Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Heron Therapeutics (NASDAQ:HRTX) presented its Q2 2025 earnings results on August 8, 2025, revealing revenue growth and improved operational metrics, yet the stock plunged 24.18% to $1.45 in morning trading. The significant market reaction came despite the company raising its full-year guidance and reporting continued product growth across its portfolio.

The biopharmaceutical company, which focuses on acute care and oncology products, generated $37.2 million in net revenue for the quarter, continuing its transition toward operational profitability with positive adjusted EBITDA figures, though still reporting a net loss.

Quarterly Performance Highlights

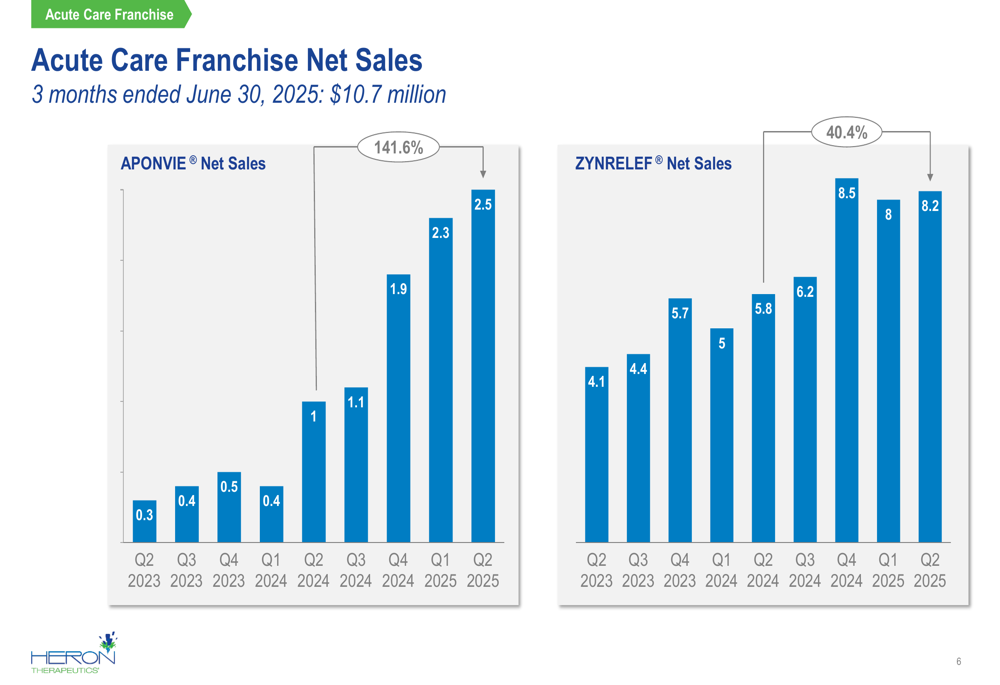

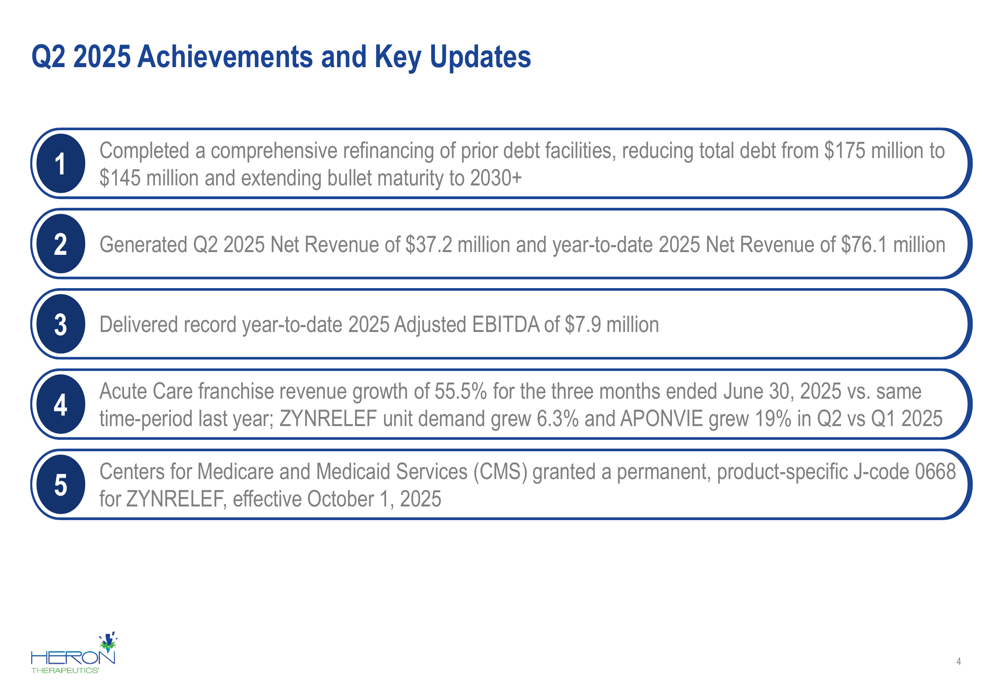

Heron reported Q2 2025 net revenue of $37.2 million and year-to-date revenue of $76.1 million. The company’s Acute Care franchise showed particularly strong performance with 55.5% revenue growth compared to the same period last year.

As shown in the following chart of Acute Care franchise net sales:

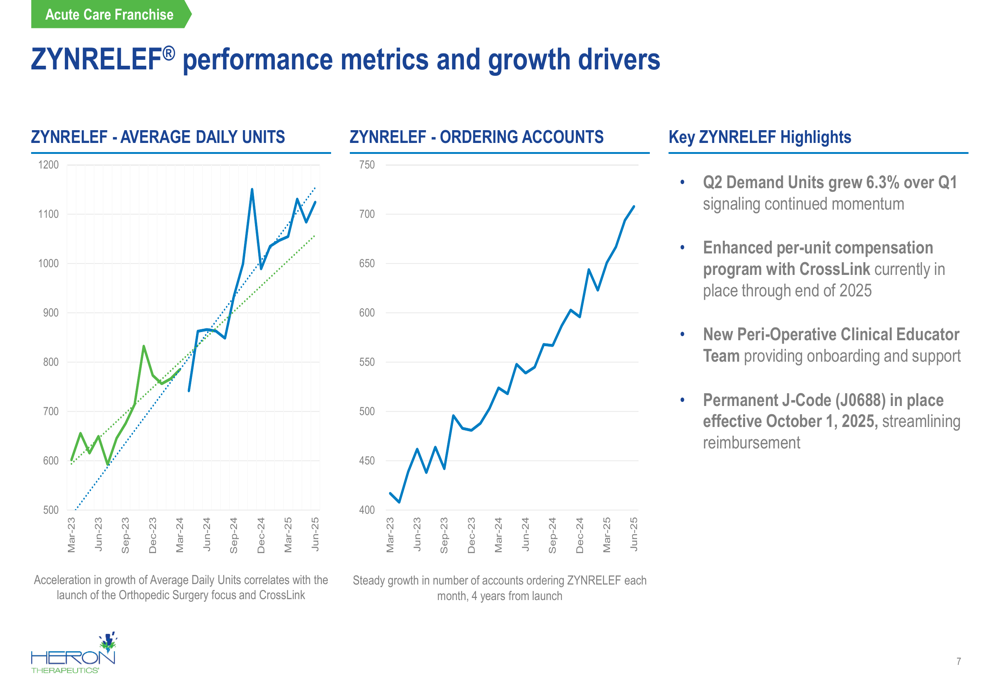

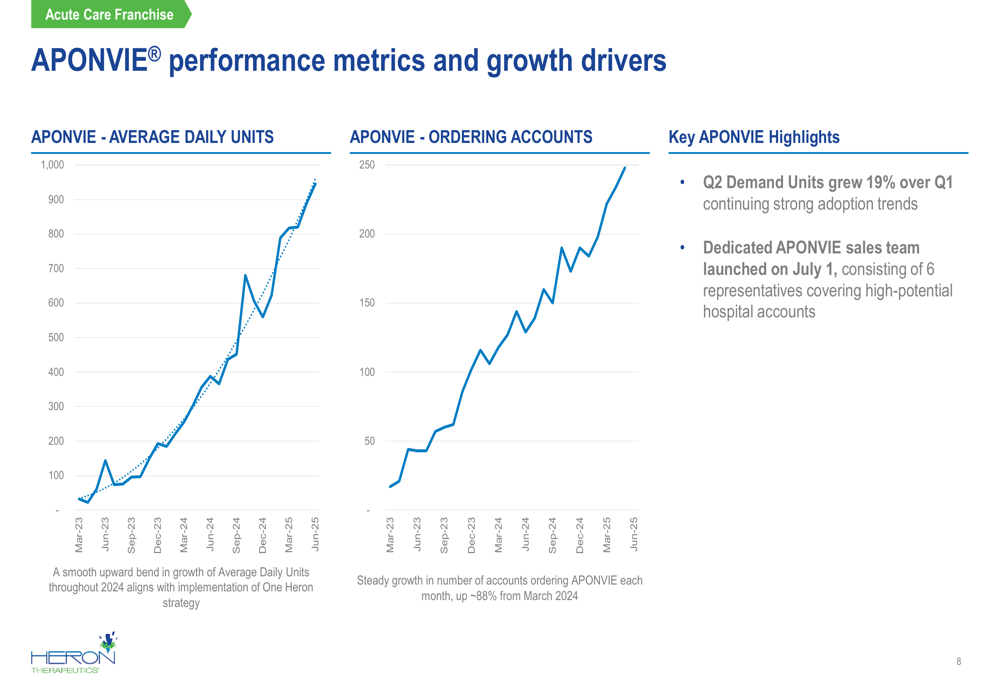

ZYNRELEF, the company’s extended-release solution for post-surgical pain, saw unit demand growth of 6.3% in Q2 compared to Q1 2025, while APONVIE, used for postoperative nausea and vomiting, grew by 19% quarter-over-quarter. The performance metrics for both products demonstrate continued market penetration:

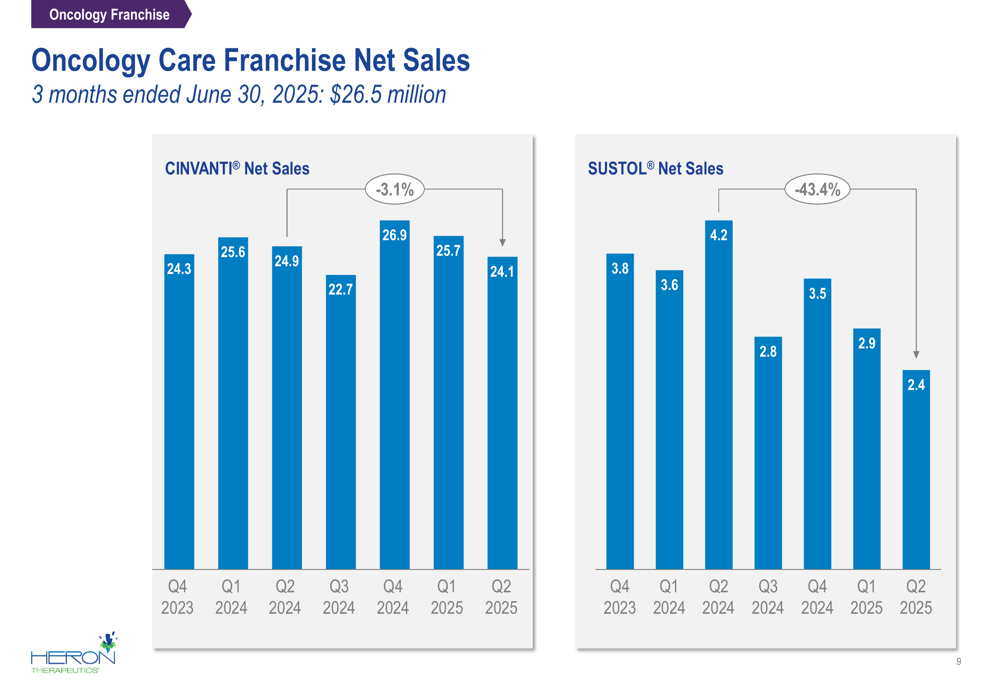

Meanwhile, the Oncology Care franchise, which includes CINVANTI and SUSTOL, generated $26.5 million in net sales for Q2 2025, showing relative stability compared to previous quarters:

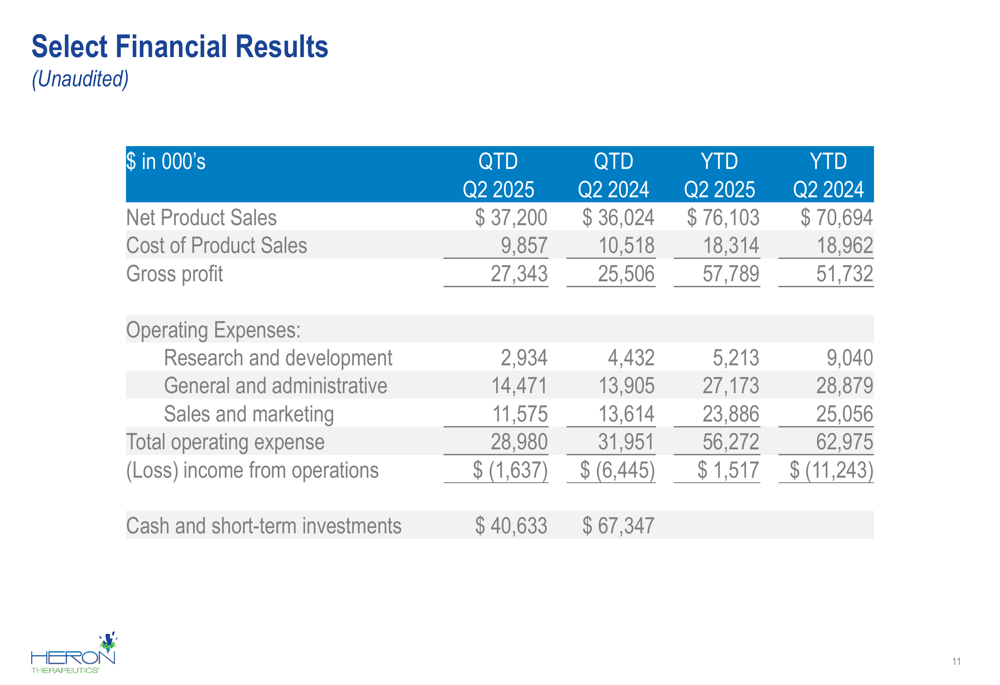

Detailed Financial Analysis

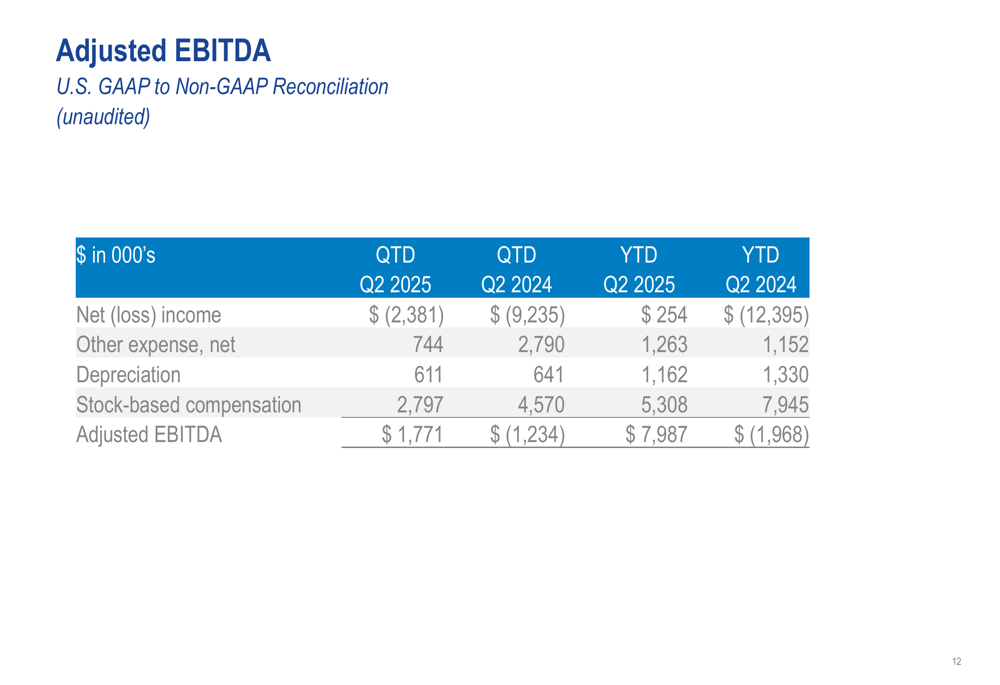

Despite revenue growth, Heron reported a net loss of $2.38 million for Q2 2025, though this represents a significant improvement from the $9.24 million loss in Q2 2024. The company achieved positive adjusted EBITDA of $1.77 million for the quarter, compared to negative $1.23 million in the same period last year.

The financial results show improved gross profit of $27.34 million (up from $25.51 million in Q2 2024) and reduced operating expenses across research and development, sales and marketing, though general and administrative costs increased slightly:

The company’s adjusted EBITDA, which excludes stock-based compensation and depreciation, shows a clear trend toward improved operational efficiency:

Notably, Heron’s cash and short-term investments position declined to $40.63 million from $67.35 million a year earlier, which may be contributing to investor concerns despite the operational improvements.

Strategic Initiatives

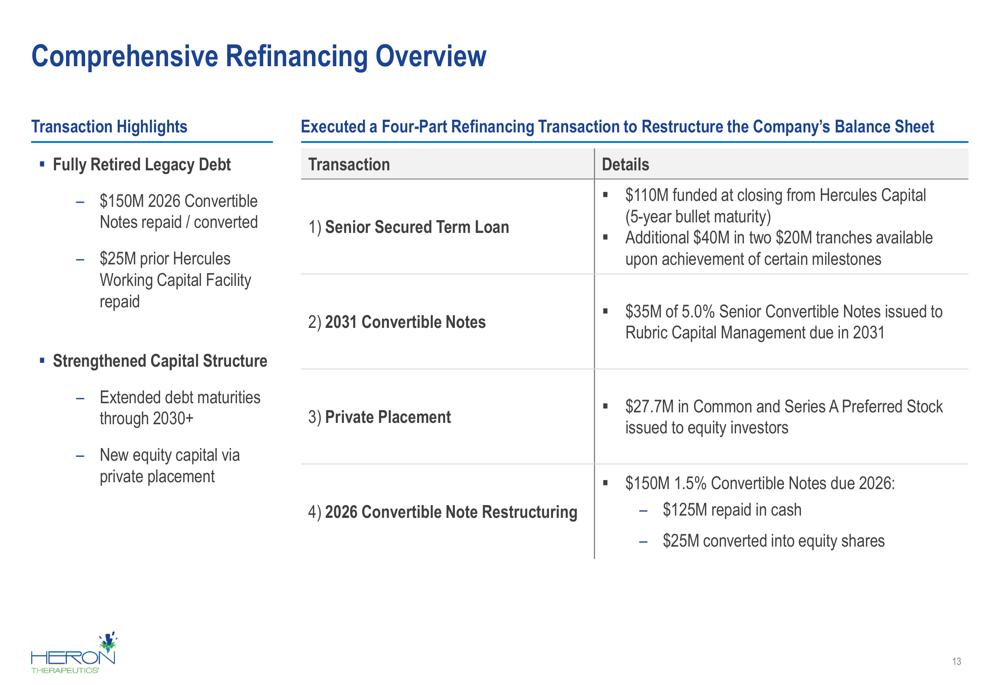

A key development during the quarter was Heron’s comprehensive refinancing, which reduced total debt from $175 million to $145 million while extending maturities beyond 2030. The four-part transaction included a new senior secured term loan, convertible notes, a private placement, and restructuring of existing convertible notes:

The company also secured a permanent, product-specific J-code (J0688) for ZYNRELEF, effective October 1, 2025, which should streamline the reimbursement process and potentially accelerate adoption. Additionally, Heron launched a dedicated APONVIE sales team on July 1, consisting of six representatives focused on high-potential hospital accounts.

Forward-Looking Statements

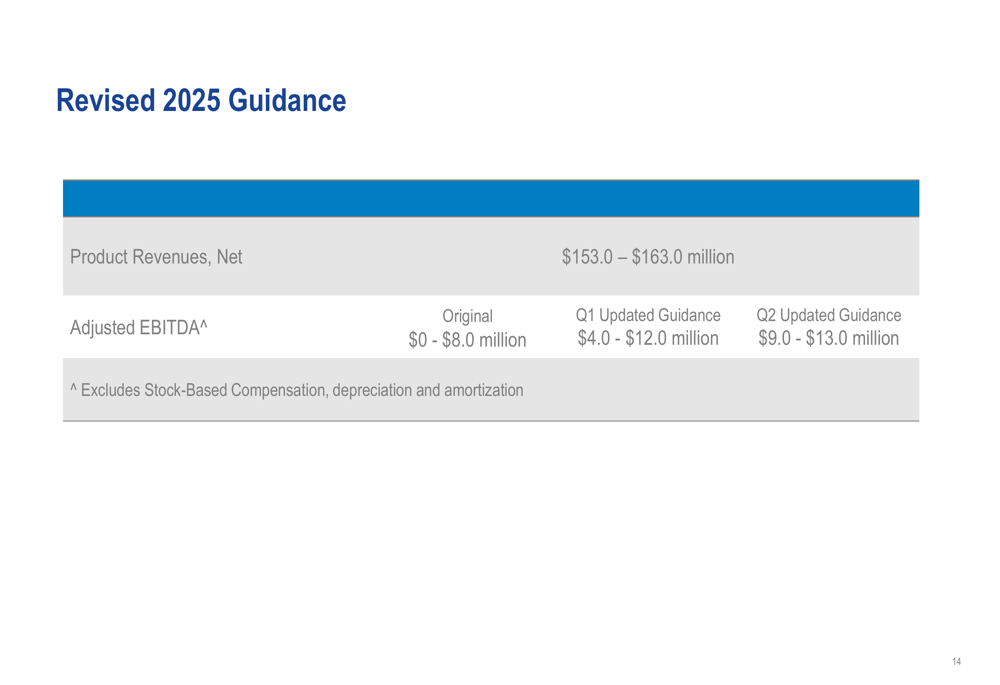

Heron raised its 2025 guidance for the second consecutive quarter, now projecting product revenues of $153-$163 million and adjusted EBITDA of $9-$13 million. This represents a significant increase from the original adjusted EBITDA guidance of $0-$8 million and the Q1 updated guidance of $4-$12 million:

The company highlighted several key achievements and updates that position it for continued growth:

Market Reaction and Outlook

Despite the improved operational metrics and raised guidance, Heron’s stock fell sharply following the earnings release. The 24.18% decline suggests investors may be concerned about the company’s cash burn rate, ongoing net losses, and the sustainability of its path to profitability.

This reaction contrasts with the previous quarter’s performance, when Heron’s stock surged 10.8% after reporting Q1 2025 earnings that included a surprise profit of $0.01 per share. The current quarter’s return to net loss territory, despite positive adjusted EBITDA, appears to have dampened investor enthusiasm.

Looking ahead, Heron’s ability to continue growing product revenues while managing expenses will be critical to achieving sustainable profitability. The debt refinancing provides financial flexibility, but the declining cash position will likely remain a focus for investors in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.