Commerce launches BigCommerce Payments powered by PayPal for 2026

Introduction & Market Context

HELLA, a part of the FORVIA Group, presented its H1 2025 financial results on July 25, 2025, showing relatively stable performance despite challenging market conditions. The presentation comes as parent company Forvia saw its stock surge 11.68% following the broader group’s earnings announcement, closing at €11.58 on July 28.

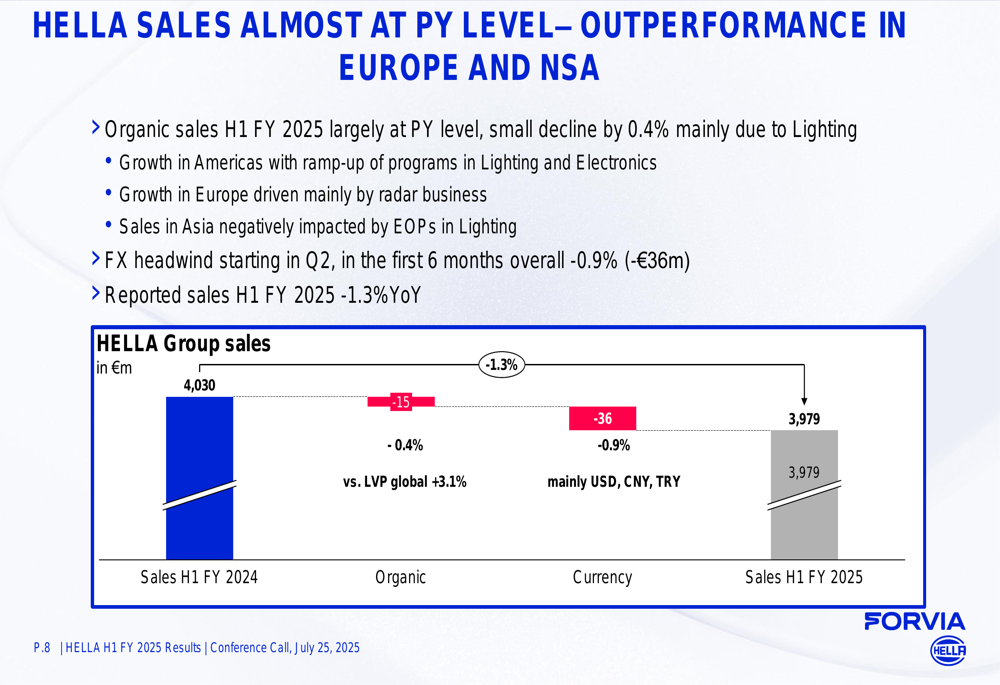

The automotive supplier operated in a mixed global market environment, with light vehicle production up 3.1% globally during the period, primarily driven by China (+11.9%). However, HELLA’s performance varied significantly by region, with strong outperformance in Europe and the Americas contrasting with substantial underperformance in Asia-Pacific markets.

Quarterly Performance Highlights

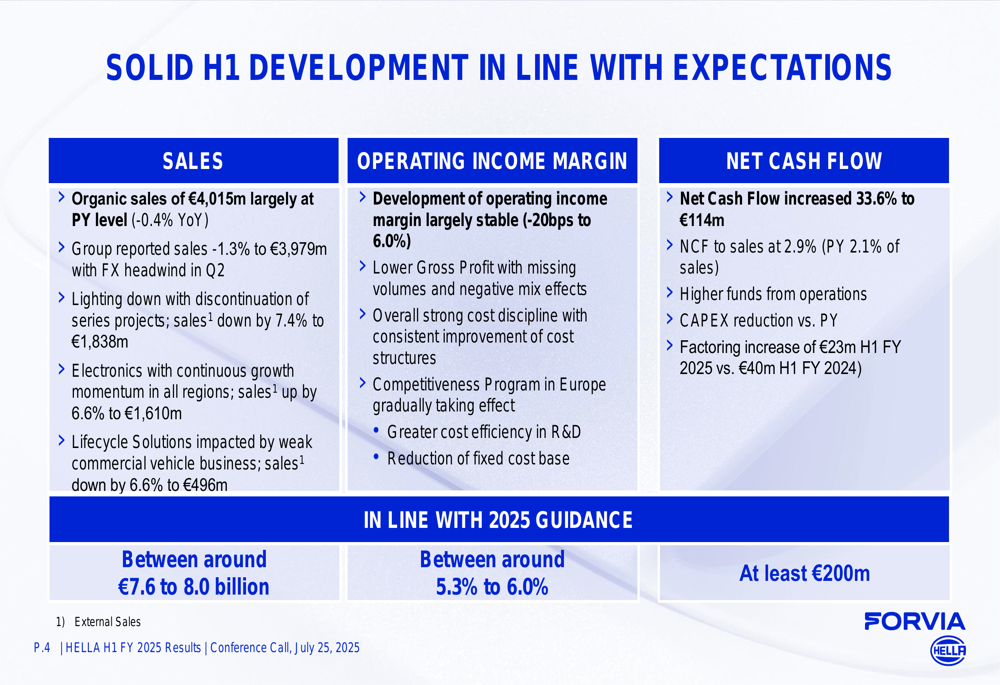

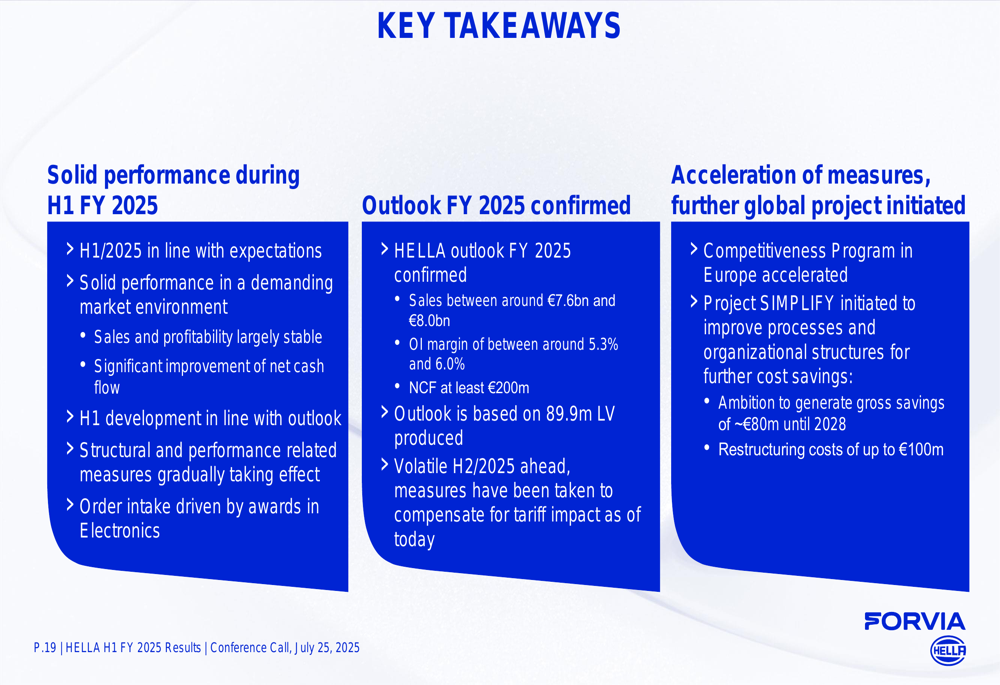

HELLA reported organic sales of €4,015 million for H1 2025, representing a slight decline of 0.4% year-over-year. Group reported sales decreased by 1.3% to €3,979 million, primarily due to foreign exchange headwinds that began impacting results in Q2.

As shown in the following chart summarizing H1 2025 development:

The company maintained relatively stable profitability with an Operating Income Margin of 6.0%, down just 20 basis points from the previous year. This stability was achieved through strong cost discipline and the positive effects of the Competitiveness Program in Europe, which helped offset lower gross profit.

Net Cash Flow showed significant improvement, increasing by 33.6% to €114 million, with NCF to sales ratio reaching 2.9%.

Detailed Financial Analysis

HELLA’s performance varied considerably across its three business divisions, with Electronics showing growth while Lighting and Lifecycle Solutions experienced declines.

The following chart illustrates the Group’s overall sales performance:

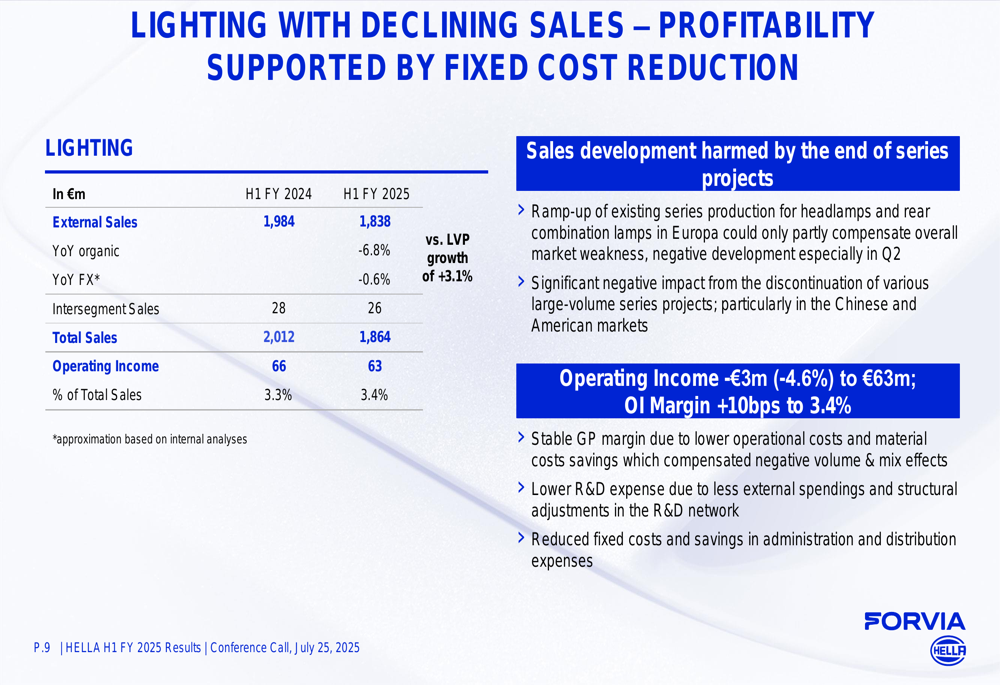

In the Lighting division, external sales decreased by 7.4% to €1,838 million, primarily due to the end of several series projects. Despite this, the division’s operating income margin improved slightly to 3.4% (from 3.3%), benefiting from lower R&D expenses and reduced fixed costs.

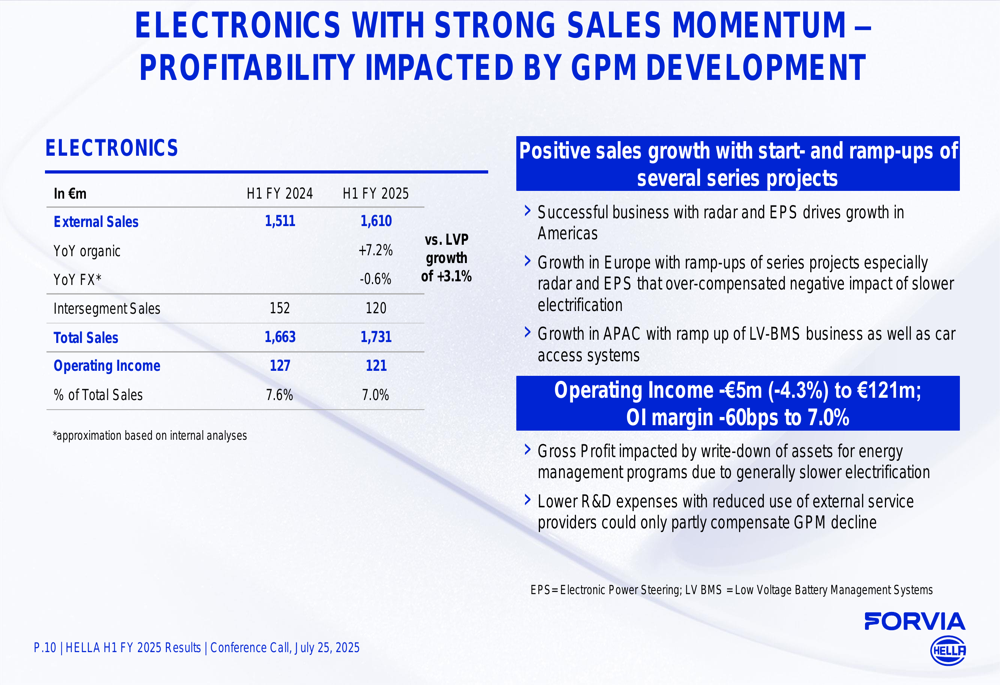

The Electronics division was the standout performer, with external sales increasing by 6.6% to €1,610 million. This growth was driven by the start and ramp-up of several series projects. However, operating income declined by 4.3% to €121 million, with margin decreasing 60 basis points to 7.0%, partly due to asset write-downs for energy management programs.

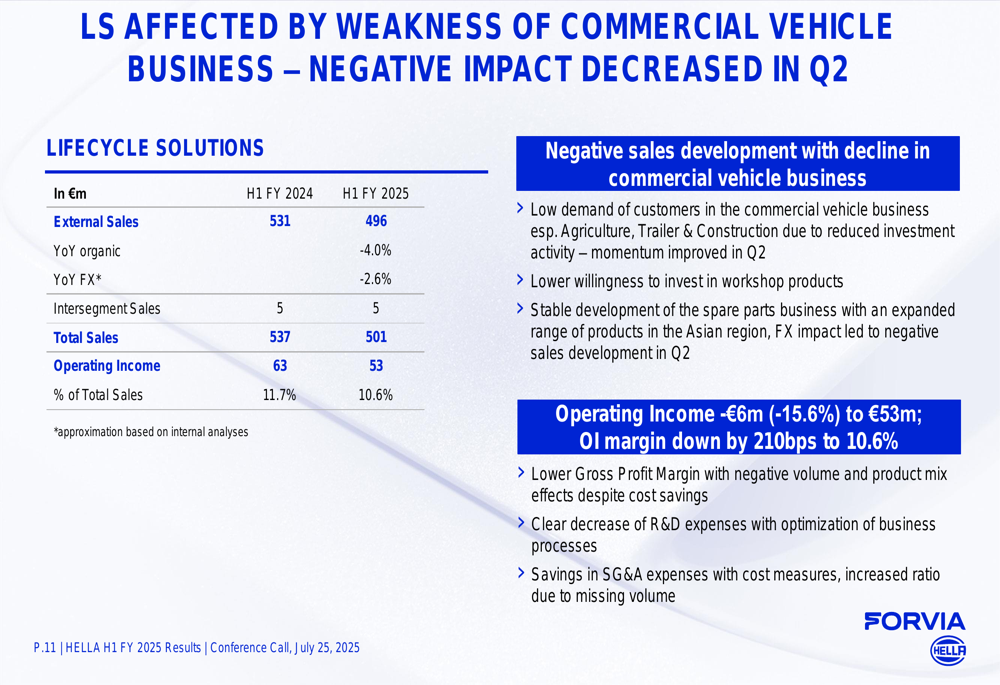

The Lifecycle Solutions division experienced a 6.6% decline in external sales to €496 million, primarily due to weakness in the commercial vehicle business. Operating income fell by 15.6% to €53 million, with margin dropping 210 basis points to 10.6%, though the division did achieve a reduction in R&D expenses through business process optimization.

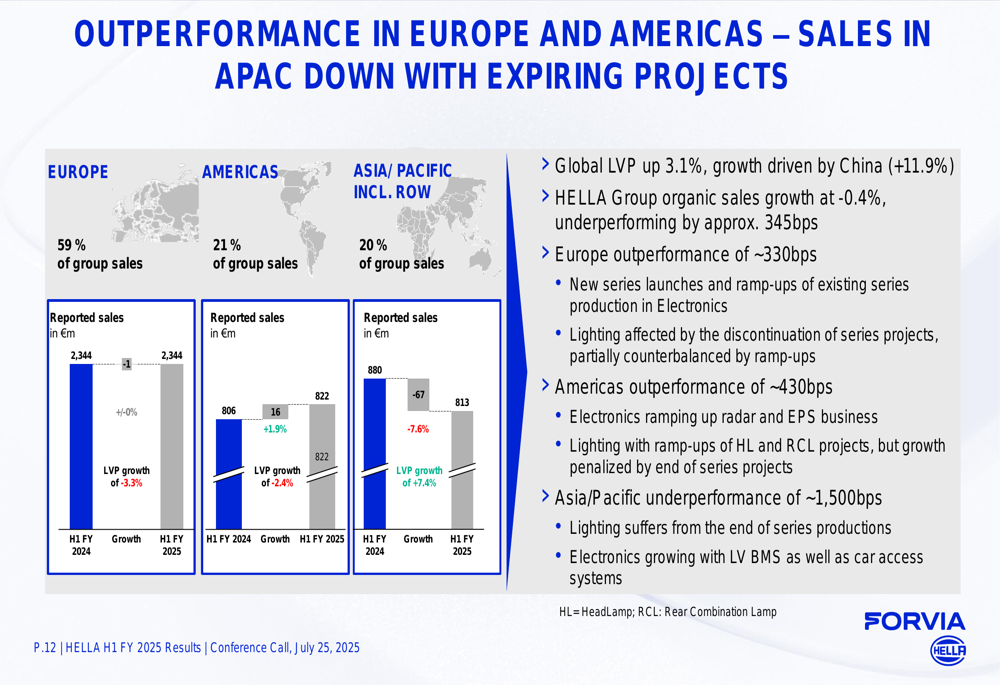

Regional performance showed significant variations, as illustrated in the following geographical breakdown:

Europe maintained stable sales at €2,344 million, outperforming the market by approximately 330 basis points. The Americas region saw sales growth of 1.9% to €822 million, outperforming its market by around 430 basis points. In contrast, Asia/Pacific (including Rest of World) experienced a 7.6% sales decline to €813 million, significantly underperforming the market by approximately 1,500 basis points, despite China driving global light vehicle production growth.

Strategic Initiatives

HELLA emphasized its focus on improving competitiveness through two key initiatives. The ongoing Competitiveness Program in Europe aims to enhance efficiency through capacity reduction, standardization, automation, administrative cost reduction, and increased R&D efficiency.

Additionally, the company announced Project "Simplify," a new global initiative targeting approximately €80 million in further gross savings until 2028. This project focuses on streamlining administration and functions, simplifying processes, adjusting roles, consolidating functions, and leveraging synergies. HELLA expects to incur up to €100 million in restructuring costs for this initiative.

The company also highlighted strong global order intake across all divisions, demonstrating continued innovation and technological advancement. Notable orders included headlamp packages for European premium OEMs, three-digit million orders for electronics components, and lighting modules for commercial vehicles.

Forward-Looking Statements

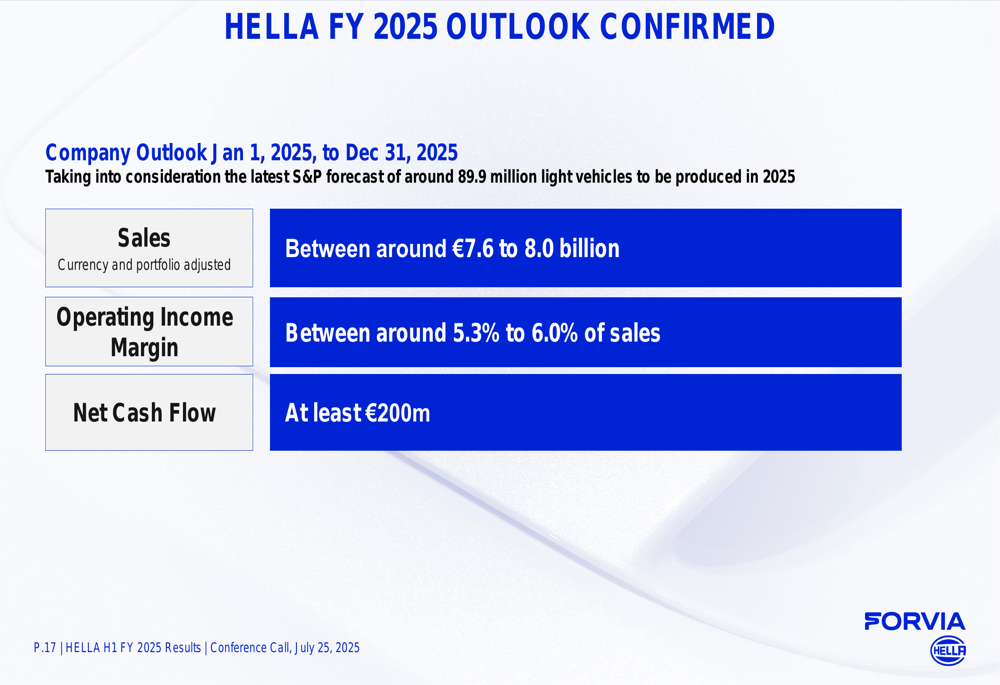

HELLA confirmed its guidance for fiscal year 2025, projecting:

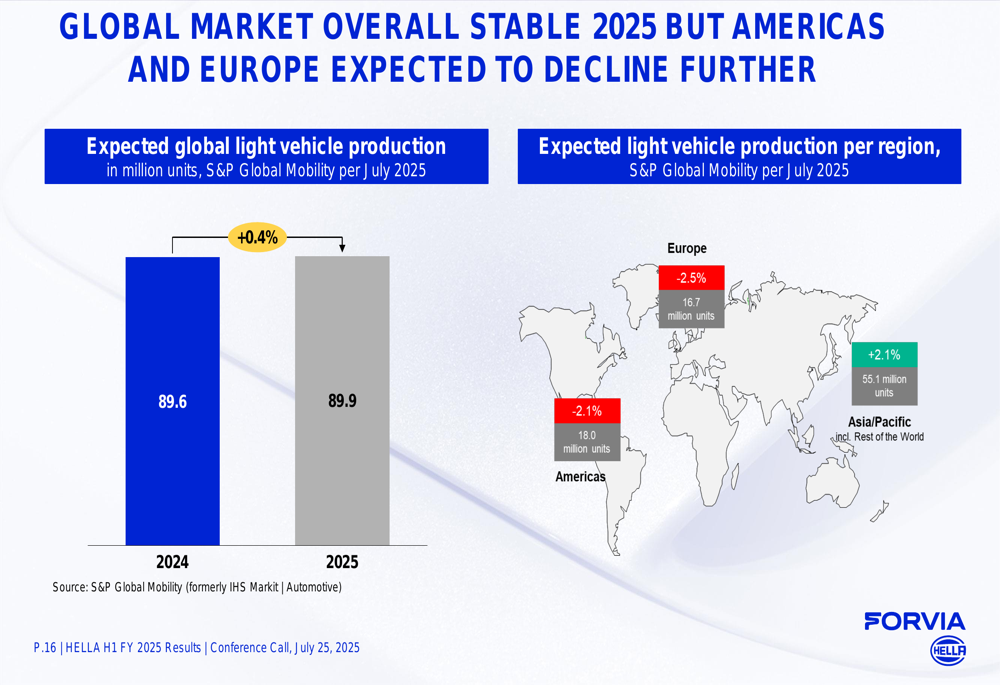

The outlook is based on S&P’s forecast of approximately 89.9 million light vehicles to be produced globally in 2025, representing a modest 0.4% increase year-over-year. Regional production is expected to decline in both the Americas (-2.1%) and Europe (-2.5%), while Asia/Pacific is forecast to grow by 2.1%.

In summarizing the company’s position and outlook, HELLA emphasized that H1 2025 performance was in line with expectations, with structural and performance-related measures gradually taking effect. Management expressed confidence in the confirmed FY 2025 outlook and highlighted the acceleration of efficiency measures through the newly initiated global project.

These results align with parent company Forvia’s broader performance, which saw a 1.1% organic growth in H1 2025 revenue to €13.5 billion and an operating margin improvement of 20 basis points to 5.4%. The positive market reaction to the group’s results suggests investor confidence in the strategic direction despite the mixed performance across HELLA’s divisions and regions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.