TSX runs higher on rate cut expectations

Introduction & Market Context

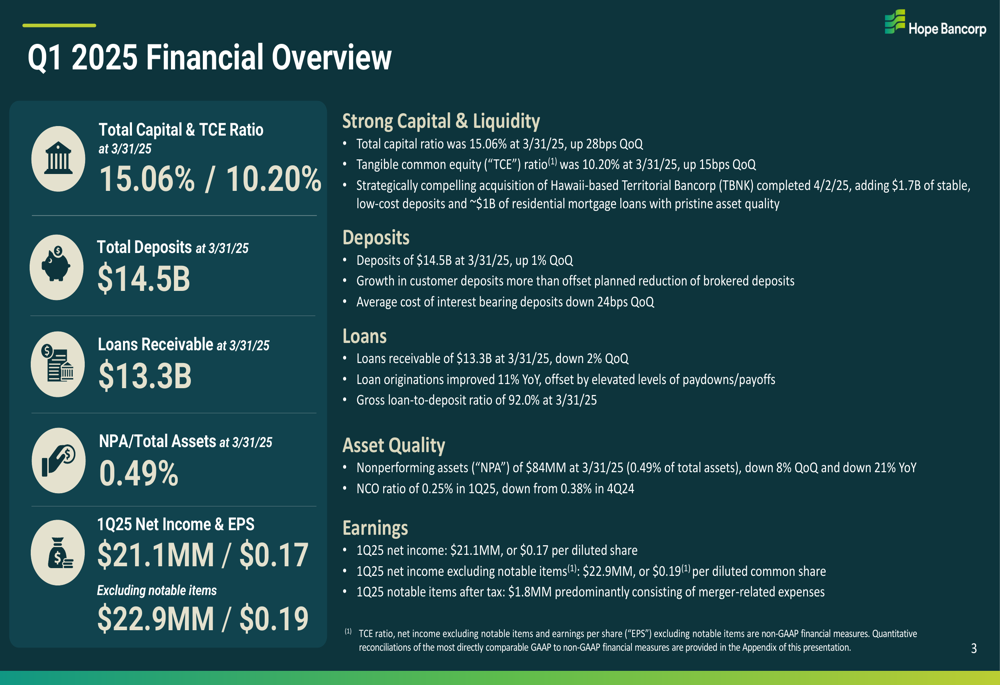

Hope Bancorp, Inc. (NASDAQ:HOPE) presented its first quarter 2025 earnings results on April 22, 2025, revealing a mixed financial performance as the company completed its strategic acquisition of Territorial Bancorp (NASDAQ:TBNK). The bank reported net income of $21.1 million, translating to earnings per share (EPS) of $0.17, or $22.9 million and $0.19 per share when excluding notable items.

The bank’s stock has been under pressure recently, trading at $9.56 as of April 21, 2025, well below its 52-week high of $14.54. In premarket trading following the earnings release, the stock was down 1.67% to $9.40, suggesting investors may have concerns about the company’s performance and outlook.

Quarterly Performance Highlights

Hope Bancorp’s Q1 2025 results showed modest deposit growth offset by a decline in loans. The bank reported total deposits of $14.5 billion as of March 31, 2025, representing a 1% increase quarter-over-quarter. Meanwhile, loans receivable stood at $13.3 billion, down 2% from the previous quarter.

As shown in the following comprehensive financial overview from the company’s presentation:

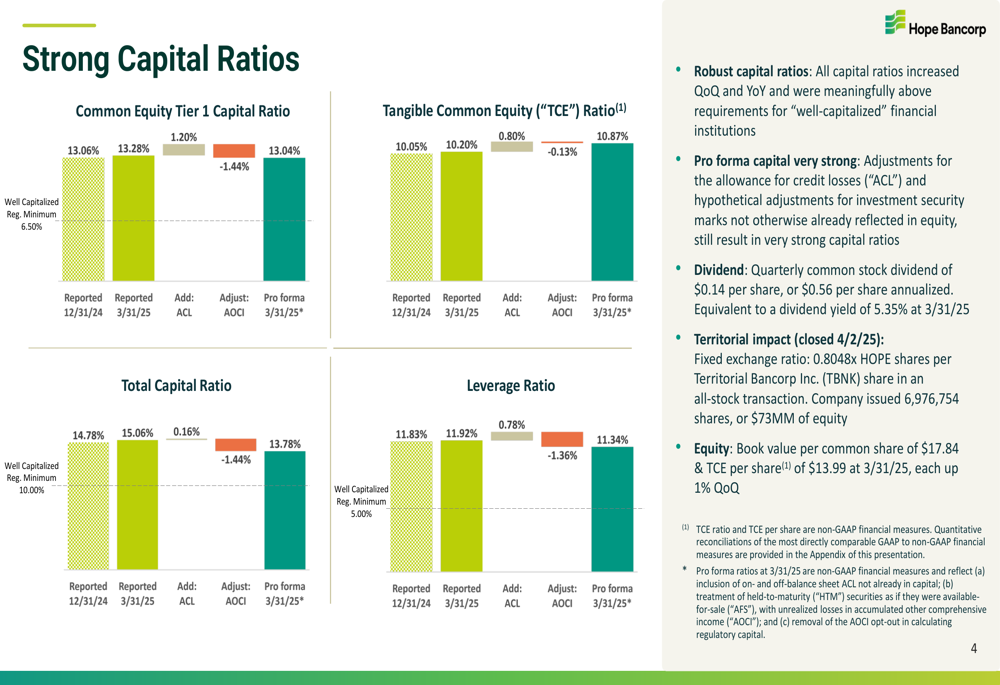

The bank maintained strong capital ratios with a total capital ratio of 15.06% and tangible common equity (TCE) ratio of 10.20% as of March 31, 2025. Asset quality remained stable with nonperforming assets to total assets ratio at 0.49%, reflecting the bank’s prudent risk management approach.

Hope Bancorp’s capital position remains robust, as illustrated in this chart of capital ratios:

The bank’s net interest margin (NIM) showed improvement, increasing by 4 basis points quarter-over-quarter to 2.54%. This was primarily driven by a decrease in the average cost of interest-bearing deposits, which fell by 24 basis points compared to the previous quarter.

Strategic Initiatives

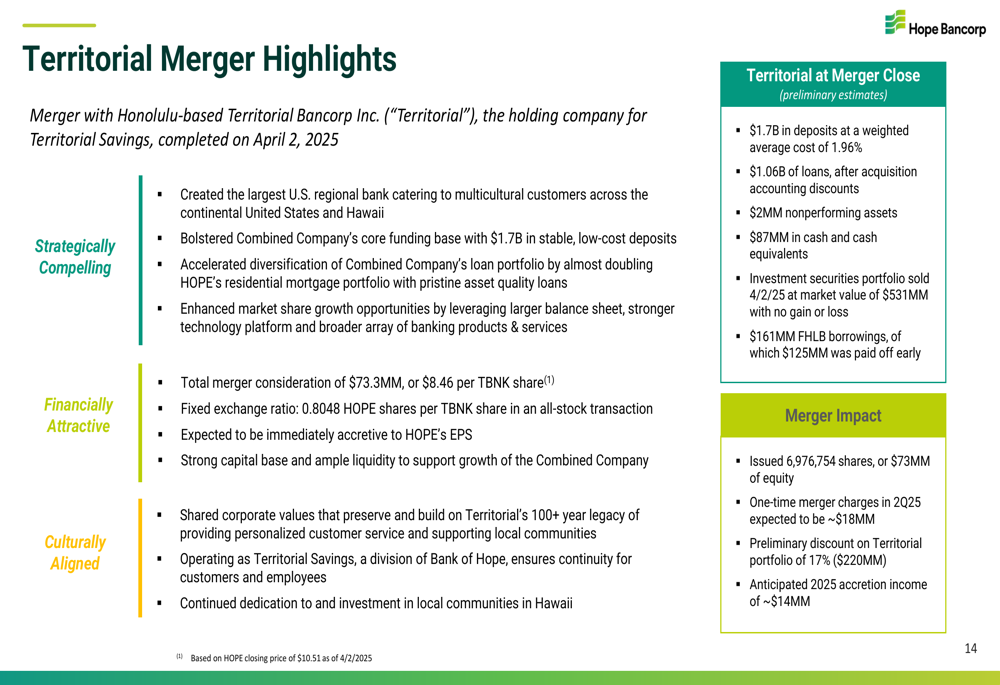

The most significant development in Q1 2025 was the completion of Hope Bancorp’s acquisition of Territorial Bancorp, positioning the combined entity as the largest U.S. regional bank catering to multicultural communities. This strategic transaction is expected to enhance Hope’s deposit base and geographic footprint.

The following slide details the key highlights of the Territorial merger:

The acquisition brings $1.7 billion in deposits at a weighted average cost of 1.96% and $1.06 billion in loans. Management expects the transaction to generate approximately $14 million in accretion income in 2025, though one-time merger charges in Q2 2025 are anticipated to be around $18 million.

Detailed Financial Analysis

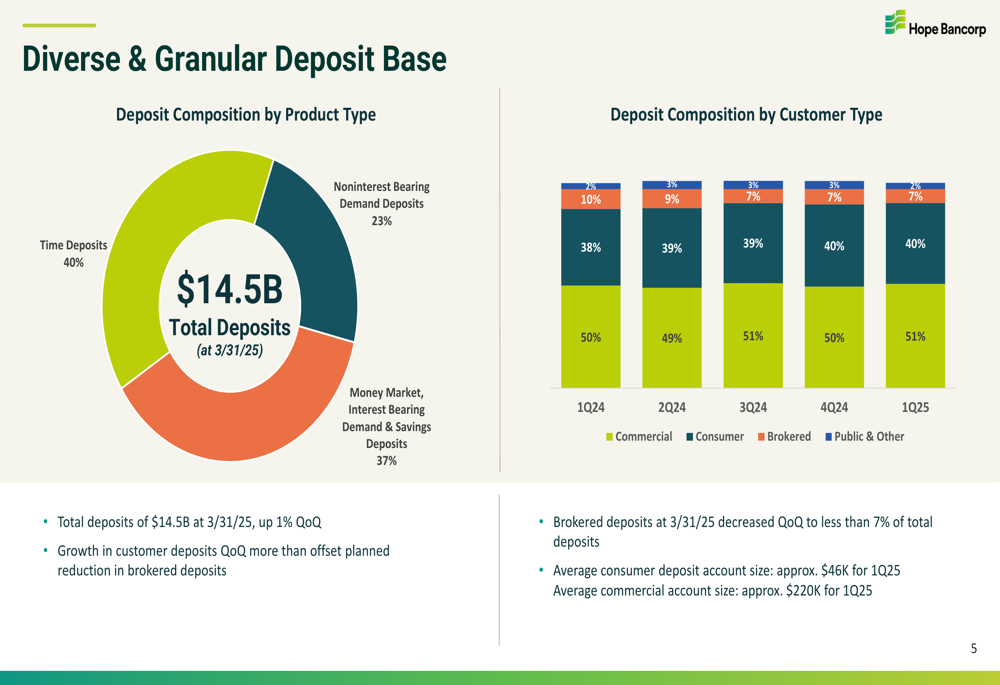

Hope Bancorp maintains a diverse deposit base, with noninterest-bearing demand deposits comprising 23% of total deposits, time deposits at 40%, and money market/interest-bearing demand and savings deposits at 37%. This diversification helps provide stability to the bank’s funding sources.

The composition of the bank’s deposit base is illustrated in the following chart:

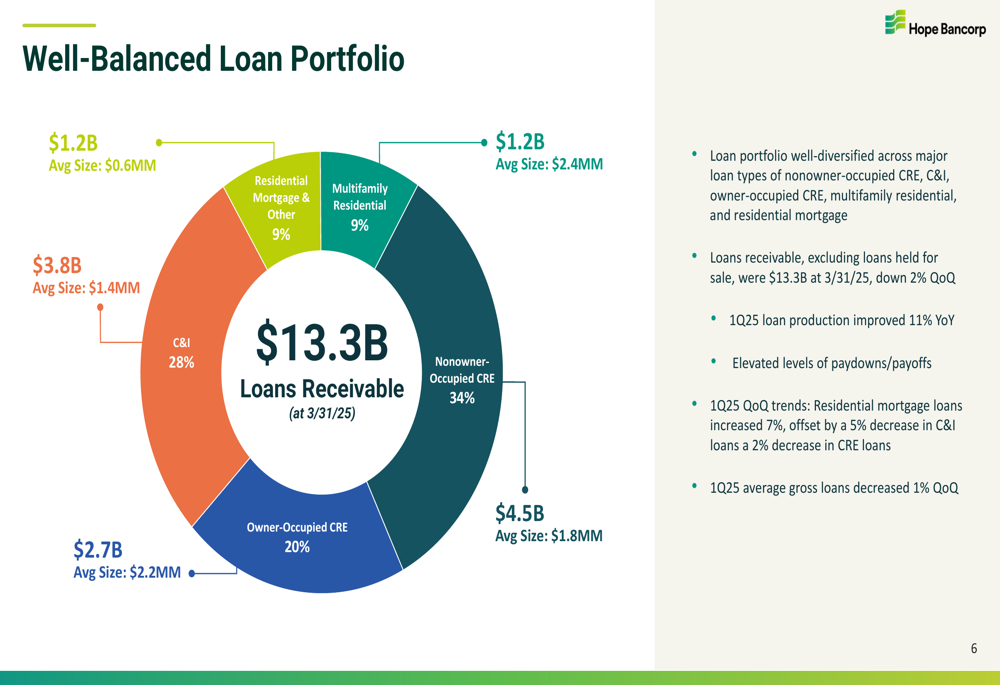

On the lending side, Hope Bancorp has cultivated a well-balanced loan portfolio distributed across various segments. Commercial real estate (CRE) loans, both owner-occupied and nonowner-occupied, represent 54% of the total portfolio, while commercial and industrial (C&I) loans account for 28%.

The bank’s loan portfolio composition is shown in this chart:

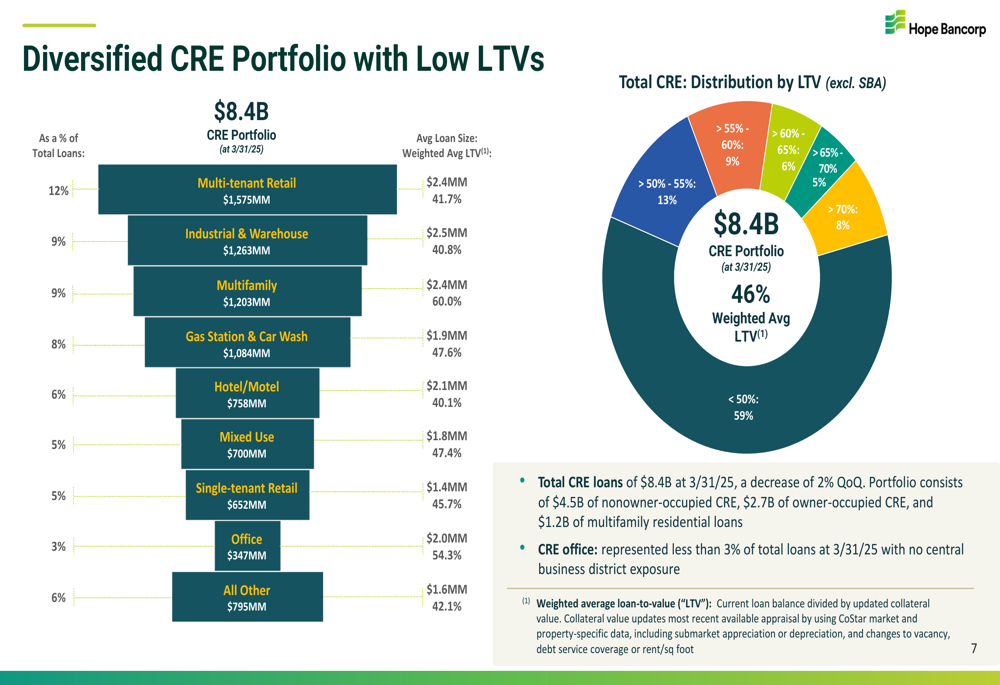

Hope Bancorp’s CRE portfolio is well-diversified by property type with notably low loan-to-value (LTV) ratios, averaging 46%. This conservative approach to lending provides a buffer against potential market downturns.

The diversification of the CRE portfolio by property type is illustrated here:

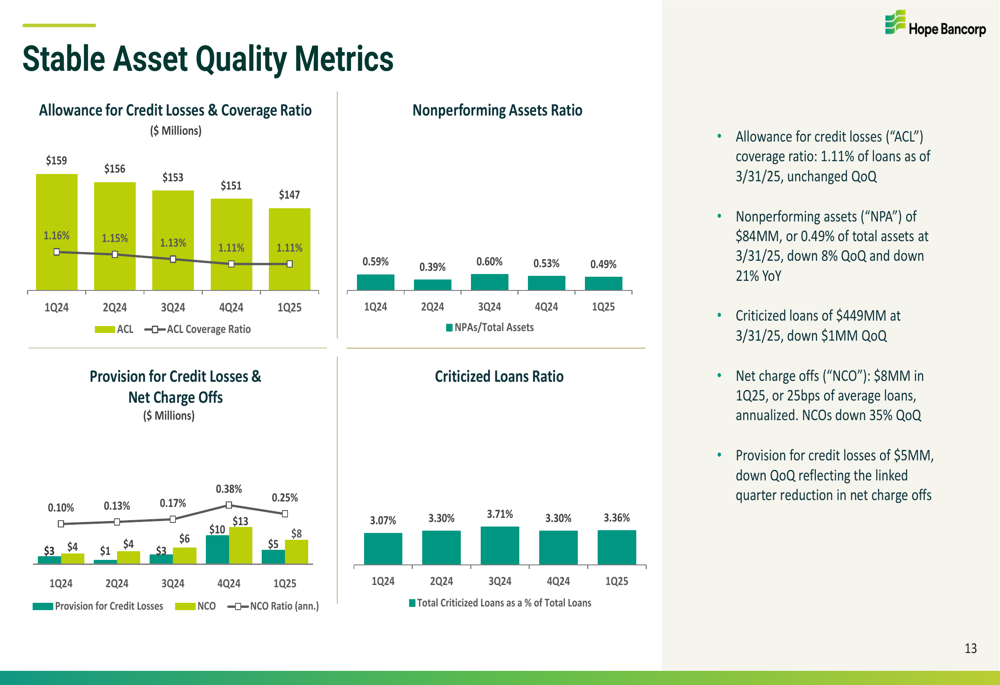

Asset quality metrics remained stable during the quarter. Nonperforming assets decreased to $84 million, or 0.49% of total assets, representing an 8% reduction quarter-over-quarter and a 21% decrease year-over-year. Criticized loans totaled $449 million, down slightly from the previous quarter.

The bank’s asset quality trends are shown in this chart:

Forward-Looking Statements

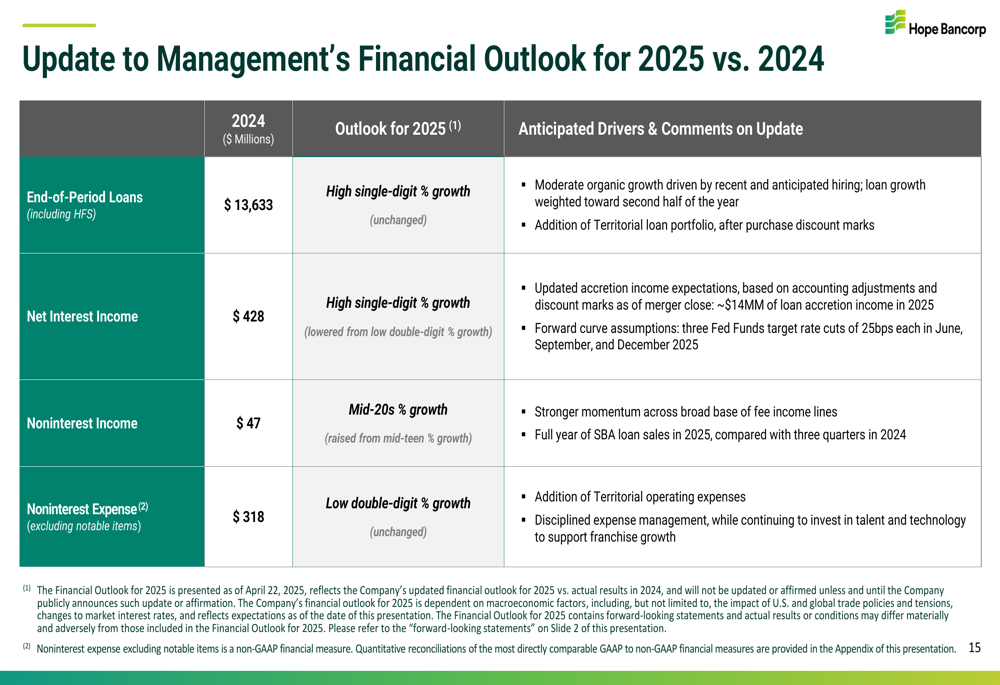

Management has updated its financial outlook for 2025, maintaining expectations for high single-digit percentage growth in end-of-period loans but revising other projections. The outlook for net interest income growth has been lowered from low double-digit percentage to high single-digit percentage, while the forecast for noninterest income growth has been raised from mid-teen percentage to mid-20s percentage.

The updated financial outlook is detailed in this slide:

This revision suggests that while Hope Bancorp expects loan growth to remain consistent with previous projections, the bank anticipates that interest margin pressures may persist. However, the increased outlook for noninterest income indicates confidence in fee-based revenue streams, including SBA (LON:SBA) loan sales, which generated $3.1 million in gains during Q1 2025.

The bank sold $50 million of the guaranteed portion of SBA 7(a) loans during the quarter, slightly higher than the $48 million sold in Q4 2024. This focus on fee income appears to be a strategic priority as the bank navigates the current interest rate environment.

Looking ahead, Hope Bancorp’s management remains focused on integrating the Territorial Bancorp acquisition and leveraging the combined entity’s expanded market presence to drive growth and improve profitability. The bank’s strong capital position provides flexibility to pursue additional strategic initiatives while maintaining its quarterly dividend of $0.14 per share.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.