Bitcoin price today: surges to $122k, near record high on US regulatory cheer

Introduction & Market Context

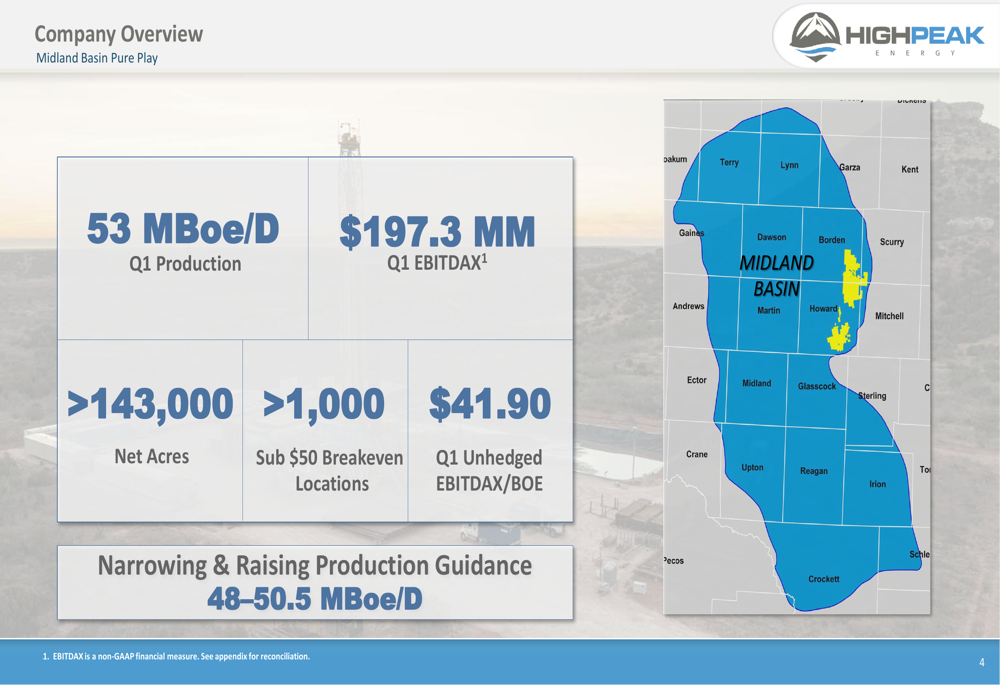

HighPeak Energy (NASDAQ:HPK) revealed strong operational results in its Q1 2025 investor presentation, highlighting production increases and efficiency gains despite plans to temporarily reduce drilling activity. The Midland Basin-focused producer reported Q1 production of 53 MBoe/d, exceeding the high end of its annual guidance range of 48-50.5 MBoe/d.

The presentation comes after a challenging period for the company, whose stock has struggled in recent months. HPK shares closed at $9.14 on May 12, 2025, up 8.75% for the day but still near their 52-week low of $7.82, reflecting broader concerns about energy sector profitability in the current price environment.

Quarterly Performance Highlights

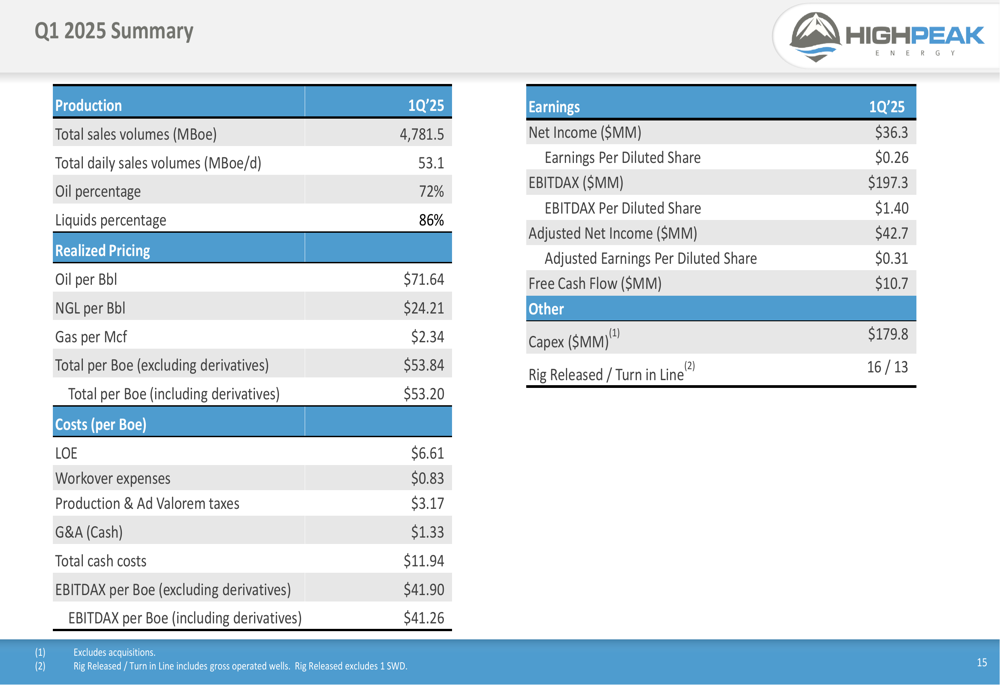

HighPeak reported solid Q1 2025 financial and operational results, with total sales volumes reaching 4,781.5 MBoe (53.1 MBoe/d). The company’s production remains heavily oil-weighted at 72%, with total liquids comprising 86% of output. This favorable production mix helped drive an EBITDAX of $197.3 million for the quarter, translating to $41.90 per BOE.

The company’s comprehensive Q1 performance data shows strong operational execution despite challenging market conditions:

Net income for Q1 2025 reached $36.3 million, while capital expenditures totaled $179.8 million. The company maintained a reasonable leverage ratio of 1.26x based on Q1 2025 LQA figures, indicating a relatively strong balance sheet compared to many peers in the sector.

Operational Efficiency Improvements

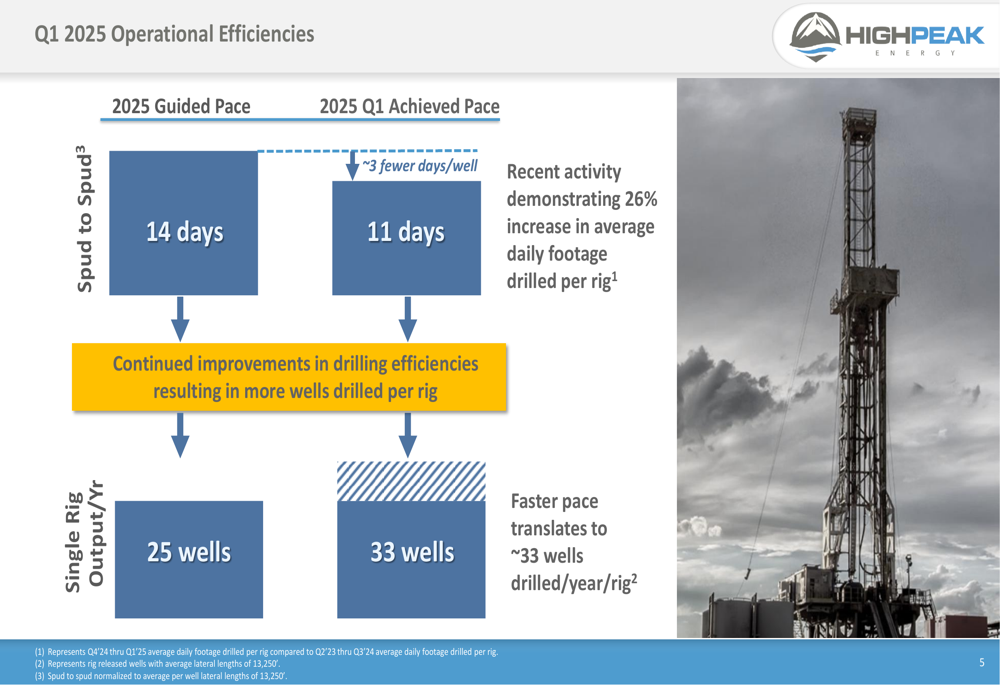

A key highlight of HighPeak’s presentation was the significant improvement in drilling efficiency. The company reduced its drilling time from a guided pace of 14 days spud to spud to an achieved pace of just 11 days, representing a 26% increase in average daily footage drilled per rig.

This efficiency gain has enabled the company to increase its well output from 25 wells to 33 wells per year per rig, creating substantial operational leverage:

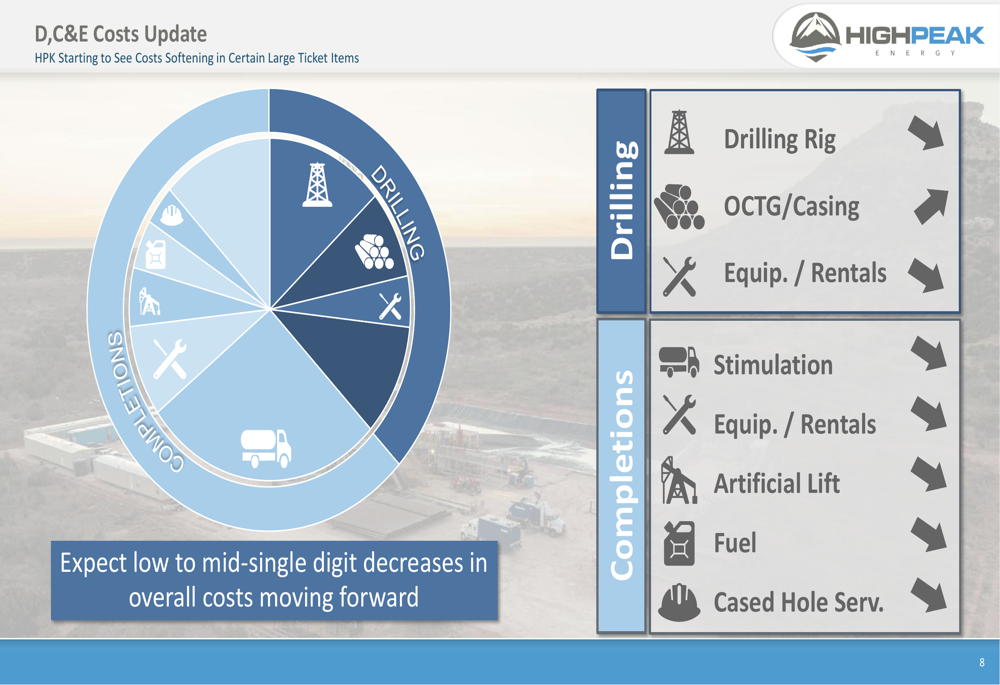

HighPeak also reported progress on cost reduction initiatives, noting that it is "starting to see costs softening in certain large ticket items" with expectations for "low to mid-single digit decreases" in drilling, completion, and equipment costs moving forward.

Strategic Initiatives

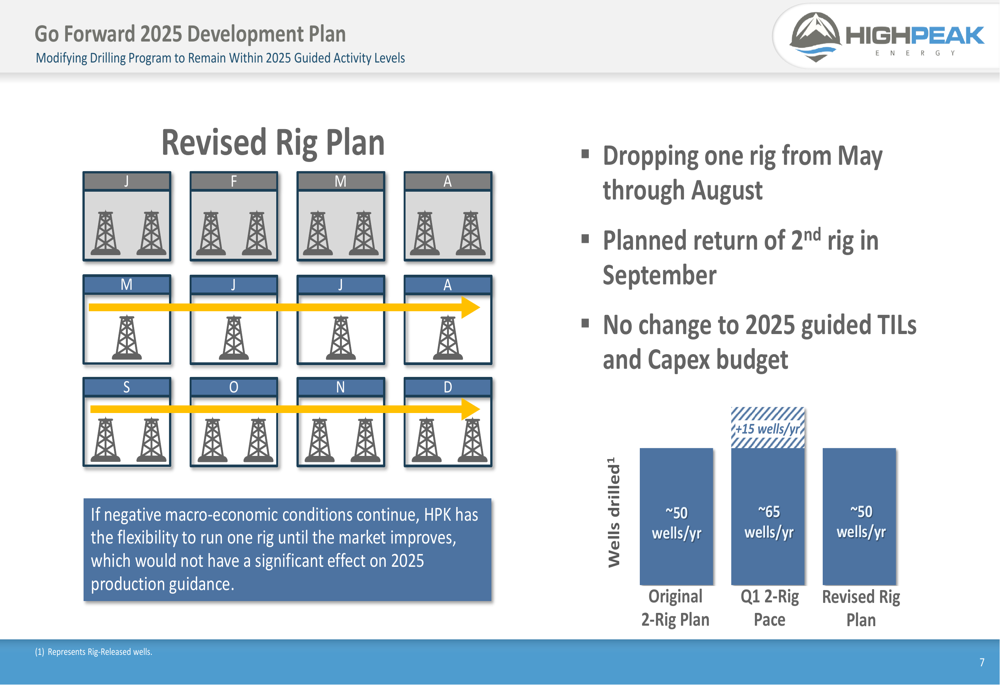

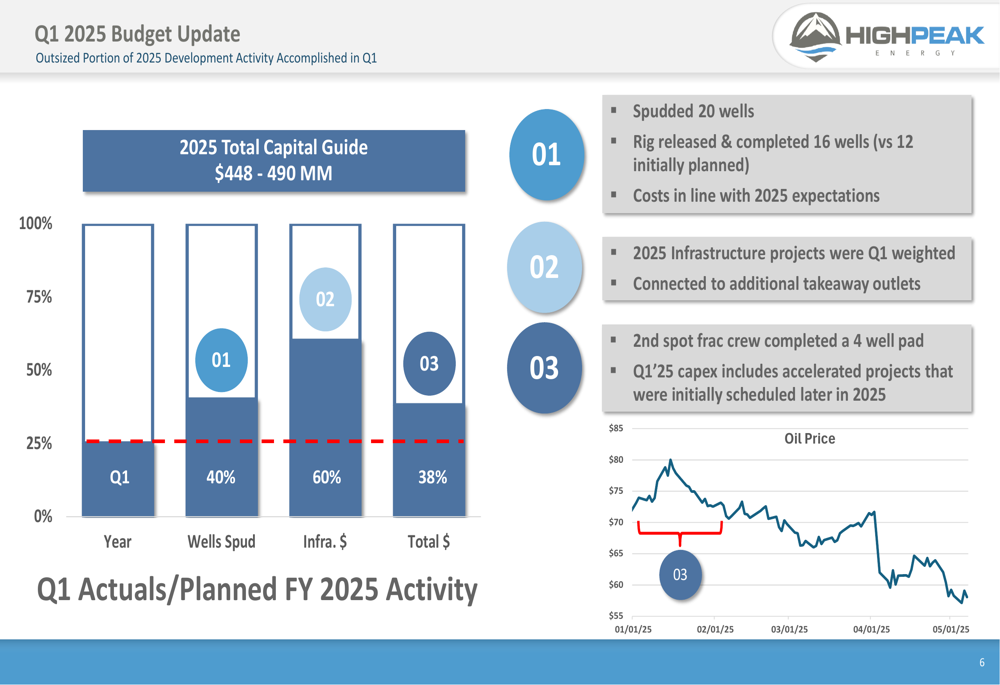

In a significant strategic shift, HighPeak announced plans to modify its 2025 drilling program by temporarily reducing its rig count. The company will drop one rig from May through August before returning to a two-rig program in September. Despite this temporary reduction, management emphasized that there would be no change to the company’s 2025 guided turned-in-line wells or capital expenditure budget of $448-490 million.

This approach aligns with comments made during the company’s Q4 2024 earnings call, where management discussed plans to reduce 2025 capital expenditures by approximately 20% compared to 2024 while targeting flat production. The temporary rig reduction appears to be part of this capital discipline strategy.

The company’s Q1 budget update shows that HighPeak spudded 20 wells and completed 16 wells during the quarter, with costs tracking in line with 2025 expectations:

Competitive Industry Position

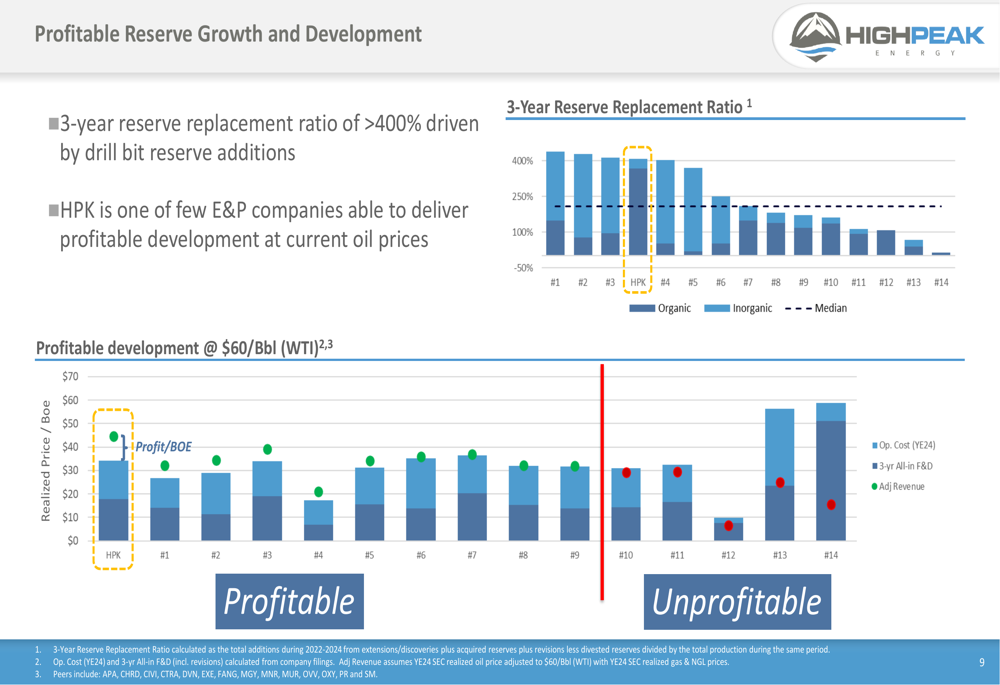

HighPeak emphasized its advantageous position within the industry, highlighting its profitable reserve growth and development capabilities. The company boasts a three-year reserve replacement ratio exceeding 400%, driven primarily by drill bit reserve additions rather than acquisitions.

Management positioned HighPeak as "one of few E&P companies able to deliver profitable development at current oil prices," with economics that work at $60/Bbl WTI:

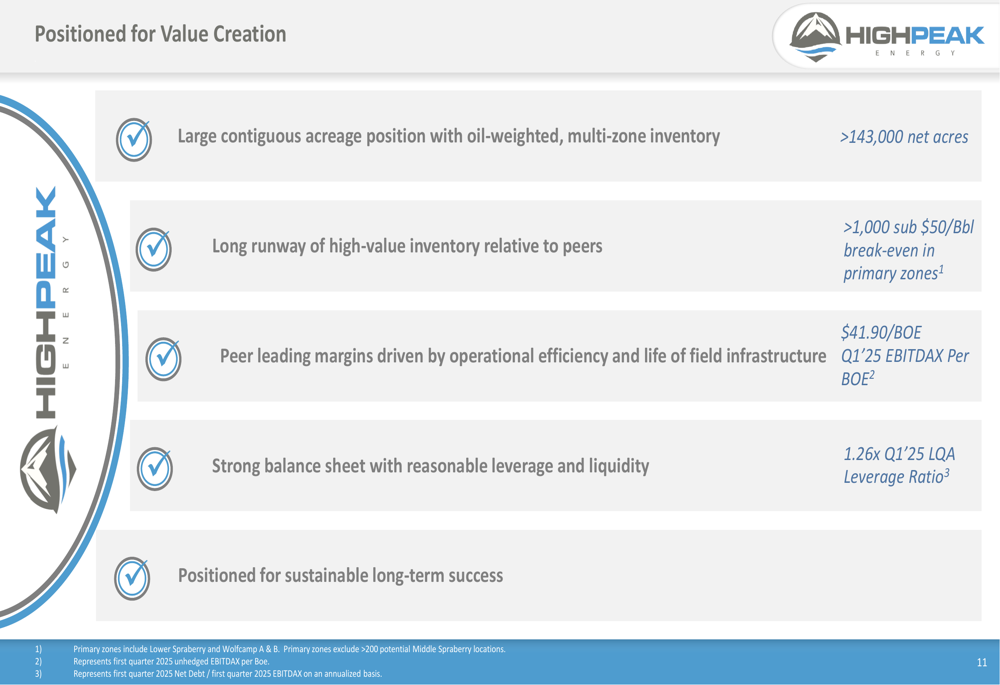

The company’s competitive advantages stem from its large contiguous acreage position of over 143,000 net acres in the Midland Basin, with more than 1,000 drilling locations featuring sub-$50/Bbl breakeven costs. This inventory depth provides a long runway for development compared to many peers.

Forward-Looking Statements

Looking ahead, HighPeak remains focused on value creation through operational excellence and capital discipline. The company has hedged approximately 15.4 MBo/d of oil production and 30,000 MMBtu/d of gas production for the remainder of 2025, providing some price protection in a volatile commodity environment.

The presentation emphasized five key factors positioning the company for future success: its large contiguous acreage position, long runway of high-value inventory, peer-leading margins, strong balance sheet, and sustainable long-term strategy:

While the temporary rig reduction signals caution, management maintained its full-year production guidance of 48-50.5 MBoe/d, suggesting confidence in the company’s ability to deliver consistent results despite the modified drilling schedule.

This measured approach to growth reflects the broader industry trend toward capital discipline and free cash flow generation, particularly following HighPeak’s Q4 2024 earnings report, which showed the company beating EPS expectations but missing revenue forecasts, resulting in negative market reaction at that time.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.