BofA: Investors pour into bonds, pull back from crypto

Introduction & Market Context

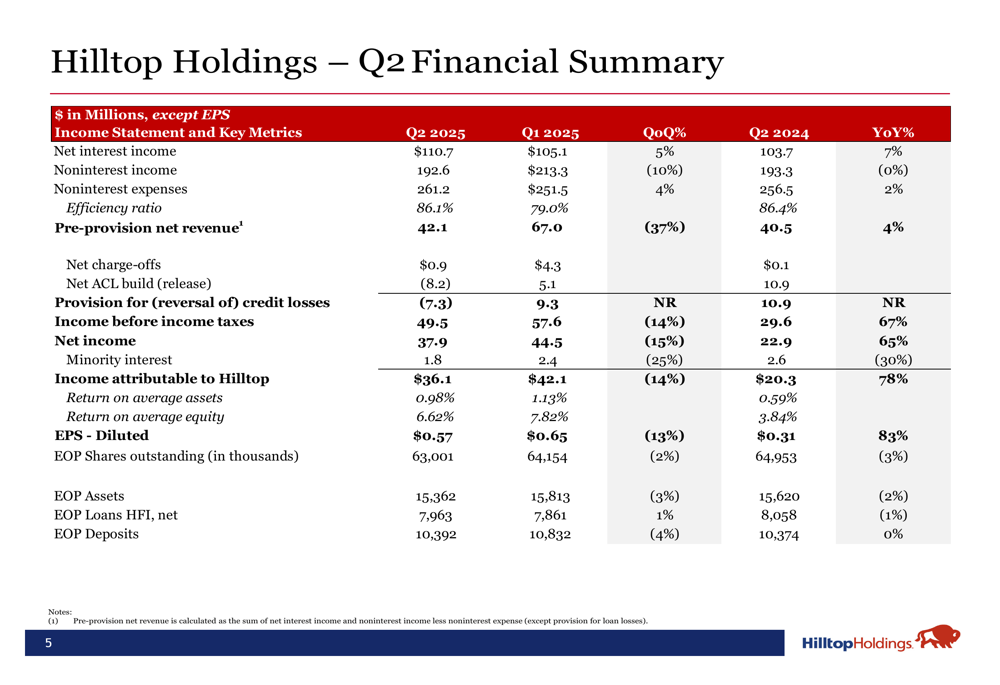

Hilltop Holdings Inc . (NYSE:HTH) presented its second quarter 2025 earnings results on July 25, 2025, reporting net income of $36.1 million and diluted earnings per share of $0.57. The financial services company’s stock closed at $30.59 on the day of the presentation, up 0.78% from the previous close.

The Q2 results represent a sequential decline from the first quarter’s $44.5 million in net income and $0.65 in EPS, but show improvement over the $22.9 million and $0.31 reported in the same quarter last year. The company’s performance was supported by expanding net interest margin and increased mortgage origination volume, though offset by higher noninterest expenses.

Quarterly Performance Highlights

Hilltop’s Q2 2025 financial performance showed mixed results across its three main business segments. The company reported a return on average assets (ROAA) of 0.98% and return on average equity (ROAE) of 6.62%.

PlainsCapital Bank, the company’s banking segment, delivered pre-tax income of $54.9 million, benefiting from an improved net interest margin that increased from 2.97% in Q1 2025 to 3.16% in Q2. The bank also recorded a $7.3 million reversal of credit losses, indicating improved credit quality in the loan portfolio.

As shown in the following quarterly financial summary:

PrimeLending, Hilltop’s mortgage origination business, reported pre-tax income of $3.2 million with origination volume reaching $2.4 billion, a substantial increase of $690 million from the previous quarter. The gain-on-sale margin remained stable at 233 basis points, while non-interest expenses decreased by 2.5%.

HilltopSecurities generated pre-tax income of $6.4 million on net revenue of $109.7 million, resulting in a pre-tax margin of 5.8%. Net revenue increased by $5.4 million compared to the previous quarter.

The company’s results included a nonrecurring $9.5 million pre-tax income ($7.4 million after-tax) related to a legal settlement at PrimeLending, contributing approximately $0.12 to the diluted EPS.

Detailed Financial Analysis

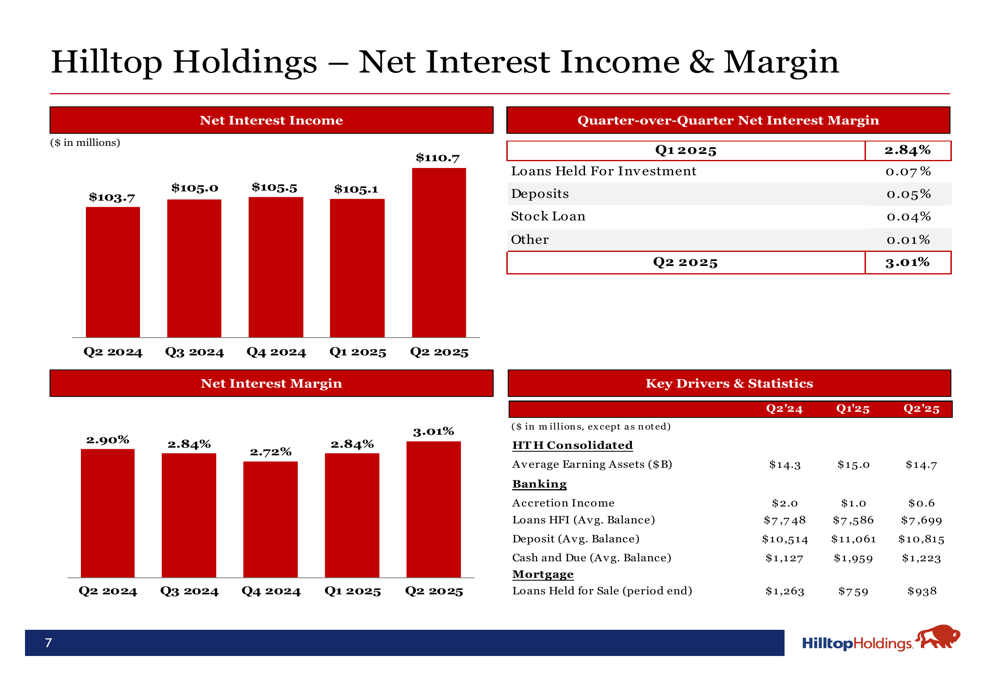

Net interest income rose to $110.7 million in Q2 2025, up from $105.1 million in the first quarter and $103.7 million in the same period last year. The net interest margin expanded to 3.01%, compared to 2.90% in Q2 2024, driven by improved loan yields and stabilizing deposit costs.

The following chart illustrates the improvement in net interest income and margin:

Hilltop’s deposit base remained stable at $10.4 billion, consisting of approximately $7.0 billion in interest-bearing deposits, $2.8 billion in noninterest-bearing deposits, and $0.6 billion in broker-dealer sweep deposits. The company’s deposit mix shows a healthy diversity with 50% in interest-bearing demand accounts, 31% in money market accounts, 16% in savings, and 3% in time deposits.

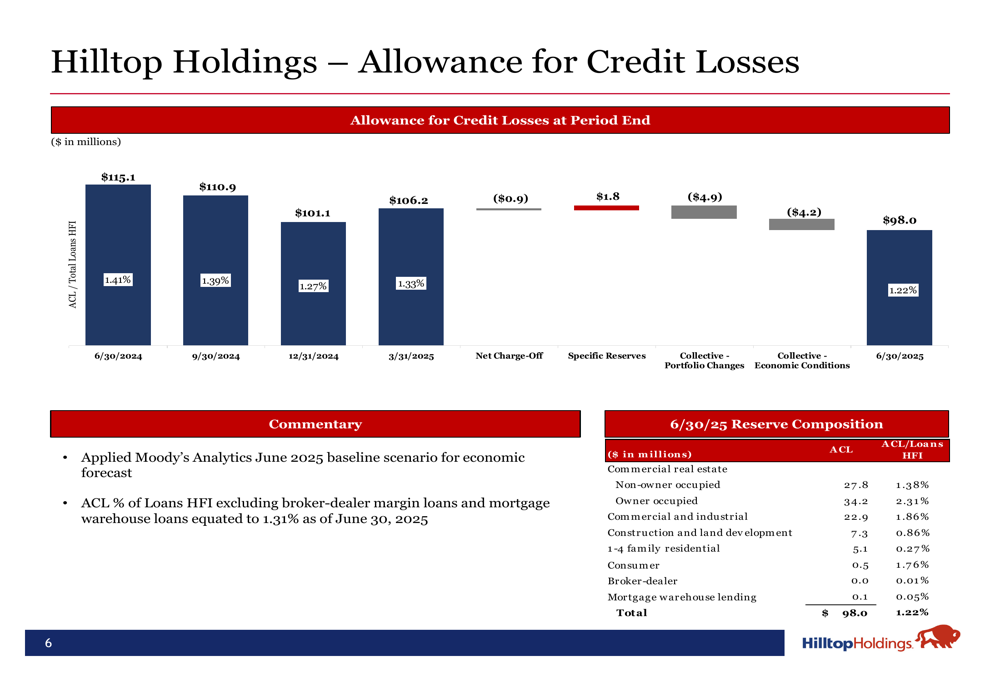

The allowance for credit losses stood at $98.0 million as of June 30, 2025, representing 1.31% of loans held for investment (excluding broker-dealer margin loans and mortgage warehouse loans). This reflects the company’s continued conservative approach to credit risk management.

Capital Management & Shareholder Returns

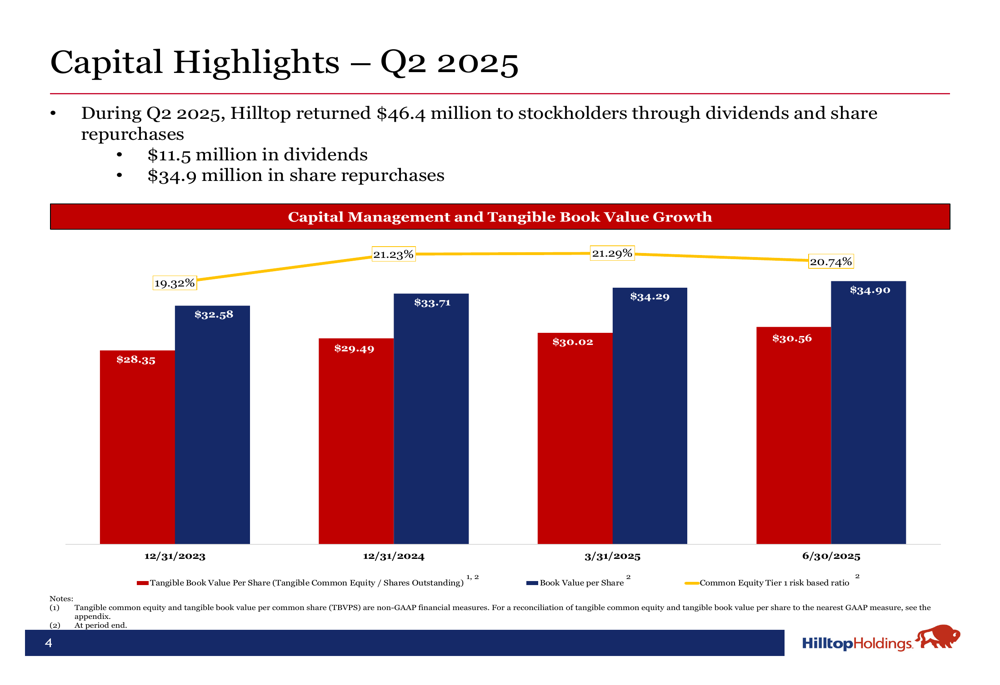

Hilltop maintained its strong capital position while returning significant value to shareholders during the quarter. The company returned $46.4 million to stockholders through a combination of $11.5 million in dividends and $34.9 million in share repurchases.

Tangible book value per share continued its upward trajectory, reaching $30.56 as of June 30, 2025, compared to $30.02 at the end of the first quarter and $29.49 at year-end 2024. This represents a growth rate of 20.74% and reflects the company’s effective capital management strategy.

The following chart shows the consistent growth in tangible book value per share:

Strategic Initiatives & Outlook

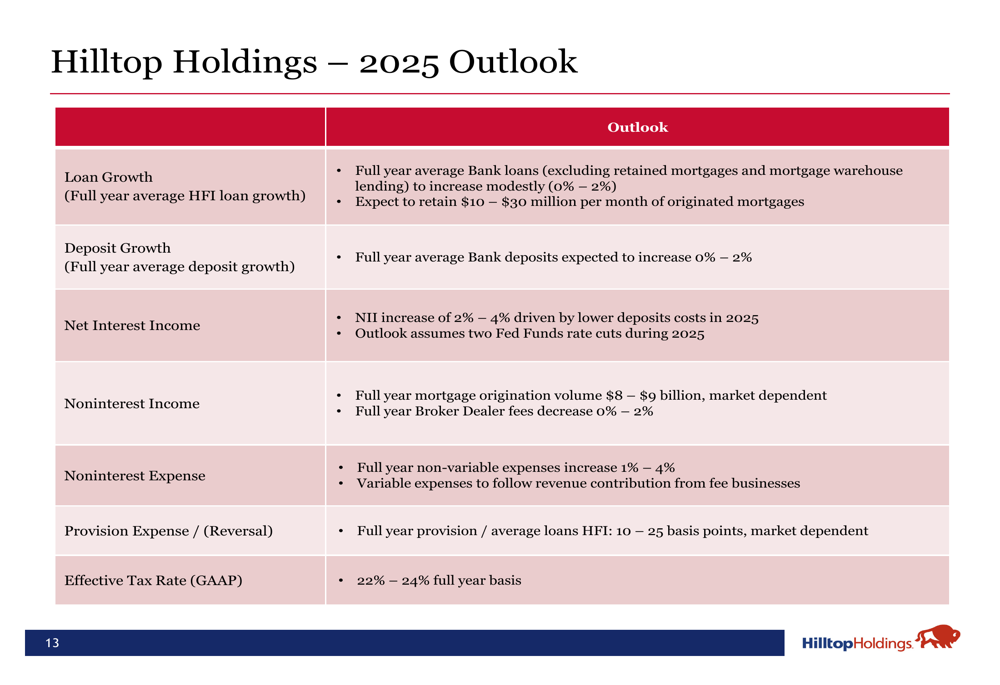

Hilltop Holdings maintained its full-year 2025 outlook, projecting modest growth across key metrics. The company expects average bank loans (excluding retained mortgages and mortgage warehouse lending) to increase by 0-2%, with deposit growth also in the 0-2% range.

Net interest income is forecast to increase by 2-4%, primarily driven by lower deposit costs. For the mortgage business, full-year origination volume is estimated at $8-9 billion, consistent with previous guidance despite the stronger Q2 performance.

The company projects noninterest expenses to increase by 1-4% and anticipates provision expense or reversal to be between 10 and 25 basis points. The effective tax rate is expected to remain between 22% and 24%.

As illustrated in the company’s outlook slide:

Forward-Looking Statements

While Hilltop’s overall financial position remains solid, the company faces several challenges in the coming quarters. The auto lending portfolio, which comprises 1.06% of total bank loans held for investment, continues to experience pressure from higher interest rates and declining used vehicle values.

The commercial real estate portfolio, particularly the office segment which represents approximately 14% of CRE exposure, requires ongoing monitoring given broader market concerns about commercial real estate valuations.

Despite these challenges, Hilltop’s diversified business model, improving net interest margin, and strong capital position provide a foundation for navigating the current economic environment. The company’s active capital management strategy, including share repurchases and dividends, demonstrates management’s commitment to delivering shareholder value while maintaining financial flexibility.

As interest rates potentially stabilize or decline in the coming quarters, Hilltop appears well-positioned to benefit from improved mortgage activity and potentially lower funding costs, though competitive pressures in deposit pricing may continue to impact margins.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.