Gold prices rise on economic uncertainty; cooling rate cut bets limit upside

Introduction & Market Context

Hiab, the global load handling specialist recently spun off from Cargotec, presented its Q1 2025 investor slides outlining its strategy as a standalone company. The presentation highlighted Hiab’s strong market position across all product segments, consistent historical growth, and ambitious targets for 2028.

With 2024 sales of 1,647 MEUR and a comparable operating profit margin of 13.2%, Hiab has established itself as a leader in essential industries including construction, waste management, defense logistics, and retail. The company’s asset-light business model spans over 3,000 service locations across 100 countries, with particularly strong presence in Europe (49% of sales) and North America (42%).

Market Position & Product Portfolio

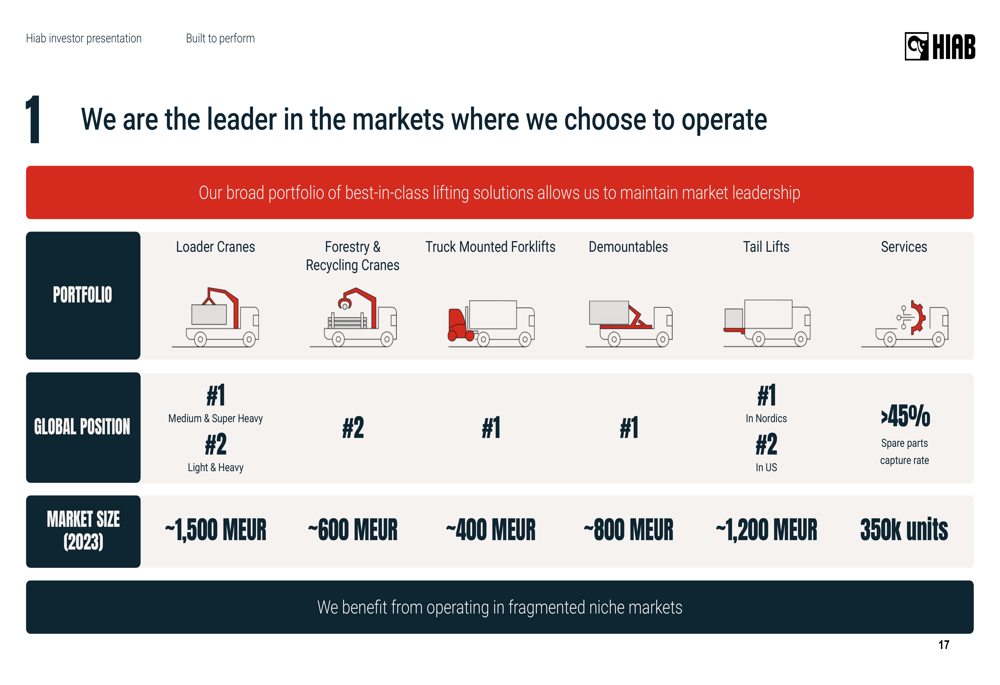

Hiab maintains market leadership positions across its diverse product portfolio, holding either #1 or #2 positions in all segments. The company’s extensive brand portfolio includes loader cranes (HIAB, ARGOS, EFFER), forestry & recycling cranes (JONSERED, LOGLIFT), truck mounted forklifts (MOFFETT, PRINCETON), demountables (MULTILIFT, GALFAB), and tail lifts (ZEPRO, WALTCO, DEL).

As shown in the following market leadership breakdown, Hiab commands significant market share across its product categories:

The company serves a diverse customer base across infrastructure & construction, wholesale & retail, forestry & agriculture, and rental sectors. This diversity provides resilience, with the top 10 customers representing only approximately 13% of total sales.

Financial Performance

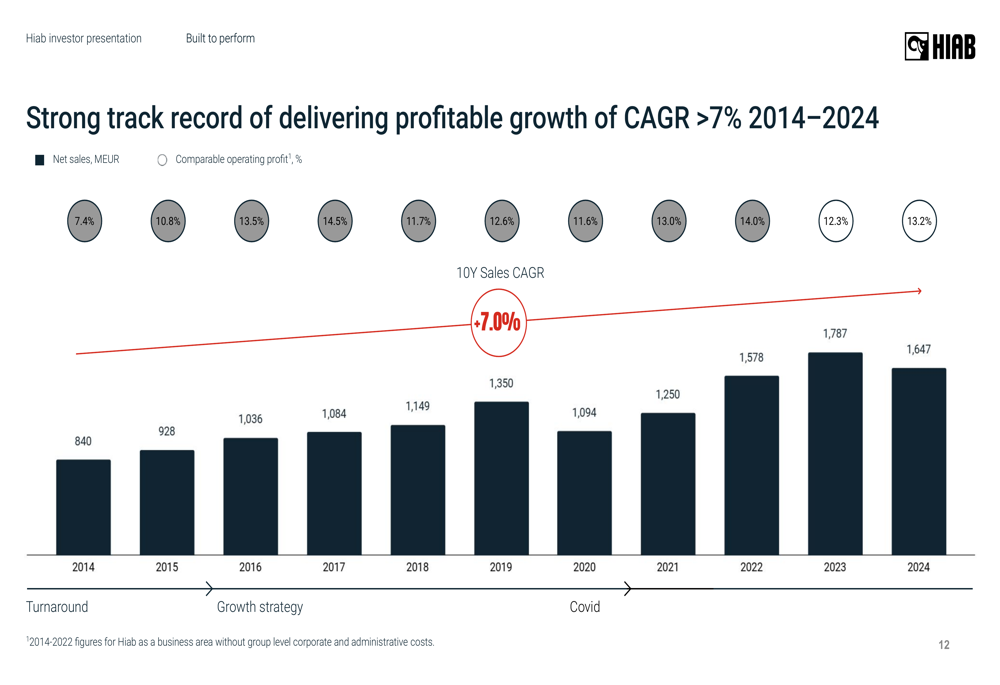

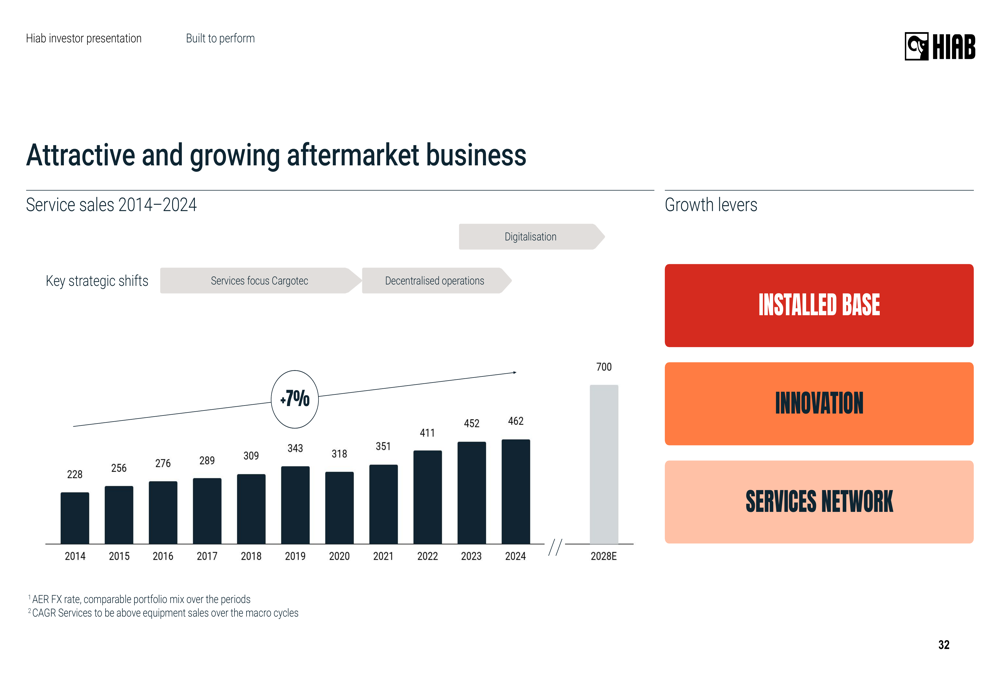

Hiab has demonstrated consistent growth over the past decade, with a 10-year sales CAGR of 7.0%. The company’s financial profile is characterized by strong profitability (13.2% operating margin) and exceptional return on operating capital (30.5%).

The following chart illustrates Hiab’s track record of profitable growth from 2014 to 2024:

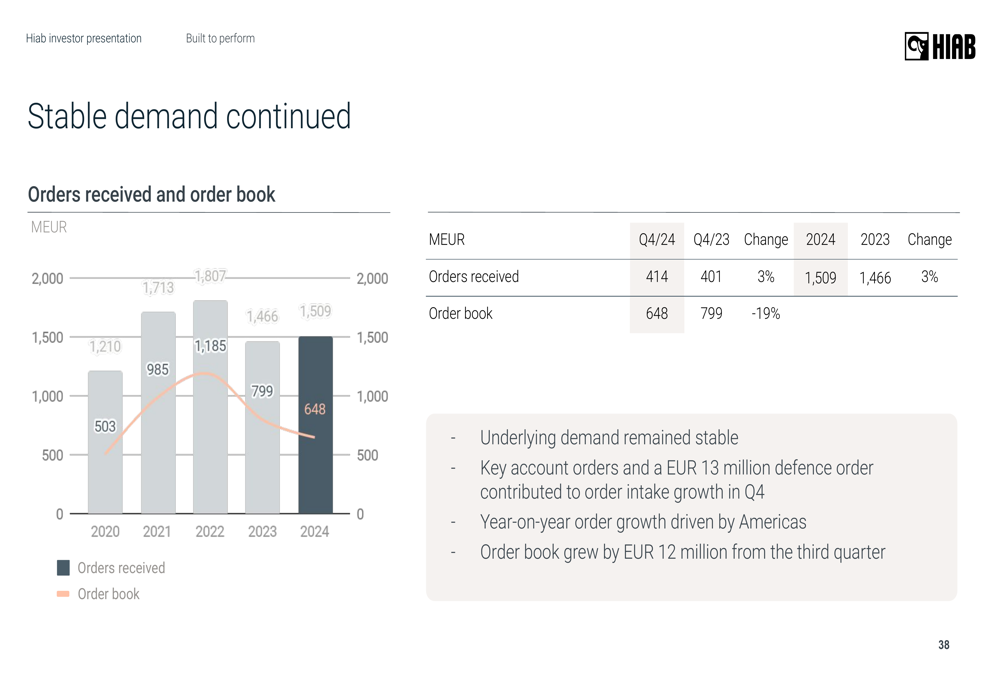

Despite recent market challenges, Hiab maintained stable demand in Q4 2024, with order intake growth supported by key account orders and a EUR 13 million defense order. While equipment sales declined as order books normalized, service sales continued to grow, demonstrating the resilience of Hiab’s business model.

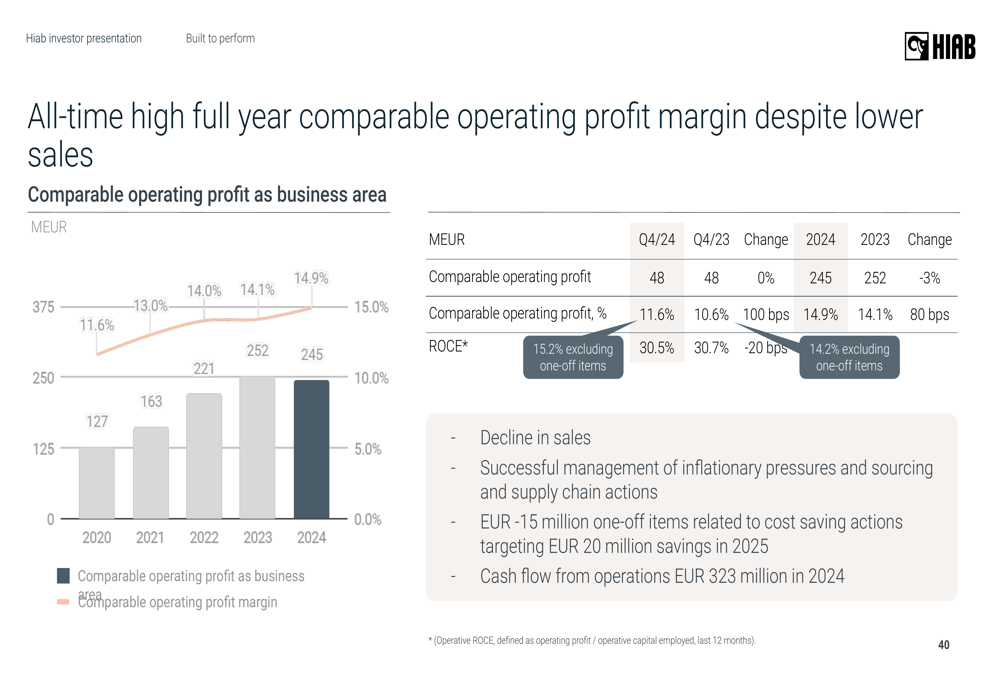

The company achieved an all-time high full-year comparable operating profit margin despite lower sales, showcasing effective cost management and operational efficiency. For 2025, Hiab aims to implement EUR 20 million in cost savings.

Growth Strategy

Hiab’s growth strategy focuses on three key pillars: expanding in North America, growing the service business, and investing in innovation.

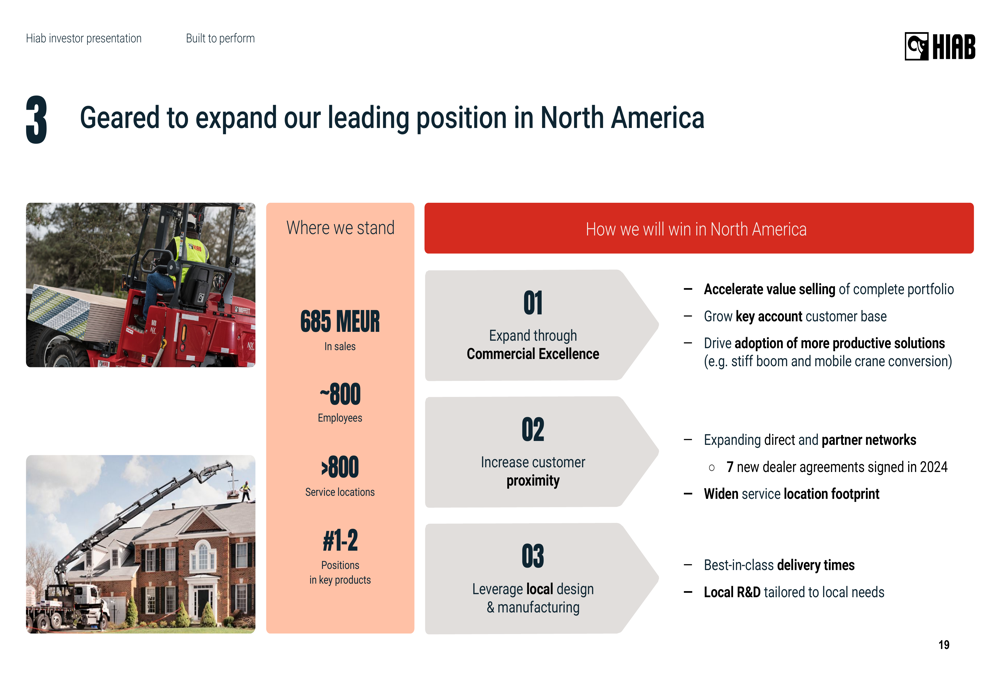

North America represents a significant growth opportunity, with Hiab already generating 685 MEUR in sales through approximately 800 employees and over 800 service locations. The company plans to accelerate value selling, grow key accounts, increase customer proximity, and leverage local design and manufacturing capabilities.

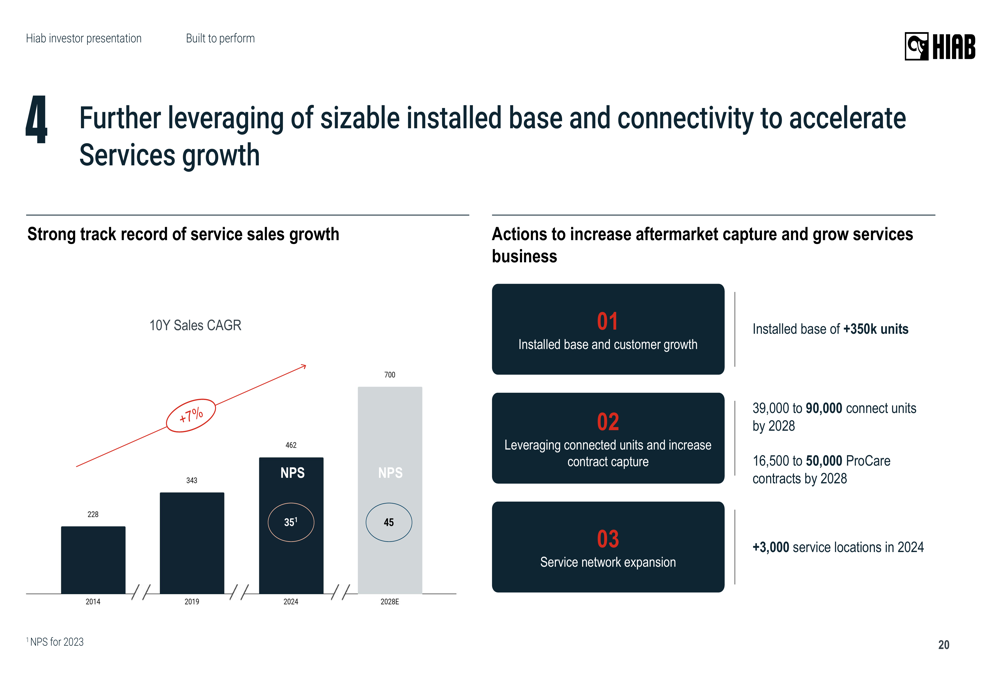

In services, Hiab aims to further leverage its sizeable installed base by increasing part capture rates, procare contracts, and connected fleet. The company has already made substantial progress, growing part capture rates from 43% to 47% and more than doubling both procare contracts and connected fleet units between 2020 and 2023.

To drive innovation, Hiab plans to double its R&D investments, focusing on sustainability solutions, addressing operator shortages, increasing productivity and safety, and optimizing weight-to-payload ratios. This increased investment will be funded by reallocating costs from indirect and administrative functions to sales, marketing, and R&D.

2028 Targets

Hiab has set ambitious targets for 2028, including:

- Sales CAGR >7%

- Comparable operating profit margin of 16%

- Return on capital employed (ROCE) >25%

- Sustainability targets aligned with Science Based Targets initiative (SBTi)

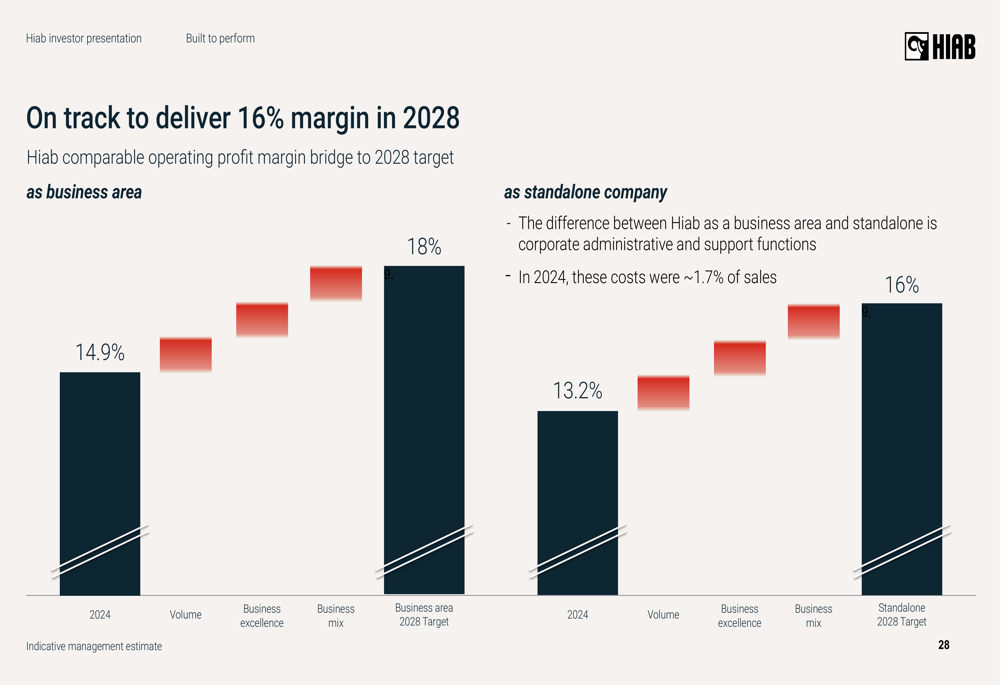

The company’s path to achieving 16% operating margin by 2028 is illustrated in the following bridge chart:

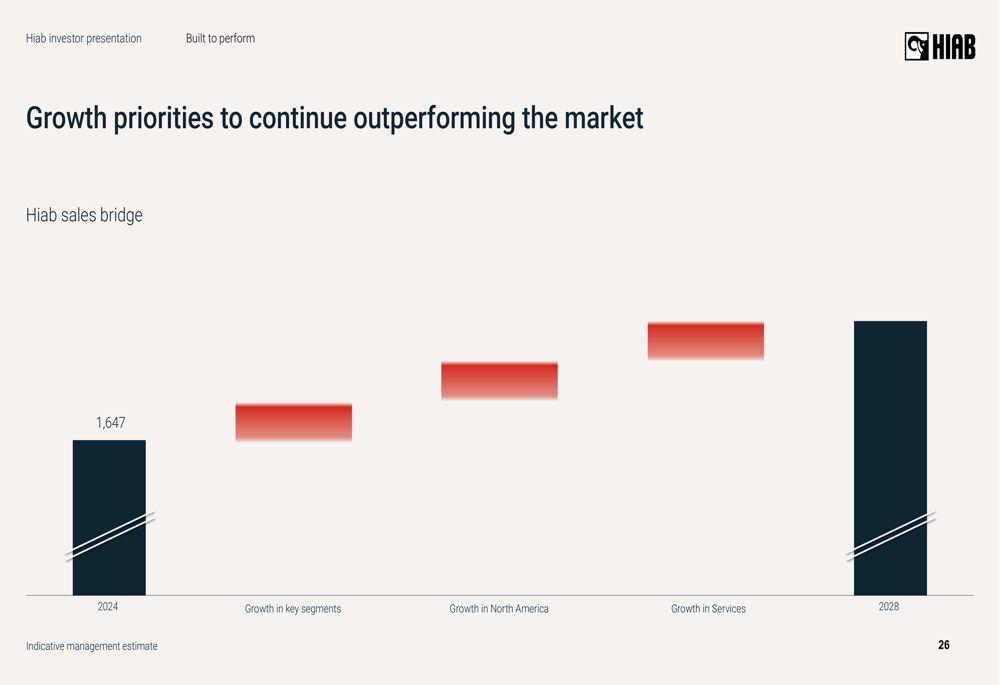

Growth priorities to outperform the market include focusing on key segments (waste & recycling, defense logistics, retail & last mile, and construction), expanding in North America, and growing service revenues.

Outlook & Investment Case

For 2025, Hiab estimates its comparable operating profit margin will be above 12.0%. The company’s decentralized business model is expected to deliver productivity gains of approximately 1.5% of sales through commercial, sourcing, and manufacturing excellence.

Hiab’s investment case is built on its leading market positions, potential to grow faster than the market, profitability upside, and sustainable value creation. The company has a proven track record of successful M&A, having acquired ARGOS, EFFER, Galfab, and Olsbergs in recent years to expand its geographic reach and product portfolio.

The aftermarket business represents a particularly attractive growth opportunity, with digital sales increasing and service sales steadily climbing. By 2028, Hiab aims to increase its part capture rate to 53%, triple its procare contracts to 50,000, and more than double its connected fleet to 90,000 units.

As Hiab transitions to a standalone company following its separation from Cargotec, it brings a strong financial profile with further value creation potential through both organic growth and strategic acquisitions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.