Palantir shares slip premarket despite posting record revenue in third quarter

Introduction & Market Context

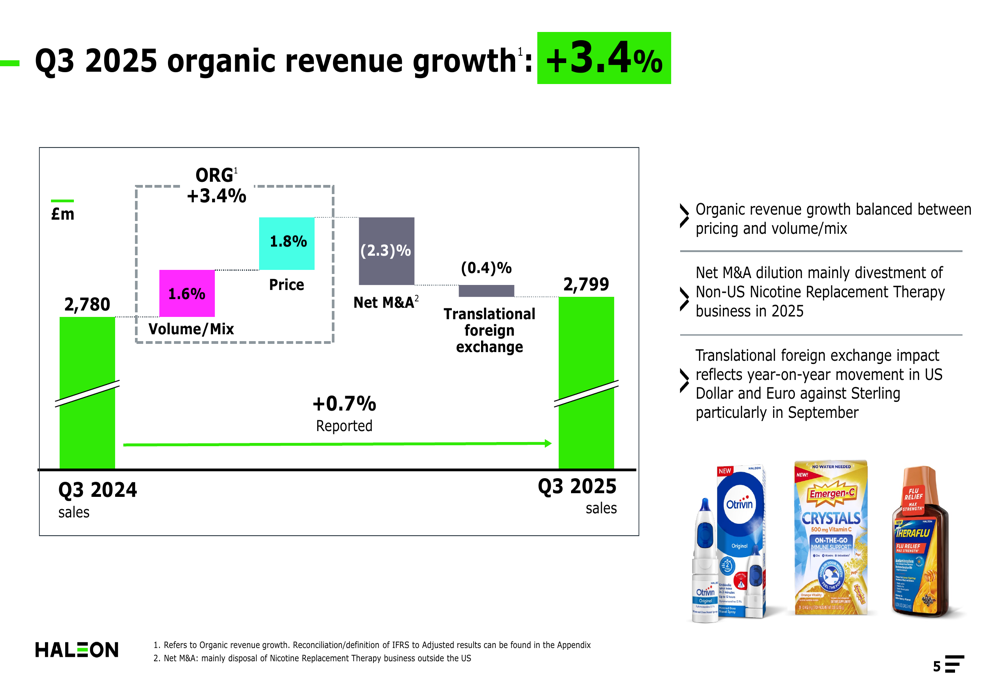

Haleon PLC ADR (NYSE:HLN) released its third-quarter 2025 trading statement on October 30, revealing 3.4% organic revenue growth despite challenges in key markets. The consumer healthcare giant reported revenue of £2.8 billion ($3.71 billion), slightly below analyst expectations of $3.72 billion, while earnings per share of $0.1167 missed forecasts by 7.45%.

The stock showed modest premarket activity, trading up 0.44% at $9.09, though it remains near its 52-week low of $8.71, reflecting cautious investor sentiment following the earnings miss.

Quarterly Performance Highlights

Haleon’s Q3 2025 organic revenue growth of 3.4% was balanced between pricing contributions (1.8%) and volume/mix (1.6%). However, reported revenue growth was limited to 0.7% due to a 2.3% dilution from net M&A activity—primarily from the divestment of the Non-US Nicotine Replacement Therapy business—and a 0.4% negative impact from foreign exchange movements.

As shown in the following breakdown of Q3 2025 organic revenue growth:

The company completed £500 million in share buybacks for fiscal year 2025, with approximately £1.1 billion returned to shareholders during the year. Despite the earnings miss, Haleon maintained its full-year guidance of around 3.5% organic revenue growth and high-single-digit organic operating profit growth.

Regional Performance Analysis

Haleon’s performance varied significantly across regions, with North America showing particular weakness while emerging markets demonstrated robust growth.

North America, representing 35% of Q3 revenue (£977 million), delivered just 0.4% organic growth with pricing contributing 0.7% while volume/mix declined by 0.3%. This underperformance aligns with management’s commentary about challenges in the region, though the company highlighted continued strength in Oral Health and low-single-digit growth in the Vitamins, Minerals & Supplements (VMS) category.

As illustrated in the North America performance summary:

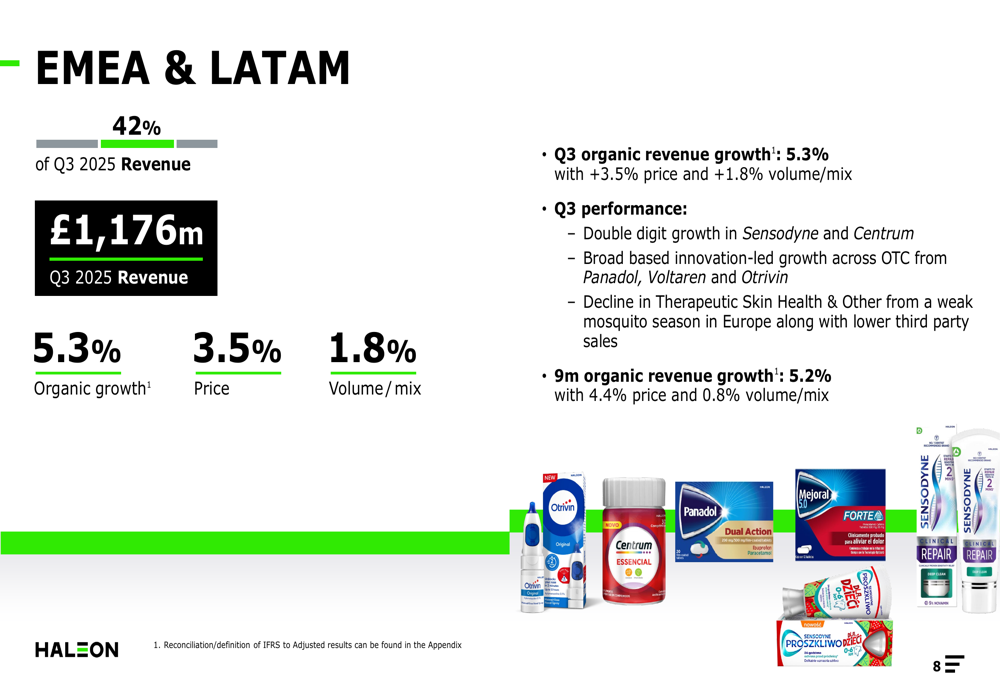

In contrast, EMEA & LATAM markets, accounting for 42% of Q3 revenue (£1,176 million), showed strong 5.3% organic growth with balanced contributions from both pricing (3.5%) and volume/mix (1.8%). The region benefited from double-digit growth in Sensodyne and Centrum brands, along with broad-based innovation-led growth in over-the-counter products.

The following chart details EMEA & LATAM performance:

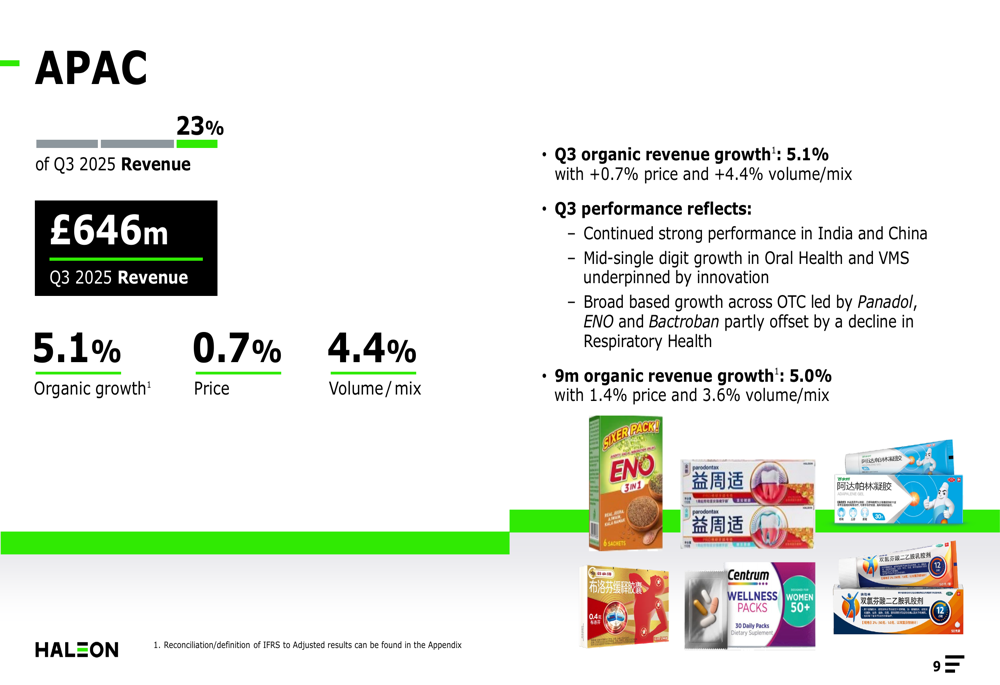

The Asia-Pacific region, representing 23% of Q3 revenue (£646 million), also demonstrated robust performance with 5.1% organic growth, primarily driven by volume/mix (4.4%) with modest pricing contributions (0.7%). India and China continued to be standout markets, with mid-single-digit growth across Oral Health and VMS categories.

As shown in the APAC performance summary:

Category Performance Breakdown

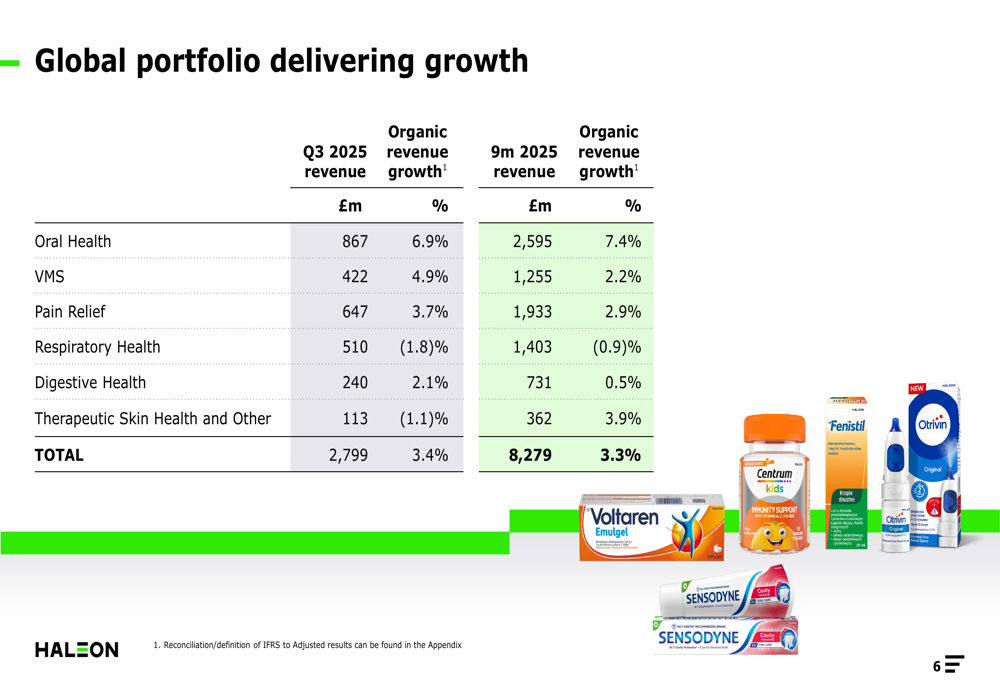

Haleon’s product portfolio showed varied performance across categories, with Oral Health emerging as the clear leader. The category, which includes brands like Sensodyne and Aquafresh, delivered 6.9% organic growth in Q3 2025, generating £867 million in revenue.

Other strong performers included VMS with 4.9% growth (£422 million revenue) and Pain Relief with 3.7% growth (£647 million revenue). However, Respiratory Health declined by 1.8% to £510 million, reflecting challenges from previous year comparisons when COVID cases were more prevalent.

The following table illustrates the performance across Haleon’s global portfolio:

Forward-Looking Statements

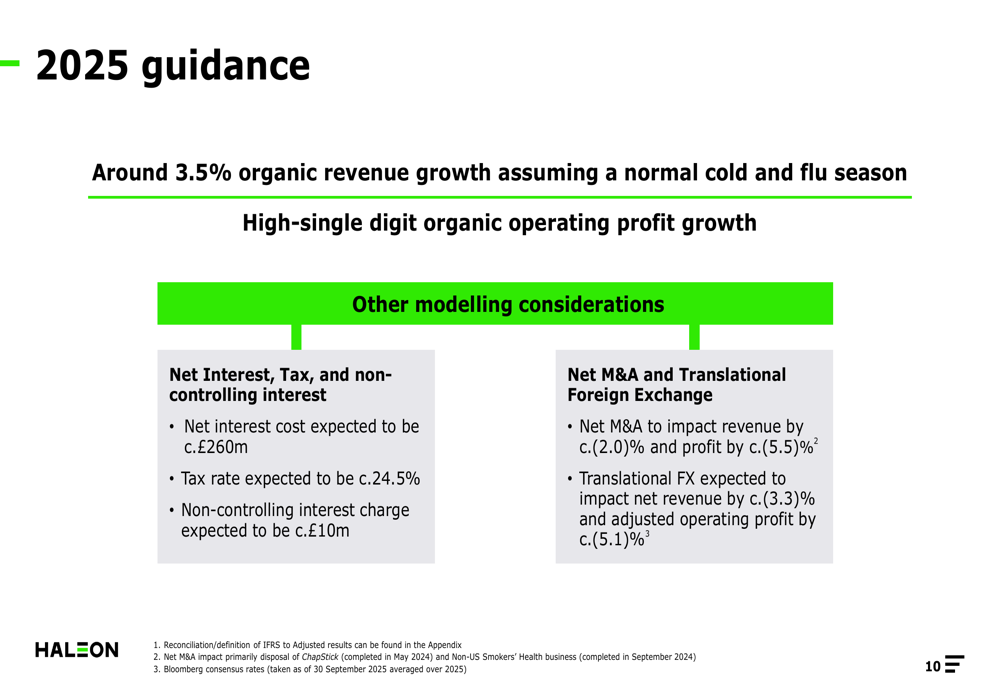

Despite the Q3 earnings miss, Haleon maintained its full-year 2025 guidance of approximately 3.5% organic revenue growth, assuming a normal cold and flu season, and high-single-digit organic operating profit growth.

The company expects net interest costs of around £260 million, a tax rate of approximately 24.5%, and a non-controlling interest charge of about £10 million. Management anticipates net M&A activity to impact revenue by approximately -2.0% and profit by around -5.5%, while translational foreign exchange is expected to affect net revenue by -3.3% and adjusted operating profit by -5.1%.

As detailed in the 2025 guidance slide:

CFO Dawn Allen expressed confidence in the company’s trajectory, stating, "We delivered 3.4% organic revenue growth in the quarter, with a good balance between price at 1.8% and volume mix of 1.6%." She highlighted actions being taken in the US market to set up growth for next year and emphasized the company’s focus on building flexibility and agility in the P&L through productivity savings.

Haleon’s management remains confident in delivering on its value creation framework and medium-term guidance despite the near-term challenges, particularly in North America. The company expects North American operations to return to growth in 2026 while continuing to capitalize on strong momentum in emerging markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.