Microvast Holdings announces departure of chief financial officer

Heritage Financial Corporation (NASDAQ:HFWA) released its Q1 2025 investor presentation on April 24, 2025, highlighting improved financial performance following a disappointing Q4 2024. The regional bank, which operates across Washington, Oregon, and Idaho, reported strengthened net interest margin and continued loan growth while maintaining solid credit quality.

Quarterly Performance Highlights

Heritage Financial reported net income of $13.9 million for Q1 2025, with an improved net interest margin of 3.44%, up from 3.39% in the previous quarter. This improvement aligns with management’s projection for continued margin expansion following Q4 2024’s earnings miss, when the company reported EPS of $0.34 against analyst expectations of $0.45.

The company’s adjusted return on average tangible common equity (ROATCE) reached 11.21%, while the adjusted efficiency ratio improved to 67.3%. Adjusted diluted earnings per share stood at $0.49 for the quarter.

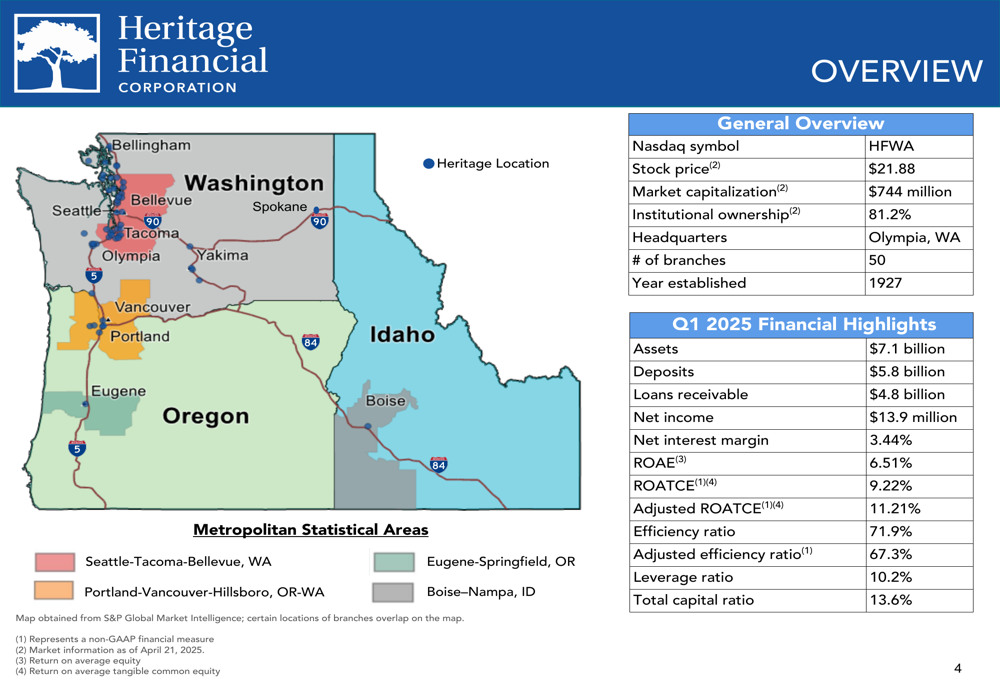

As shown in the following comprehensive overview, Heritage maintains a strong presence across the Pacific Northwest with 50 branches and total assets of $7.1 billion:

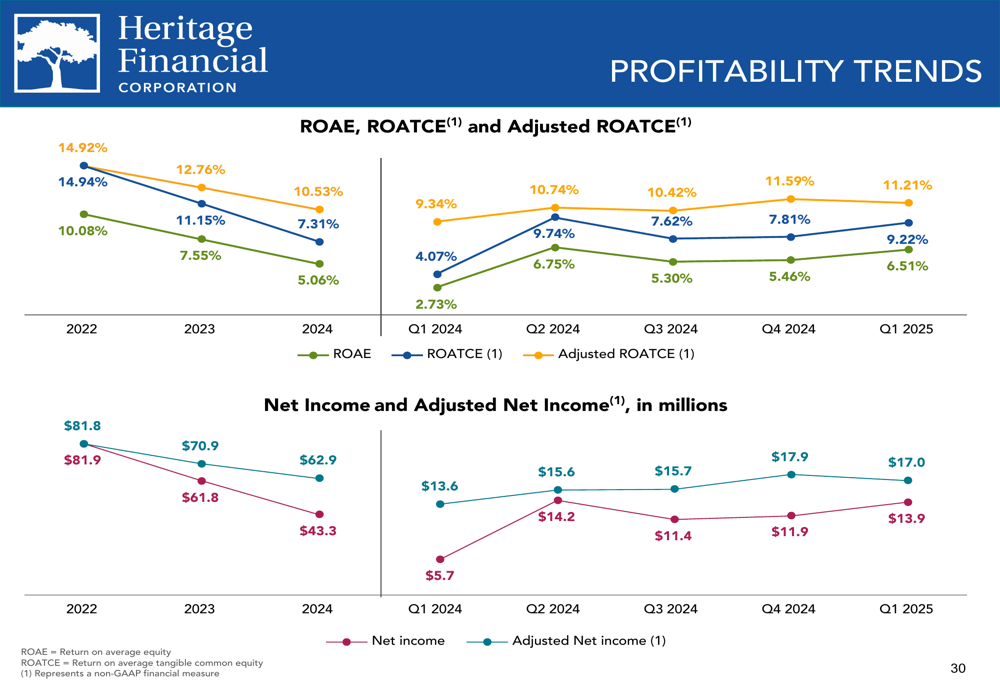

The company’s profitability metrics show consistent improvement, with adjusted net income approaching $14 million in Q1 2025, reflecting the benefits of strategic balance sheet repositioning and operational efficiency initiatives:

Strategic Initiatives

Heritage has been implementing a strategic balance sheet repositioning through investment sales over recent quarters. In Q1 2025, the company sold $60.9 million in investments with a weighted average book yield of 2.60% and purchased $28.2 million with a yield of 4.55%. This repositioning resulted in a $3.9 million loss on sale but is expected to generate an estimated annualized EPS impact of $0.04.

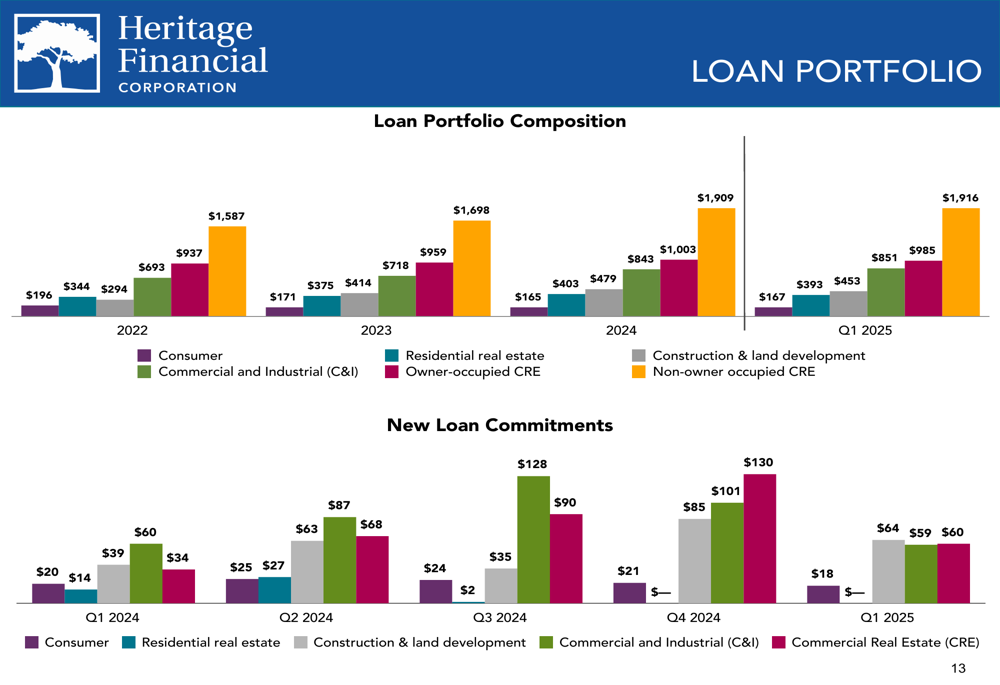

The company’s loan portfolio continues to grow, with a focus on commercial and industrial (C&I) lending. New loan commitments in Q1 2025 totaled $59 million for C&I loans, the highest among all loan categories.

The following chart illustrates the composition of Heritage’s loan portfolio and new loan commitments:

Heritage operates in economically robust regions, with Seattle representing 49% of the loan portfolio and 44.2% of deposits. The company’s strategic focus on these high-growth markets positions it well for continued expansion.

Credit Quality and Risk Management

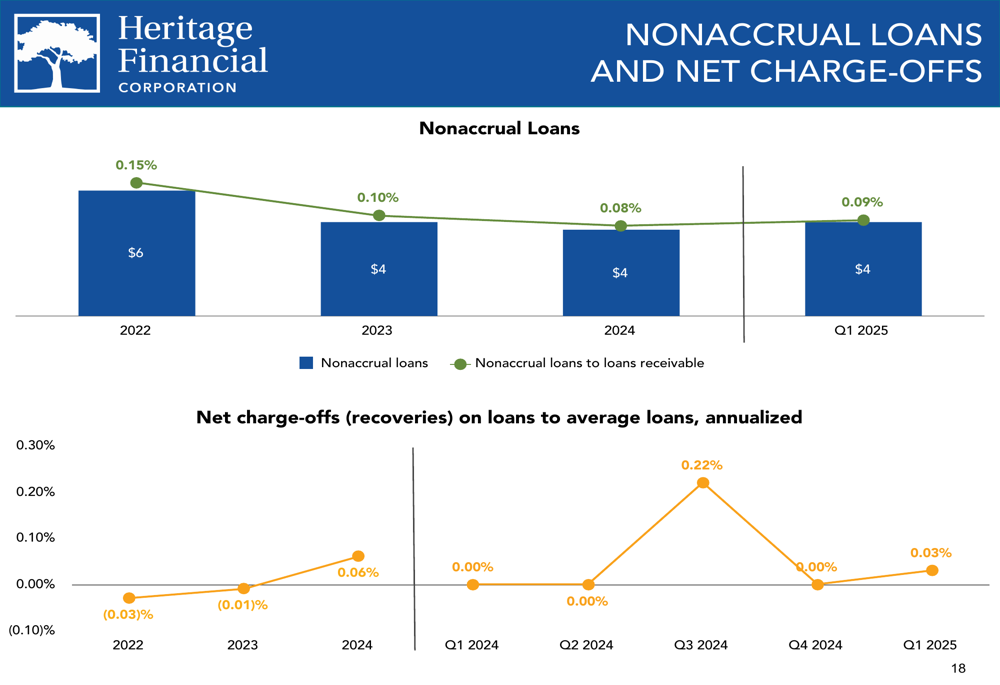

Heritage maintained strong credit quality metrics in Q1 2025, with nonaccrual loans at just $4 million, representing 0.09% of loans receivable, down from 0.15% in 2022. Net charge-offs remained low at 0.03% of average loans (annualized).

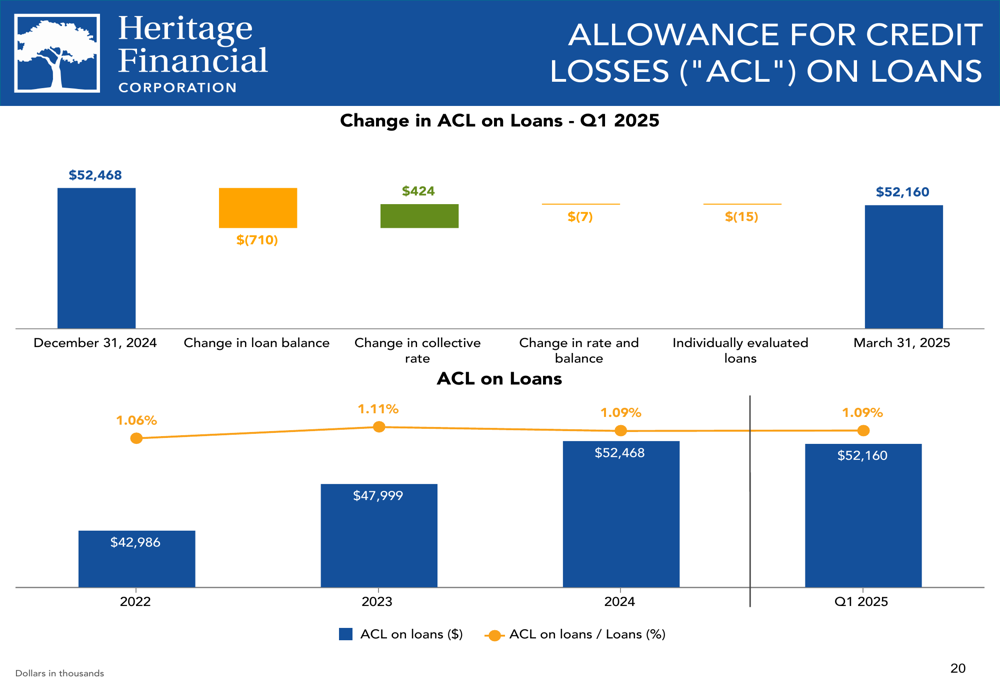

The following chart demonstrates the company’s consistently strong asset quality metrics:

The allowance for credit losses on loans stood at $52.16 million as of March 31, 2025, reflecting a slight decrease from $52.47 million at the end of 2024:

Heritage’s commercial real estate (CRE) office portfolio, often a concern for investors in the current market environment, shows strong risk management practices. The company reported that 81% of these loans have recourse to the owner, and 52% are owner-occupied, which typically carry a lower risk profile.

Capital Position and Shareholder Returns

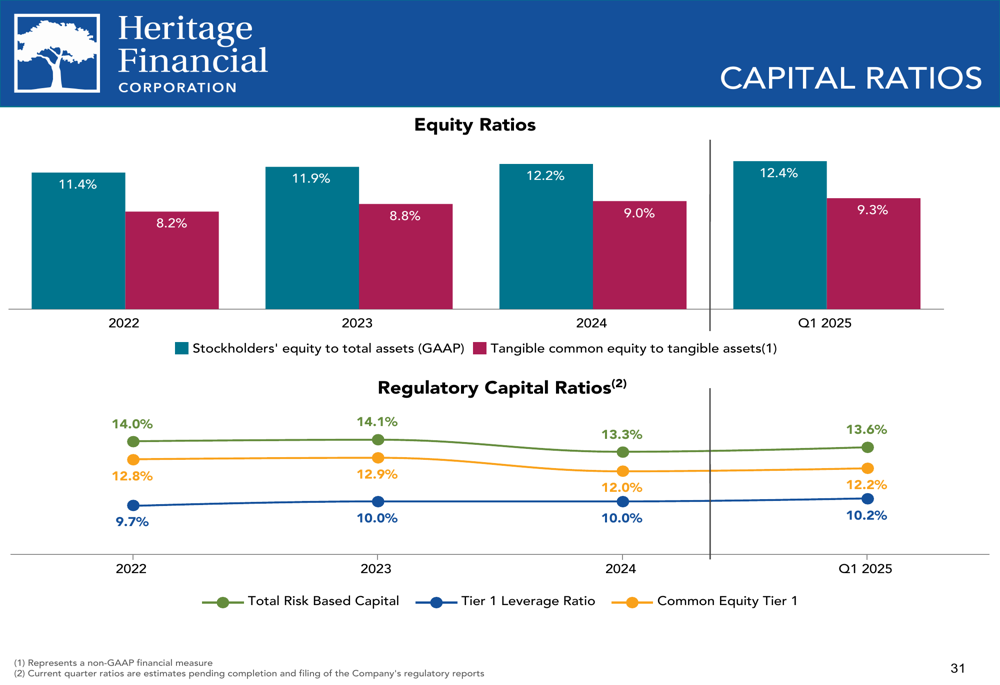

Heritage maintains a robust capital position with a leverage ratio of 10.2% and a total capital ratio of 13.6% as of Q1 2025. These strong capital ratios provide flexibility for potential growth opportunities, including possible acquisitions in the Pacific Northwest.

The company’s capital strength is illustrated in the following chart:

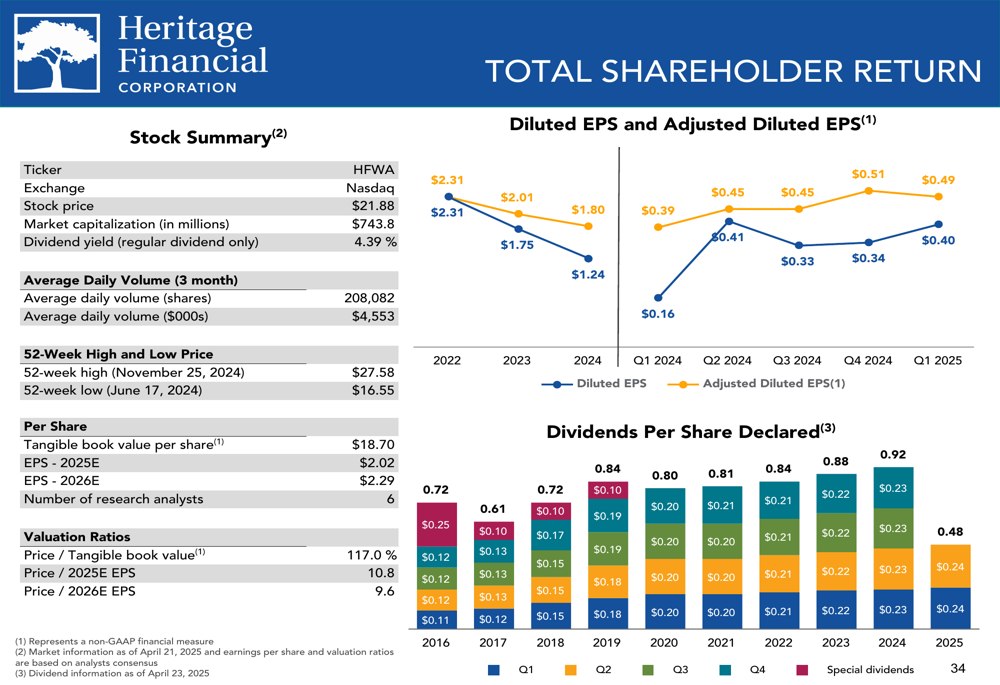

Heritage has maintained a consistent dividend policy, declaring a quarterly dividend of $0.24 per share in Q1 2025, unchanged from the previous quarter. The company’s tangible book value per share stood at $18.70 as of March 31, 2025.

The following chart summarizes key shareholder return metrics:

Forward-Looking Statements

Heritage Financial appears well-positioned for continued growth, focusing on commercial lending and potential strategic acquisitions. The company’s strong presence in economically vibrant regions provides a solid foundation for expansion.

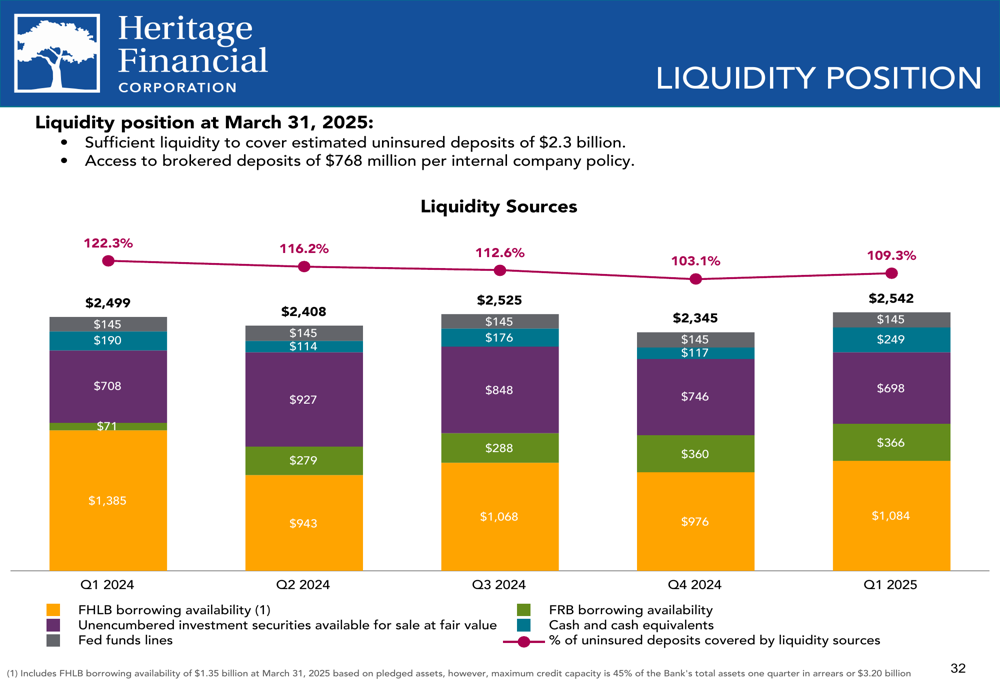

The bank’s liquidity position remains strong, with multiple sources available to meet potential funding needs:

Despite trading down 0.78% in pre-market activity to $22.80 on April 24, Heritage’s stock has shown resilience, trading well above its 52-week low of $16.55 and approaching its 52-week high of $27.58.

CEO Brian MacDonald had previously expressed optimism about the company’s growth prospects, stating, "We are optimistic the combination of core balance sheet growth and prudent risk management will continue to benefit our core profitability." The Q1 2025 presentation appears to support this outlook, with improved performance metrics across multiple categories following the Q4 2024 earnings disappointment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.