e.l.f. Beauty stock plummets 20% as revenue and guidance fall short of expectations

Introduction & Market Context

IDACORP, Inc. (NYSE:IDA) presented its third-quarter 2025 earnings results on October 30, showing solid financial performance and raising its full-year guidance despite some operational challenges. The Idaho-based utility company reported earnings that exceeded analyst expectations, though its stock dipped 2% in aftermarket trading to close at $133.80.

The company continues to benefit from robust customer growth in its service territory, which includes major industrial customers like Meta, Micron, and Chobani. This growth is driving significant infrastructure investments as IDACORP positions itself to meet increasing energy demands in the coming years.

Quarterly Performance Highlights

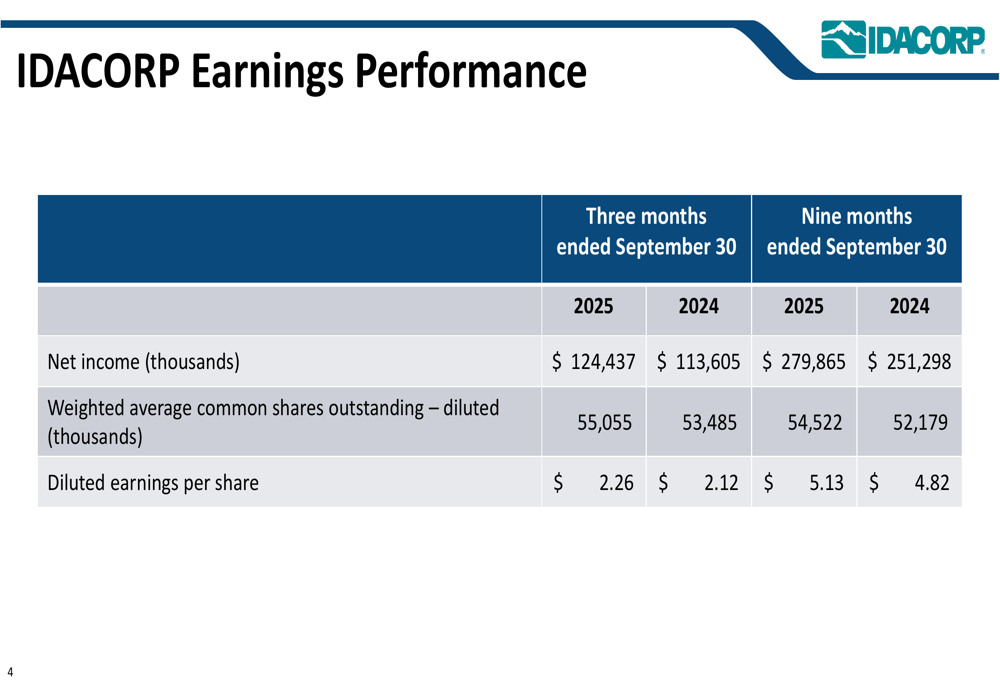

IDACORP reported third-quarter 2025 net income of $124.4 million, or $2.26 per diluted share, compared to $113.6 million, or $2.12 per diluted share, for the same period in 2024. This represents a 6.6% increase in earnings per share, slightly exceeding analysts’ expectations of $2.25.

For the nine months ended September 30, 2025, IDACORP reported net income of $279.9 million, or $5.13 per diluted share, up from $251.3 million, or $4.82 per diluted share, for the same period in 2024.

As shown in the following earnings performance table:

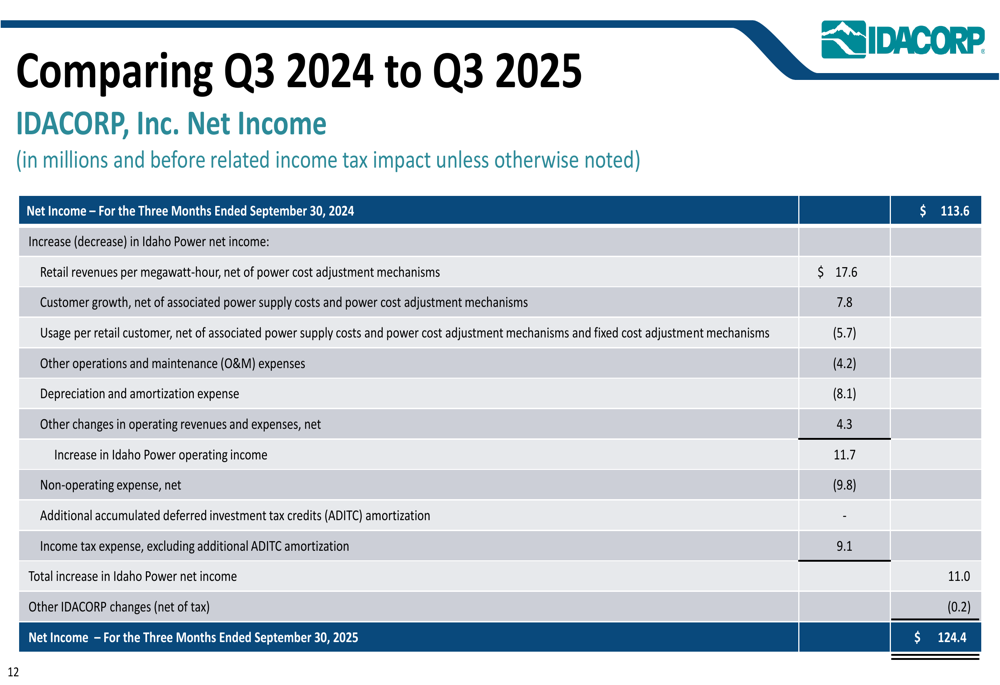

The company’s performance was primarily driven by increased retail revenues per megawatt-hour, which contributed $17.6 million to the bottom line, along with customer growth adding another $7.8 million. Decreases in operations and maintenance expenses and non-operating expenses further boosted results.

The following chart breaks down the factors contributing to IDACORP’s improved quarterly performance:

Strategic Growth Initiatives

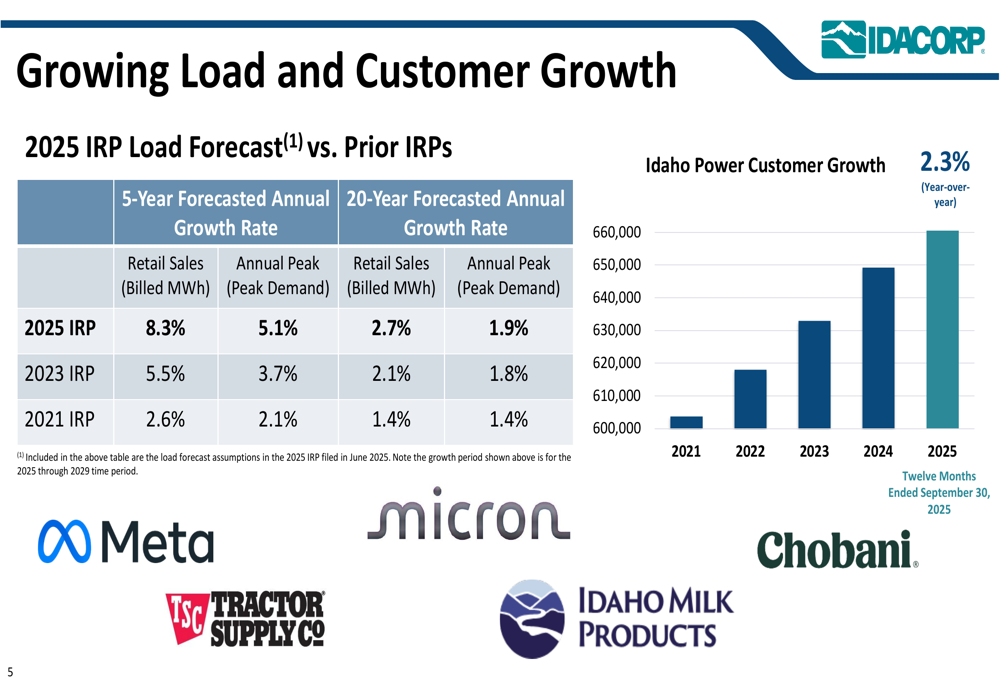

IDACORP is experiencing significant customer growth, with its customer base increasing by 2.3% year-over-year. The company now serves approximately 655,000 customers, up from around 605,000 in 2021. This growth is driving substantial increases in load forecasts compared to previous years.

The company’s latest Integrated Resource Plan (IRP) projects a 5-year forecasted annual growth rate of 8.3% for retail sales and 5.1% for peak demand, significantly higher than previous forecasts. This accelerated growth is illustrated in the following chart:

To meet this growing demand, IDACORP is making substantial investments in infrastructure. A key project is the Boardman-to-Hemingway (B2H) transmission line, which broke ground in June 2025 and is expected to be in service by late 2027. Idaho Power owns approximately 45% of this project.

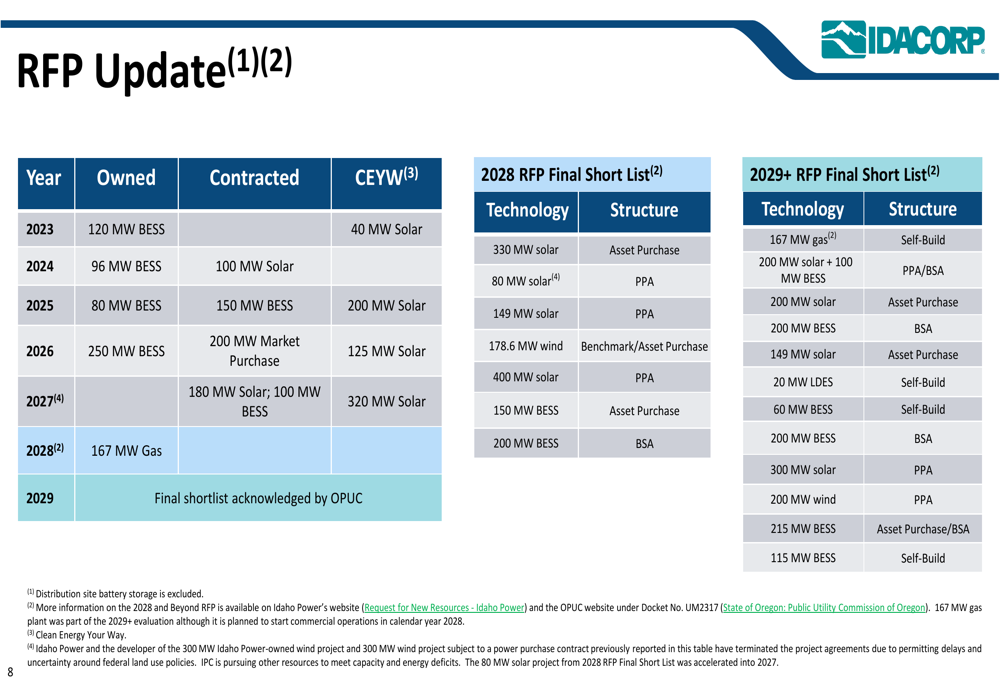

Additionally, the company is diversifying its energy portfolio through significant investments in battery energy storage systems (BESS) and solar power, as outlined in its resource planning update. IDACORP is also expanding its Bennett Mountain gas-fired plant with a 167-megawatt addition.

Financial Outlook & Guidance

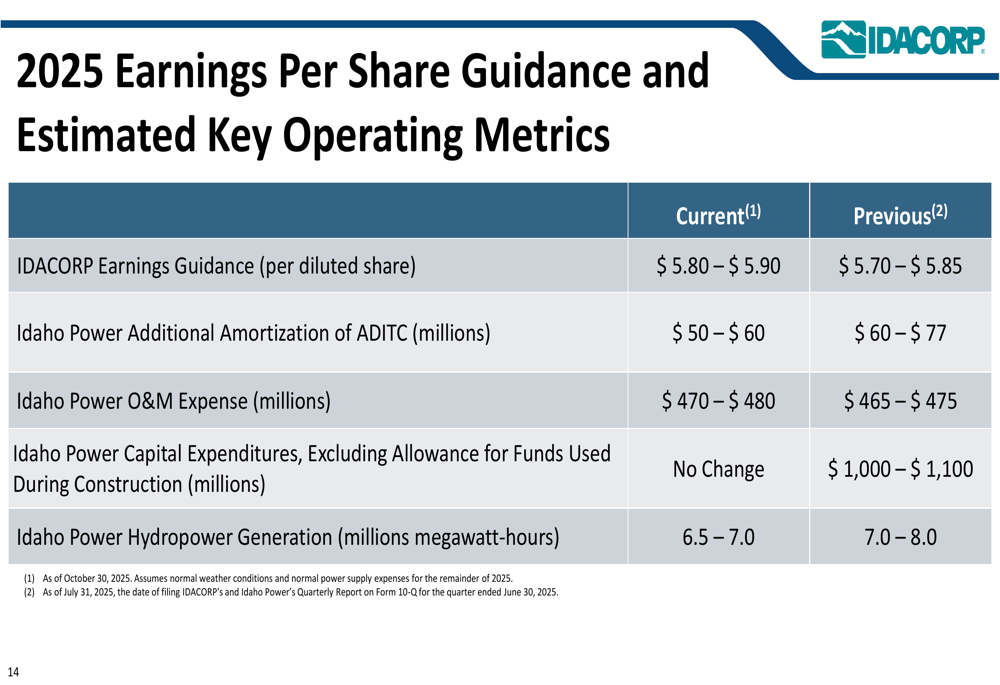

Based on strong year-to-date performance, IDACORP has raised its full-year 2025 earnings guidance to $5.80-$5.90 per diluted share, up from the previous range of $5.70-$5.85. However, the company has also increased its operations and maintenance expense guidance to $470-$480 million, up from $465-$475 million previously.

The company also revised its hydropower generation forecast downward to 6.5-7.0 million megawatt-hours from the previous 7.0-8.0 million, potentially reflecting operational challenges or changing water conditions.

The updated guidance and key metrics are presented in the following table:

IDACORP maintains a strong liquidity position, with $464.1 million in net cash provided by operating activities for the first nine months of 2025, slightly up from $458.0 million for the same period in 2024. The company has $100 million available under its credit facility, while Idaho Power has $400 million available.

Rate Case Settlement & Competitive Position

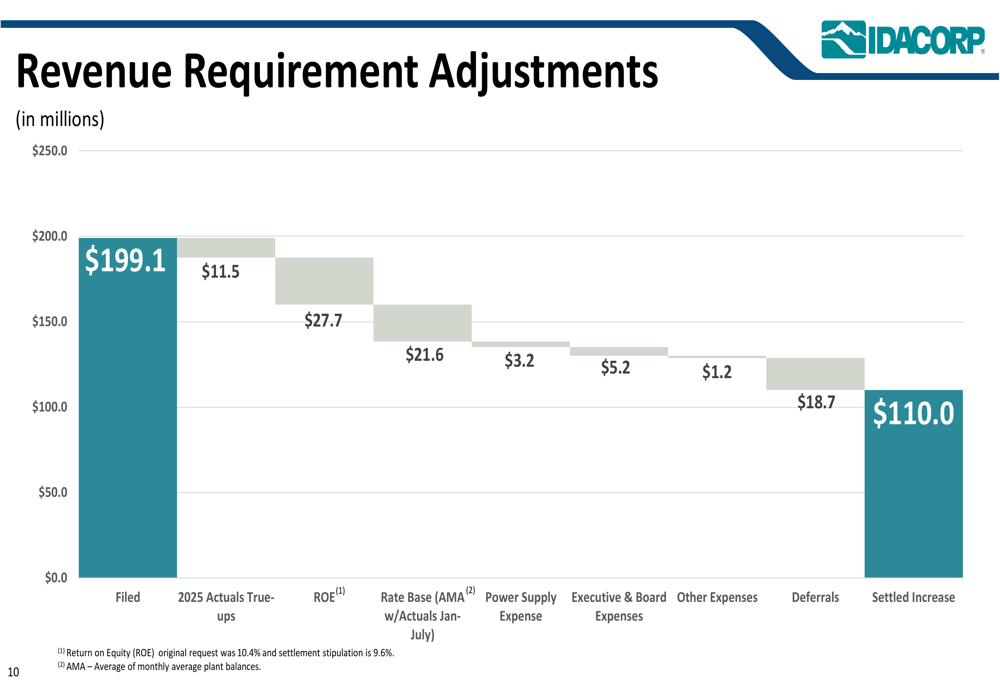

IDACORP recently reached a settlement in its Idaho General Rate Case, which is pending approval by the Idaho Public Utilities Commission. The settlement provides for a $110 million increase (7.48%) in annual Idaho-jurisdictional revenue, with rates expected to become effective January 1, 2026.

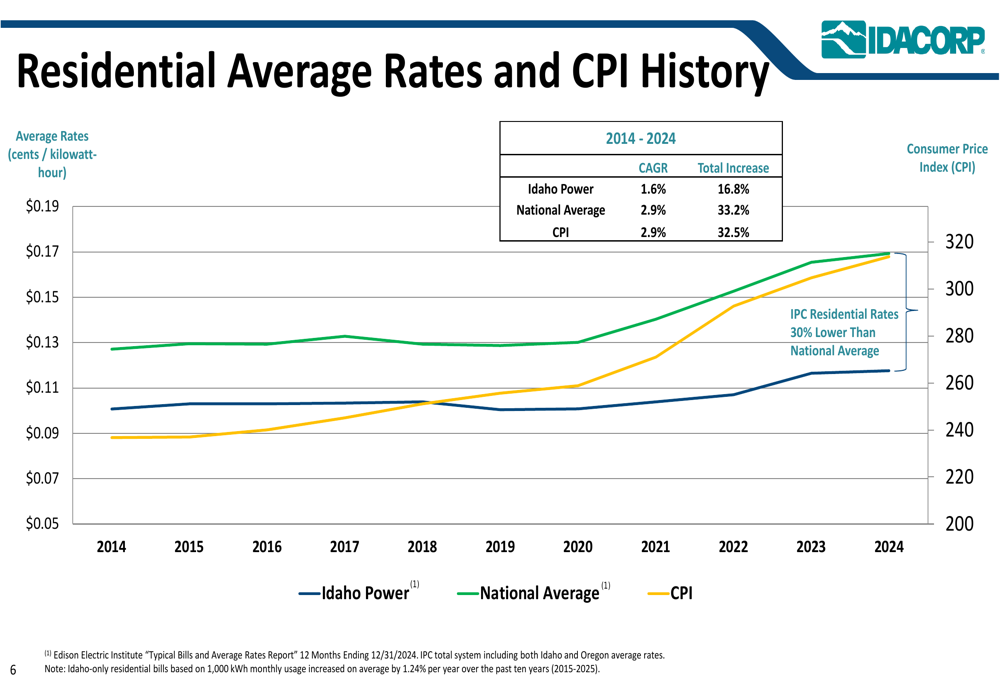

Despite this increase, IDACORP maintains a competitive advantage with residential rates that are 30% lower than the national average. Over the past decade (2014-2024), the company’s average rate increase was just 1.6% annually (16.8% total), compared to the national average of 2.9% annually (33.2% total) and CPI growth of 2.9% annually (32.5% total).

This favorable rate position is illustrated in the following chart:

The details of the rate case settlement are further broken down in this revenue requirement adjustments chart:

Market Reaction & Analyst Perspectives

Despite the positive earnings report and raised guidance, IDACORP’s stock fell 2% in aftermarket trading following the earnings release. This decline may reflect investor concerns about increased operational costs, as evidenced by the higher O&M expense guidance, or uncertainty following the cancellation of the Jackalope Wind Project mentioned during the earnings call.

During the call, CEO Lisa Grow emphasized the company’s strategic planning to meet growing demand, stating, "We’re in a continuous state of planning and execution to affordably serve the growing demand with a reliable mix of generation resources." She also highlighted the importance of maintaining financial health during this period of expansion.

Analysts have focused their questions on IDACORP’s strategy following the Jackalope Wind Project’s cancellation and the company’s plans to meet accelerating customer growth. The company’s ability to execute its ambitious infrastructure projects while maintaining its competitive rate advantage will likely remain a key focus for investors in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.