Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Hexagon Composites (OB:HEX) reported a challenging second quarter of 2025 with significant revenue decline but emphasized strategic progress and building commercial momentum, according to the company’s presentation delivered on August 14, 2025.

Quarterly Performance Highlights

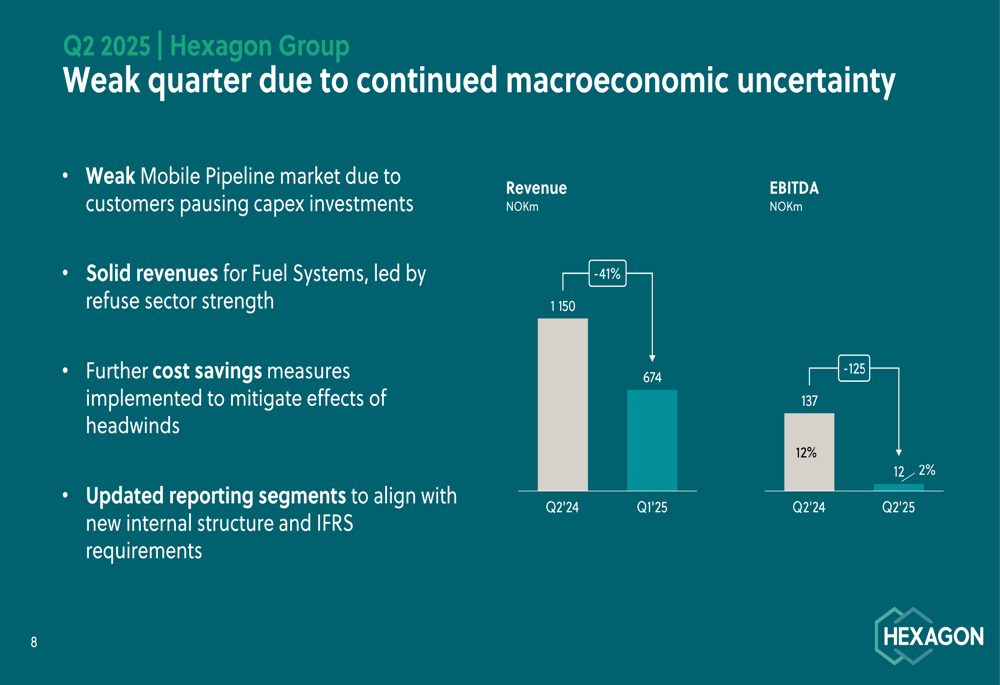

Hexagon Composites experienced a substantial downturn in its financial performance during Q2 2025, with revenue falling to NOK 674 million, representing a 41% decline compared to NOK 1,150 million in Q2 2024. The company’s EBITDA plummeted to NOK 12 million from NOK 137 million in the same period last year, resulting in an EBITDA margin of just 2%.

As shown in the following chart detailing the group’s financial results:

The company attributed this weak performance primarily to continued macroeconomic uncertainty affecting customer spending decisions. This represents a significant deterioration from Q1 2025, when the company maintained stable year-over-year revenue but experienced a decline in EBITDA margin to 5%.

CEO Philipp Schramm summarized the quarter as one where the company "navigated a weak quarter with strategic progress and momentum building," highlighting that while macro-economic headwinds severely impacted Q2 results, the company is taking decisive actions with cost-savings measures and strategic initiatives.

Segment Performance Analysis

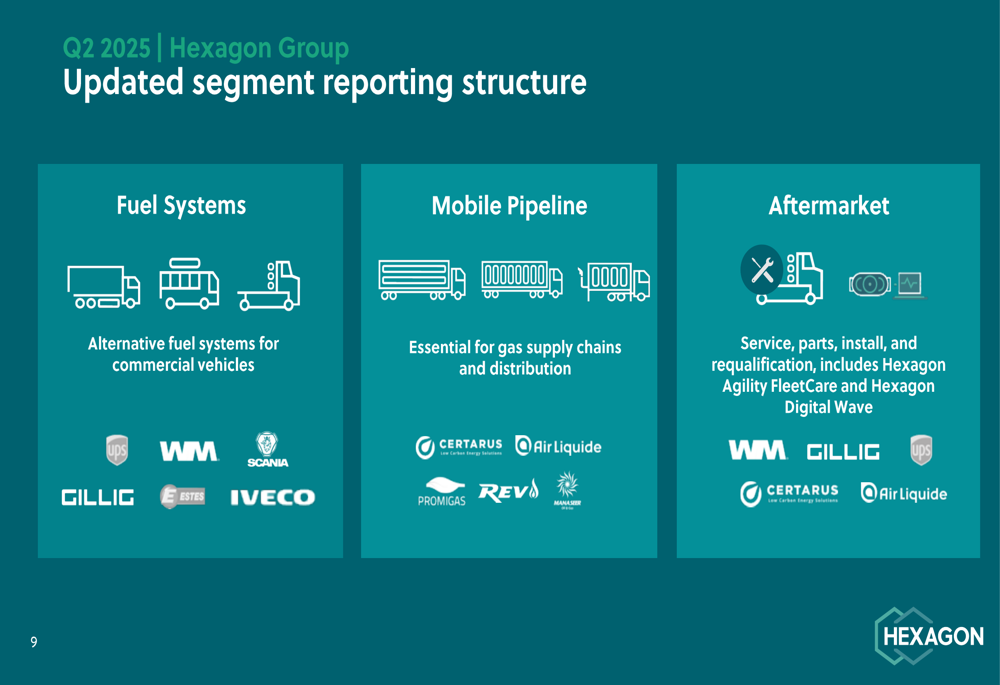

Hexagon has updated its segment reporting structure to focus on three key areas: Fuel Systems, Mobile Pipeline, and Aftermarket. This restructuring aims to provide greater transparency into the performance of each business area.

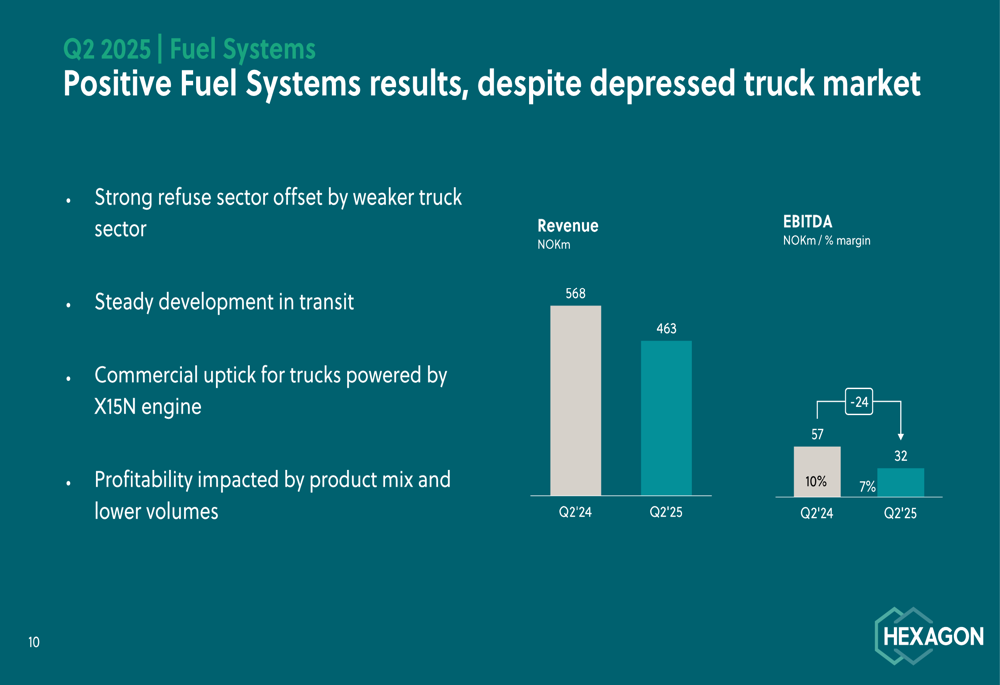

The Fuel Systems segment, which includes solutions for transit buses and trucks, showed relative resilience with revenue of NOK 463 million, down from NOK 568 million in Q2 2024. The segment maintained a 7% EBITDA margin, compared to 10% in the prior year period. Management noted that strong performance in the refuse sector helped offset weakness in the broader truck market.

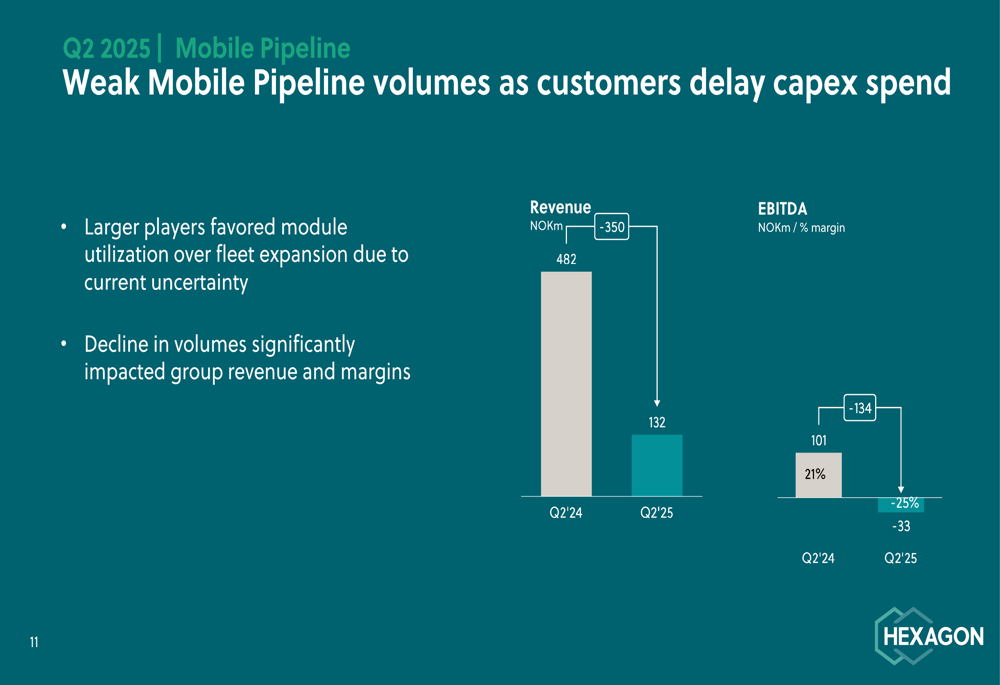

The Mobile Pipeline segment was hardest hit, with revenue dropping to NOK 132 million from NOK 482 million in Q2 2024. This segment, which enables the transportation of compressed natural gas where pipelines don’t exist, swung to a negative EBITDA margin of -25%, compared to a positive 21% margin in the prior year. The company explained that larger customers were favoring module utilization over fleet expansion, significantly impacting both group revenue and margins.

The Aftermarket segment, which includes services and parts, maintained stable revenue at NOK 109 million year-over-year but saw its EBITDA margin decline to 3% from 12% in Q2 2024. This was primarily due to reduced inspection and requalification activities for Mobile Pipeline trailers and lower sales of cylinder inspection machines.

Strategic Initiatives

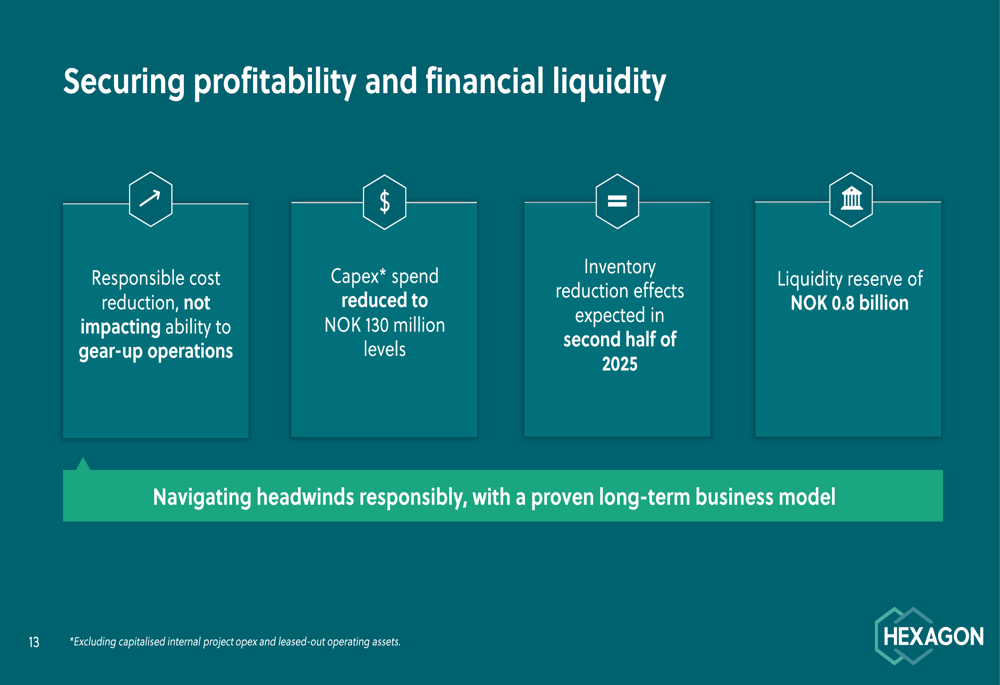

Despite the challenging quarter, Hexagon highlighted several strategic initiatives aimed at positioning the company for future growth. The company emphasized its responsible approach to navigating current headwinds, including cost reduction measures, reduced capital expenditure, and inventory management to improve cash flow. Hexagon maintains a liquidity reserve of NOK 0.8 billion.

A key strategic move during the quarter was the acquisition of SES Composites, strengthening Hexagon’s European footprint. The company is taking 100% ownership of SES, a significant supplier to European transit bus OEMs, from its previous 49% minority shareholding. The transaction, valued at EUR 6.1 million, was settled using Hexagon Composites and Hexagon Purus shares. SES Composites is expected to generate 2025 revenue of EUR 33 million and EBITDA of EUR 2 million.

Hexagon also extended its strategic alliance agreement with Mitsui & Co. through 2030. Mitsui has been a key strategic partner and shareholder since 2016 and has been instrumental in the development of the Hexagon Group.

On the commercial front, the company secured new orders that signal potential future growth. These include an inaugural order from Watani to deliver Mobile Pipeline modules for compressed natural gas delivery across Jordan, and fuel systems for 160 heavy-duty trucks powered by the X15N engine, described as the "largest natural gas fuel system configuration ever installed across Americas."

Outlook and Forward-Looking Statements

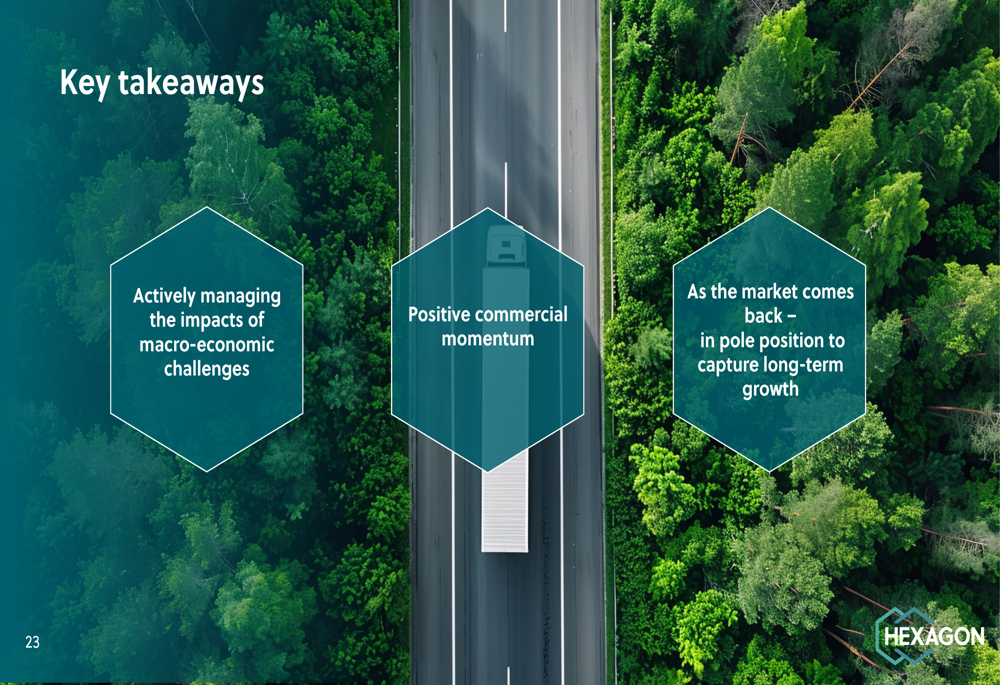

Looking ahead, Hexagon emphasized three key takeaways: actively managing the impacts of macro-economic challenges, positive commercial momentum building, and positioning to capture long-term growth when the market recovers.

The company highlighted continued regulatory support for natural gas in the US, including the extension of renewable natural gas (RNG) support until 2029 through what they termed the "Big Beautiful Bill," and the EPA maintaining NOx standards. This regulatory environment is expected to provide a supportive backdrop for the company’s products and services.

Hexagon’s management remains confident in the company’s long-term growth potential, emphasizing that they have "already invested in capacity" and are "well positioned to deliver future growth" across the full value chain of natural gas, where they claim to be "#1 in its markets."

However, the company’s leverage ratio has increased slightly to 2.9x following the weaker operating performance, indicating some financial pressure. With available liquidity of approximately NOK 0.8 billion at the end of the quarter, Hexagon appears to have sufficient resources to navigate the current challenging environment while pursuing strategic opportunities.

The presentation suggests that while Hexagon faces significant near-term challenges, the company is taking appropriate measures to manage costs and liquidity while positioning itself to benefit from an eventual market recovery and the ongoing transition to cleaner energy solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.