Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Hudbay Minerals Inc . (NYSE:HBM) released its Q1 2025 results presentation on May 12, 2025, revealing record quarterly adjusted EBITDA and exceptionally low cash costs across its operations. The company’s stock responded positively, rising 8.56% on the day of the announcement, reflecting investor confidence in the company’s operational performance and growth strategy.

The diversified miner, with operations across Peru, Manitoba, and British Columbia, continues to benefit from its exposure to copper and gold prices while maintaining a disciplined approach to cost management and capital allocation.

Quarterly Performance Highlights

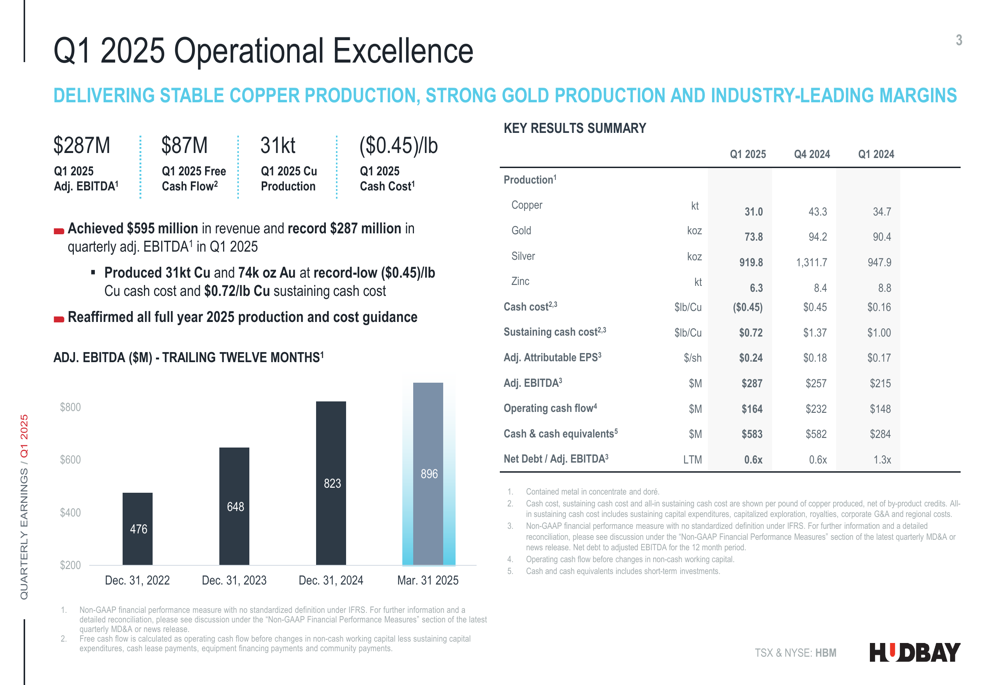

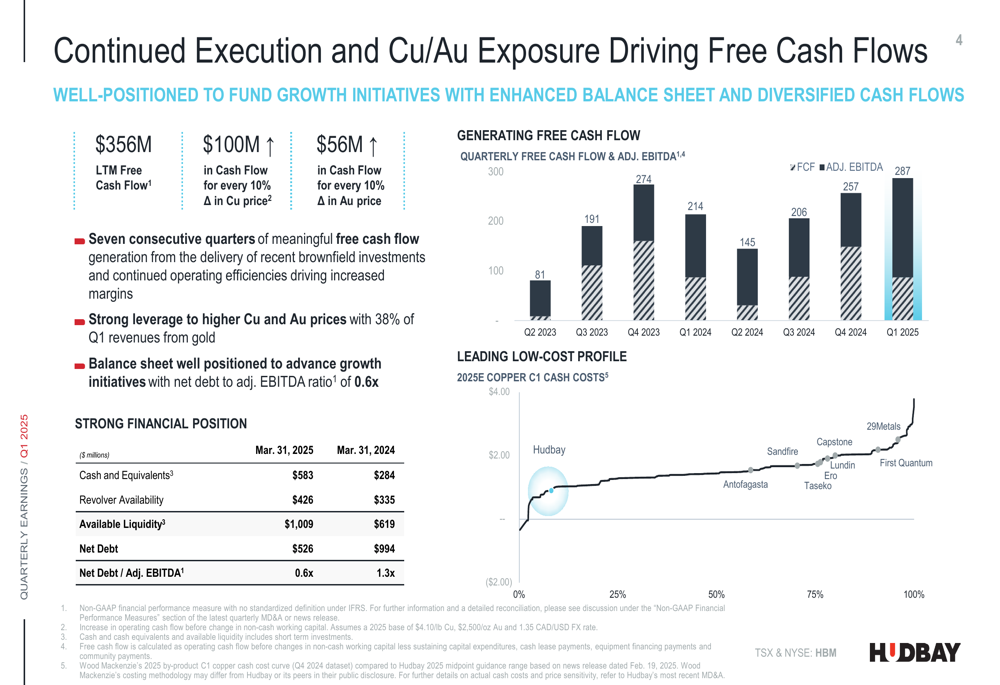

Hudbay delivered impressive financial and operational results in the first quarter of 2025, generating $595 million in revenue and a record $287 million in quarterly adjusted EBITDA. The company produced 31,000 tonnes of copper and 73,800 ounces of gold at a record-low cash cost of ($0.45) per pound of copper, demonstrating exceptional operational efficiency.

Free cash flow reached $87 million, marking the seventh consecutive quarter of meaningful free cash flow generation. The company reaffirmed its full-year 2025 production and cost guidance across all operations.

As shown in the following chart of trailing twelve months adjusted EBITDA, Hudbay has demonstrated consistent growth in this key financial metric:

Regional Operations Analysis

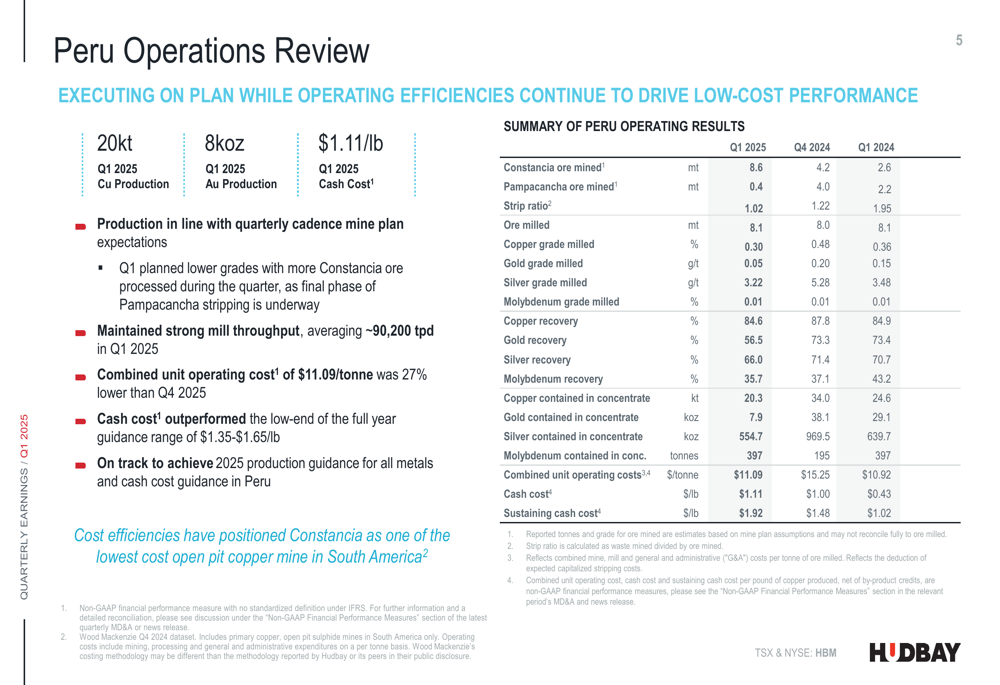

Peru Operations

Hudbay’s Peruvian operations produced 20,300 tonnes of copper and 7,900 ounces of gold in Q1 2025 at a cash cost of $1.11 per pound. Production aligned with the quarterly cadence mine plan expectations, with Q1 featuring lower grades as more Constancia ore was processed during the final phase of Pampacancha stripping.

The operation maintained strong mill throughput, averaging approximately 90,200 tonnes per day. Combined unit operating cost of $11.09 per tonne was 27% lower than Q4 2024, positioning Constancia as one of the lowest-cost open pit copper mines in South America.

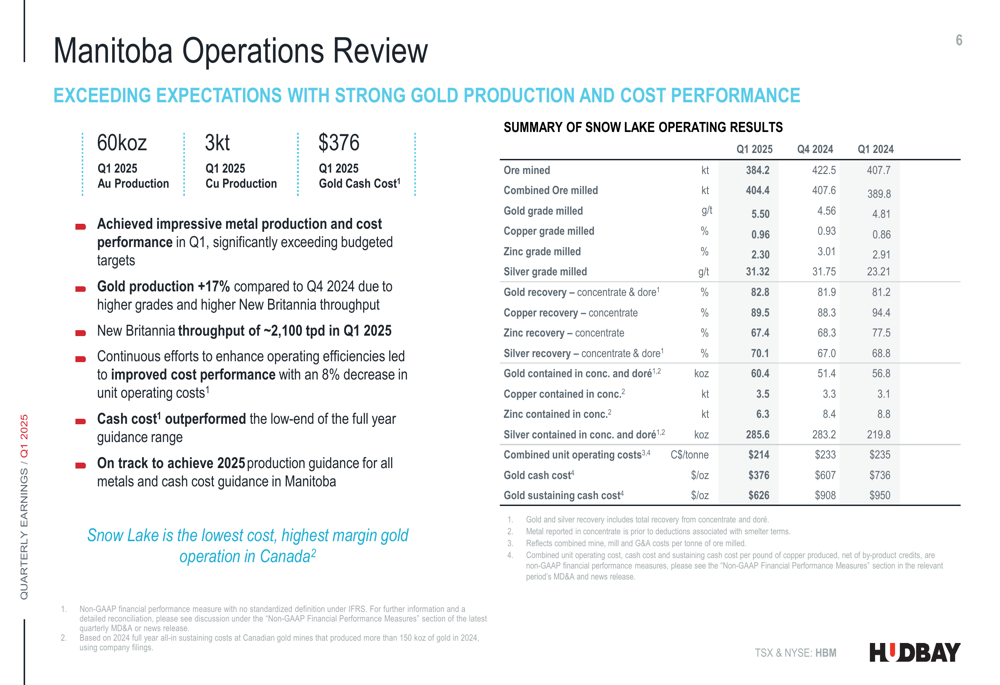

Manitoba Operations

The Manitoba operations delivered exceptional results with 60,400 ounces of gold production and 3,500 tonnes of copper production at a gold cash cost of $376 per ounce. Gold production increased 17% compared to Q4 2024 due to higher grades and increased throughput at the New Britannia mill.

According to the company, Snow Lake represents the lowest cost, highest margin gold operation in Canada, a claim supported by the impressive cost metrics presented.

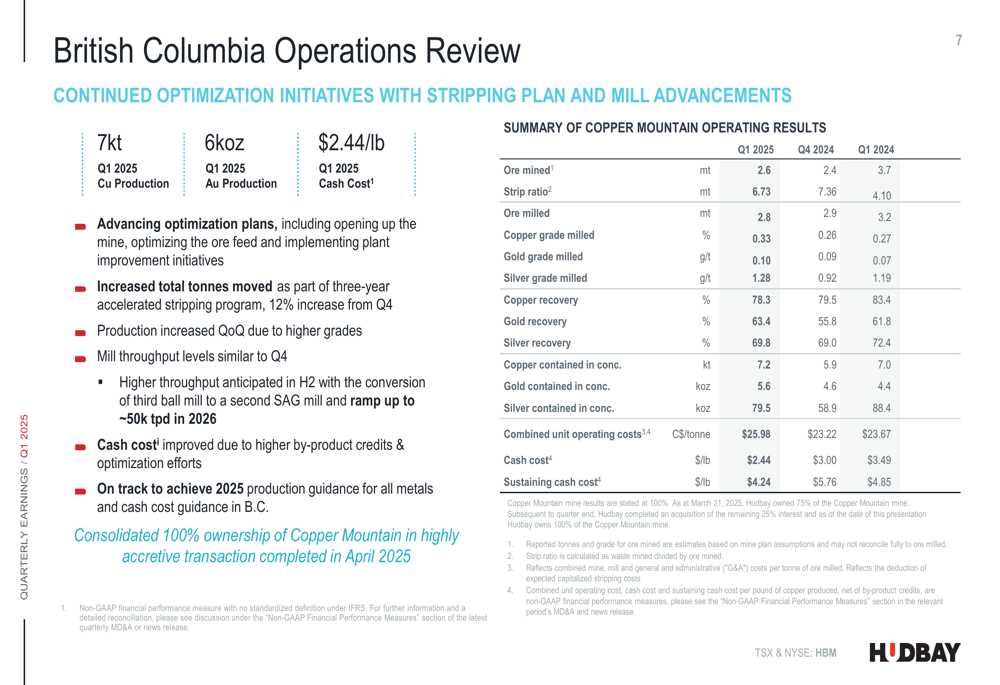

British Columbia Operations

In British Columbia, Hudbay’s Copper Mountain mine produced 7,200 tonnes of copper and 5,600 ounces of gold at a cash cost of $2.44 per pound. The company is advancing optimization plans for the operation, including opening up the mine, optimizing ore feed, and implementing plant improvement initiatives.

Notably, Hudbay consolidated 100% ownership of Copper Mountain in what it described as a "highly accretive transaction" completed in April 2025.

Growth Projects and Future Outlook

Hudbay’s three-year production outlook shows strong and stable output across its portfolio, with a three-year average copper production of 144,000 tonnes and gold production of 253,000 ounces. The company’s production profile is well-diversified across its three operating regions.

The flagship growth project, Copper World, represents a significant expansion opportunity. Described as the "Highest Grade Open Pit Copper Project in Americas," the project is expected to increase Hudbay’s copper production by more than 50%. Located on private land and fully permitted, Copper World is designed to produce 85,000 tonnes of copper annually over a 20-year mine life.

The project economics appear robust, with an estimated NPV of $1.1 billion and an IRR of 19% at conservative copper price assumptions of $3.75 per pound. The project will produce copper cathode, contributing to domestic U.S. supply chains while reducing greenhouse gas emissions compared to traditional concentrate shipping and smelting.

Financial Position and Market Sensitivity

Hudbay maintains a strong financial position with $583 million in cash and equivalents and total available liquidity of over $1 billion. The company’s net debt stands at $526 million, representing a net debt to adjusted EBITDA ratio of just 0.6x, positioning the balance sheet well to advance growth initiatives.

The company has significant leverage to commodity prices, with every 10% increase in copper prices generating an additional $100 million in cash flow, while a similar percentage increase in gold prices adds $56 million. This sensitivity highlights Hudbay’s attractive position in a potentially strengthening metals market.

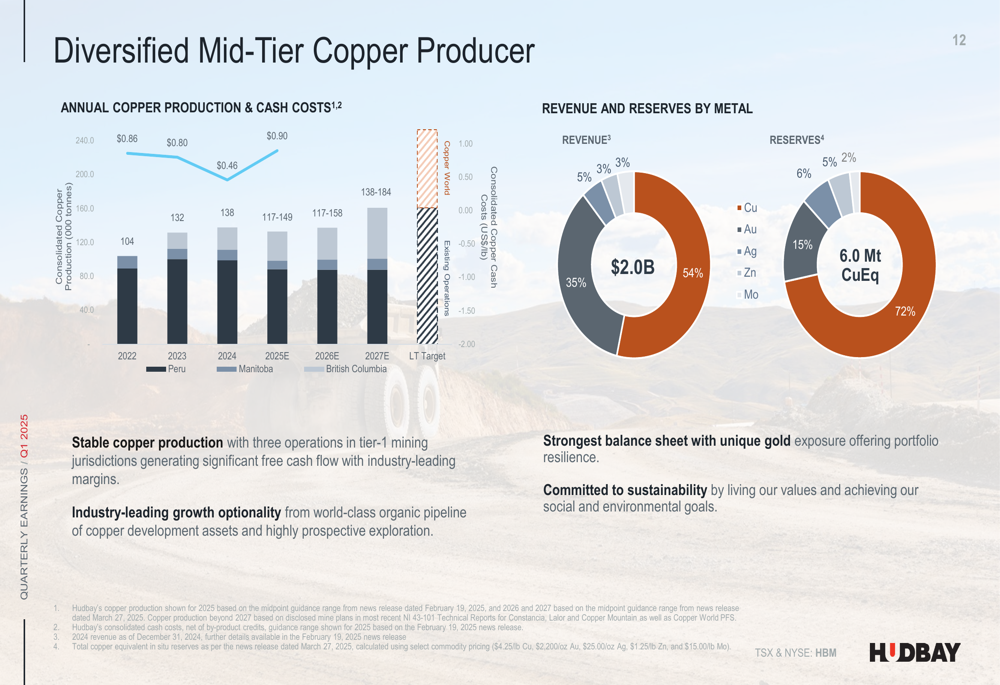

As illustrated in the following slide, Hudbay’s copper cash costs position it favorably on the global cost curve, providing strong margins even in a more challenging price environment:

Looking ahead, Hudbay is positioning itself as a diversified mid-tier copper producer with stable production from three operations in tier-1 mining jurisdictions. The company’s revenue mix currently shows 55% from copper and 35% from gold, while its reserves are predominantly copper-focused at 72%.

In conclusion, Hudbay’s Q1 2025 results presentation demonstrates strong operational execution across its portfolio, record financial performance, and a clear growth strategy centered on the Copper World project. With a solid balance sheet, low operating costs, and significant leverage to copper and gold prices, the company appears well-positioned to deliver value to shareholders in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.