Canopy Growth stock tumbles after announcing $200 million share sale plan

Introduction & Market Context

Hormel Foods Corporation (NYSE:HRL) shares plunged 8.3% in premarket trading after the company’s third-quarter fiscal 2025 presentation revealed significant profit challenges despite strong sales growth. The food producer reported solid top-line performance across all segments but substantially lowered its full-year earnings guidance due to unexpected commodity cost inflation.

The presentation, delivered on August 28, 2025, showed Hormel achieved volume and sales growth in each of its business segments. However, steep rises in commodity input costs severely pressured bottom-line results, forcing management to revise profit expectations downward for the remainder of the fiscal year.

Quarterly Performance Highlights

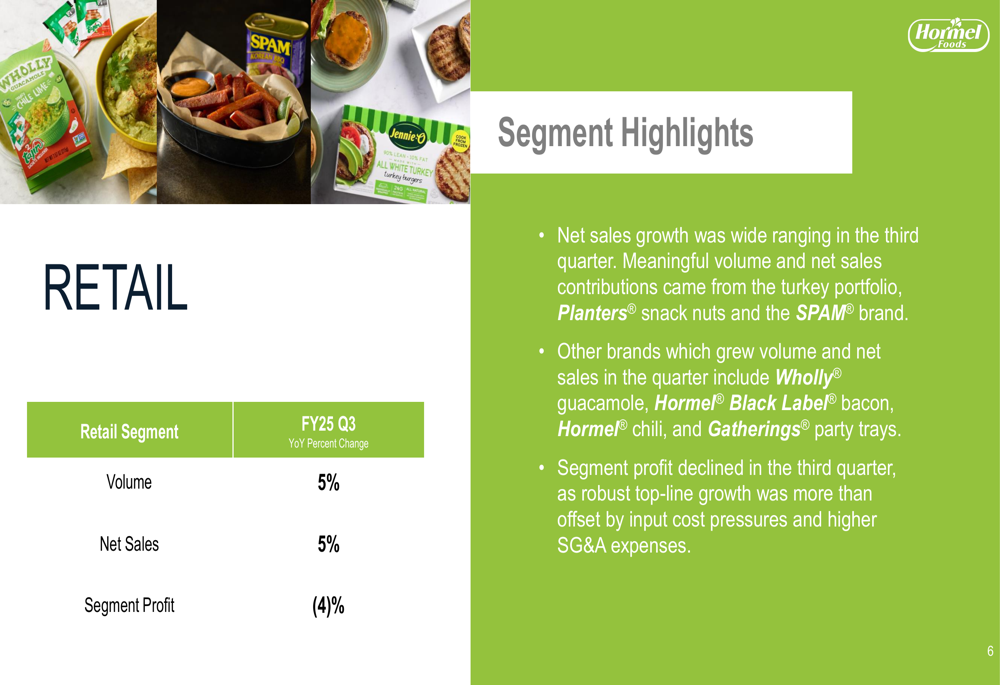

Hormel’s retail segment posted impressive results with both volume and net sales increasing by 5% compared to the prior year. However, segment profit decreased by 4%, primarily due to input cost pressures and SG&A expenses. Key growth drivers included the Jennie-O turkey portfolio, Planters snack nuts, and SPAM products.

As shown in the following retail segment performance overview:

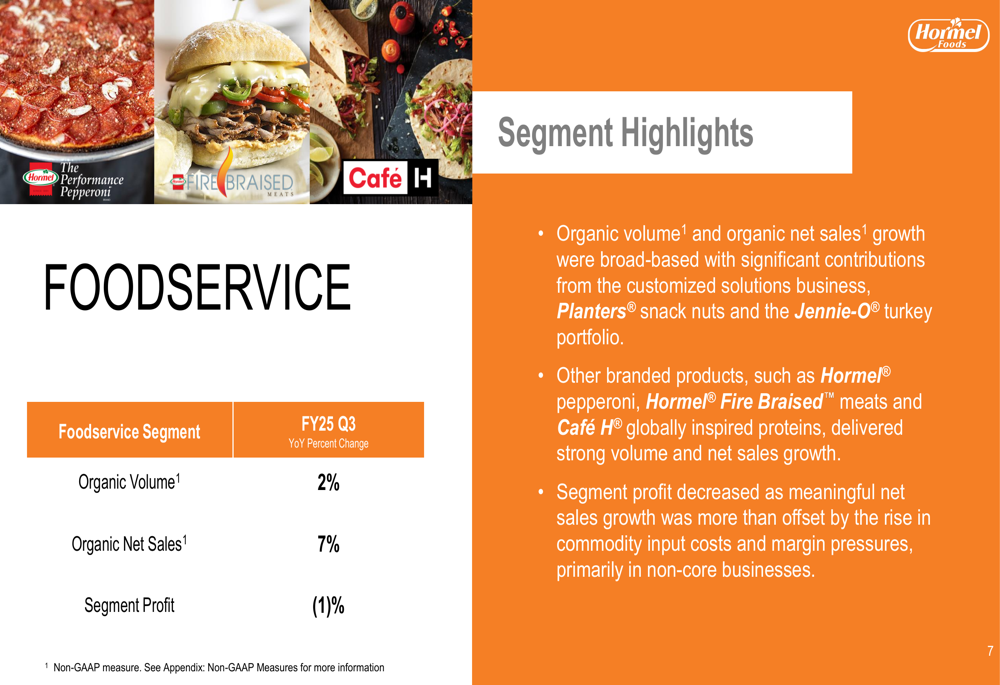

The foodservice segment delivered 2% organic volume growth and 7% organic net sales growth, with segment profit declining slightly by 1%. Growth was broad-based with significant contributions from customized solutions, Planters snack nuts, and the Jennie-O turkey portfolio.

The foodservice performance highlights included strong showings from several key brands:

International operations showed the strongest volume growth at 8%, with net sales increasing by 6%. However, this segment experienced the most significant profit decline at 13%, which the company attributed to competitive pressures in Brazil and lower pork offal margins, despite growth in the China market and robust SPAM exports.

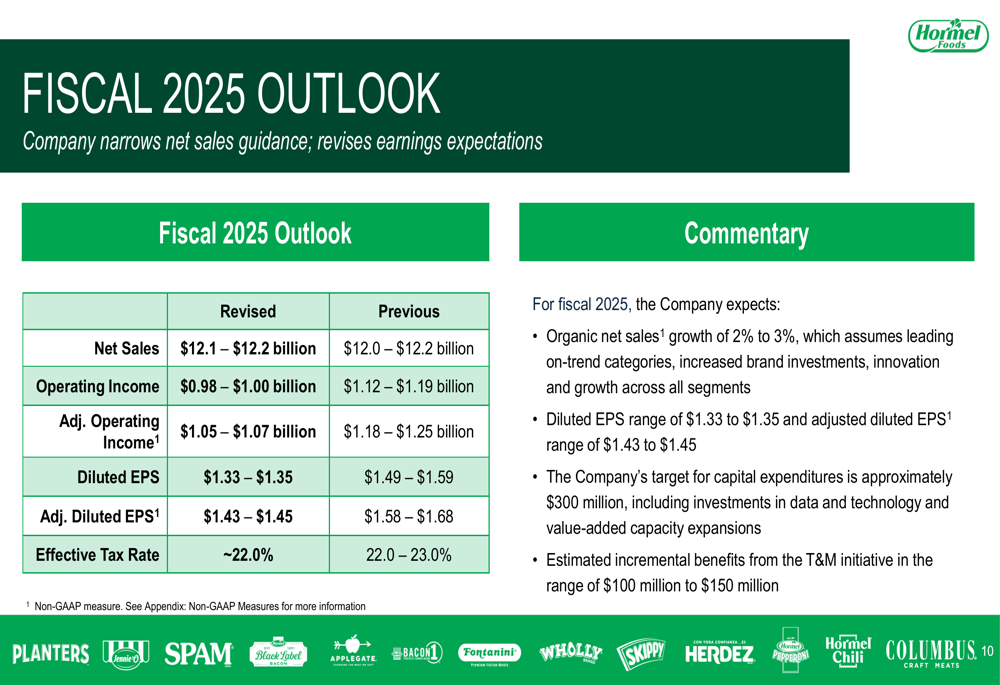

Revised Outlook

In a significant update, Hormel revised its full-year guidance, maintaining its sales outlook but substantially lowering profit expectations. The company now expects adjusted diluted earnings per share of $1.43-$1.45, down from the previous guidance of $1.58-$1.68 provided during its Q2 earnings call.

The following chart clearly illustrates the revised outlook compared to previous guidance:

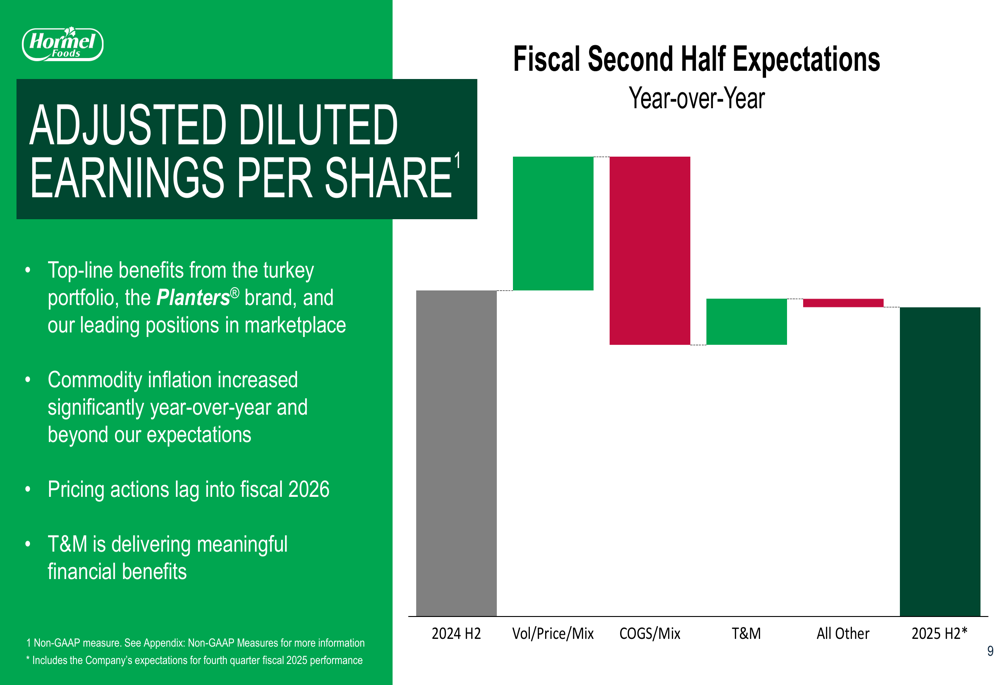

Management explained that commodity inflation increased significantly beyond expectations, with pricing actions expected to lag into fiscal 2026. This timing gap between cost increases and pricing adjustments is the primary driver behind the reduced profit outlook.

The factors affecting adjusted diluted earnings per share are illustrated in this bridge analysis:

Strategic Initiatives

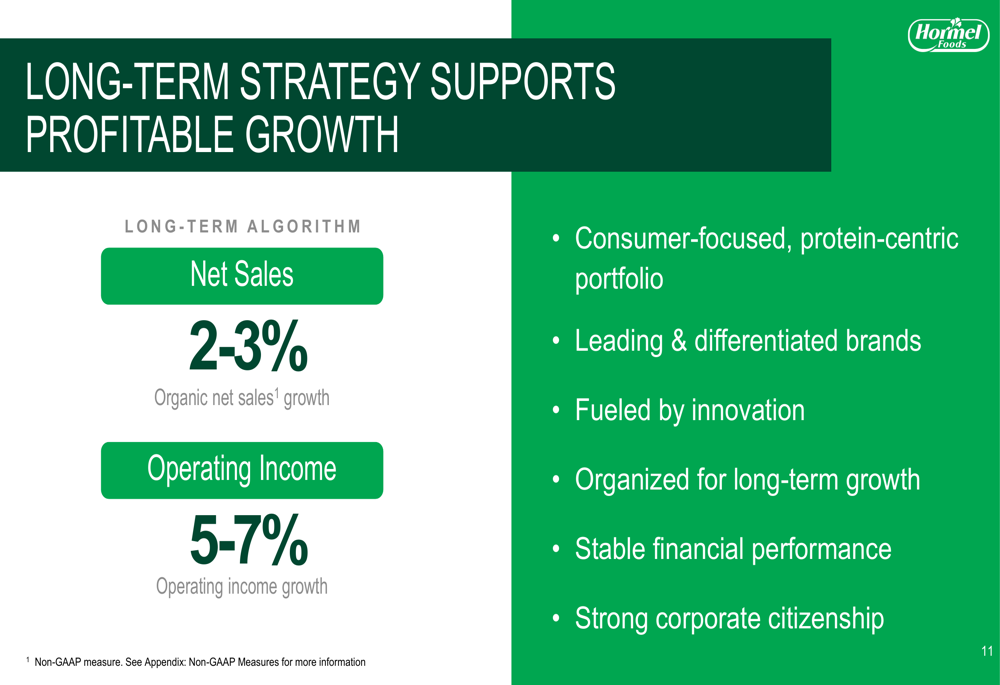

Despite near-term challenges, Hormel emphasized its Transform and Modernize (T&M) initiative is delivering meaningful financial benefits, estimated between $100-150 million for the fiscal year. The company continues to focus on its five strategic priorities: driving retail growth, expanding foodservice leadership, developing global presence, executing its entertaining and snacking vision, and transforming operations.

The company’s long-term strategy remains focused on profitable growth, as outlined in this strategic framework:

Dividend Performance

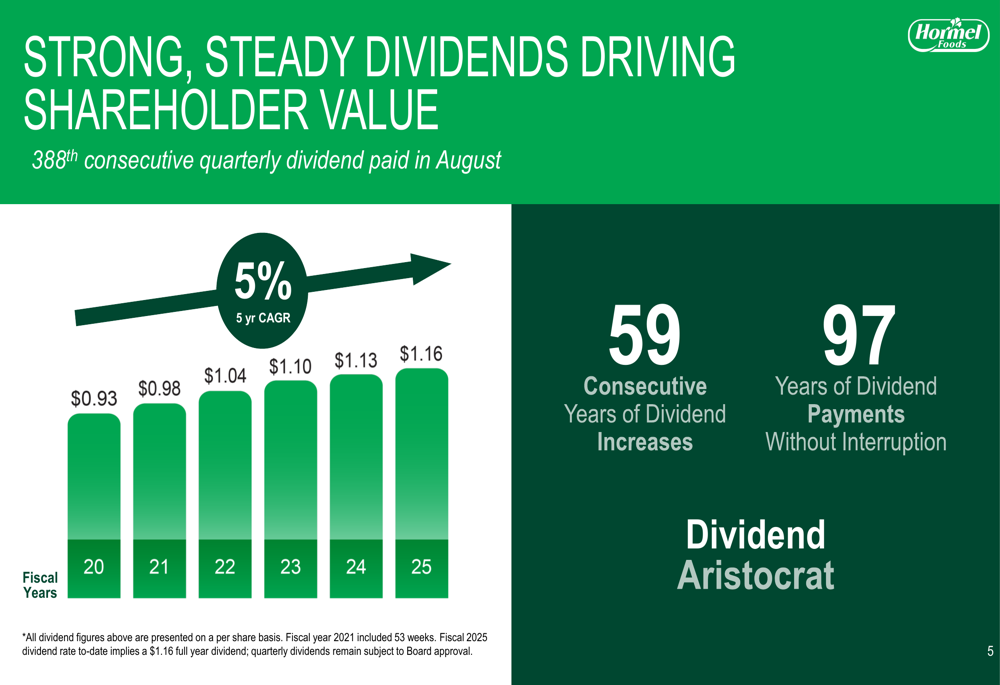

A bright spot in Hormel’s presentation was its continued dividend strength. The company paid its 388th consecutive quarterly dividend in August, marking 59 consecutive years of dividend increases and 97 years of uninterrupted dividend payments. This performance maintains Hormel’s status as a Dividend Aristocrat.

The following chart demonstrates Hormel’s consistent dividend growth trajectory:

Forward-Looking Statements

Looking ahead, Hormel maintained its organic net sales growth target of 2-3% for fiscal 2025, despite the profit challenges. Capital expenditures are expected to be approximately $300 million, supporting the company’s long-term growth strategy.

Management reaffirmed its long-term algorithm of 2-3% organic net sales growth and 5-7% operating income growth, suggesting confidence that current commodity pressures are temporary rather than structural. The company’s leadership emphasized they remain aligned on a clear mission of profitable growth, despite the near-term headwinds.

The significant market reaction to the presentation highlights investor concerns about Hormel’s ability to manage inflationary pressures and maintain margins in a challenging cost environment. While the company’s sales performance demonstrates continued consumer demand for its products, the profit outlook suggests a potentially extended period of margin compression as the company works to implement pricing actions to offset the higher input costs.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.