Stock market today: S&P 500 extends monthly win streak despite Nvidia-led stumble

Introduction & Market Context

Hamilton Lane (NASDAQ:HLNE) presented its fiscal year 2025 fourth quarter and full-year results on May 29, 2025, revealing strong performance across all key financial metrics. The alternative investment management firm reported significant growth in assets under management, fee revenue, and profitability, continuing its multi-year expansion trajectory.

The company’s shares closed at $175.49 on May 28, 2025, up 1.67% ahead of the earnings presentation, and have traded between $114.85 and $203.72 over the past 52 weeks.

Financial Performance Highlights

Hamilton Lane reported substantial growth across all major financial metrics for fiscal year 2025, with particularly strong performance in net income and earnings per share.

As shown in the following comprehensive financial summary:

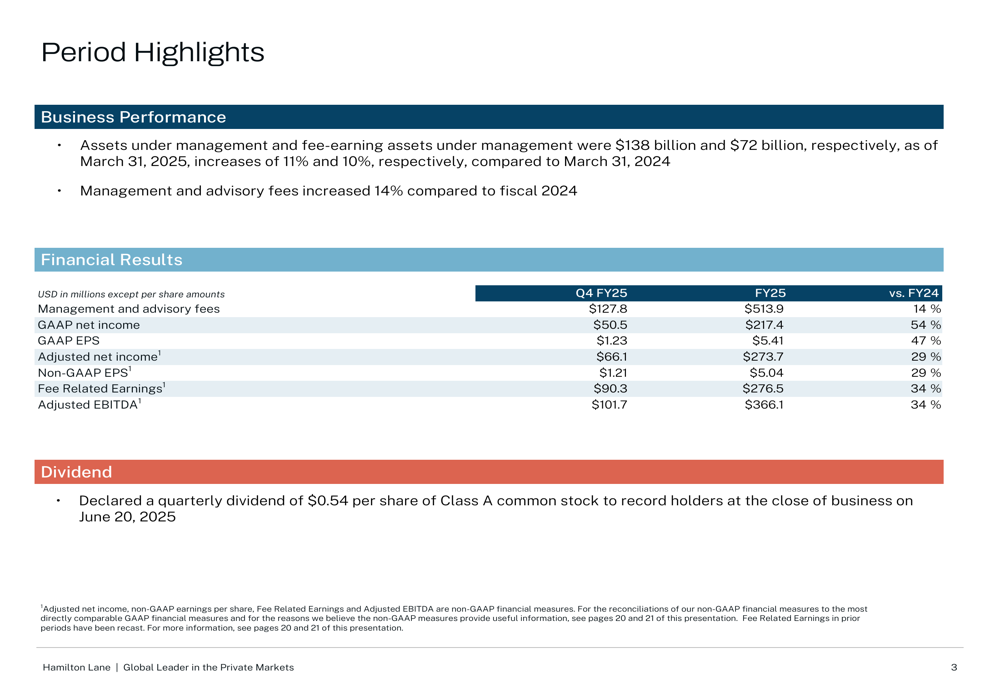

The company’s assets under management reached $138 billion as of March 31, 2025, representing an 11% increase compared to the previous year. Fee-earning assets under management grew to $72 billion, up 10% year-over-year. Management and advisory fees increased by 14% to $513.9 million compared to fiscal 2024.

GAAP net income saw a remarkable 54% jump to $217.4 million, while GAAP earnings per share rose 47% to $5.41. Adjusted net income increased 29% to $273.7 million, with non-GAAP EPS also growing 29% to $5.04. Fee Related Earnings and Adjusted EBITDA both increased by 34% to $276.5 million and $366.1 million, respectively.

The company also declared a quarterly dividend of $0.54 per share of Class A common stock, payable to shareholders of record as of June 20, 2025.

Asset Growth and Management

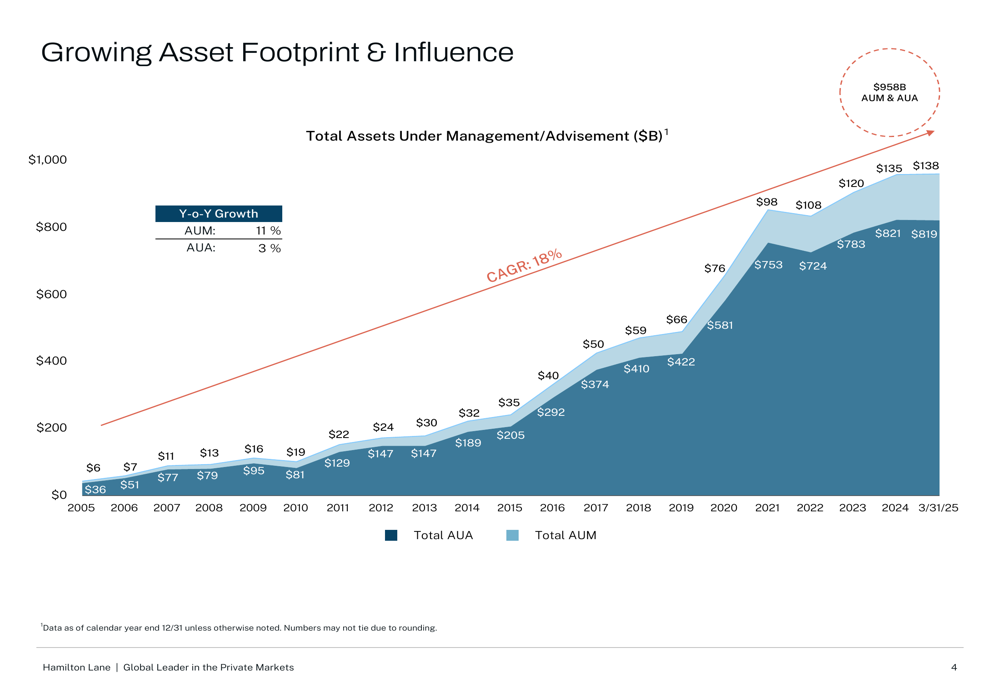

Hamilton Lane’s total asset footprint has shown consistent growth over the past two decades, approaching the $1 trillion mark. The following chart illustrates this impressive trajectory:

Total (EPA:TTEF) assets under management and advisement reached $958 billion as of March 31, 2025. The company achieved year-over-year growth of 11% in AUM and 3% in AUA, maintaining a compound annual growth rate of 18% over the long term.

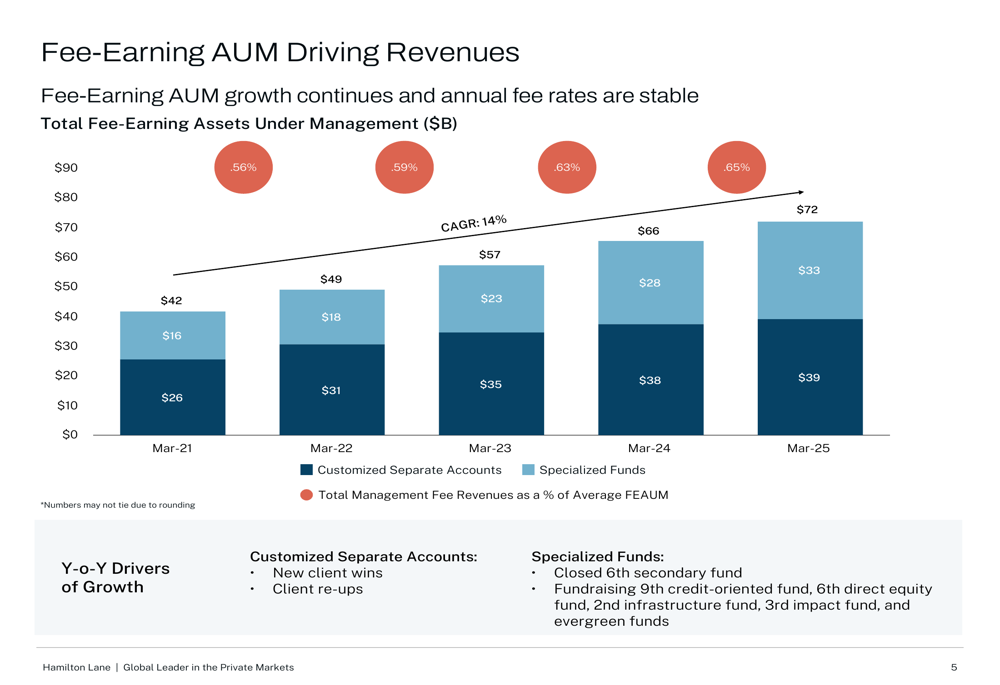

Fee-earning assets under management, a critical driver of the company’s recurring revenue, have also shown steady growth:

Fee-earning AUM increased from $66 billion in March 2024 to $72 billion in March 2025, continuing a consistent upward trend from $42 billion in March 2021. Importantly, the company has maintained stable fee rates, with total management fee revenues as a percentage of average FEAUM rising slightly to 0.65% in FY25 from 0.63% in FY24.

The growth in fee-earning assets was driven by both customized separate accounts and specialized funds. The company closed its sixth secondary fund and is currently fundraising for several other vehicles, including its ninth credit-oriented fund, sixth direct equity fund, second infrastructure fund, third impact fund, and various evergreen funds.

Revenue and Earnings Analysis

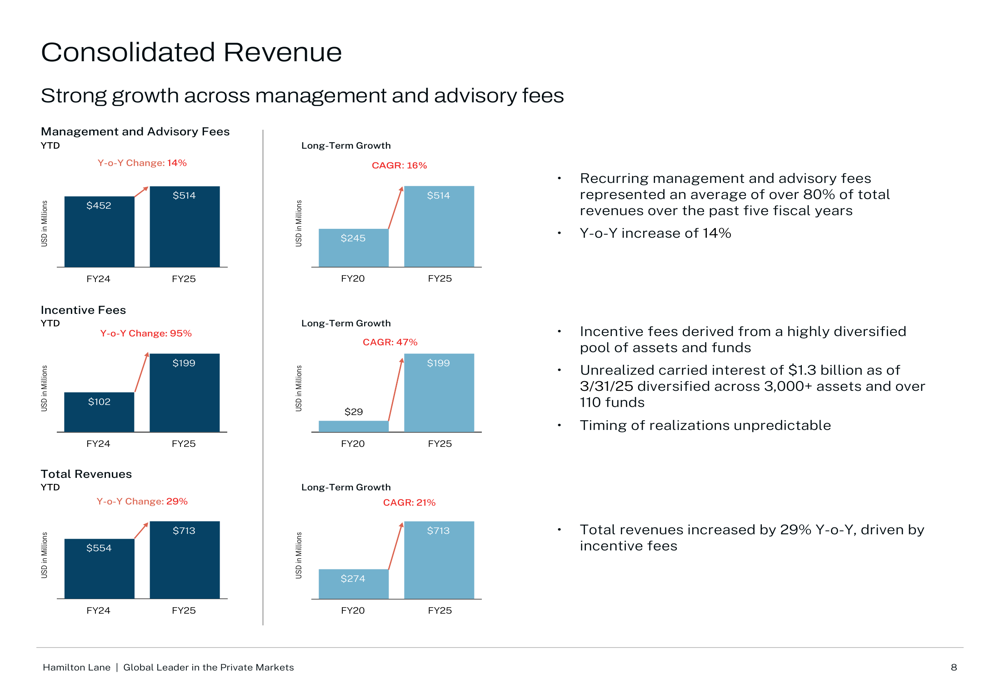

Hamilton Lane’s revenue streams showed robust growth across both management and advisory fees and incentive fees:

Management and advisory fees, which represent the company’s most stable revenue source, grew 14% year-over-year to $514 million in FY25. These recurring fees have demonstrated impressive long-term growth with a 16% CAGR from FY20 to FY25.

Incentive fees nearly doubled, increasing 95% year-over-year to $199 million, driven by a diversified pool of assets and funds. The company’s total revenues increased 29% to $713 million, with a five-year CAGR of 21%.

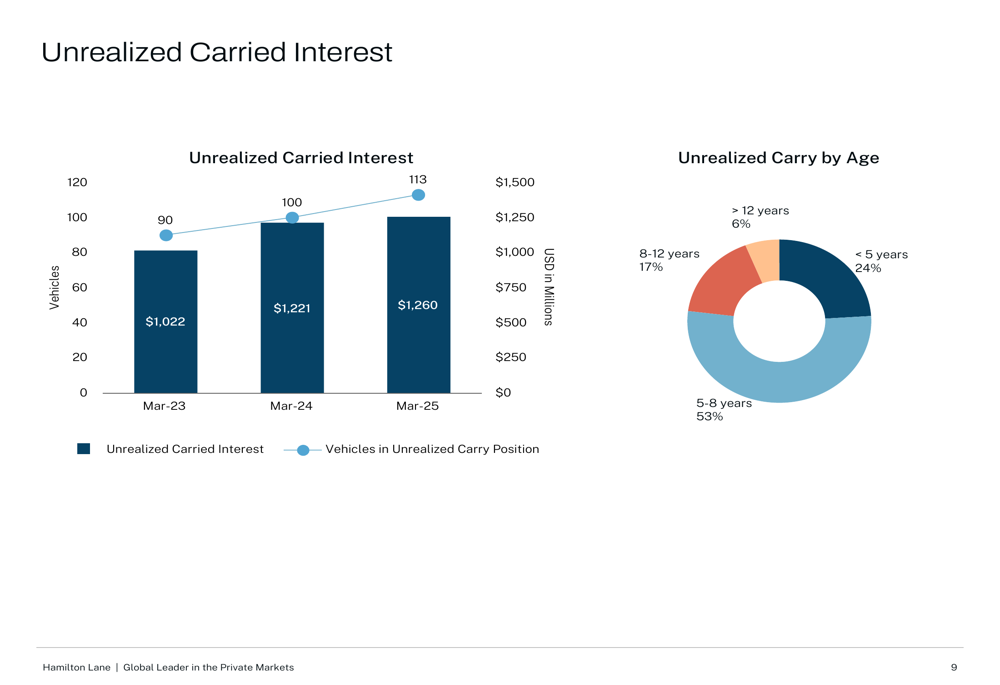

The company’s unrealized carried interest, which represents potential future revenue, continues to grow:

Unrealized carried interest reached $1.26 billion as of March 2025, up from $1.22 billion a year earlier. The number of vehicles in an unrealized carry position increased to 113, up from 100 in March 2024. The age distribution of this carried interest is well-balanced, with 77% being less than 8 years old, indicating significant future revenue potential.

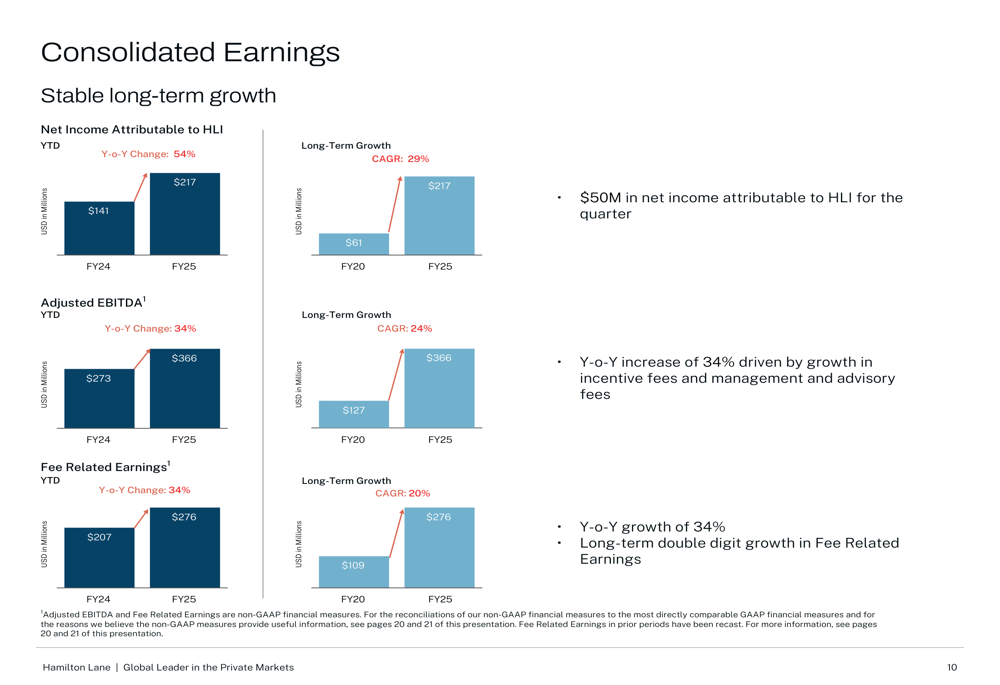

Hamilton Lane’s consolidated earnings showed equally impressive growth:

Net income attributable to Hamilton Lane Incorporated surged 54% year-over-year to $217 million, with a long-term CAGR of 29% from FY20 to FY25. Adjusted EBITDA and Fee Related Earnings both increased by 34% to $366 million and $276 million, respectively, continuing their double-digit long-term growth trajectories.

Balance Sheet and Investment Position

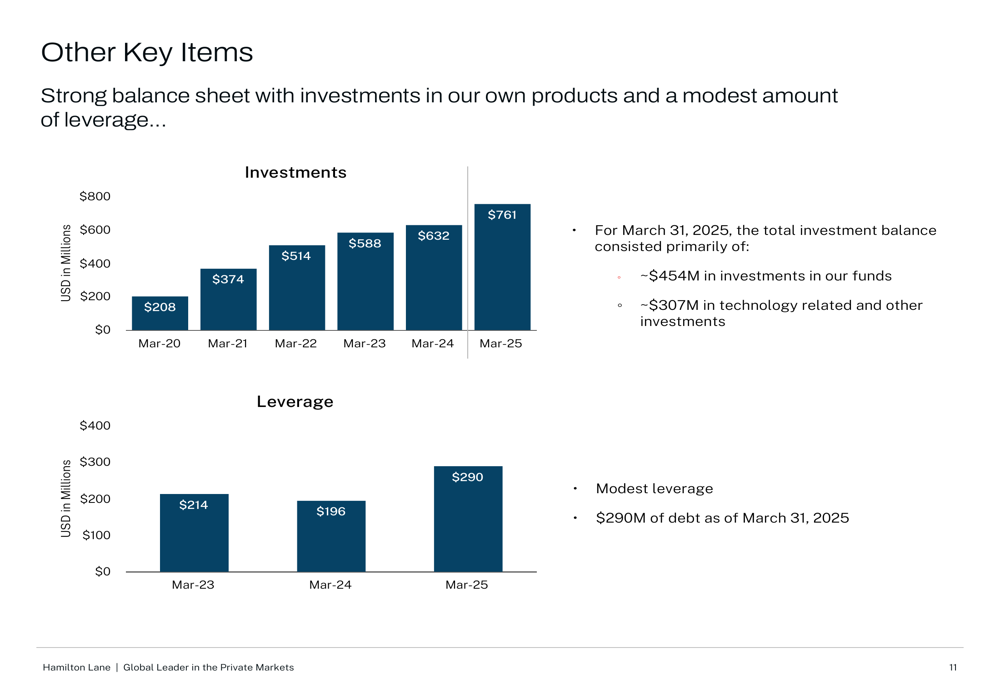

The company has maintained a strong balance sheet while growing its investment portfolio:

Hamilton Lane’s investments increased to $761 million as of March 31, 2025, up from $632 million a year earlier and continuing a steady growth trend from $208 million in March 2020. This investment balance consists primarily of approximately $454 million in investments in the company’s own funds and $307 million in technology-related and other investments.

The company maintains modest leverage, with $290 million of debt as of March 31, 2025, an increase from $196 million in the previous year but still at manageable levels relative to the company’s earnings and investment portfolio.

Strategic Initiatives

Hamilton Lane’s growth strategy continues to focus on three key areas: customized separate accounts, specialized funds, and advisory services.

Customized separate accounts saw a $1.8 billion year-over-year increase in fee-earning AUM, with over 80% of gross contributions in the last 12 months coming from existing clients, demonstrating strong client retention and satisfaction.

Specialized funds contributed a $4.5 billion year-over-year increase in fee-earning AUM. The company continues to diversify its fund offerings across various strategies, including direct equity, credit, infrastructure, impact, and evergreen funds.

Advisory services, which typically serve larger clients with wide-ranging mandates, generated a $23.3 billion year-over-year increase in assets under advisement. These services include technology-driven reporting, monitoring, and analytics, aligning with the company’s previous strategic investments in technology mentioned in earlier earnings reports.

Forward Outlook

While the presentation did not provide specific forward guidance, Hamilton Lane’s consistent growth across all key metrics positions the company well for continued expansion. The significant increase in unrealized carried interest ($1.26 billion) across 113 vehicles provides visibility into potential future revenue streams.

The company’s diversified business model, with revenue coming from management and advisory fees, incentive fees, and a growing investment portfolio, offers multiple growth drivers. The strong client retention rate, with over 80% of contributions coming from existing clients, suggests continued stability in the company’s core business.

Hamilton Lane’s FY25 results represent a significant improvement over FY24, when the company reported 22% growth in management and advisory fees, GAAP EPS of $3.69, and non-GAAP EPS of $3.92. The acceleration in earnings growth and continued expansion of assets under management demonstrate the company’s strengthening market position in the alternative investment management industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.