiencies

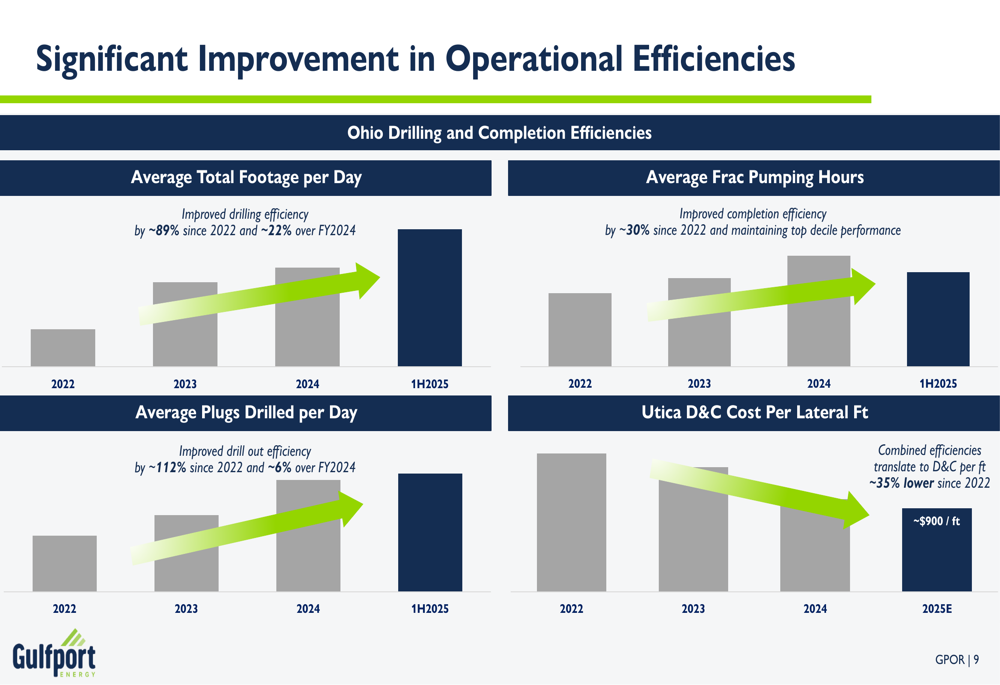

Gulfport has achieved significant operational improvements, particularly in its Ohio operations, which have translated to substantial cost reductions. The company reported an 89% improvement in average total footage drilled per day since 2022 and a 22% improvement over FY2024. Similarly, average plugs drilled per day improved by 112% since 2022.

These operational gains are illustrated in the following efficiency metrics:

These combined efficiencies have reduced drilling and completion costs per lateral foot by approximately 35% since 2022, to approximately $900/ft for 2025E. This cost reduction has been a key driver of the company’s free cash flow generation despite challenging natural gas prices.

In the liquids-rich areas, Gulfport is seeing strong results from its revised managed pressure flowback approach, which delivered approximately 65% greater cumulative oil volumes after 120 days compared to nearby developments:

Financial Outlook & Free Cash Flow Potential

Gulfport projects substantial free cash flow generation over the next five years, ranging from approximately $2.8 billion to $3.6 billion cumulatively from 2025-2029, depending on commodity price scenarios. This represents approximately 85-120% of the company’s current market capitalization.

The following chart details Gulfport’s adjusted free cash flow generation potential under different price scenarios:

These projections are based on low single-digit production growth of 0-5%, cash costs of $1.31-$1.43/Mcfe, and total capital expenditures of $370-$395 million annually. The company notes potential upside from improving base decline rates, reduced cycle times, and increased liquids production.

Financial Position

Gulfport maintains a strong balance sheet with $3.8 million in cash equivalents and approximately $885 million in liquidity as of Q2 2025. The company’s debt consists of $55 million in borrowings under its credit facility and $650 million of senior notes due 2029, resulting in a leverage ratio of approximately 0.85x.

The company’s capital structure and debt maturity profile are shown below:

This financial flexibility supports Gulfport’s capital allocation strategy, including its expanded $1.5 billion authorized equity repurchase program that now includes the redemption of preferred equity.

Forward-Looking Statements

For full-year 2025, Gulfport is guiding to total net production between 1.04-1.065 Bcfe/day, with liquids production between 18.0-20.5 MBbls/day. The company expects to incur capital expenditures between $370-$395 million, with approximately 83% allocated to Utica/Marcellus development, 10% to SCOOP, and 7% to land.

Management noted in the Q1 earnings call that "the rising natural gas curve over the next twelve months... position 2025 to be a transformative year for Gulfport from a cash flow perspective," according to CFO Michael Hodges. This optimism appears to be reflected in the company’s aggressive share repurchase program and preferred equity redemption plans.

While Gulfport’s presentation emphasizes its operational efficiencies and free cash flow generation, investors should note the company’s Q1 revenue miss and its continued dependence on natural gas market conditions. The company’s strategic shift toward dry gas development in the Utica, while maintaining liquids-rich opportunities, appears designed to maximize returns in the current commodity price environment while positioning for potential natural gas price improvements.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.