Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Helmerich & Payne , Inc. (NYSE:HP) presented its Q2 fiscal 2025 corporate update on May 8, 2025, highlighting the company’s financial performance and strategic initiatives. As the premier U.S. driller and a significant global player, H&P continues to navigate a challenging market environment while maintaining strong margins and pursuing international growth opportunities.

The presentation comes as H&P’s stock trades at $19.00, significantly below its 52-week high of $42.39, reflecting broader industry pressures despite the company’s operational resilience. The drilling contractor has maintained its position as the largest driller in the U.S. while expanding its international footprint.

Quarterly Performance Highlights

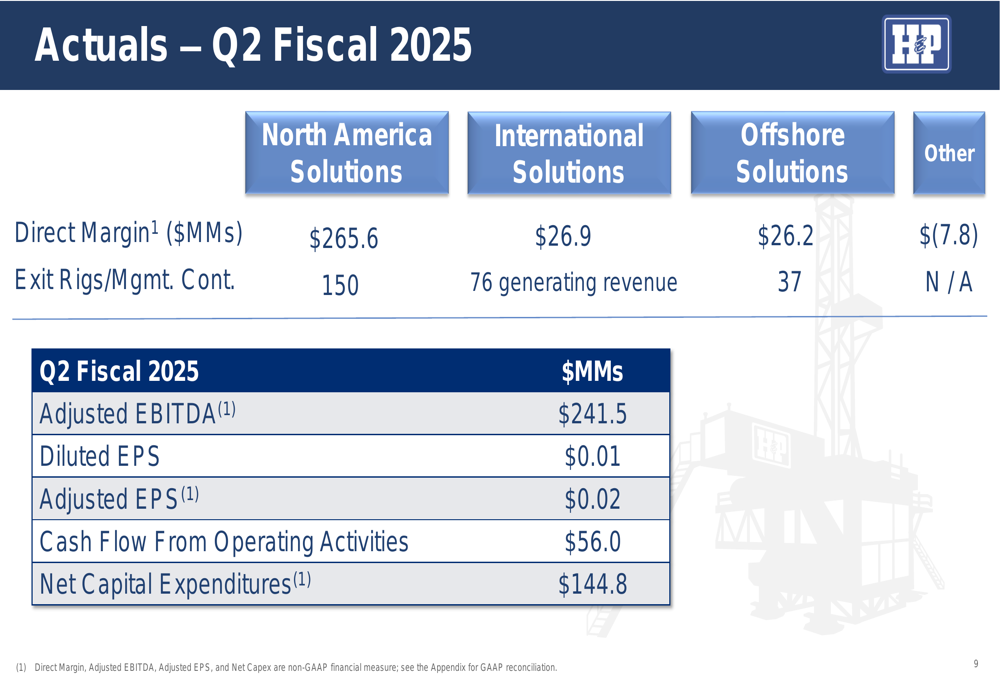

H&P reported solid financial results for Q2 fiscal 2025, with an Adjusted EBITDA of $241.5 million. The company’s North America Solutions segment generated a direct margin of $265.6 million, while International Solutions and Offshore Solutions contributed $26.9 million and $26.2 million, respectively.

As shown in the company’s quarterly results:

However, earnings per share figures were modest, with diluted EPS at $0.01 and adjusted EPS at $0.02. Cash flow from operating activities reached $56.0 million, while net capital expenditures totaled $144.8 million.

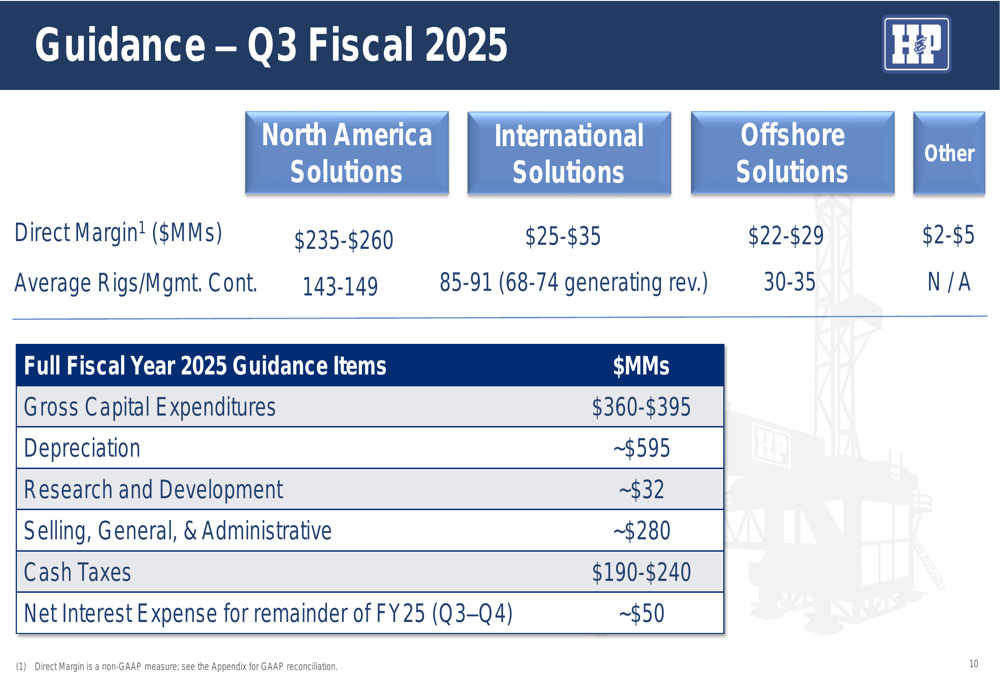

Looking ahead to Q3 fiscal 2025, H&P expects a slight decrease in its North America Solutions direct margin to $235-$260 million, while projecting International Solutions direct margin between $25-$35 million and Offshore Solutions between $22-$29 million.

The guidance reflects the company’s realistic outlook for the coming quarter:

Strategic Initiatives

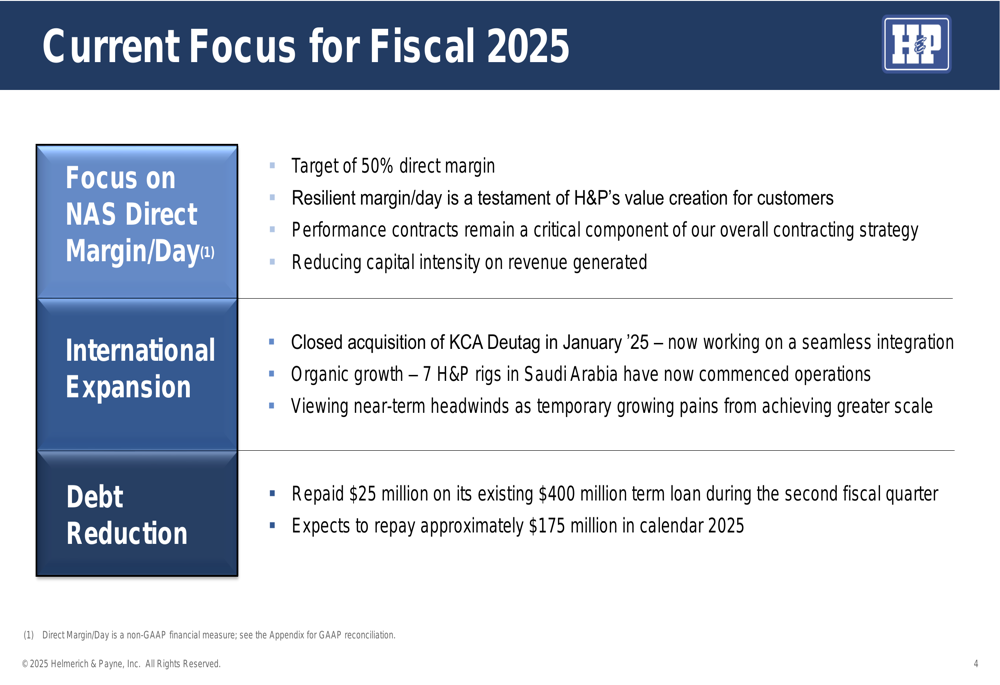

H&P has outlined three key focus areas for fiscal 2025: maintaining strong direct margins in North America, expanding internationally, and reducing debt. The company is targeting a 50% direct margin in its North America Solutions segment while focusing on performance contracts and reducing capital intensity.

The strategic roadmap for the current fiscal year emphasizes these priorities:

International expansion remains a priority, with the KCA Deutag acquisition playing a central role despite near-term headwinds in Saudi Arabia. The company noted that 17 rigs in Saudi Arabia have either temporarily suspended operations or have been notified to suspend operations, reflecting regional challenges mentioned in previous earnings calls.

H&P’s global footprint continues to expand, with the company maintaining a strong presence across key drilling markets:

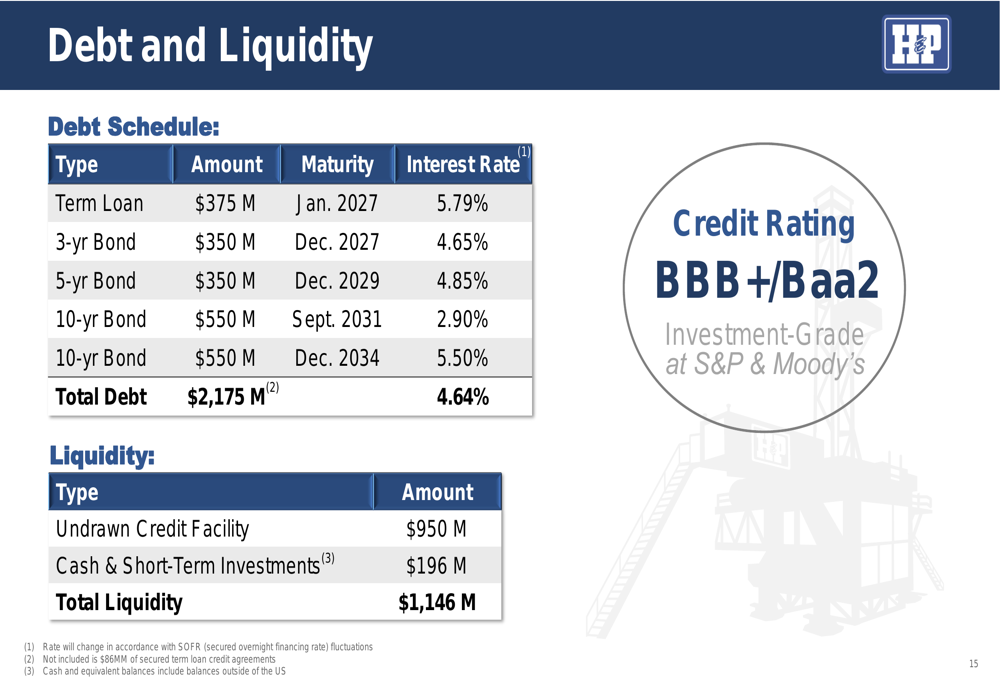

Financial Position

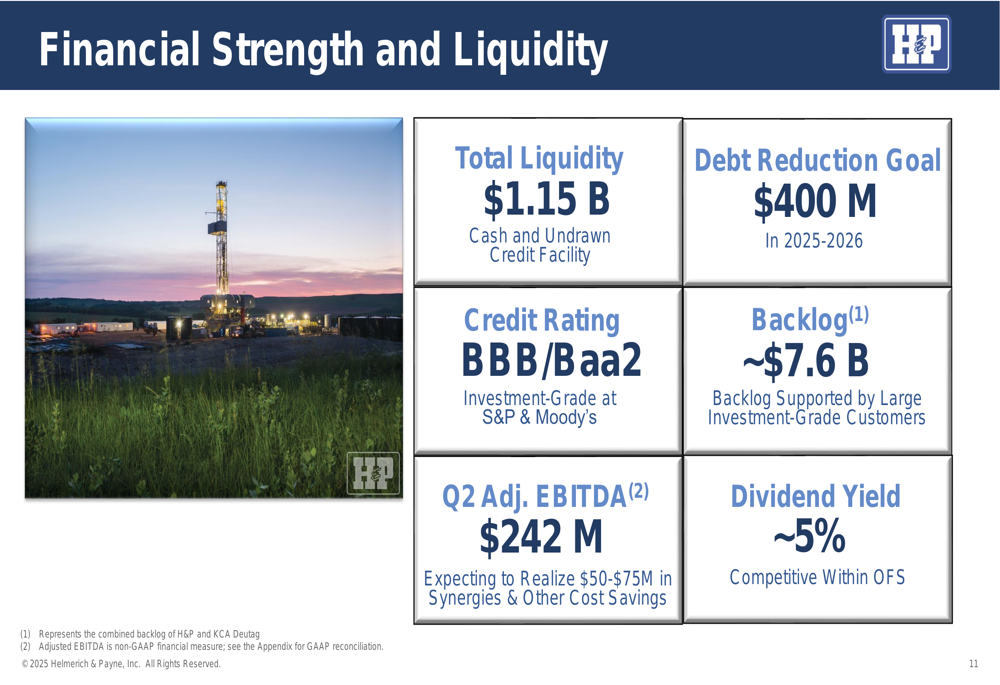

The company highlighted its strong financial position, with total liquidity of $1.15 billion, including cash and undrawn credit facilities. H&P maintains an investment-grade credit rating of BBB/Baa2 from S&P and Moody’s, respectively, and has a significant backlog of approximately $7.6 billion, providing substantial revenue visibility.

The financial strength metrics underscore H&P’s solid foundation:

Debt reduction remains a key priority, with H&P having repaid $25 million on its existing term loan and expecting to repay approximately $175 million more in calendar 2025. The company has set an ambitious debt reduction goal of $400 million for 2025-2026.

The company’s debt schedule shows a well-structured maturity profile:

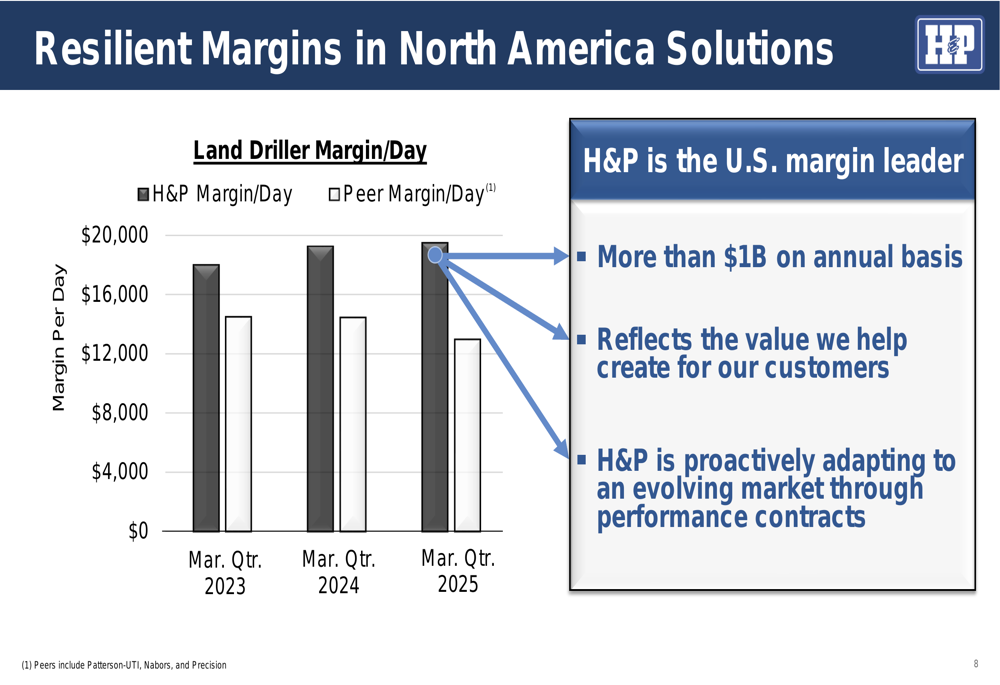

Competitive Industry Position

H&P emphasized its differentiation in the market through scale, an evolving commercial model, and technology. The company noted that approximately 50% of its North America Solutions contracts are performance-based, which integrate H&P’s technology to help achieve desired customer outcomes and are accretive to margins.

The presentation highlighted H&P’s position as the U.S. margin leader, consistently outperforming peers:

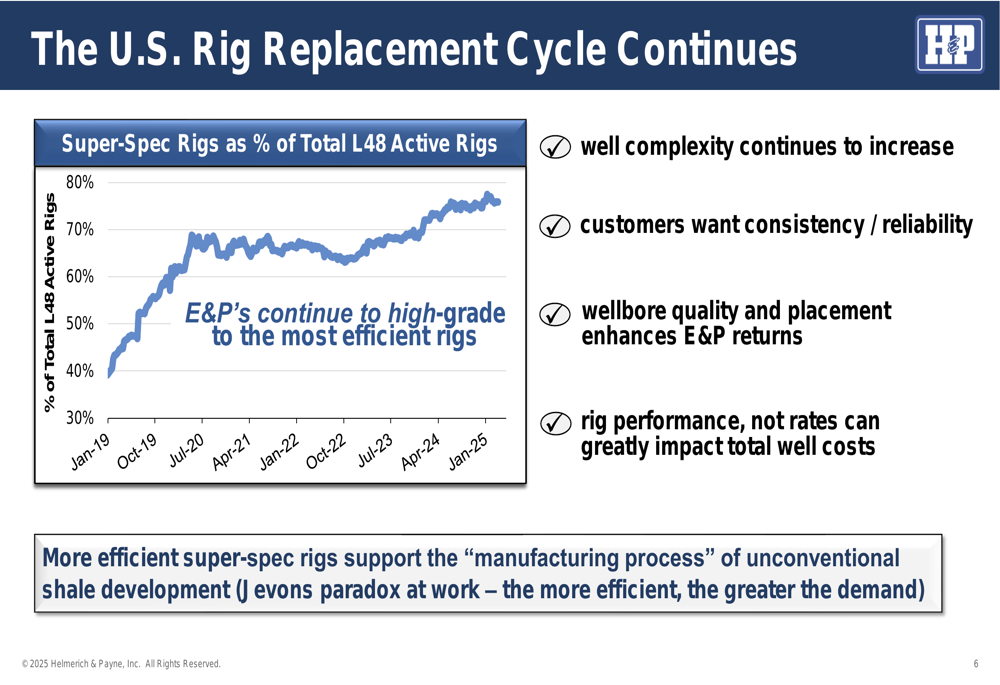

The industry continues to shift toward super-spec rigs, which now represent over 70% of total L48 active rigs, up from 40% in January 2019. This trend benefits H&P, which has the largest fleet of super-spec rigs in the U.S. market.

The increasing preference for super-spec rigs is clearly illustrated:

Forward-Looking Statements

For the remainder of fiscal 2025, H&P expects to generate $50-$75 million in synergies and other cost savings, likely related to the KCA Deutag acquisition. The company maintains a dividend yield of approximately 5%, which it describes as competitive within the oilfield services sector.

H&P’s capital allocation strategy focuses on maintaining its investment-grade credit rating, delivering shareholder returns through a base dividend of $1 per share annually, and funding capital expenditures based on market demand and growth opportunities.

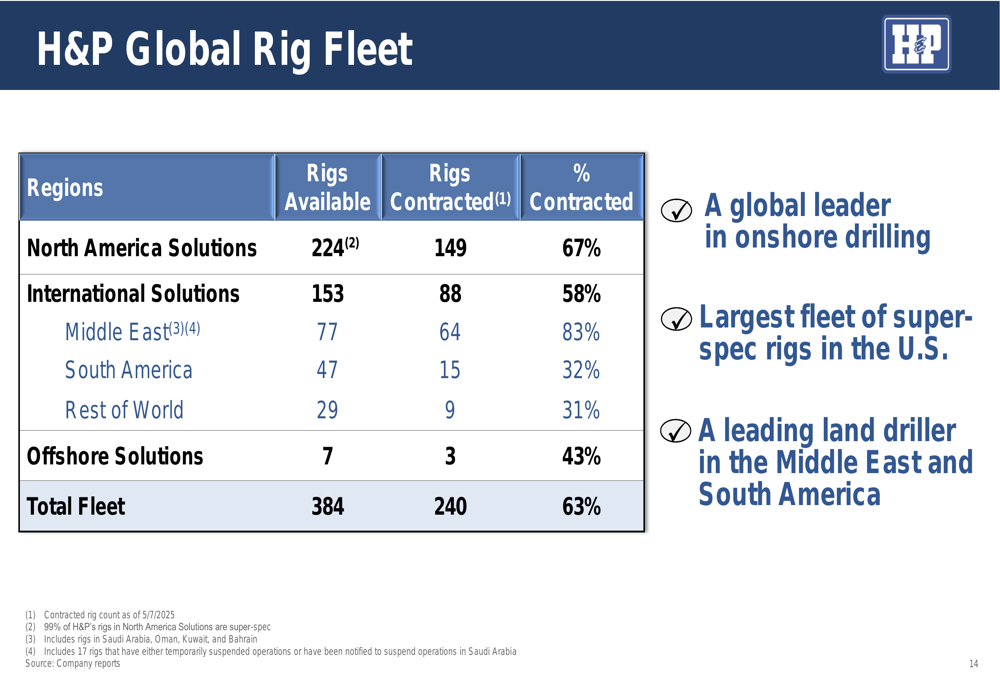

The company’s global rig fleet provides a strong foundation for future growth, with 384 rigs available worldwide and 240 currently contracted (63% utilization):

While H&P faces challenges, particularly in Saudi Arabia where operations have been affected by contract suspensions, the company’s diversified global presence and strong financial position appear to provide a buffer against regional volatility as it continues to execute its strategic plan for fiscal 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.