Gold ticks up but remains pressured by Fed rate caution, easing trade fears

Introduction & Market Context

Heritage Financial Corporation (NASDAQ:HFWA) reported solid third-quarter 2025 results, with performance metrics showing improvement amid preparations for its upcoming merger with Olympic Bancorp. The company’s stock responded positively to the earnings announcement, rising 2.87% in pre-market trading to $23.64, reflecting investor confidence in the bank’s strategic direction.

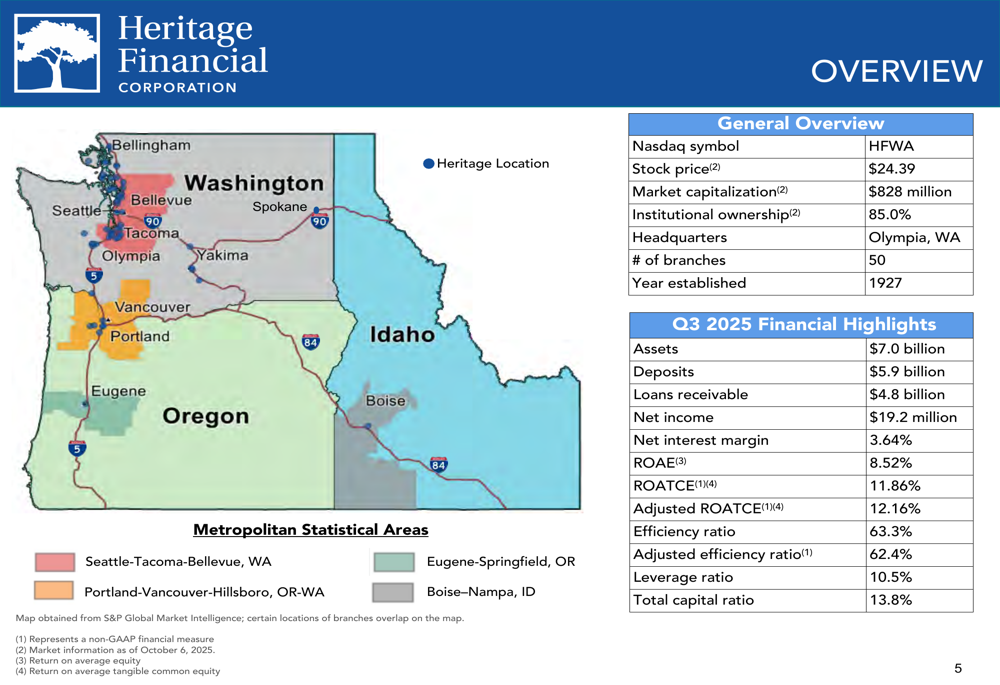

With a market capitalization of $828 million and institutional ownership of 85%, Heritage continues to strengthen its position as a significant regional player in the Pacific Northwest banking sector. The company’s focus on maintaining strong capital ratios while pursuing strategic growth has resonated with investors, particularly as it prepares for the Olympic Bancorp acquisition announced on September 25, 2025.

Quarterly Performance Highlights

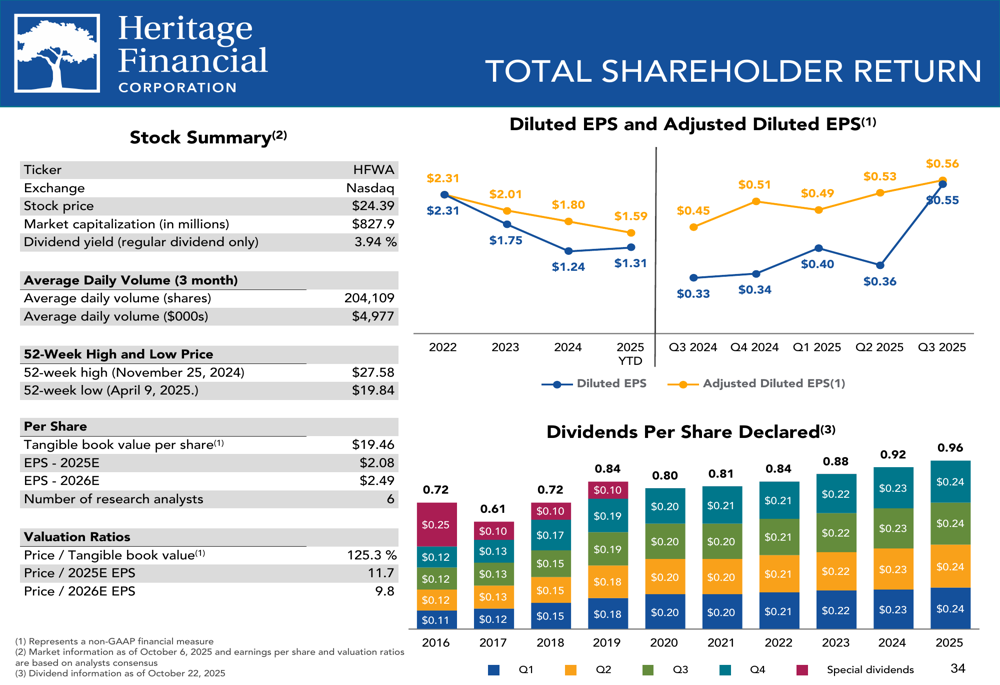

Heritage Financial reported net income of $19.2 million for Q3 2025, exceeding analyst expectations with earnings per share of $0.56 compared to the forecasted $0.55. The company’s profitability metrics showed notable improvement, with return on average assets (ROAA) reaching 1.09% (1.11% adjusted) and return on average tangible common equity (ROATCE) at 11.86% (12.16% adjusted).

As shown in the following company overview, Heritage maintained a strong balance sheet with $7.0 billion in assets, $5.9 billion in deposits, and $4.8 billion in loans receivable:

The bank’s net interest margin improved to 3.64% in Q3 2025, contributing to net interest income of $57.4 million. This represents a 4.3% increase from the previous quarter, demonstrating the company’s ability to navigate the current interest rate environment effectively.

Heritage’s efficiency ratio stood at 63.3% (62.4% adjusted), indicating ongoing efforts to optimize operational performance while maintaining strong capital ratios, with the leverage ratio at 10.5% and total capital ratio at 13.8%.

Strategic Initiatives

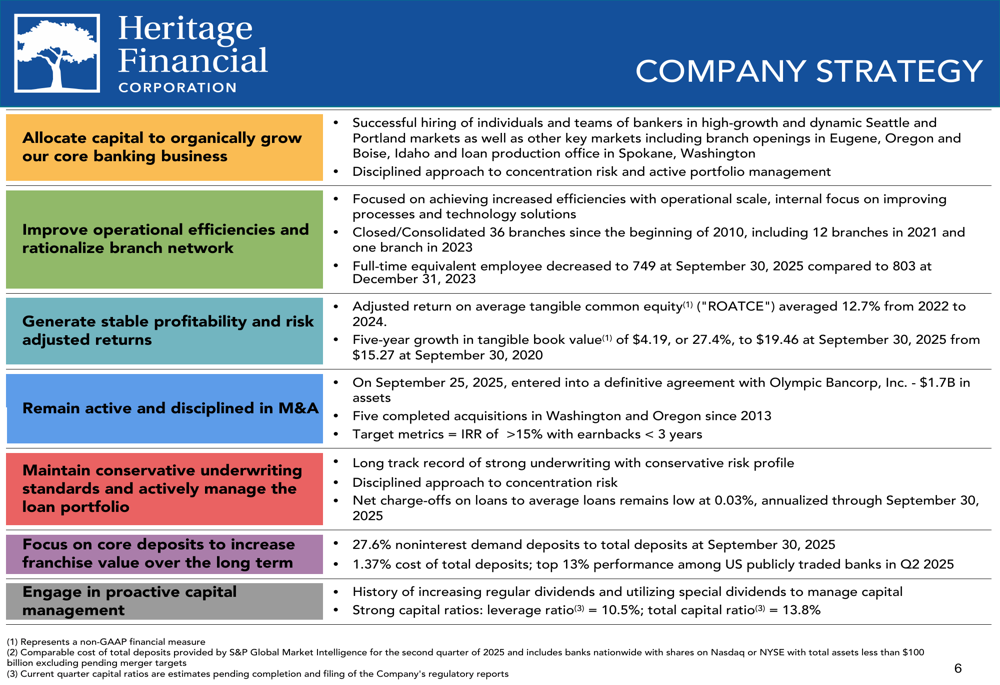

Heritage Financial’s strategic priorities center around building a strong Pacific Northwest regional commercial community bank through both organic growth and strategic acquisitions. The company’s most significant strategic development is the pending merger with Olympic Bancorp, Inc., a $1.7 billion asset institution, which is expected to close in early Q1 2026.

As illustrated in the following strategy overview, Heritage is focusing on seven key strategic priorities, including organic growth, operational efficiency, profitability, M&A activity, conservative underwriting, core deposit focus, and proactive capital management:

The company has demonstrated a consistent approach to growth through both acquisitions and team additions. Since 2013, Heritage has completed multiple acquisitions while also expanding its commercial banking teams in key markets including Seattle, Portland, Eugene, Boise, and most recently Spokane.

Heritage’s growth strategy is particularly focused on the Pacific Northwest region, where economic indicators remain favorable. The company is targeting merger and acquisition opportunities with a 15% internal rate of return (IRR) and earnback periods of less than three years.

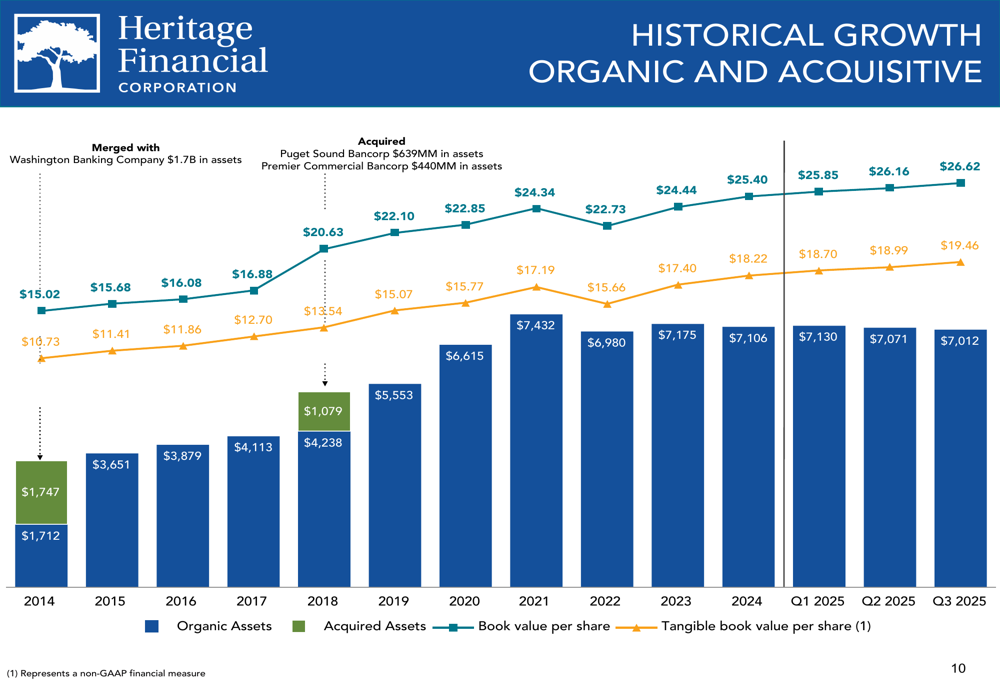

As shown in the following historical growth chart, Heritage has steadily increased its book value per share through both organic growth and acquisitions:

Detailed Financial Analysis

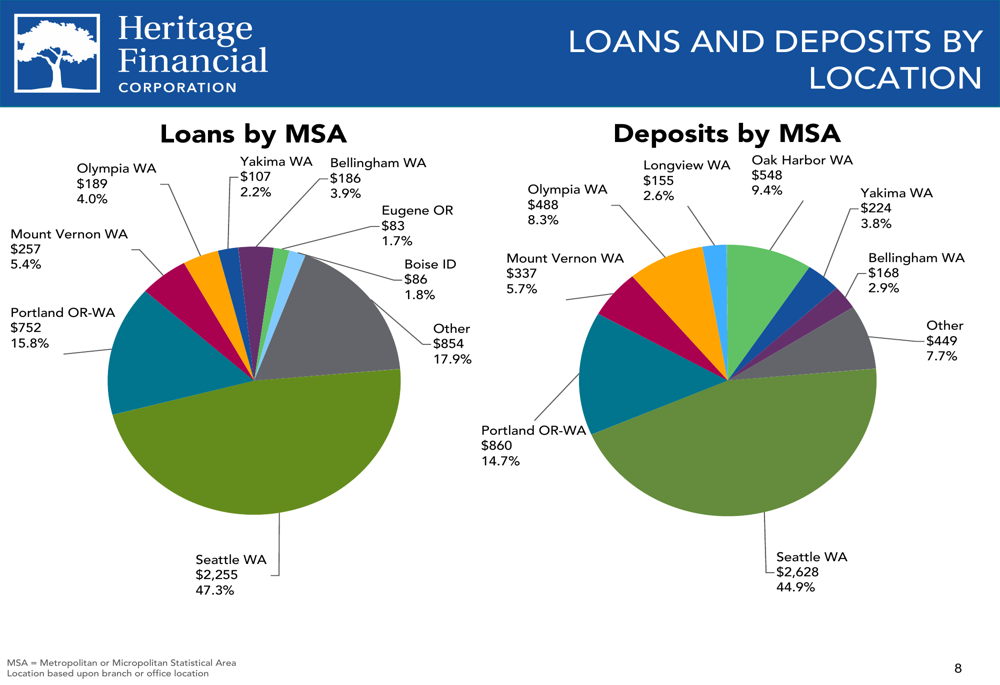

Heritage Financial’s loan portfolio remains well-diversified across multiple segments, with a significant portion in commercial real estate and commercial and industrial loans. The company’s loan distribution by metropolitan statistical area (MSA) shows a concentration in the Seattle market, which accounts for 47.3% of total loans, followed by Portland at 15.8%.

The following chart illustrates the geographic distribution of both loans and deposits across the company’s footprint:

The company’s deposit base remains stable with a favorable composition that includes 27.6% noninterest-bearing demand deposits. This contributes to a relatively low cost of funds despite the rising interest rate environment. Total deposits saw a significant increase of $73 million during the quarter, demonstrating the bank’s ability to attract and retain core deposits.

Heritage’s credit quality metrics remain solid, with net charge-offs to average loans at just 0.01% in Q3 2025. The allowance for credit losses on loans stands at approximately 1.1% of total loans, reflecting the company’s conservative approach to credit risk management.

The company’s investment portfolio is primarily composed of high-quality securities, with 89.8% of available-for-sale securities in U.S. government and agency securities. The portfolio has an estimated $561 million in cashflows through Q3 2028, providing liquidity flexibility as the bank manages its balance sheet.

Forward-Looking Statements

Looking ahead, Heritage Financial expects loan balances to remain relatively flat in Q4 2025 before resuming more normal growth levels in 2026. The company is targeting a loan-to-deposit ratio of around 85% and anticipates new commercial loan commitments of approximately $320 million in Q4.

The pending merger with Olympic Bancorp represents a significant growth opportunity that aligns with Heritage’s strategic vision. During the earnings call, CEO Bryan McDonald expressed optimism about the merger, stating, "We are excited about the pending merger with Olympic Bank Corp. Their addition to the Heritage franchise will add to the profitability of our operations."

Heritage’s strong capital position provides flexibility for future growth initiatives beyond the Olympic Bancorp merger. The company has maintained a history of increasing dividends while supporting organic growth and strategic acquisitions.

As shown in the following total shareholder return slide, Heritage has demonstrated a commitment to delivering value to shareholders through both dividends and earnings growth:

While the company faces potential challenges including merger integration, competitive deposit pricing pressures, and economic uncertainties, its strong market position in the Pacific Northwest and disciplined approach to growth position it well for continued success. The management team has expressed openness to future merger and acquisition opportunities after completing the Olympic Bancorp transaction, suggesting a continued focus on strategic expansion in its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.