S&P 500 pares some losses as Fed cuts rates; Powell eyed

Introduction & Market Context

Halliburton Company (NYSE:HAL) recently presented its second quarter 2025 results, highlighting international growth and strong cash flow generation despite missing earnings expectations. The oilfield services giant reported revenue of $5.51 billion, exceeding forecasts of $5.41 billion, while posting earnings per share of $0.55, slightly below the anticipated $0.56.

The company’s stock reacted negatively to the earnings miss, declining 2.46% in pre-market trading following the announcement, though it has since recovered slightly to $21.35. With a current P/E ratio of 8.77x, Halliburton appears undervalued according to some analysts, despite facing challenges in certain markets.

Quarterly Performance Highlights

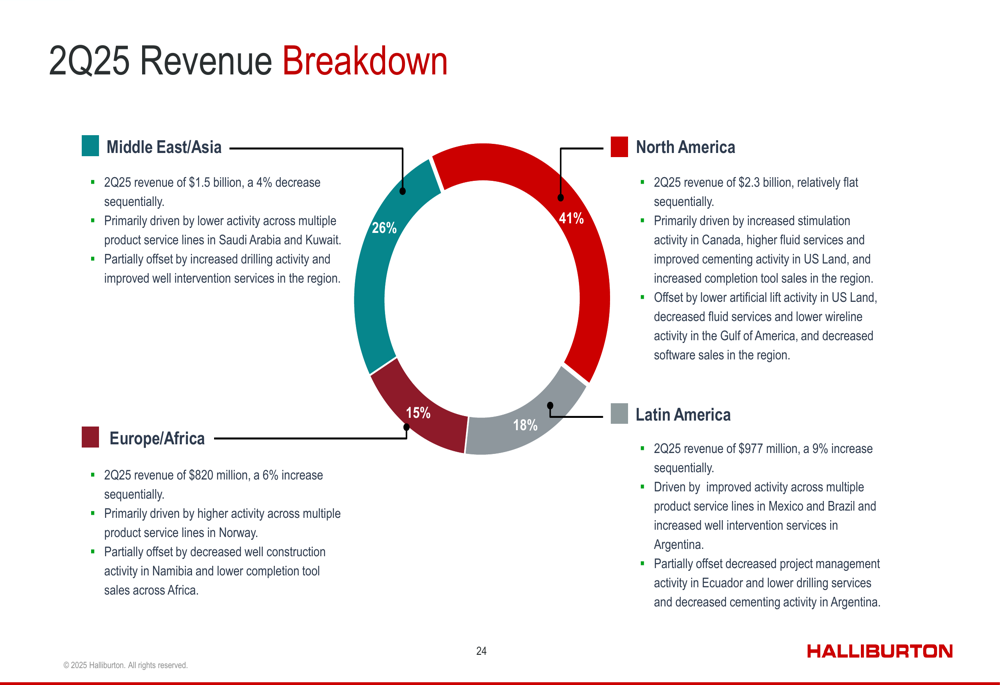

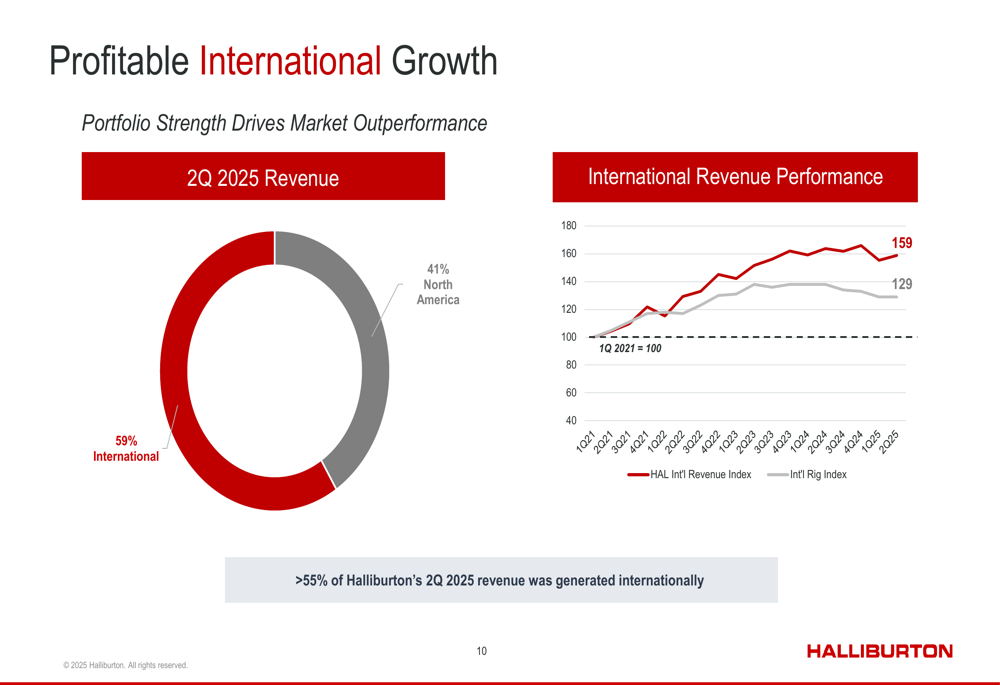

Halliburton’s Q2 2025 revenue breakdown shows varying performance across regions, with international operations now accounting for 59% of total revenue compared to 41% from North America. This shift reflects the company’s strategic focus on international growth.

As shown in the following regional revenue breakdown:

North American revenue remained relatively flat sequentially at $2.3 billion, while international markets showed mixed results. Latin America delivered the strongest performance with a 9% sequential increase to $977 million, followed by Europe/Africa with a 6% increase to $820 million. However, the Middle East/Asia region experienced a 4% sequential decrease to $1.5 billion.

The company’s international revenue has significantly outpaced international rig count growth since Q1 2021, as illustrated in this performance chart:

CEO Jeff Miller emphasized the company’s resilience during the earnings call, stating: "Despite industry cycles, I believe the demand fundamentals remain strong for both oil and gas." He also highlighted Halliburton’s technology advantages as a key differentiator in the market.

Strategic Priorities & Technology Investments

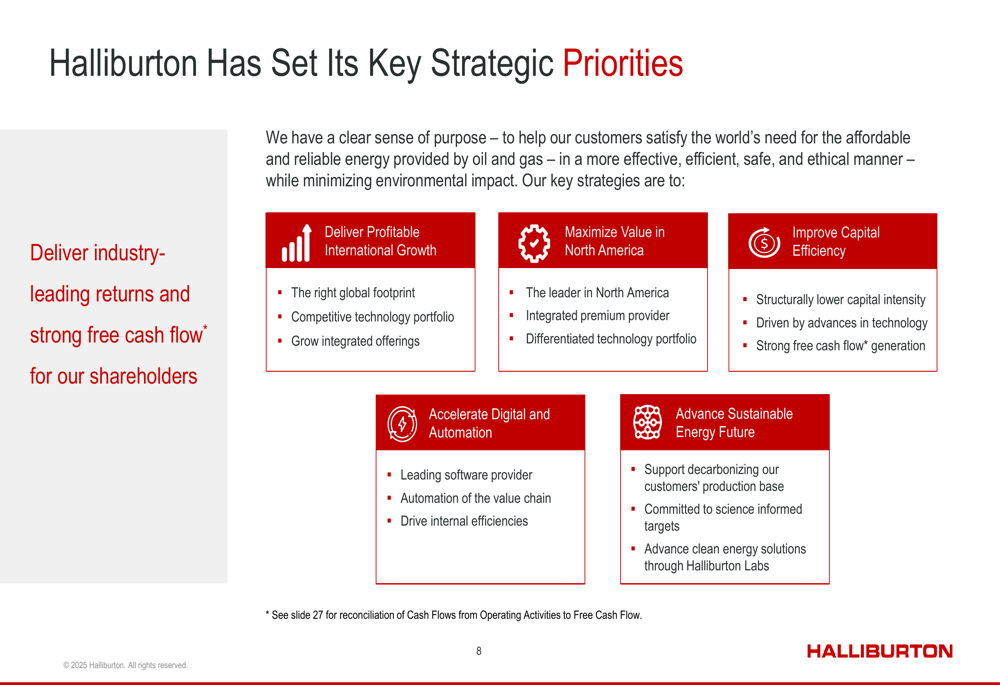

Halliburton outlined five key strategic priorities that guide its operations and investments:

The company continues to invest in innovative technologies that drive operational efficiency and sustainability. Notable among these are the Zeus™ Electric Fracturing System, which reduces emissions and operating costs, and the Sensori™ Fracture Monitoring Service, which optimizes fracture effectiveness through continuous subsurface feedback.

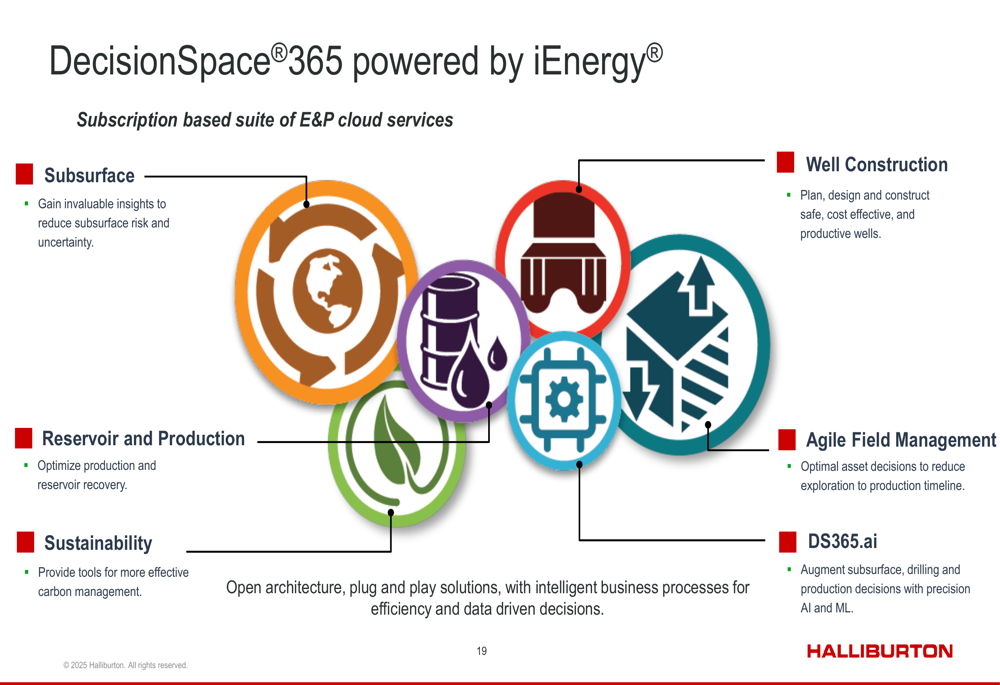

Digital transformation remains a priority, with the company’s DecisionSpace®365 platform providing integrated solutions across the energy value chain:

Environmental sustainability is increasingly central to Halliburton’s strategy, with a commitment to reduce Scope 1 and Scope 2 emissions by 40% by 2035 from its 2018 baseline. This aligns with the industry’s broader shift toward lower-carbon operations while maintaining energy reliability.

Capital Efficiency & Shareholder Returns

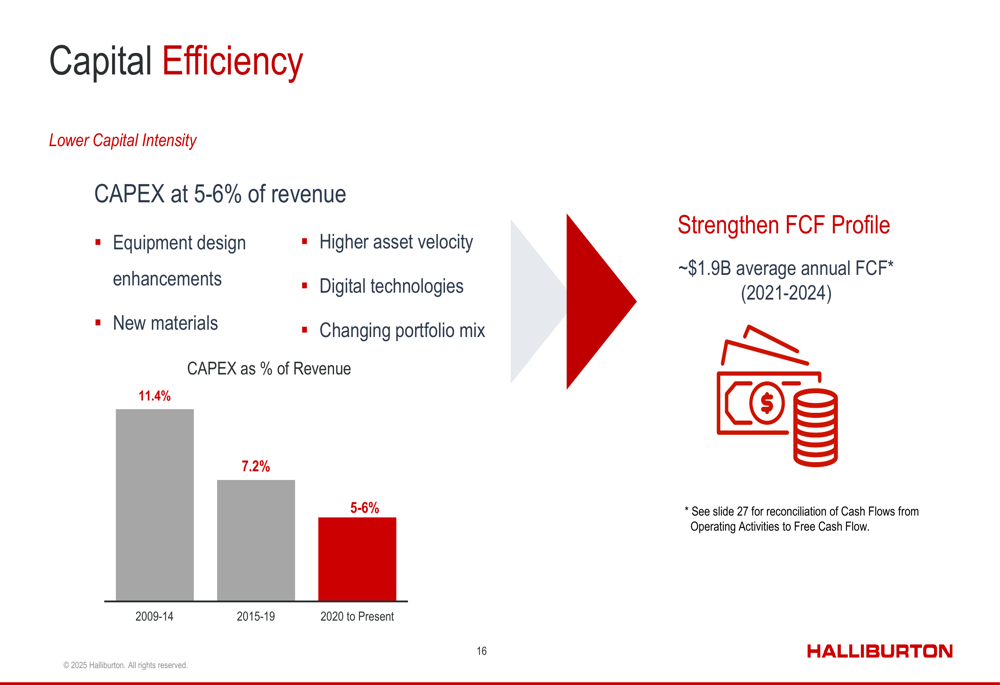

A standout aspect of Halliburton’s presentation was its improved capital efficiency, with capital expenditures maintained at 5-6% of revenue, down significantly from 11.4% during 2009-2014. This structural reduction has strengthened free cash flow generation.

The following chart illustrates this trend:

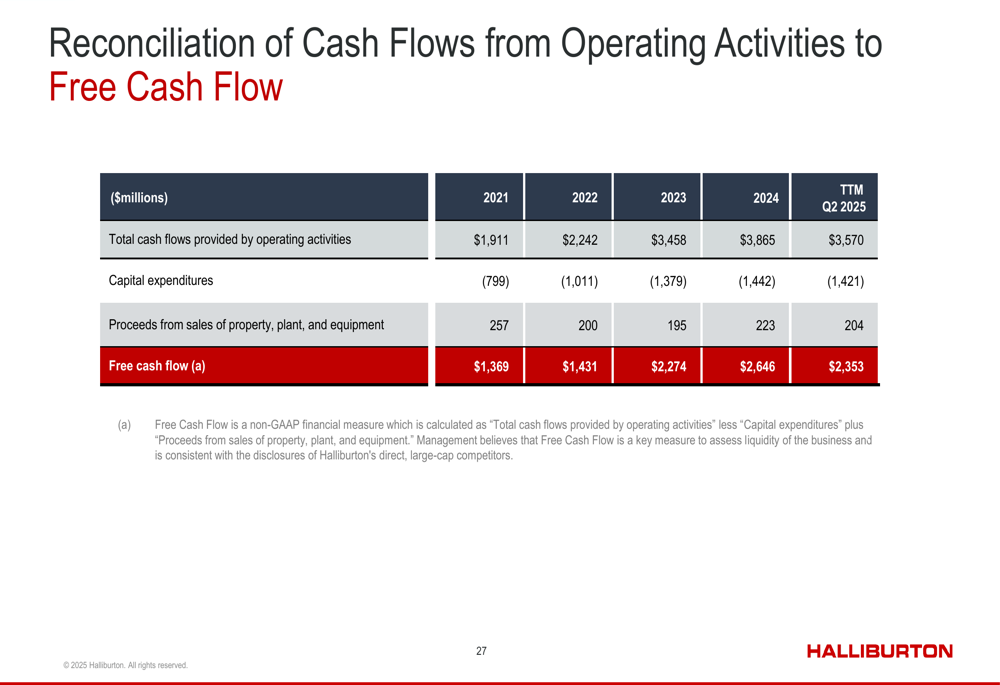

For the trailing twelve months ending Q2 2025, Halliburton generated $2.35 billion in free cash flow, calculated as follows:

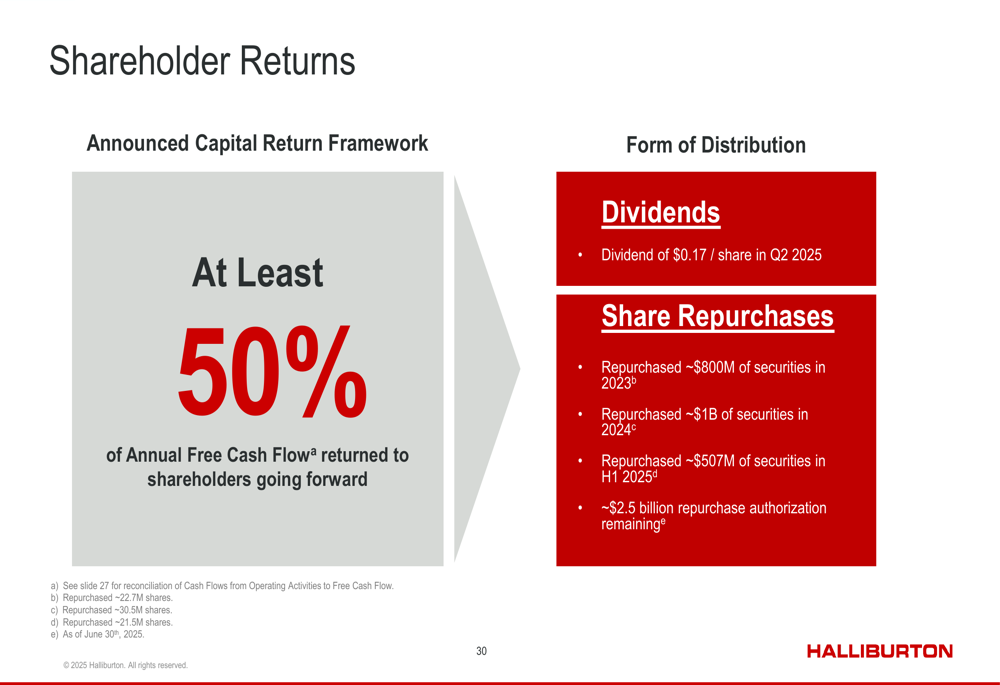

This strong cash flow supports Halliburton’s commitment to return at least 50% of annual free cash flow to shareholders through dividends and share repurchases:

The company maintained its quarterly dividend at $0.17 per share for Q2 2025 and continued its share repurchase program, buying back approximately $507 million in securities during the first half of 2025. This follows repurchases of approximately $1 billion in 2024 and $800 million in 2023, with $2.5 billion in repurchase authorization still remaining.

Forward-Looking Statements

Despite the positive cash flow and international growth, Halliburton faces challenges in the near term. Management projects a decrease in revenue for both its Completion and Production and Drilling and Evaluation divisions in Q3 2025, with an expected decline of 1-3%. The company anticipates relatively flat revenue in Q4 2025.

Key risks identified include volatile commodity markets influenced by trade uncertainties, OPEC+ production cuts impacting market dynamics, and economic returns pressure on equipment utilization. These factors may explain the cautious outlook despite the company’s strong financial position.

Nevertheless, Halliburton remains confident in its competitive positioning as "the only integrated services company with a strong presence in both North America and International markets." The company’s focus on technology differentiation, operational execution, and financial discipline is expected to support long-term performance even amid market volatility.

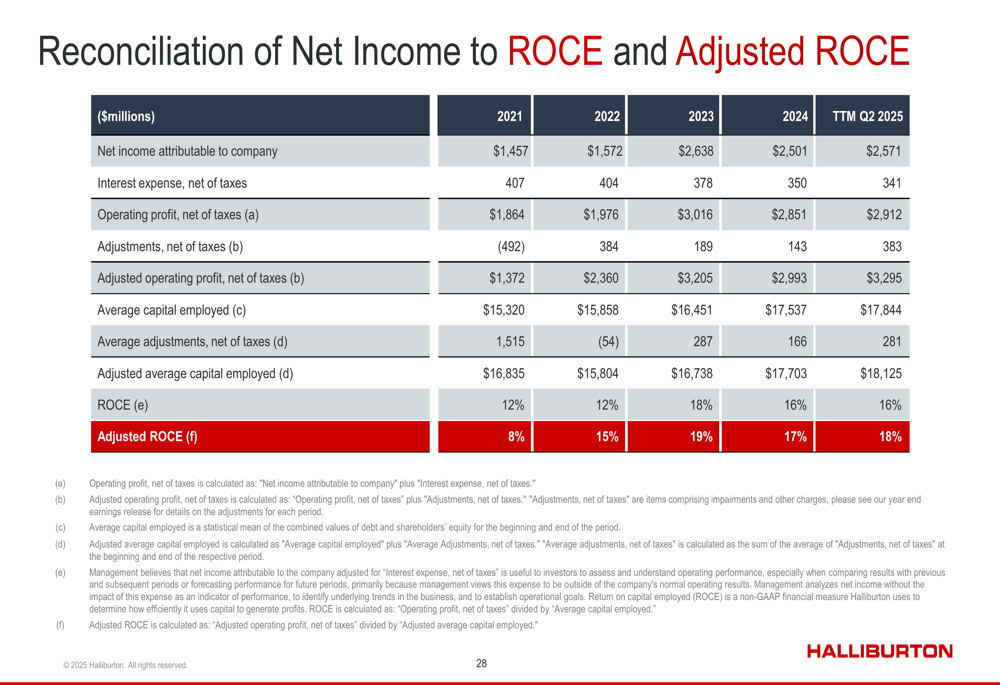

With an adjusted return on capital employed of 18% for the trailing twelve months ending Q2 2025, Halliburton continues to demonstrate strong operational efficiency despite the challenging market environment.

As the company navigates these challenges, its global footprint across more than 70 countries and diverse service portfolio position it to capitalize on opportunities in both traditional and emerging energy markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.