BofA update shows where active managers are putting money

Introduction & Market Context

Hancock Whitney Corporation (NASDAQ:HWC) reported its first quarter 2025 results on April 15, showcasing solid performance despite some growth challenges. The bank, with a market capitalization of $4.5 billion, saw its stock rise 2.23% to $48.7 in aftermarket trading following the announcement, reflecting positive investor sentiment despite mixed operational results.

The company’s earnings presentation revealed a strong financial foundation with top-tier capital ratios, even as it navigates a complex economic environment characterized by softer loan demand and increased payoffs in certain sectors. Management emphasized the bank’s 125-year history of stability and outlined strategic initiatives focused on expansion in high-growth markets.

Quarterly Performance Highlights

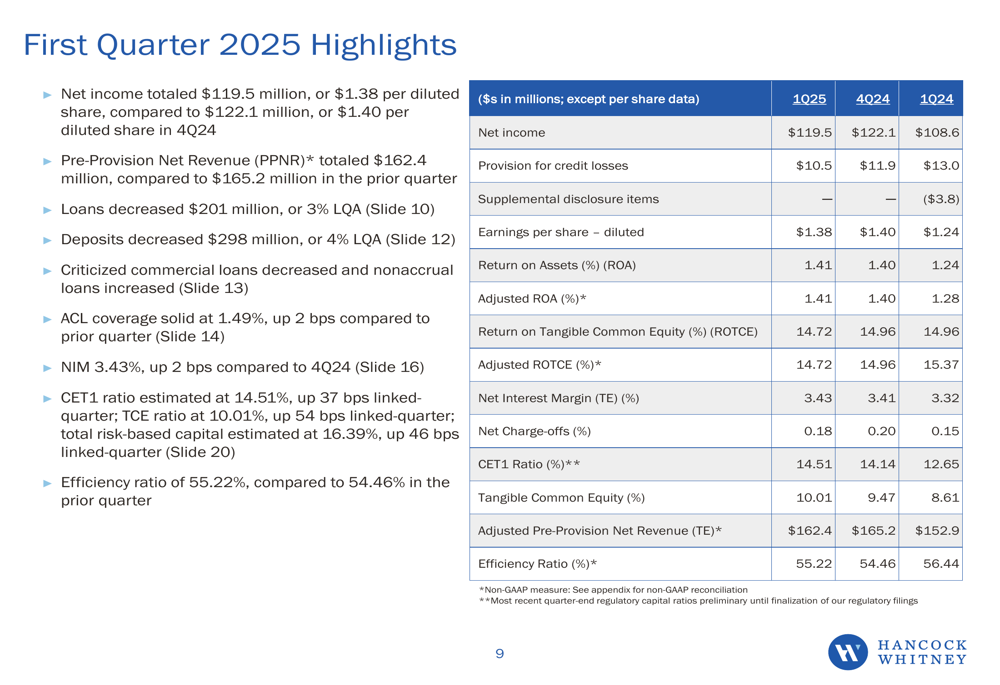

Hancock Whitney reported net income of $119.5 million for Q1 2025, translating to $1.38 per diluted share, which exceeded analyst expectations of $1.29. Pre-provision net revenue (PPNR) reached $162.4 million, while the company maintained strong capital metrics with a CET1 ratio of 14.51% and tangible common equity ratio of 10.01%.

As shown in the following quarterly highlights summary:

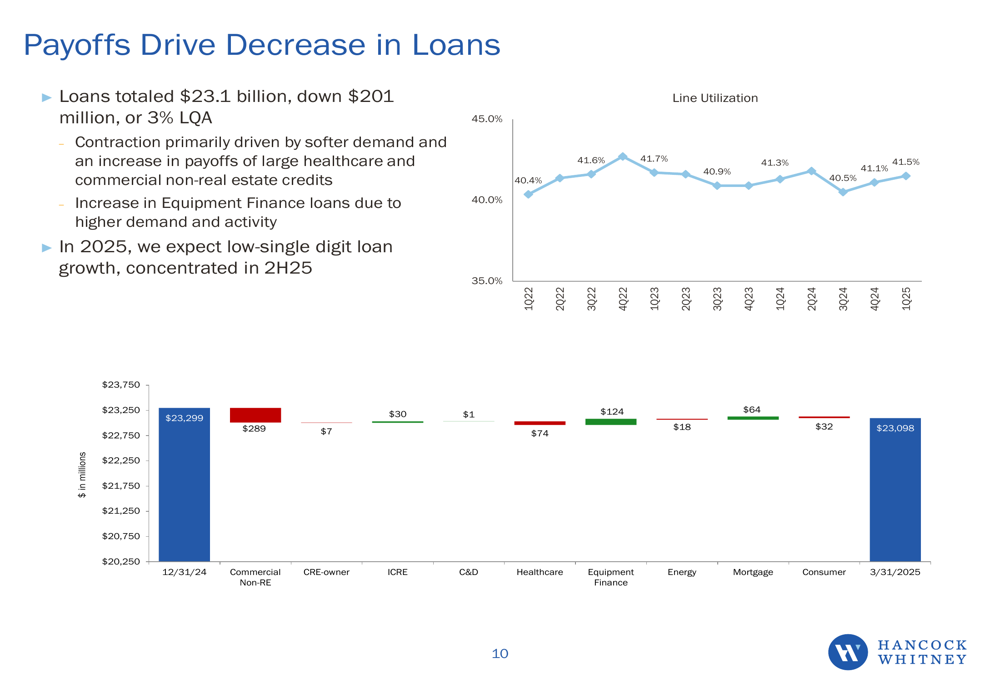

Despite the earnings beat, the bank faced some headwinds in the quarter. Total (EPA:TTEF) loans decreased by $201 million, primarily due to softer demand and increased payoffs in healthcare and commercial real estate sectors. Similarly, deposits declined by $298 million, though management noted this was largely driven by seasonal public funds outflows.

The company’s net interest margin (NIM) stood at 3.43%, while its efficiency ratio was reported at 55.22%, indicating reasonable operational efficiency. The allowance for credit losses remained robust at 1.49% of total loans, reflecting the bank’s conservative risk management approach.

Strategic Initiatives

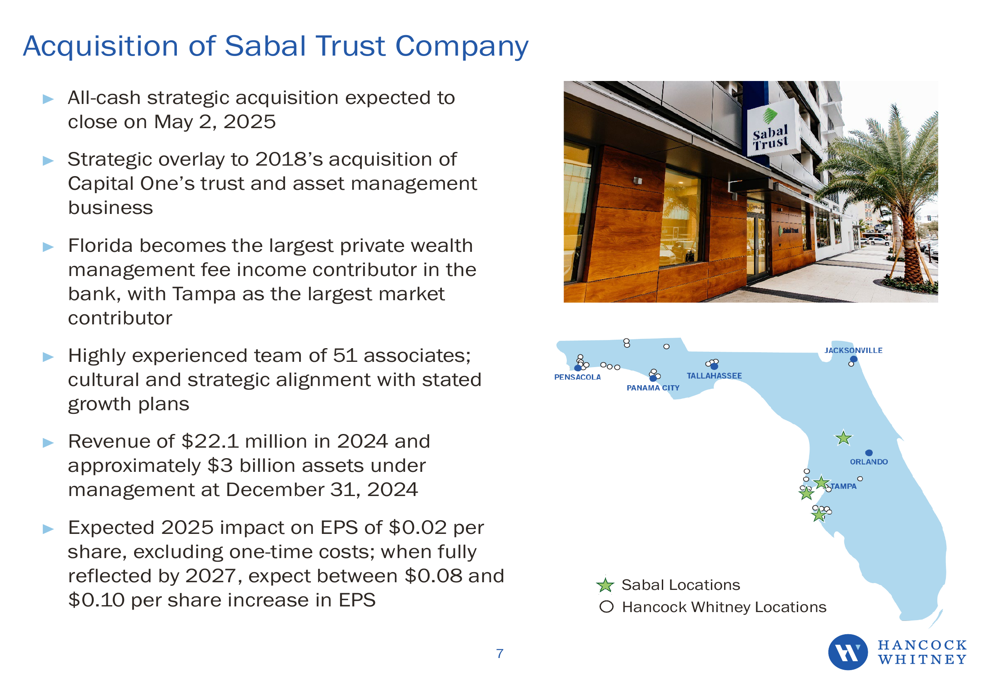

A centerpiece of Hancock Whitney’s strategic vision is the pending acquisition of Sabal Trust Company, an all-cash transaction expected to close on May 2, 2025. This acquisition represents a significant expansion of the bank’s wealth management capabilities in Florida, as illustrated in the following slide:

Sabal Trust generated $22.1 million in revenue in 2024 and managed $3 billion in assets as of December 31, 2024. Management projects the acquisition will contribute $0.02 to EPS in 2025, growing to $0.08-$0.10 by 2027, making Florida the largest private wealth management fee income contributor for the bank.

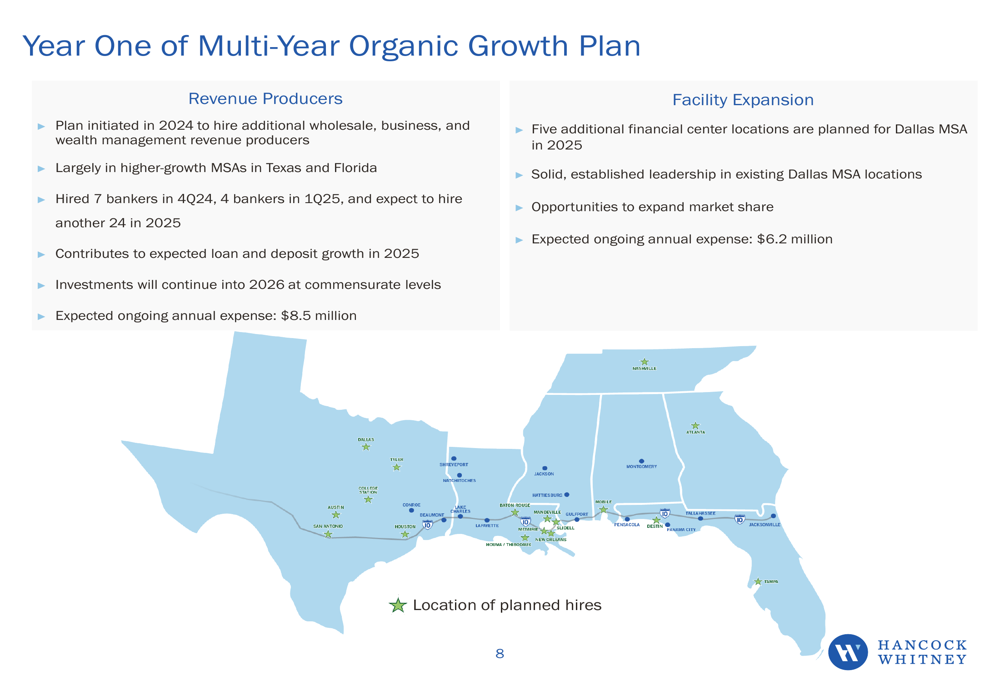

In addition to this acquisition, Hancock Whitney outlined its organic growth initiatives, focusing on expanding its presence in Texas and Florida:

The company has already hired 7 bankers in Q4 2024 and 4 in Q1 2025, with plans to add 24 more revenue producers throughout 2025. Management also announced plans for five additional financial centers in the Dallas metropolitan area this year, representing an ongoing annual expense of $6.2 million.

Detailed Financial Analysis

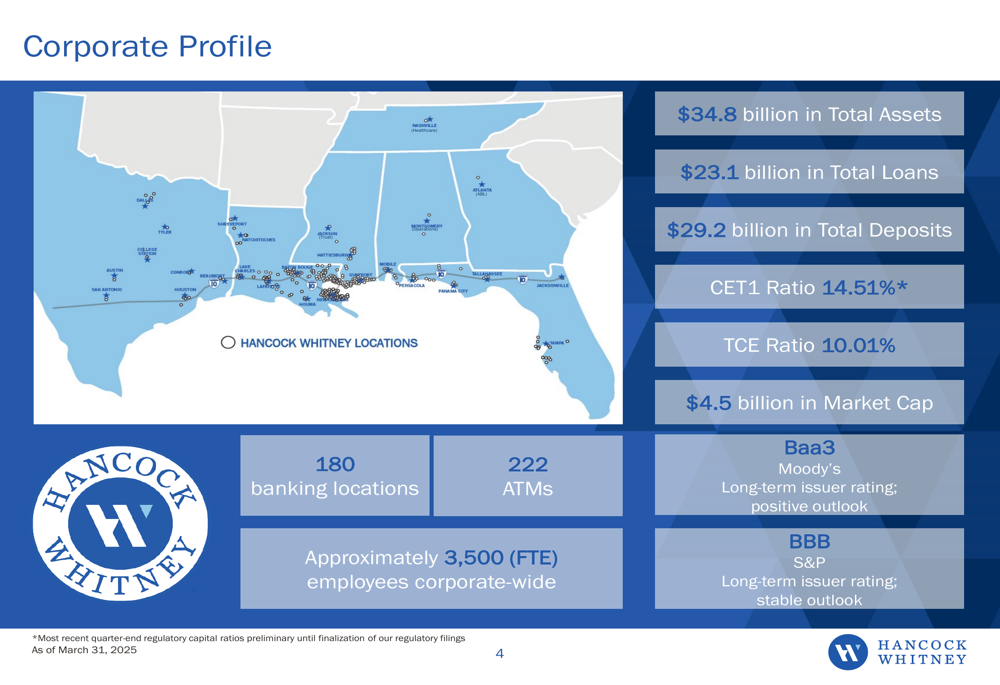

Hancock Whitney’s corporate profile reveals a substantial regional banking presence with $34.8 billion in total assets, $23.1 billion in loans, and $29.2 billion in deposits. The bank operates 180 banking locations and 222 ATMs across its footprint, employing approximately 3,500 people.

The loan portfolio analysis reveals that Commercial Non-Real Estate loans constitute the largest segment at nearly $10 billion. The decrease in loans during Q1 was primarily attributed to higher payoffs, particularly in healthcare and commercial real estate sectors, while Equipment Finance loans showed growth due to higher demand.

Management expects low single-digit loan growth for 2025, with most of the growth anticipated in the second half of the year. This represents a moderation from previous guidance, reflecting current market uncertainties and client sentiment.

Forward-Looking Statements

Hancock Whitney emphasized several strengths that position the bank for continued stability and growth, including top quartile capital levels, a de-risked balance sheet, proactive expense management, and ongoing technology investments to enhance client experience.

For 2025, management projects:

- Low single-digit loan growth, concentrated in the second half of the year

- 6-7% growth in Pre-tax Pre-provision Net Revenue

- Fee income growth of 9-10% year-over-year (updated to reflect the Sabal Trust acquisition)

- Expense growth of 4-5% year-over-year

- Modest net interest margin expansion

The company continues to return capital to shareholders through share repurchases (350,000 shares in Q1) and recently increased its common stock dividend to $0.45 per share, representing a 50% increase from the previous year.

Conclusion

Hancock Whitney’s Q1 2025 presentation portrays a bank with solid financial fundamentals and a clear strategic vision, despite facing some growth challenges in the current economic environment. The company’s strong capital position provides flexibility to pursue both strategic acquisitions and organic growth initiatives while continuing to return capital to shareholders.

The Sabal Trust acquisition and targeted expansion in high-growth markets like Texas and Florida demonstrate management’s commitment to diversifying revenue streams and building long-term value. While loan growth remains a challenge in the near term, the bank’s focus on relationship banking and strategic hiring suggests potential for improved performance in the latter half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.