Gold prices hold sharp gains as soft US jobs data fuels Fed rate cut bets

Introduction & Market Context

Huntington Ingalls Industries (NYSE:HII), America’s largest military shipbuilding company, presented its first quarter 2025 financial results on May 1, 2025. The company reported a 2.5% year-over-year revenue decline while maintaining its full-year guidance, suggesting confidence in performance improvement through the remainder of the year.

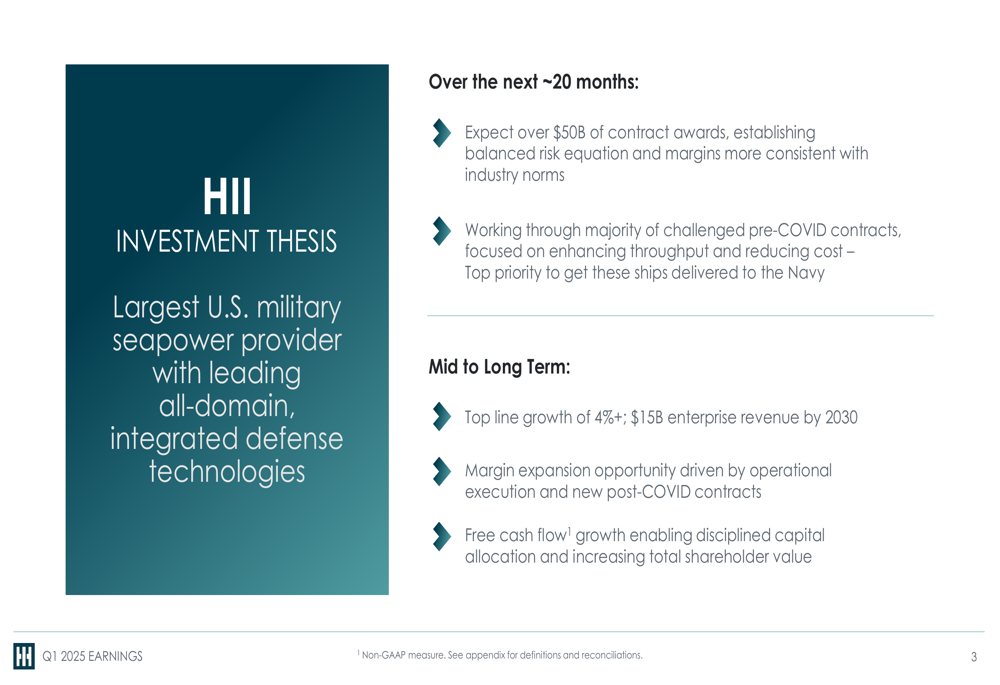

HII positions itself as the "Largest U.S. military seapower provider with leading all-domain, integrated defense technologies" and is currently working through challenged pre-COVID contracts while targeting significant new contract awards. The company’s stock closed at $230.34 on April 30, 2025, and was trading slightly lower in pre-market activity.

Quarterly Performance Highlights

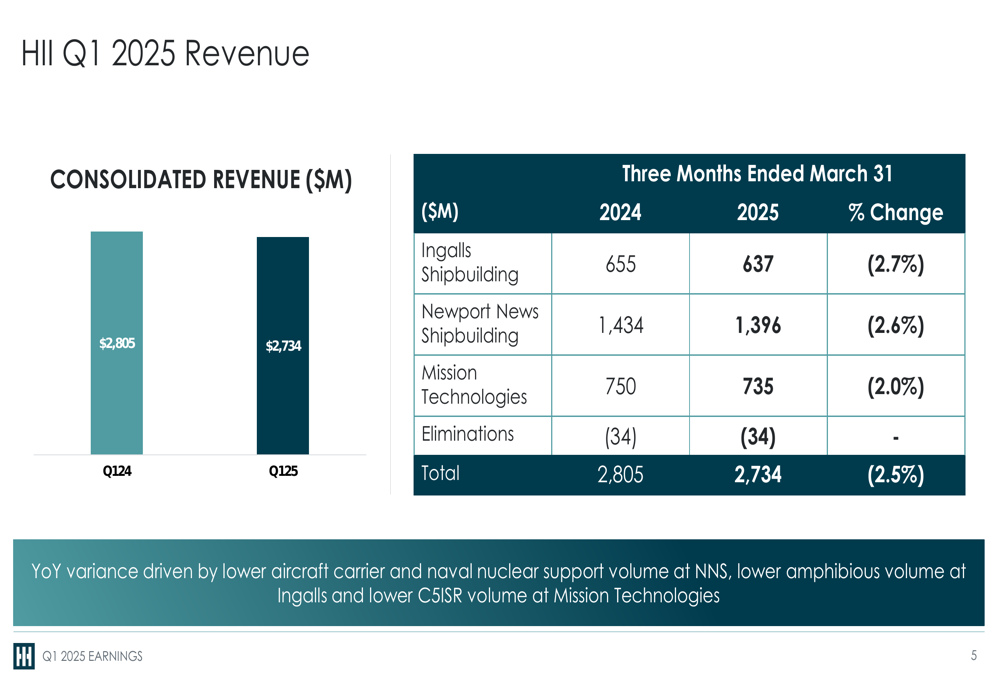

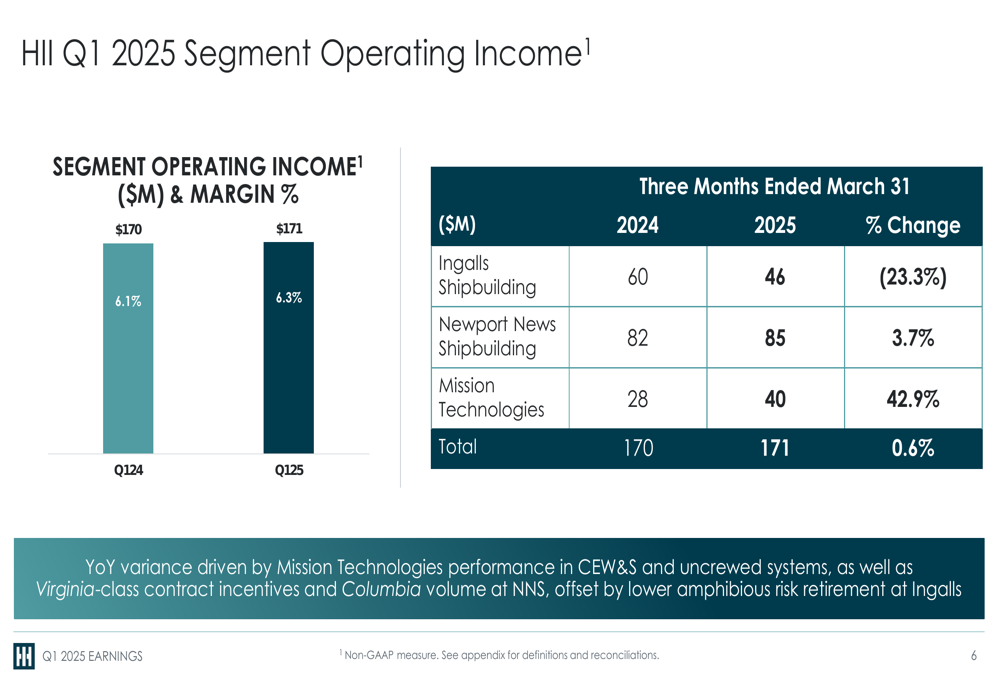

HII reported Q1 2025 revenue of $2,734 million, a 2.5% decrease from $2,805 million in the same quarter last year. Despite the revenue decline, segment operating income increased slightly by 0.6% to $171 million, compared to $170 million in Q1 2024.

The revenue decrease was attributed to "lower aircraft carrier and naval nuclear support volume at Newport News Shipbuilding, lower amphibious volume at Ingalls and lower C5ISR volume at Mission Technologies," according to the company’s presentation.

As shown in the following chart of quarterly revenue performance:

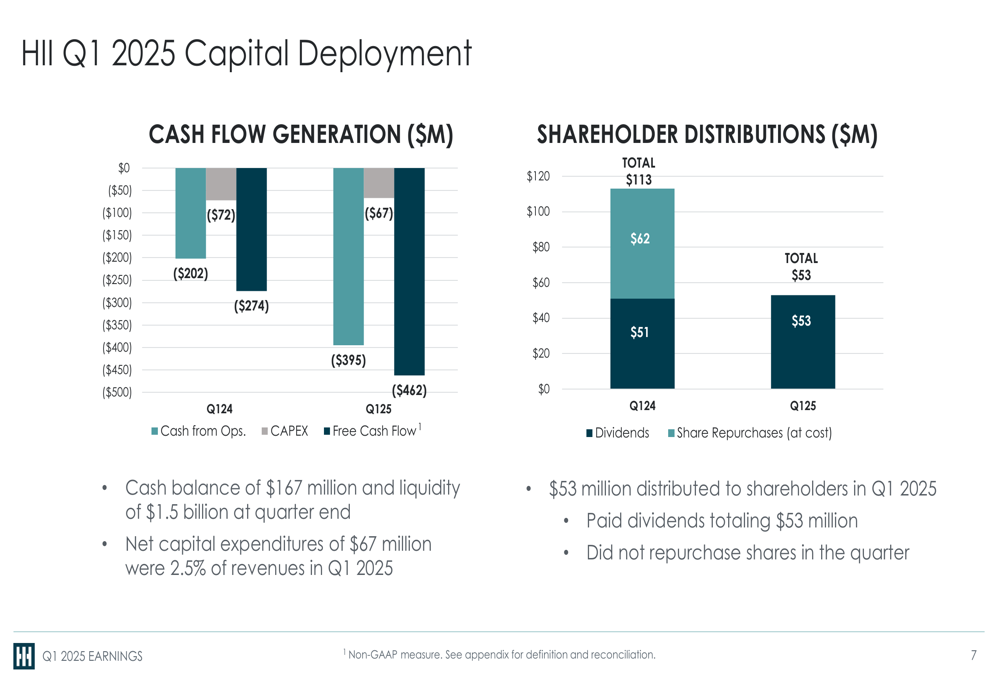

Free cash flow was negative $462 million for the quarter, compared to negative $274 million in Q1 2024. The company maintained its shareholder distributions with $53 million in dividends paid during the quarter.

Segment Analysis

HII’s three business segments showed varying performance in the first quarter:

1. Ingalls Shipbuilding: Revenue decreased 2.7% to $637 million, while operating income declined significantly by 23.3% to $46 million, attributed to "lower amphibious risk retirement."

2. Newport News Shipbuilding: Revenue fell 2.6% to $1,396 million, but operating income increased by 3.7% to $85 million, driven by "Virginia-class contract incentives and Columbia volume."

3. Mission Technologies: Despite a 2.0% revenue decrease to $735 million, this segment emerged as the bright spot with operating income surging 42.9% to $40 million. The company noted strong performance in CEW&S (Cyber, Electronic Warfare & Space) and uncrewed systems.

The following chart illustrates the segment operating income and margin performance:

Mission Technologies’ EBITDA margin improved significantly to 9.1% in Q1 2025 from 7.7% in the same period last year, demonstrating the segment’s growing profitability despite revenue challenges.

Strategic Initiatives

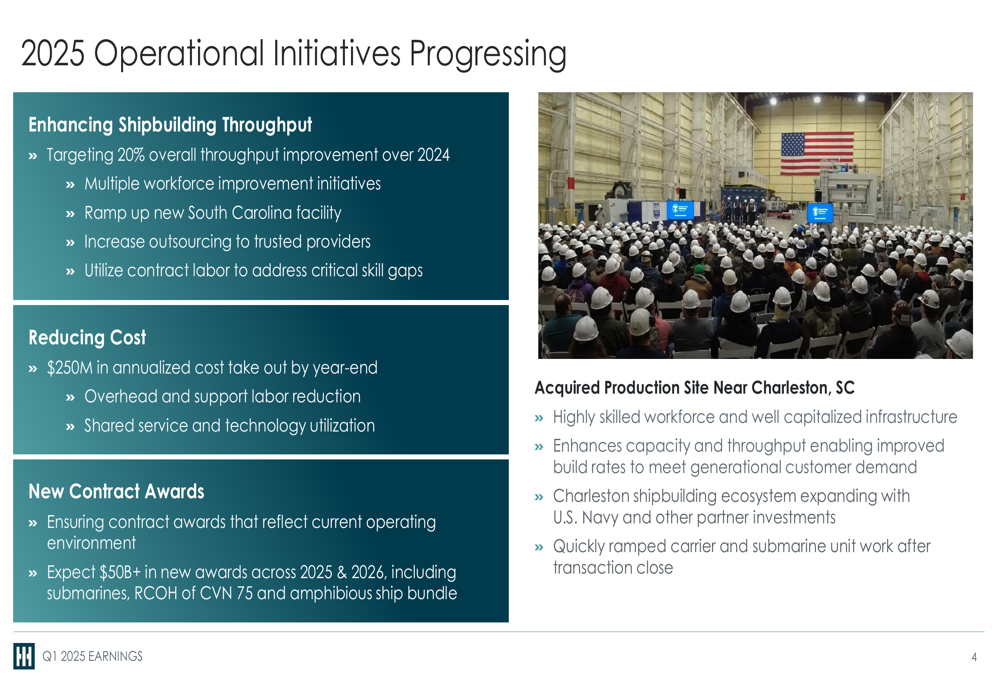

HII outlined several key operational initiatives for 2025 that are already progressing:

1. Enhancing Shipbuilding Throughput: The company is targeting a 20% overall throughput improvement over 2024 through workforce improvement initiatives, ramping up a new South Carolina facility, increasing outsourcing to trusted providers, and utilizing contract labor to address critical skill gaps.

2. Reducing Cost: HII aims to achieve $250 million in annualized cost takeout by year-end through reducing overhead and support labor, and sharing services and technology.

3. New Contract Awards: The company expects over $50 billion in new awards across 2025 and 2026, including submarines, RCOH (Refueling and Complex Overhaul) of CVN 75, and an amphibious ship bundle.

4. Expanded Production Capacity: HII highlighted its newly acquired production site near Charleston, SC, which has "quickly ramped carrier and submarine unit work" since the transaction closed.

As illustrated in the company’s operational initiatives slide:

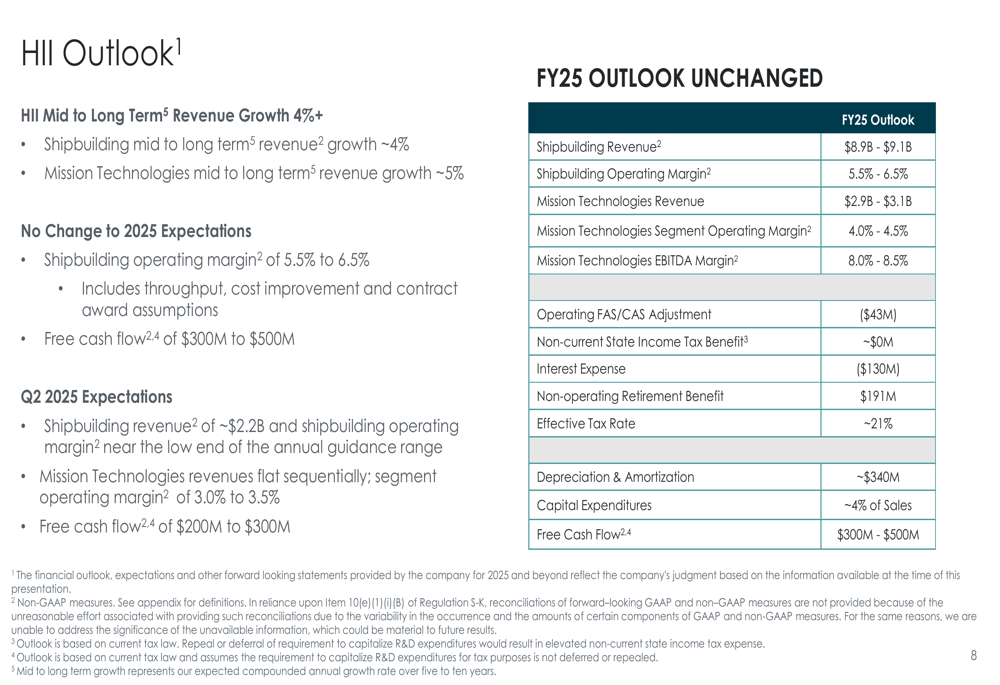

Financial Outlook

HII maintained its full-year 2025 guidance across all metrics, suggesting confidence in its ability to improve performance in the coming quarters despite the Q1 challenges. The outlook includes:

- Shipbuilding Revenue: $8.9-$9.1 billion

- Shipbuilding Operating Margin: 5.5%-6.5%

- Mission Technologies Revenue: $2.9-$3.1 billion

- Mission Technologies Operating Margin: 4.0%-4.5%

- Free Cash Flow: $300-$500 million

The company’s investment thesis emphasizes top-line growth of over 4%, targeting $15 billion in enterprise revenue by 2030, along with margin expansion driven by operational execution and new post-COVID contracts.

As shown in the company’s detailed outlook slide:

The company’s investment thesis highlights both short-term goals for the next ~20 months and mid-to-long-term objectives:

While HII faces near-term challenges with pre-COVID contracts and negative free cash flow in Q1, the maintained guidance and strategic initiatives suggest management expects performance improvement as the year progresses. The strong performance in the Mission Technologies segment, despite revenue headwinds, indicates potential for growth in this higher-margin business area.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.